South Africa has been saved

Cover image by: Jaime Austin

After recording one of its deepest contractions (–6.4%)1 in 2020, South Africa’s real GDP growth bounced back to 4.9% in 20212—driven primarily by a combination of base effects, strong commodity prices, and the gradual reopening of the economy after strict COVID-19 regulations and mobility restrictions. As reassuring as this turnaround is, economic activity continues to lag prepandemic levels—the economic output during the last quarter of 2021 was on par with the output seen in Q3 2017.3 Furthermore, a more sustained economic recovery remains under risk, unless proposed structural reforms are put in place.

Real GDP growth is forecast to remain below 2% in 2023 and 2024, a rate that is not sufficient to address the country’s growing socioeconomic needs. For example, in Q3 2021, the official unemployment rate rose to 34.9% and the expanded definition—which includes discouraged work-seekers that are no longer searching for job opportunities—reached 46.6%.4 What South Africa needs now is a sustained period of above 3% growth to tackle these challenges, rather than returning to the ‘growth rut’ that the country has been stuck in since 2008.

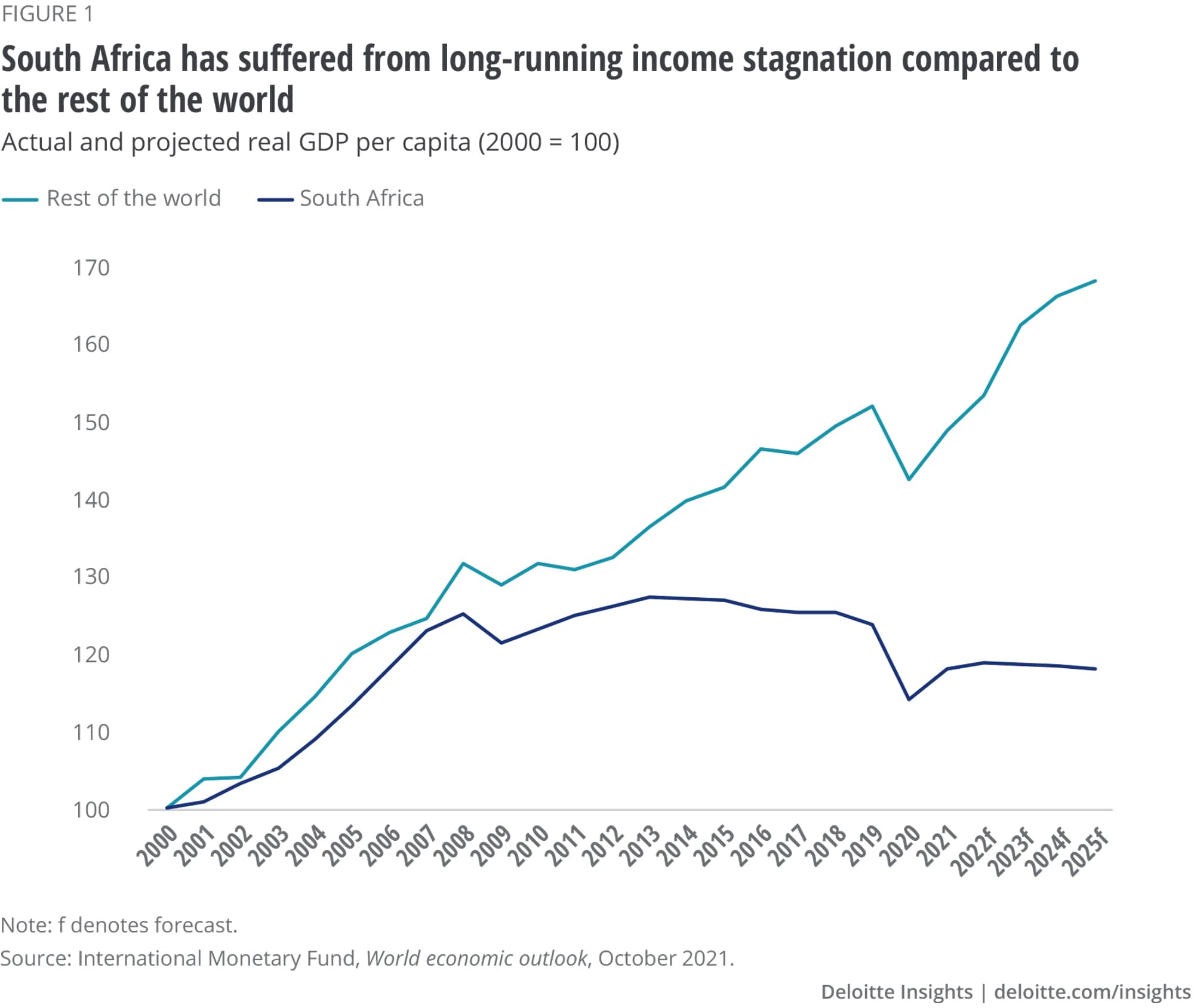

Despite the economic revival of 2021, South African consumers continue to be under severe pressure. Income per capita growth has been flat since 2010 and on a decline since 2015 as economic growth hasn’t been able to keep up with population growth.5 Unless the country moves into a higher and more sustainable growth gear, South Africans will continue to be worse off over the next few years.

This was acknowledged in the 2022 budget speech read by Finance Minister Enoch Godongwana on 23 February 2022 as he looked at ways to keep money in South Africans’ pockets. He also looked to respond to the immediate needs of lower-income households. Relief included adjusting tax brackets for inflation and not raising personal income taxes, not hiking fuel- and transport-related levies, extending the COVID-19 social relief grant for another 12 months, and supporting employment creation through a tax incentive expansion.6

The limited escalation in spending was made possible in part by the boom in commodity prices experienced through much of 2021.7 However, as the minister noted, the boom was slowing, and the benefits should only be used for short-term spending, such as extending current relief measures. As such, the surprise upside in revenue was largely used to maintain breathing space for the South African consumer while the government continued to unlock constraints to growth.8

Household consumption, meanwhile, recovered in 2021 (estimated at 5.6%), but it is forecast to average only about 2% over the next three years.9 As per Deloitte’s Global Consumer Tracker, households have taken on more debt, and consumers are particularly concerned about rising prices, making upcoming payments, savings, and credit card debt. Yet, of the 23 countries surveyed by Deloitte, South African consumers emerged as the most optimistic about their financial situation improving over the next three years.10 This relatively optimistic outlook is despite the National Treasury expectation for South Africa’s real GDP growth to drop to 2.1% in 2022, and taper off further to 1.6% and 1.7% in the outer years of the three-year forecast period.11

Higher interest rates, increasing inflation, high unemployment, ongoing power cuts together with high debt levels and limited fiscal space, against a backdrop of an unstable global growth environment (largely due to persisting supply bottlenecks, economic disruptions caused by the Ukraine crisis, higher food and energy prices, and rising policy rates globally), and the possibility of new variants of the coronavirus emerging on the scene are some of the downside risks to South Africa’s economic outlook. If left unaddressed, these risks could prolong the stagnant growth path the country has found itself on for more than a decade pre–COVID-19.

While economic recovery and fiscal sustainability featured prominently in Godongwana’s budget speech, crafting a higher, inclusive, and more sustainable growth path remains a challenging task. As per the latest budget, the fiscal deficit is expected to narrow, switching to an expected primary surplus in 2023–24, and gross loan debt is now forecast to stabilise at 75.1% of GDP in 2024–25.12

However, any dip in growth in the medium term (which is likely given a history of overoptimistic GDP projections in the prepandemic years13) will challenge fiscal consolidation efforts and potentially restrict South Africa from truly coming out of its ‘low-growth high-debt’ position. To raise economic growth to above 3% per annum, long-mooted productivity-enhancing structural economic reforms will need to gain greater momentum.14

After the onset of the COVID-19 pandemic in 2020, President Cyril Ramaphosa released an economic reconstruction and recovery plan according to which a sustained recovery that reignites growth amid fiscal consolidation will need to be underpinned by a faster pace of economic reforms to boost competition and productivity. This holds true specifically for the electricity sector and other network industries such as transport and communications, and for stimulating infrastructure investment.

This was echoed in the most recent State of the Nation Address by the president and the 2022 budget.15 Unfortunately, the pace of these reforms—in line with South Africa’s poor track record on policy implementation—has been slow.

Nevertheless, Operation Vulindlela—a joint initiative by the Presidency and National Treasury established to fast-track the implementation of economic reforms across sectors such as electricity, telecommunications and transport—has made some gains. For example, there has been notable momentum in the electricity sector, including the lifting of the licensing threshold from 1 MW to 100 MW for embedded electricity generation, which is expected to see an additional 4,000 MW of renewable generation and boost investment in the short to medium term. The Renewable Energy Independent Power Producer Procurement programme, meanwhile, is expected to add close to 7,000 MW of additional generation capacity through new bid windows. These two initiatives alone could see close to R200 billion of additional private sector investment in electricity generation.16

The government’s unbundling of the country’s power utility, Eskom, and its plans to legally constitute a stand-alone transmissions company later this year are other promising developments.17 In fact, a more competitive energy market could not only see more reliable supply of electricity, but with a progressive increase in the carbon tax, South Africa could also double its share of renewable energy by 2030.18 Given an energy mix still overly reliant on coal, this is in line with the country’s energy transition pledges made at COP26 in November 2021.19

Some progress is also underway in the transport and communications sectors. This includes target-setting for greater private sector participation in rail and harbours, with pilots underway this year to expand capacity and improve port efficiencies, respectively.20 It also includes the auction of spectrum in 2022, as spectrum release is anticipated to benefit consumers and businesses alike.

Heavy lifting will, however, continue to be the need of the hour on the infrastructure investment front, considering the fact that the government’s promises with regard to its infrastructure-led strategy to rebuild the economy have remained inconsistent with its actions on the ground. Overall investment had been on a declining trend in the years leading up to the pandemic. Gross fixed capital formation as a percentage of GDP has been on a 13-year decline in line with the slowdown in South Africa’s growth, dropping from a high of 22% of GDP in 200821 (pre–FIFA World Cup) to about 14% of GDP in mid-2021. Private investment, furthermore, has been particularly slow to recover from the lows of the pandemic.22

The 2022 budget allocated more than R800 billion over the next three years for infrastructure investment, but government-led infrastructure projects have been slow to get off the ground. In fact, South Africa’s construction industry, which could be a key driver of job creation, contracted for the fifth year in a row in 2021.23 In light of this, a greater sense of urgency, together with understanding the real needs of the private sector to co-invest—given government’s expectation to crowd-in private sector investment for such projects—as well as building capacity to set-up, package, and fast-track projects for private funding and development will be required.24

By having the ‘basics for growth’ in place (for example, sufficient electricity supply and lower costs to doing business due to improved transport and communications through accelerated reforms) while pursuing a path of fiscal consolidation, National Treasury estimates an additional 0.7 percentage points to the baseline forecast for GDP growth by 2024. Reforms boost confidence and create an enabling environment for business, while improving investor confidence and consumer demand.25

Although the downside risks to South Africa’s economic growth will persist in an uncertain global environment, maintaining the momentum in implementing economic reforms in the years to come will go a long way in addressing the long-standing structural constraints to growth.

{kind=link}