The future of mobility has been saved

The future of mobility How transportation technology and social trends are creating a new business ecosystem

25 September 2015

Will technological advances and shifts in social attitudes lead to our no longer owning or driving vehicles? The global auto industry's transformation has far-reaching implications for how we move from point A to point B and, in turn, affects carmakers, energy companies, insurers, health care, government funding, and more. Value shifts as a new ecosystem of mobility emerges.

Introduction

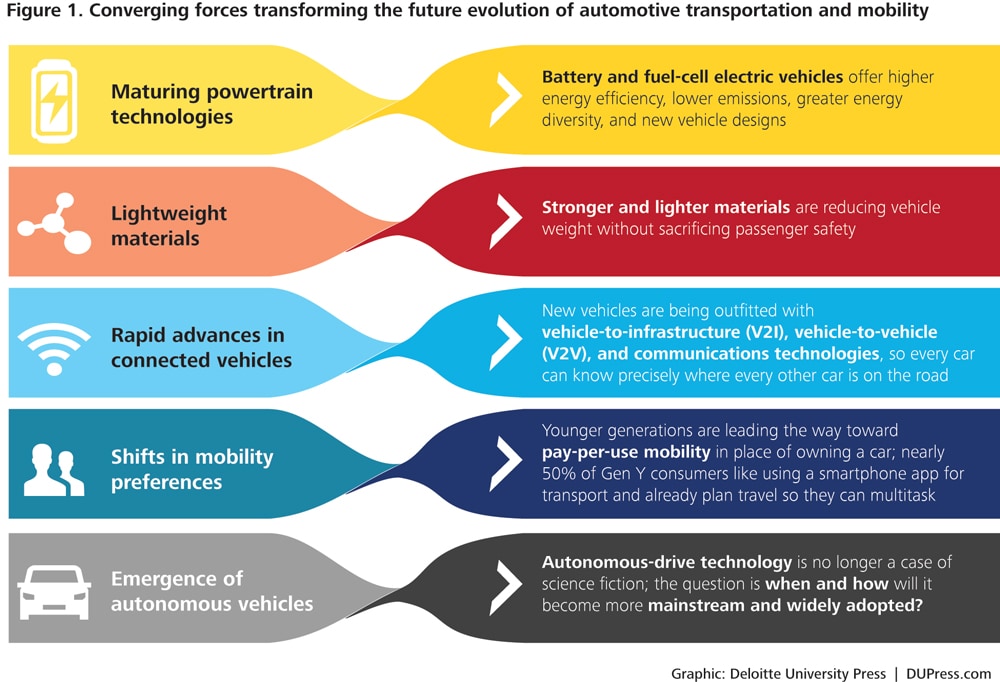

There is a critically important dialogue going on across the extended global automotive industry about the future evolution of transportation and mobility. This debate is driven by the convergence of a series of industry-changing forces and mega-trends (see figure 1).

Explore

Visit the Future of Mobility collection

Watch a video of Ben's journey

Listen to the podcast

Subscribe to receive updates on Future of Mobility

Explore Deloitte Review, issue 20

Innovative technologies are changing how companies develop and build vehicles. Electric and fuel-cell powertrains tend to offer greater propulsion for lower energy investment at lower emission levels.1 New, lightweight materials enable automakers to reduce vehicle weight without sacrificing passenger safety.2

Further breakthroughs are advancing the introduction of autonomous vehicles; increasingly, daily news reports suggest that driverless cars will soon become a commercial reality.3 We have already seen rapid advances in the “connected car”—innovations that integrate communications technologies and the Internet of Things to provide valuable services to drivers.4 Vehicles outfitted with electronic control modules and sensors that enable vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications can proactively suggest re-routings to avoid road hazards and call for assistance in the event of an accident.5 Soon, cars will routinely gain precise-enough awareness of where they are in relation to other vehicles and potential hazards to take preemptive action to avoid accidents.6

Simultaneously, young adults, along with urbanites, are gravitating toward a model of personal mobility consumption based on pay-per-use rather than upfront purchase of a capital asset, which fundamentally challenges today’s consumption model centered on personal ownership of cars.7

All told, a system that has been well established for a century is on the verge of a major transformation that could result in the emergence of a new ecosystem8 of personal mobility.

Today’s debate centers on whether the extended automotive industry will evolve incrementally toward some future mobility ecosystem or whether change will occur at a more radical pace and in a highly disruptive manner. No one knows the full scope and magnitude of the changes that are to come, what they entail, or how they will evolve, yet these forces have the potential to alter current industry structures, business models, competitive dynamics, value creation, and customer value propositions. We may be on the threshold of change as great as any the industry has ever seen.

The importance of the automotive industry

There’s no mystery about why we pay such close attention to the ups and downs of the auto industry—its extended value chain is an essential engine of global economic growth. In the United States, the sector generated $2 trillion of annual revenue in 2014 (see figure 2)—11.5 percent of US GDP9—from auto manufacturers, suppliers, dealers, financial services companies, oil companies, fuel retailers, aftermarket services and parts, insurance, public and private parking, public-sector taxes, tolling and traffic enforcement, medical care, and others.

At Deloitte, we’ve been engaged in a deep and broadly ranging study of the extended auto industry, the economics of alternative future states, and the potential impact of each on related industries.10 We have concluded that change will happen systematically—a rising tide, not a tsunami. At no point will the world be presented with a Manichean choice and collectively decide to plunge all-in to a system of driverless, pay-per-use travel—or else to change nothing at all. Rather, the new personal mobility ecosystem will likely emerge unevenly across geographic, demographic, and other dimensions, and evolve in phases over time.

Two divergent visions

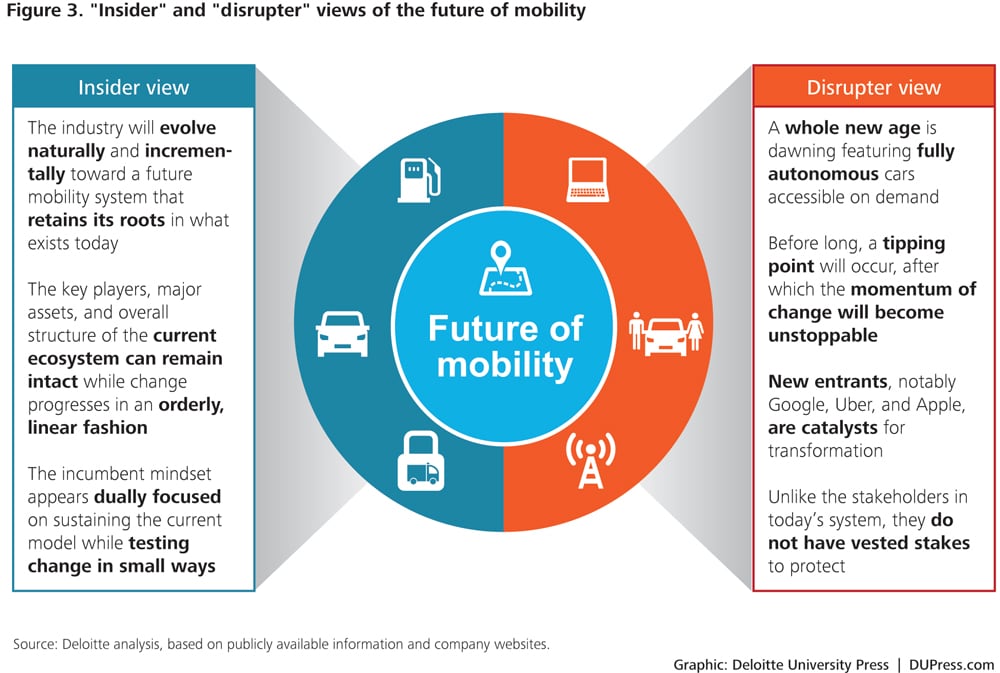

There are two profoundly different visions of the future of mobility. Fundamental differences center around whether today’s system of private ownership of driver-controlled vehicles remains relatively unchanged or whether we eventually migrate to a driverless system of predominantly shared mobility. There is also a critical difference about the pathway forward. The “insider” view believes that today’s system can progress in an orderly, linear fashion, in which the current industry assets and fundamental structure remain essentially intact. The “disrupter” view envisions a tipping-point approach to a very different future, one that offers great promise and potential societal benefits (see figure 3).

Within the high-tech community, companies are working to arrive at something radically different than today’s system of personally owned driver-driven passenger automobiles. According to this perspective, which we label the disrupter view, a new age is dawning, featuring fully autonomous cars accessible on demand. Progress toward it might be measured at first, but before long, a tipping point will occur, after which the momentum of change could gather speed. Imagine a world where the following statements are all true:

- Vehicles hardly ever crash. Autonomous operation removes the cause of almost all accidents: human error.11

- Traffic jams are rarities, thanks to sensors allowing for less space between vehicles and guidance systems with real-time awareness of congestion.

- Energy demand drops, since smaller mass and weight allow cars to be propelled by more compact, efficient, and environmentally friendly powertrains.

- Trip costs plummet, with average cost per passenger mile dipping from today’s ~$1 per mile to approximately 30¢ per mile, thanks to dramatically higher rates of asset utilization.

- Infrastructure is funded by charges for actual usage, since connected-car technology allows systems to precisely calculate personal road use.

- Parking lots disappear, as the rise of autonomous-drive and carsharing models diminish need.

- Law enforcement ceases to concern itself with traffic, since autonomous vehicles are programmed not to exceed speed limits or otherwise violate traffic laws.

- Speed of deliveries quickens and costs decrease through the rise of fully autonomous networks of long-haul trucks that can operate for more extended time periods and cover longer distances with lower labor costs.

- Seamless multimodal transportation becomes the new norm, as greater system interoperability enables consumers to get from point A to point B via multiple, connected modes of transportation on a single fixed price charged on a single payment system.

Much of the technology already exists to turn this vision into reality, and disrupters are working toward implementing it, catalyzing the transformation. Google’s driverless cars have already driven more than 1 million miles in autonomous mode, and the company is running pilot and testing programs with small fleets of fully autonomous vehicles in Mountain View, CA, and Austin, TX.12 Less technologically dazzling but equally disruptive—and far more mature—are carsharing and ridesharing: The movement that started with Zipcar has more recently spawned the ridesharing concepts of Uber and Lyft; Uber alone delivers 1 million trips per day worldwide13 and is growing rapidly.

Still, these industry-changing technologies may fail to reach transformational scale—or at least fail to do so within a strategically relevant time frame. Insiders, heavily invested in the current auto industry, see change evolving slowly toward a future that retains its roots in what exists today.

We see the major auto companies pursuing strategies that address the converging forces incrementally, creating future option value while preserving flexibility. These industry players’ efforts and investments are yielding a steady stream of benefits for customers. For example, in introducing connected-car technology, manufacturers offer drivers many of the benefits associated with autonomous drive without fundamentally altering how humans currently interact with vehicles.

Automakers are experimenting and inventing, and have passionate voices within their ranks describing much-altered futures. Most have set up offices in Silicon Valley to gain greater proximity to technology development and early-stage funding. Among the noteworthy examples of forward-thinking initiatives are Ford’s 25 mobility projects,14 BMW iVentures,15 Daimler’s engineering advances in intelligent driving,16 and Cadillac’s “super cruise” functionality.17 In addition, public-private partnerships such as the recently opened Mcity in Ann Arbor, MI, provide a platform to enable more efficient and effective automated vehicle (and feature) testing.18

This approach is consistent with historic norms, in which automakers invest in new technologies—e.g., antilock brakes, electronic stability control, backup cameras, and telematics—across higher-end vehicle lines and then move down market as scale economics take hold.19 In our ongoing conversations with auto-industry leaders, they repeatedly and collectively argue that outsiders simply do not appreciate the sheer complexity of developing a vehicle today, the challenge of introducing new advanced technologies into a vehicle’s architecture, or the rigor and inertia of the regulatory environment. All of this encourages incumbents to believe that they can be at the center of actively managing the timing and pace of these converging forces.

But the interplay of the converging forces of change may be less predictable and lead to faster upheaval than they think. Automakers might be overestimating how much power they have to manage the course of future events.

Four futures will coexist

Given the disparate forces shaping the landscape, we envision four different personal mobility futures emerging from the intersection of two critical trends (see figure 4):

- Vehicle control (driver versus autonomous)

- Vehicle ownership (private versus shared)

Our analysis concludes that change will happen unevenly around the world, with different populations requiring different modes of transportation—which means that the four future states may well exist simultaneously. In other words, business leaders will need to prepare their organizations to be capable of operating in four different futures, with distinct sets of customers—beginning in as little as 5–15 years. Here we offer a high-level description of each future state and the conditions that promote its eventual emergence.

Future state 1: Incremental change

This most conservative vision of the future puts heavy weight on the massive assets tied up in today’s system, assuming that these assets’ owners will neither willingly abandon them nor eagerly transfer capital into new enterprises with uncertain returns. It sees private ownership remaining the norm, with consumers opting for the particular forms of privacy, flexibility, security, and convenience that come with owning vehicles. Importantly, while incorporating driver-assist technologies, this vision assumes that fully autonomous drive won’t become widely available anytime soon.

With so little change envisioned, this future state reinforces automakers’ reliance on a business model that emphasizes unit sales. They continue to invest in the development and introduction of new vehicle lines with advanced technologies, and dealers retain responsibility for the customer experience. Other industry players are similarly incented to rely on the practices and structures that have been well established for decades.

Future state 2: A world of carsharing

The second future state anticipates continued growth of shared access to vehicles.20 In this state, economic scale and increased competition drive the expansion of shared vehicle services into new geographic territories and more specialized customer segments. Here, passengers more heavily value the convenience of point-to-point transportation created through ridesharing and carsharing, saving them the hassle of navigating traffic and finding parking spaces. Plus, the system offers options for non-drivers such as seniors, low-income families, and minors without licenses.

In this future state, as the cost per mile decreases, some come to view ridesharing as a more economical, convenient, and sustainable way to get around, particularly for short point-to-point movements (see below for our analysis of the economics of mobility). As shared mobility serves a greater proportion of local transportation needs, multivehicle households can begin reducing the number of cars they own while others may abandon ownership altogether, reducing future demand.

Future state 3: The driverless revolution

The third state is one in which autonomous-drive technology proves to be viable, safe, convenient, and economical, yet private ownership continues to prevail. Collaboration between leading academics, regulatory agencies, and businesses accelerates progress toward this future.21 Both technology and automotive firms continue investing heavily to increase “V2X” (V2V and V2I) capabilities; in parallel, driverless technology matures, with the success of early pilots fostering quick adoption.

Given that this future state assumes most drivers still prefer owning their own vehicles, individuals seek the driverless functionality for its safety and other potential benefits but continue to own cars for many of the same reasons they did before the advent of autonomous drive. They might even invest more in their vehicles as a new era of customization dawns and it becomes appealing to use vehicles tailored for specific occasions and circumstances.22 That said, the features in which owners are willing to invest, and the design of the vehicles themselves, may change; this new segment of the market may offer lighter, more technically advanced vehicles that embrace design principles counter to today’s four-door, driver-in-front-on-left, gripping-the-steering-wheel reality.

Future state 4: A new age of accessible autonomy

The fourth future state anticipates a convergence of both the autonomous and vehicle-sharing trends. In this future, mobility management companies offer a range of passenger experiences to meet widely varied needs at differentiated price points.23 The earliest, most avid adopters seem likely to be urban commuters, given the potential for faster trips thanks to reduced distances between highly automated vehicles, and routes enhanced by real-time awareness of conditions. Over time, as smart infrastructure expands and driver usage nears a tipping point, fleets of autonomous shared vehicles could spread from urban centers to densely populated suburbs and beyond.

Advanced communications technologies coordinate the customer’s point-to-point mobility experience: Intuitive interfaces enable users to order a vehicle pickup within minutes and travel from point A to point B efficiently, safely, and cost-effectively. Vehicle and traffic network systems operators, in-vehicle content-experience providers (e.g., software and infotainment firms), and data owners (e.g., telecoms) could have further opportunities to monetize the value of passengers’ attention in transit as well as additional metadata pertaining to system use.

How much per mile?

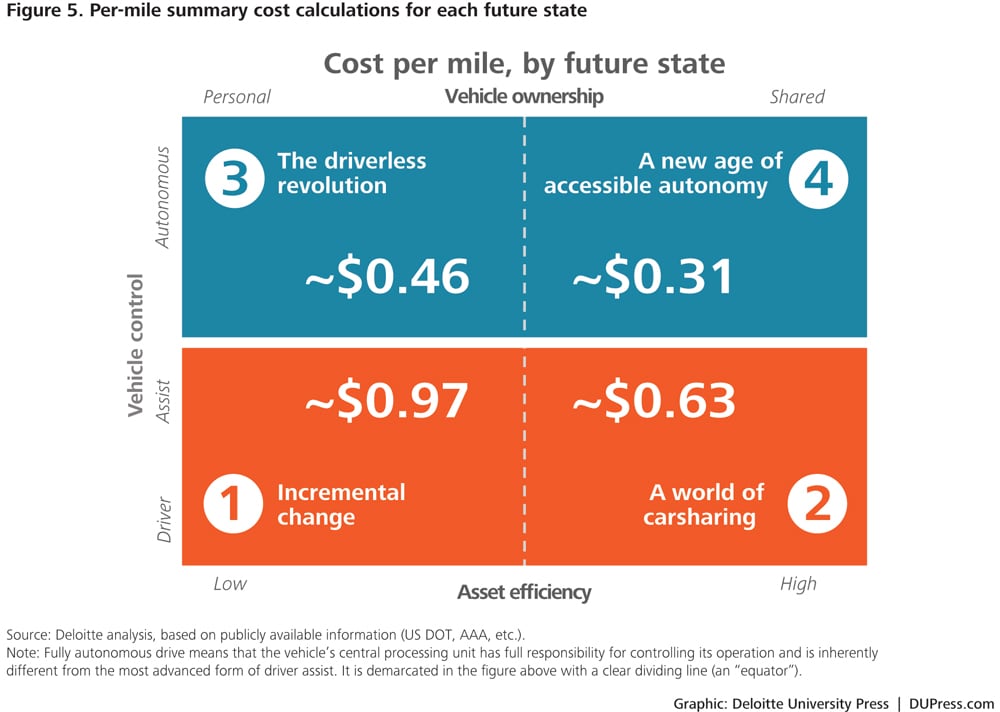

We conducted an analysis to calculate the average cost per mile under each of these future states; this analysis shows that consumers could benefit from lower per-mile travel costs in future states 2, 3, and 4 (see figure 5 for a summary of these costs by future state, and figure 6 for a more detailed breakdown of associated costs).

According to our calculations, personally owned vehicles today impose costs of approximately $0.97 per mile. This includes vehicle depreciation, financing, insurance, and fuel, as well as the value of the individual driver’s time. By adjusting these key variables for each future state, we have developed high-level directional estimates of per-mile costs for each future state at maturity.

Our projections indicate that in future state 2 of shared mobility, the economics become more favorable compared to private vehicle ownership, due to greater asset utilization and reduced consumer time spent driving. Over time, the efficiencies of greater asset utilization offset the higher costs associated with employing a driver. Our analysis suggests that a fully scaled shared-service model would cost approximately $0.63 per mile.

If personally owned autonomous-drive vehicles become widely adopted (future state 3), projecting the cost per mile becomes trickier, since calculations depend on the assumptions made for the value of reallocating the driver’s time and productivity. Based on conservative estimates of this time value, future state 3 would cost approximately $0.46 per mile.24

And in a world of autonomous shared vehicles (future state 4), our analysis finds the economics to be highly favorable: Cost per mile could drop as low as $0.31 for single-person trips—in other words, lower by roughly two-thirds than the cost of driving today. Savings partly result from key assumptions around the availability of lighter-weight vehicles (for example, two-person pods for as little as $10,000) reducing capital costs, high rates of asset utilization (much higher than today’s 4 percent), and the value placed on freeing up driver time for more productive purposes.

The course of change

In our view, moves from the current state of mobility will likely occur fastest in the direction of shared access, in turn catalyzing the (upward) adoption of autonomous drive. We see this progression occurring in a number of steps, as illustrated in figure 7.

Step 1: Gradual adoption of shared access

The move from pure personal ownership of vehicles to a system more reliant on shared access (i.e., from quadrant 1 to quadrant 2 of figure 7), is already under way in some parts of the United States. For example, carsharing services, such as Zipcar, have roughly doubled their customer base in the last six years,25 while ridesharing services, such as Uber, have been adding 50,000 drivers per month and completed 140 million rides worldwide in 2014 alone.26 The software and hardware systems these services employ to match drivers with riders are evolving rapidly, incorporating information about observed behaviors to improve rider and driver experiences.27 Furthermore, intense competition offers the prospect of reducing market prices as improved economics related to increased asset utilization take hold.

Step 2: Tipping-point shift to driverless

Currently, wide acceptance of autonomous operation seems much further away than a broad carsharing/ridesharing culture.28 Sources of delay include the need to address existing technological limitations, such as sensor functioning in all weather and the wide availability of 3D mapping, as well as concerns over cyber security and liability.29 How quickly these and other issues are addressed will be a key determinant of the pace of adoption for autonomous drive.

Automakers—both in partnership and competition with tech firms—are sequentially and systematically pursuing a shift of control from driver-only to driver-assist to autonomous drive. If driverless technology were the only vector of change, uptake might gradually gain steam, following the pattern of adoption that has become classic to the automotive industry. In our view, this is the pathway from quadrant 1 to quadrant 3, incremental change to driverless revolution, which is well under way.

However, we also see change progressing along a second, parallel northward vector—from a world of carsharing toward a new age of accessible autonomy. Along this path, a powerful, additional boost toward driverless adoption is also under way. Uber recently partnered with both Carnegie Mellon University and the University of Arizona to open an Advanced Technologies Center in Pittsburgh and test driverless cars and optics for mapping technologies.30 Ridesharing services have economic incentives to accelerate the adoption of autonomous vehicles, since it could reduce one of the biggest operational costs in this system: the driver. These companies could capture a significant share of the consumer surplus value generated by reducing this cost. If autonomous drive becomes viable for ridesharing services, it could dramatically accelerate broad adoption, as consumers have greater opportunity to experience the technology while simultaneously realizing significant reductions in the cost of personal mobility.

Finally, other high-tech players are forging a third path to autonomous drive. For example, Google’s self-driving car program is testing cars that do not rely on driver-assist progression but, rather, immediately jump to fully autonomous; Google has stated publicly that “taking the driver out of the loop” is the safest path.31 And in the long term, it is still unclear whether Google intends to choose between supporting shared autonomous mobility, personal ownership, or both.

Rather than following the historical pattern for technological innovation, autonomous driving, when it arrives, could constitute a step-change. And the ensuing changes to the personal mobility ecosystem could unfold much more quickly than many companies can imagine. (See “Forces of delay—or acceleration.”)

Forces of delay—or acceleration

The inertial forces slowing down the process that Joseph Schumpeter called “creative destruction”32 in the realm of personal mobility are not to be underestimated. The table below summarizes the key drivers that could either significantly delay or accelerate the adoption of new technologies.

The future for the extended automotive industry

Deloitte’s recent Business Trends report “Business ecosystems come of age”33 describes a broad pattern by which many of the industries that make up the global economy are undergoing a kind of metamorphosis. What we inherited from the 20th century, the paper states, were “narrowly defined industries built around large, vertically integrated and mainly ‘self-contained’ corporations”—but in recent years, thanks largely to digital technologies, those monoliths have been fracturing into independent, tightly focused, highly interconnected businesses, many of which perform their specialized functions across former industry lines. We argue, “The fundamental boundaries that have specified the relationships, interactions, and possibilities of most businesses are rapidly blurring and dissolving.”34 The basic human needs that industries were built to serve remain, but serving them is now the work of much more fluid ecosystems. In the future mobility system, the mobility needs that today’s industries were built to serve remain, but much more fluid ecosystems will likely emerge to serve them. And this portends significant change to current business models—and partnerships (e.g., between insiders and disrupters) will be critical to deliver new mobility.

Complementary analysis from Deloitte’s Center for the Edge argues that a new mobility ecosystem could spark a “virtual” value chain in which the ability to capture, aggregate, and analyze mobility-related data becomes a tremendous source of value. In this vision, value will accrete to those who:

- Provide end-to-end seamless mobility

- Manage the mobility network operating system

- Holistically create and manage the in-vehicle experience

Rewards could be great for players that are able to capture, analyze, and (securely) monetize the awareness of where people travel to, the routes they take to get there, and what they do along the way. While third parties will no doubt pay for access to this information, perhaps the greatest value will be realized by new entrants who emerge as “trusted advisers” to help all of us navigate the new ecosystem and increase our “return on mobility.” These companies may also enable the ecosystem to monetize new services and ownership models.

The future mobility system will also need firms to develop and manage the vehicle-operating and traffic network information system that helps direct and control the movement of autonomous vehicles and shared mobility fleets. Technology companies already have access to passenger data and seek to capture this value, but they will likely face challenges from entrants with new business models.35 Vehicle manufacturers could design and develop vehicles not to accommodate drivers but, rather, to emphasize passenger experience, potentially giving rise to new vehicle structures and forms.

In the meantime, it is reasonable to anticipate a healthy tension between automakers, heavily invested in today’s product-centered system, and technological innovators looking to realize a more virtually dependent world of mobility options.36 And in this case, since shared driverless cars could decrease total auto sales, it’s no wonder why carmakers might be reluctant to embrace such a vision.

But there’s little question that some version, perhaps multiple versions, of a new ecosystem—one based on shared access and autonomous driving—will indeed eventually emerge. Where and when it does, the change could be profound: lower cost per mile, improved safety, reduced need for parking lots and traffic enforcement, dramatically lower overall environmental impact, and more. Questions revolve around what will happen to today’s automotive sector and how these will affect auto OEMs, suppliers, dealers, oil companies, fuel retailers, aftermarket service and parts companies, insurance companies, public and private parking, public-sector traffic enforcement, and others. However the forces of change unfold, every company may need to determine, in Roger Martin’s succinct phrasing, “where to play and how to win.”37

What follows is an initial overview of the enormous scope of change that could affect the key stakeholders in the current system as well as in the new mobility ecosystem.

Global automotive manufacturers (OEMs) face momentous and difficult decisions. The auto industry currently struggles with the fundamental economics of an intensely competitive business with enormous capital requirements; operating margins and return on invested capital remain low.38 The industry operates with sizeable excess production capacity: Globally, it is possible to produce 113 million vehicles annually, while sales hover around 70 million.39 In addition, regulatory requirements (such as CAFE, zero-emission vehicles, and safety standards) are becoming ever more stringent and costly.40 And consumers relentlessly demand that automakers integrate the latest technologies.

OEMs will need to determine if they should evolve from a (relatively) fixed capital production, first-transaction, product-sale business into one centered on being an end-to-end mobility services provider. This would represent a profound business-model change and the development of entirely new capabilities to be competitively and sustainably viable.

At a minimum, they will need to weigh how to meet the needs of a changing landscape as consumers increasingly use shared mobility and become interested in highly tailored, customized, personally owned autonomous-drive vehicles.41 This could require transforming product-development and innovation capabilities and reconfiguring supply chains and production operating systems to be even more lean, flexible, and “smart customization”-enabled. At the same time, consumers could begin demanding shared autonomous vehicles for different kinds of trips, which could spur the creation of more varied vehicle forms. This could drive the development of high-speed, low-cost vehicle assembly operations to create and produce vehicles with lightweight frames, custom experience-focused software, and highly customized, design-focused interiors. Light autonomous-drive vehicles can be made to be highly energy-efficient and, with a longer driving range, might make electric vehicles more viable and help automakers meet stringent regulatory standards.

Automotive suppliers will have to adjust as OEMs transform. As sales of autonomous-drive vehicles grow, suppliers will need lean, agile operations to serve the highly varying needs of the personally owned segment. While most of the core powertrain, chassis, brake systems, and electronic wiring components on such vehicles may be standard, giving suppliers some benefits of operational scale, the packaging for personally owned vehicles will likely be tailored and customized. Building the more standardized vehicles needed for shared mobility solutions could offer large volumes, and the demand will likely be for less complex and lower-value-added products; therefore, the economics in this new marketplace will strongly favor the lowest-cost producers.

Technology firms are driving much of the change under way. Earlier we referred to these firms as the disrupters; their strategic vision is that toppling longstanding institutional structures and frameworks can generate massive value. Unlike the manufacturers and asset holders in today’s system, they have few vested stakes in the current automotive ecosystem, and they view the market for mobility as a new frontier. They share a conviction that the system’s dominant source of value could be in creating and managing the operating system and in-transit experience as well as mining the data generated.

These companies have shown to be adept at building large, complex information networks and operating systems, introducing artificial intelligence to help minimize human error and randomness, creating compelling environments that drive consumer behavior, and creating digital communities. They view the vehicle as another platform in a multidevice world. Vehicle sensors and personal devices could generate ever-greater amounts of data, with insights producing personalized customer experiences and delivering targeted advertising and services.42 Integrated information systems can enable effective intermodal transportation. And mobile, wireless, location-based systems can create new opportunities for dynamic-pricing, single-payment, and consumption-based models to become much more prevalent. Technology leaders in general, relative to traditional auto-industry leaders, are in highly advantaged positions to capture this information and virtual-based value.

Cargo delivery and long-haul trucking currently face significant challenges that the future mobility ecosystem could alleviate. In the most ambitious version of the future, cargo transportation and delivery systems could become predominantly driverless through daisy chains or remote operation—an appealing scenario, considering the US trucking industry’s growing labor shortages, with as many as 30,000 driver positions unfilled and an annual turnover rate of 92 percent.43 Autonomous vehicles offer a way to overcome restrictions on hours driven and increase capital utilization. Given long-haul cargo transportation’s $700 billion in annual revenues,44 major fleets such as UPS and USPS have a sizeable economic incentive to actively explore how to operate for more extended time periods, cover longer distances without stops, and reduce the cost of drivers (accounting for 26 percent of operating costs).45 With such compelling economics, this sector could become an early test bed for driverless technologies.

Insurers face a complex set of strategic questions in how they will continue to grow their business and serve various segments, geographies, and demographic groups depending on which future states of mobility take hold. With $205 billion in premiums for personal liability, collision, and umbrella insurance in play, the stakes are high. Insurers today largely insure the vehicle and not the individual driver; they are currently unable to accurately assess risk associated with new forms of mobility and safety—ridesharing in the short term, and driverless cars and inter-modal transportation in the long term. Insurers need an operating model that fosters innovation and allows them to adapt to a rapidly changing market: As shared mobility continues to become more popular, insurers will need to evolve their business model to be more driver-centric, as there will be fewer vehicles to insure and more drivers using each one. With the emergence of autonomous drive, insurers will have to continue supporting vehicle and driver-centric models while developing new forms of insurance for the more technical, systemic failure risk associated with a driverless vehicle. This new system faces clearly significant issues associated with assigning liabilities: Risk pools morphing will likely force dramatic changes in insurers’ cost structure. The flood of new information provided by greater connectivity provides ways to offset these costs through more accurate ways to assign risk.

The US public sector will likely have to figure out how to offset anticipated declines in the $251 billion annually generated from fuel taxes, public-transportation fees, tolls, vehicle sales taxes, municipal parking, and registration and licensing fees. All these revenues are tied to today’s reality of individually owned and operated vehicles—for instance, the need for parking diminishes with the rise of autonomous-drive shared mobility. Agencies may need to evaluate alternatives—e.g., taxing “movement” versus ownership. Monetization for road usage in the future could transition to a much more dynamic model based on time of day, market demand, routes traveled, distance, and vehicle form, aligning the use of public assets more directly to usage than today’s system. On the other hand, as vehicle volumes decline, municipalities might experience reduced wear and tear on infrastructure and have the opportunity to reallocate parking and other space to more value-adding purposes. Government costs (such as the DMV) could decline significantly and potentially offset some of the public-sector revenue decline.

The value shifts for these and other industries could have a tremendous impact on revenues across the ecosystem. Figure 8 summarizes some of the potential effects of the shift to the future mobility ecosystem. The graphic also includes potential societal benefits expected as a result of autonomous drive and shared mobility technological advances. The analysis does not yet account for new business models that could evolve within the future ecosystem; it is meant to illustrate the potential effects/directional impact that autonomous cars and shared mobility may have on today’s ecosystem.

Conclusions

In the four futures of the mobility ecosystem, sources of value shift profoundly. With this evolution toward a new ecosystem still taking shape, we want to share some reflections on the strategic and operational implications for legacy incumbents, extended industry participants, and disrupters as they weigh their future direction. Specifically:

- Industries rise and fall. Cycles take long periods to play out, but eventually change occurs.

- The potential system benefits and fundamental economics of the disrupter vision are compelling.

- There is a pathway for the existing extended auto industry to lead the transition to the future of personal mobility, but it will require fundamental and expeditious business-model change. Competing effectively in the future mobility ecosystem requires building new and different capabilities. Everyone in today’s extended automotive sector needs to reassess how they will operate and create value while the four states coexist and in the longer term, when autonomous and shared mobility become more mainstream.

- The insiders and disrupters need each other. Unquestionably, fierce competition will characterize the commercial environment around personal mobility. Yet, despite their wariness and differing outlooks and perspectives, automotive incumbents and challenging new entrants will together make up a new ecosystem with high levels of interdependency, mutualism, and symbiosis.

- Profound disruption will extend far past the automotive industry. Every aspect of the modern economy based on the assumption of human-driven, personally owned vehicles will be challenged. Each company in this new ecosystem will have to determine where to play and how to win. As in any time of large-scale transformation, we can expect to see new players, with differentiated capabilities, emerge and change the fundamental dynamics of where and how value is created. Ultimately, the market, in its relentless quest for higher performance at lower cost, will decide who wins and who loses.

Deloitte will continue to periodically share insights about this evolution as part of an ongoing series. We aim to contribute to the dialogue as we all collectively wrestle with the impact and implications of the future of mobility. Our objective is to help to build a bridge between a highly uncertain futuristic vision, the realities of today’s industries, and potential pathways to alternative future realities.

The future of mobility: How transportation technology and social trends are creating a new business ecosystem is an independent publication and has not been authorized, sponsored, or otherwise approved by Apple Inc.

Further breakthroughs are advancing the introduction of autonomous vehicles; increasingly, daily news reports suggest that driverless cars will soon become a commercial reality.3 We have already seen rapid advances in the “connected car”—innovations that integrate communications technologies and the Internet of Things to provide valuable services to drivers.4 Vehicles outfitted with electronic control modules and sensors that enable vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications can proactively suggest re-routings to avoid road hazards and call for assistance in the event of an accident.5 Soon, cars will routinely gain precise-enough awareness of where they are in relation to other vehicles and potential hazards to take preemptive action to avoid accidents.6

Simultaneously, young adults, along with urbanites, are gravitating toward a model of personal mobility consumption based on pay-per-use rather than upfront purchase of a capital asset, which fundamentally challenges today’s consumption model centered on personal ownership of cars.7

All told, a system that has been well established for a century is on the verge of a major transformation that could result in the emergence of a new ecosystem8 of personal mobility.

Today’s debate centers on whether the extended automotive industry will evolve incrementally toward some future mobility ecosystem or whether change will occur at a more radical pace and in a highly disruptive manner. No one knows the full scope and magnitude of the changes that are to come, what they entail, or how they will evolve, yet these forces have the potential to alter current industry structures, business models, competitive dynamics, value creation, and customer value propositions. We may be on the threshold of change as great as any the industry has ever seen.

The importance of the automotive industry

There’s no mystery about why we pay such close attention to the ups and downs of the auto industry—its extended value chain is an essential engine of global economic growth. In the United States, the sector generated $2 trillion of annual revenue in 2014 (see figure 2)—11.5 percent of US GDP9—from auto manufacturers, suppliers, dealers, financial services companies, oil companies, fuel retailers, aftermarket services and parts, insurance, public and private parking, public-sector taxes, tolling and traffic enforcement, medical care, and others.

At Deloitte, we’ve been engaged in a deep and broadly ranging study of the extended auto industry, the economics of alternative future states, and the potential impact of each on related industries.10 We have concluded that change will happen systematically—a rising tide, not a tsunami. At no point will the world be presented with a Manichean choice and collectively decide to plunge all-in to a system of driverless, pay-per-use travel—or else to change nothing at all. Rather, the new personal mobility ecosystem will likely emerge unevenly across geographic, demographic, and other dimensions, and evolve in phases over time.

Two divergent visions

There are two profoundly different visions of the future of mobility. Fundamental differences center around whether today’s system of private ownership of driver-controlled vehicles remains relatively unchanged or whether we eventually migrate to a driverless system of predominantly shared mobility. There is also a critical difference about the pathway forward. The “insider” view believes that today’s system can progress in an orderly, linear fashion, in which the current industry assets and fundamental structure remain essentially intact. The “disrupter” view envisions a tipping-point approach to a very different future, one that offers great promise and potential societal benefits (see figure 3).

Within the high-tech community, companies are working to arrive at something radically different than today’s system of personally owned driver-driven passenger automobiles. According to this perspective, which we label the disrupter view, a new age is dawning, featuring fully autonomous cars accessible on demand. Progress toward it might be measured at first, but before long, a tipping point will occur, after which the momentum of change could gather speed. Imagine a world where the following statements are all true:

- Vehicles hardly ever crash. Autonomous operation removes the cause of almost all accidents: human error.11

- Traffic jams are rarities, thanks to sensors allowing for less space between vehicles and guidance systems with real-time awareness of congestion.

- Energy demand drops, since smaller mass and weight allow cars to be propelled by more compact, efficient, and environmentally friendly powertrains.

- Trip costs plummet, with average cost per passenger mile dipping from today’s ~$1 per mile to approximately 30¢ per mile, thanks to dramatically higher rates of asset utilization.

- Infrastructure is funded by charges for actual usage, since connected-car technology allows systems to precisely calculate personal road use.

- Parking lots disappear, as the rise of autonomous-drive and carsharing models diminish need.

- Law enforcement ceases to concern itself with traffic, since autonomous vehicles are programmed not to exceed speed limits or otherwise violate traffic laws.

- Speed of deliveries quickens and costs decrease through the rise of fully autonomous networks of long-haul trucks that can operate for more extended time periods and cover longer distances with lower labor costs.

- Seamless multimodal transportation becomes the new norm, as greater system interoperability enables consumers to get from point A to point B via multiple, connected modes of transportation on a single fixed price charged on a single payment system.

Much of the technology already exists to turn this vision into reality, and disrupters are working toward implementing it, catalyzing the transformation. Google’s driverless cars have already driven more than 1 million miles in autonomous mode, and the company is running pilot and testing programs with small fleets of fully autonomous vehicles in Mountain View, CA, and Austin, TX.12 Less technologically dazzling but equally disruptive—and far more mature—are carsharing and ridesharing: The movement that started with Zipcar has more recently spawned the ridesharing concepts of Uber and Lyft; Uber alone delivers 1 million trips per day worldwide13 and is growing rapidly.

Still, these industry-changing technologies may fail to reach transformational scale—or at least fail to do so within a strategically relevant time frame. Insiders, heavily invested in the current auto industry, see change evolving slowly toward a future that retains its roots in what exists today.

We see the major auto companies pursuing strategies that address the converging forces incrementally, creating future option value while preserving flexibility. These industry players’ efforts and investments are yielding a steady stream of benefits for customers. For example, in introducing connected-car technology, manufacturers offer drivers many of the benefits associated with autonomous drive without fundamentally altering how humans currently interact with vehicles.

Automakers are experimenting and inventing, and have passionate voices within their ranks describing much-altered futures. Most have set up offices in Silicon Valley to gain greater proximity to technology development and early-stage funding. Among the noteworthy examples of forward-thinking initiatives are Ford’s 25 mobility projects,14 BMW iVentures,15 Daimler’s engineering advances in intelligent driving,16 and Cadillac’s “super cruise” functionality.17 In addition, public-private partnerships such as the recently opened Mcity in Ann Arbor, MI, provide a platform to enable more efficient and effective automated vehicle (and feature) testing.18

This approach is consistent with historic norms, in which automakers invest in new technologies—e.g., antilock brakes, electronic stability control, backup cameras, and telematics—across higher-end vehicle lines and then move down market as scale economics take hold.19 In our ongoing conversations with auto-industry leaders, they repeatedly and collectively argue that outsiders simply do not appreciate the sheer complexity of developing a vehicle today, the challenge of introducing new advanced technologies into a vehicle’s architecture, or the rigor and inertia of the regulatory environment. All of this encourages incumbents to believe that they can be at the center of actively managing the timing and pace of these converging forces.

But the interplay of the converging forces of change may be less predictable and lead to faster upheaval than they think. Automakers might be overestimating how much power they have to manage the course of future events.

Four futures will coexist

Given the disparate forces shaping the landscape, we envision four different personal mobility futures emerging from the intersection of two critical trends (see figure 4):

- Vehicle control (driver versus autonomous)

- Vehicle ownership (private versus shared)

Our analysis concludes that change will happen unevenly around the world, with different populations requiring different modes of transportation—which means that the four future states may well exist simultaneously. In other words, business leaders will need to prepare their organizations to be capable of operating in four different futures, with distinct sets of customers—beginning in as little as 5–15 years. Here we offer a high-level description of each future state and the conditions that promote its eventual emergence.

Future state 1: Incremental change

This most conservative vision of the future puts heavy weight on the massive assets tied up in today’s system, assuming that these assets’ owners will neither willingly abandon them nor eagerly transfer capital into new enterprises with uncertain returns. It sees private ownership remaining the norm, with consumers opting for the particular forms of privacy, flexibility, security, and convenience that come with owning vehicles. Importantly, while incorporating driver-assist technologies, this vision assumes that fully autonomous drive won’t become widely available anytime soon.

With so little change envisioned, this future state reinforces automakers’ reliance on a business model that emphasizes unit sales. They continue to invest in the development and introduction of new vehicle lines with advanced technologies, and dealers retain responsibility for the customer experience. Other industry players are similarly incented to rely on the practices and structures that have been well established for decades.

Future state 2: A world of carsharing

The second future state anticipates continued growth of shared access to vehicles.20 In this state, economic scale and increased competition drive the expansion of shared vehicle services into new geographic territories and more specialized customer segments. Here, passengers more heavily value the convenience of point-to-point transportation created through ridesharing and carsharing, saving them the hassle of navigating traffic and finding parking spaces. Plus, the system offers options for non-drivers such as seniors, low-income families, and minors without licenses.

In this future state, as the cost per mile decreases, some come to view ridesharing as a more economical, convenient, and sustainable way to get around, particularly for short point-to-point movements (see below for our analysis of the economics of mobility). As shared mobility serves a greater proportion of local transportation needs, multivehicle households can begin reducing the number of cars they own while others may abandon ownership altogether, reducing future demand.

Future state 3: The driverless revolution

The third state is one in which autonomous-drive technology proves to be viable, safe, convenient, and economical, yet private ownership continues to prevail. Collaboration between leading academics, regulatory agencies, and businesses accelerates progress toward this future.21 Both technology and automotive firms continue investing heavily to increase “V2X” (V2V and V2I) capabilities; in parallel, driverless technology matures, with the success of early pilots fostering quick adoption.

Given that this future state assumes most drivers still prefer owning their own vehicles, individuals seek the driverless functionality for its safety and other potential benefits but continue to own cars for many of the same reasons they did before the advent of autonomous drive. They might even invest more in their vehicles as a new era of customization dawns and it becomes appealing to use vehicles tailored for specific occasions and circumstances.22 That said, the features in which owners are willing to invest, and the design of the vehicles themselves, may change; this new segment of the market may offer lighter, more technically advanced vehicles that embrace design principles counter to today’s four-door, driver-in-front-on-left, gripping-the-steering-wheel reality.

Future state 4: A new age of accessible autonomy

The fourth future state anticipates a convergence of both the autonomous and vehicle-sharing trends. In this future, mobility management companies offer a range of passenger experiences to meet widely varied needs at differentiated price points.23 The earliest, most avid adopters seem likely to be urban commuters, given the potential for faster trips thanks to reduced distances between highly automated vehicles, and routes enhanced by real-time awareness of conditions. Over time, as smart infrastructure expands and driver usage nears a tipping point, fleets of autonomous shared vehicles could spread from urban centers to densely populated suburbs and beyond.

Advanced communications technologies coordinate the customer’s point-to-point mobility experience: Intuitive interfaces enable users to order a vehicle pickup within minutes and travel from point A to point B efficiently, safely, and cost-effectively. Vehicle and traffic network systems operators, in-vehicle content-experience providers (e.g., software and infotainment firms), and data owners (e.g., telecoms) could have further opportunities to monetize the value of passengers’ attention in transit as well as additional metadata pertaining to system use.

How much per mile?

We conducted an analysis to calculate the average cost per mile under each of these future states; this analysis shows that consumers could benefit from lower per-mile travel costs in future states 2, 3, and 4 (see figure 5 for a summary of these costs by future state, and figure 6 for a more detailed breakdown of associated costs).

According to our calculations, personally owned vehicles today impose costs of approximately $0.97 per mile. This includes vehicle depreciation, financing, insurance, and fuel, as well as the value of the individual driver’s time. By adjusting these key variables for each future state, we have developed high-level directional estimates of per-mile costs for each future state at maturity.

Our projections indicate that in future state 2 of shared mobility, the economics become more favorable compared to private vehicle ownership, due to greater asset utilization and reduced consumer time spent driving. Over time, the efficiencies of greater asset utilization offset the higher costs associated with employing a driver. Our analysis suggests that a fully scaled shared-service model would cost approximately $0.63 per mile.

If personally owned autonomous-drive vehicles become widely adopted (future state 3), projecting the cost per mile becomes trickier, since calculations depend on the assumptions made for the value of reallocating the driver’s time and productivity. Based on conservative estimates of this time value, future state 3 would cost approximately $0.46 per mile.24

And in a world of autonomous shared vehicles (future state 4), our analysis finds the economics to be highly favorable: Cost per mile could drop as low as $0.31 for single-person trips—in other words, lower by roughly two-thirds than the cost of driving today. Savings partly result from key assumptions around the availability of lighter-weight vehicles (for example, two-person pods for as little as $10,000) reducing capital costs, high rates of asset utilization (much higher than today’s 4 percent), and the value placed on freeing up driver time for more productive purposes.

The course of change

In our view, moves from the current state of mobility will likely occur fastest in the direction of shared access, in turn catalyzing the (upward) adoption of autonomous drive. We see this progression occurring in a number of steps, as illustrated in figure 7.

Step 1: Gradual adoption of shared access

The move from pure personal ownership of vehicles to a system more reliant on shared access (i.e., from quadrant 1 to quadrant 2 of figure 7), is already under way in some parts of the United States. For example, carsharing services, such as Zipcar, have roughly doubled their customer base in the last six years,25 while ridesharing services, such as Uber, have been adding 50,000 drivers per month and completed 140 million rides worldwide in 2014 alone.26 The software and hardware systems these services employ to match drivers with riders are evolving rapidly, incorporating information about observed behaviors to improve rider and driver experiences.27 Furthermore, intense competition offers the prospect of reducing market prices as improved economics related to increased asset utilization take hold.

Step 2: Tipping-point shift to driverless

Currently, wide acceptance of autonomous operation seems much further away than a broad carsharing/ridesharing culture.28 Sources of delay include the need to address existing technological limitations, such as sensor functioning in all weather and the wide availability of 3D mapping, as well as concerns over cyber security and liability.29 How quickly these and other issues are addressed will be a key determinant of the pace of adoption for autonomous drive.

Automakers—both in partnership and competition with tech firms—are sequentially and systematically pursuing a shift of control from driver-only to driver-assist to autonomous drive. If driverless technology were the only vector of change, uptake might gradually gain steam, following the pattern of adoption that has become classic to the automotive industry. In our view, this is the pathway from quadrant 1 to quadrant 3, incremental change to driverless revolution, which is well under way.

However, we also see change progressing along a second, parallel northward vector—from a world of carsharing toward a new age of accessible autonomy. Along this path, a powerful, additional boost toward driverless adoption is also under way. Uber recently partnered with both Carnegie Mellon University and the University of Arizona to open an Advanced Technologies Center in Pittsburgh and test driverless cars and optics for mapping technologies.30 Ridesharing services have economic incentives to accelerate the adoption of autonomous vehicles, since it could reduce one of the biggest operational costs in this system: the driver. These companies could capture a significant share of the consumer surplus value generated by reducing this cost. If autonomous drive becomes viable for ridesharing services, it could dramatically accelerate broad adoption, as consumers have greater opportunity to experience the technology while simultaneously realizing significant reductions in the cost of personal mobility.

Finally, other high-tech players are forging a third path to autonomous drive. For example, Google’s self-driving car program is testing cars that do not rely on driver-assist progression but, rather, immediately jump to fully autonomous; Google has stated publicly that “taking the driver out of the loop” is the safest path.31 And in the long term, it is still unclear whether Google intends to choose between supporting shared autonomous mobility, personal ownership, or both.

Rather than following the historical pattern for technological innovation, autonomous driving, when it arrives, could constitute a step-change. And the ensuing changes to the personal mobility ecosystem could unfold much more quickly than many companies can imagine. (See “Forces of delay—or acceleration.”)

Forces of delay—or acceleration

The inertial forces slowing down the process that Joseph Schumpeter called “creative destruction”32 in the realm of personal mobility are not to be underestimated. The table below summarizes the key drivers that could either significantly delay or accelerate the adoption of new technologies.

The future for the extended automotive industry

Deloitte’s recent Business Trends report “Business ecosystems come of age”33 describes a broad pattern by which many of the industries that make up the global economy are undergoing a kind of metamorphosis. What we inherited from the 20th century, the paper states, were “narrowly defined industries built around large, vertically integrated and mainly ‘self-contained’ corporations”—but in recent years, thanks largely to digital technologies, those monoliths have been fracturing into independent, tightly focused, highly interconnected businesses, many of which perform their specialized functions across former industry lines. We argue, “The fundamental boundaries that have specified the relationships, interactions, and possibilities of most businesses are rapidly blurring and dissolving.”34 The basic human needs that industries were built to serve remain, but serving them is now the work of much more fluid ecosystems. In the future mobility system, the mobility needs that today’s industries were built to serve remain, but much more fluid ecosystems will likely emerge to serve them. And this portends significant change to current business models—and partnerships (e.g., between insiders and disrupters) will be critical to deliver new mobility.

Complementary analysis from Deloitte’s Center for the Edge argues that a new mobility ecosystem could spark a “virtual” value chain in which the ability to capture, aggregate, and analyze mobility-related data becomes a tremendous source of value. In this vision, value will accrete to those who:

- Provide end-to-end seamless mobility

- Manage the mobility network operating system

- Holistically create and manage the in-vehicle experience

Rewards could be great for players that are able to capture, analyze, and (securely) monetize the awareness of where people travel to, the routes they take to get there, and what they do along the way. While third parties will no doubt pay for access to this information, perhaps the greatest value will be realized by new entrants who emerge as “trusted advisers” to help all of us navigate the new ecosystem and increase our “return on mobility.” These companies may also enable the ecosystem to monetize new services and ownership models.

The future mobility system will also need firms to develop and manage the vehicle-operating and traffic network information system that helps direct and control the movement of autonomous vehicles and shared mobility fleets. Technology companies already have access to passenger data and seek to capture this value, but they will likely face challenges from entrants with new business models.35 Vehicle manufacturers could design and develop vehicles not to accommodate drivers but, rather, to emphasize passenger experience, potentially giving rise to new vehicle structures and forms.

In the meantime, it is reasonable to anticipate a healthy tension between automakers, heavily invested in today’s product-centered system, and technological innovators looking to realize a more virtually dependent world of mobility options.36 And in this case, since shared driverless cars could decrease total auto sales, it’s no wonder why carmakers might be reluctant to embrace such a vision.

But there’s little question that some version, perhaps multiple versions, of a new ecosystem—one based on shared access and autonomous driving—will indeed eventually emerge. Where and when it does, the change could be profound: lower cost per mile, improved safety, reduced need for parking lots and traffic enforcement, dramatically lower overall environmental impact, and more. Questions revolve around what will happen to today’s automotive sector and how these will affect auto OEMs, suppliers, dealers, oil companies, fuel retailers, aftermarket service and parts companies, insurance companies, public and private parking, public-sector traffic enforcement, and others. However the forces of change unfold, every company may need to determine, in Roger Martin’s succinct phrasing, “where to play and how to win.”37

What follows is an initial overview of the enormous scope of change that could affect the key stakeholders in the current system as well as in the new mobility ecosystem.

Global automotive manufacturers (OEMs) face momentous and difficult decisions. The auto industry currently struggles with the fundamental economics of an intensely competitive business with enormous capital requirements; operating margins and return on invested capital remain low.38 The industry operates with sizeable excess production capacity: Globally, it is possible to produce 113 million vehicles annually, while sales hover around 70 million.39 In addition, regulatory requirements (such as CAFE, zero-emission vehicles, and safety standards) are becoming ever more stringent and costly.40 And consumers relentlessly demand that automakers integrate the latest technologies.

OEMs will need to determine if they should evolve from a (relatively) fixed capital production, first-transaction, product-sale business into one centered on being an end-to-end mobility services provider. This would represent a profound business-model change and the development of entirely new capabilities to be competitively and sustainably viable.

At a minimum, they will need to weigh how to meet the needs of a changing landscape as consumers increasingly use shared mobility and become interested in highly tailored, customized, personally owned autonomous-drive vehicles.41 This could require transforming product-development and innovation capabilities and reconfiguring supply chains and production operating systems to be even more lean, flexible, and “smart customization”-enabled. At the same time, consumers could begin demanding shared autonomous vehicles for different kinds of trips, which could spur the creation of more varied vehicle forms. This could drive the development of high-speed, low-cost vehicle assembly operations to create and produce vehicles with lightweight frames, custom experience-focused software, and highly customized, design-focused interiors. Light autonomous-drive vehicles can be made to be highly energy-efficient and, with a longer driving range, might make electric vehicles more viable and help automakers meet stringent regulatory standards.

Automotive suppliers will have to adjust as OEMs transform. As sales of autonomous-drive vehicles grow, suppliers will need lean, agile operations to serve the highly varying needs of the personally owned segment. While most of the core powertrain, chassis, brake systems, and electronic wiring components on such vehicles may be standard, giving suppliers some benefits of operational scale, the packaging for personally owned vehicles will likely be tailored and customized. Building the more standardized vehicles needed for shared mobility solutions could offer large volumes, and the demand will likely be for less complex and lower-value-added products; therefore, the economics in this new marketplace will strongly favor the lowest-cost producers.

Technology firms are driving much of the change under way. Earlier we referred to these firms as the disrupters; their strategic vision is that toppling longstanding institutional structures and frameworks can generate massive value. Unlike the manufacturers and asset holders in today’s system, they have few vested stakes in the current automotive ecosystem, and they view the market for mobility as a new frontier. They share a conviction that the system’s dominant source of value could be in creating and managing the operating system and in-transit experience as well as mining the data generated.

These companies have shown to be adept at building large, complex information networks and operating systems, introducing artificial intelligence to help minimize human error and randomness, creating compelling environments that drive consumer behavior, and creating digital communities. They view the vehicle as another platform in a multidevice world. Vehicle sensors and personal devices could generate ever-greater amounts of data, with insights producing personalized customer experiences and delivering targeted advertising and services.42 Integrated information systems can enable effective intermodal transportation. And mobile, wireless, location-based systems can create new opportunities for dynamic-pricing, single-payment, and consumption-based models to become much more prevalent. Technology leaders in general, relative to traditional auto-industry leaders, are in highly advantaged positions to capture this information and virtual-based value.

Cargo delivery and long-haul trucking currently face significant challenges that the future mobility ecosystem could alleviate. In the most ambitious version of the future, cargo transportation and delivery systems could become predominantly driverless through daisy chains or remote operation—an appealing scenario, considering the US trucking industry’s growing labor shortages, with as many as 30,000 driver positions unfilled and an annual turnover rate of 92 percent.43 Autonomous vehicles offer a way to overcome restrictions on hours driven and increase capital utilization. Given long-haul cargo transportation’s $700 billion in annual revenues,44 major fleets such as UPS and USPS have a sizeable economic incentive to actively explore how to operate for more extended time periods, cover longer distances without stops, and reduce the cost of drivers (accounting for 26 percent of operating costs).45 With such compelling economics, this sector could become an early test bed for driverless technologies.

Insurers face a complex set of strategic questions in how they will continue to grow their business and serve various segments, geographies, and demographic groups depending on which future states of mobility take hold. With $205 billion in premiums for personal liability, collision, and umbrella insurance in play, the stakes are high. Insurers today largely insure the vehicle and not the individual driver; they are currently unable to accurately assess risk associated with new forms of mobility and safety—ridesharing in the short term, and driverless cars and inter-modal transportation in the long term. Insurers need an operating model that fosters innovation and allows them to adapt to a rapidly changing market: As shared mobility continues to become more popular, insurers will need to evolve their business model to be more driver-centric, as there will be fewer vehicles to insure and more drivers using each one. With the emergence of autonomous drive, insurers will have to continue supporting vehicle and driver-centric models while developing new forms of transportation for the more technical, systemic failure risk associated with a driverless vehicle. This new system faces clearly significant issues associated with assigning liabilities: Risk pools morphing will likely force dramatic changes in insurers’ cost structure. The flood of new information provided by greater connectivity provides ways to offset these costs through more accurate ways to assign risk.

The US public sector will likely have to figure out how to offset anticipated declines in the $251 billion annually generated from fuel taxes, public-transportation fees, tolls, vehicle sales taxes, municipal parking, and registration and licensing fees. All these revenues are tied to today’s reality of individually owned and operated vehicles—for instance, the need for parking diminishes with the rise of autonomous-drive shared mobility. Agencies may need to evaluate alternatives—e.g., taxing “movement” versus ownership. Monetization for road usage in the future could transition to a much more dynamic model based on time of day, market demand, routes traveled, distance, and vehicle form, aligning the use of public assets more directly to usage than today’s system. On the other hand, as vehicle volumes decline, municipalities might experience reduced wear and tear on infrastructure and have the opportunity to reallocate parking and other space to more value-adding purposes. Government costs (such as the DMV) could decline significantly and potentially offset some of the public-sector revenue decline.

The value shifts for these and other industries could have a tremendous impact on revenues across the ecosystem. Figure 8 summarizes some of the potential effects of the shift to the future mobility ecosystem. The graphic also includes potential societal benefits expected as a result of autonomous drive and shared mobility technological advances. The analysis does not yet account for new business models that could evolve within the future ecosystem; it is meant to illustrate the potential effects/directional impact that autonomous cars and shared mobility may have on today’s ecosystem.

Conclusions

In the four futures of the mobility ecosystem, sources of value shift profoundly. With this evolution toward a new ecosystem still taking shape, we want to share some reflections on the strategic and operational implications for legacy incumbents, extended industry participants, and disrupters as they weigh their future direction. Specifically:

- Industries rise and fall. Cycles take long periods to play out, but eventually change occurs.

- The potential system benefits and fundamental economics of the disrupter vision are compelling.

- There is a pathway for the existing extended auto industry to lead the transition to the future of personal mobility, but it will require fundamental and expeditious business-model change. Competing effectively in the future mobility ecosystem requires building new and different capabilities. Everyone in today’s extended automotive sector needs to reassess how they will operate and create value while the four states coexist and in the longer term, when autonomous and shared mobility become more mainstream.

- The insiders and disrupters need each other. Unquestionably, fierce competition will characterize the commercial environment around personal mobility. Yet, despite their wariness and differing outlooks and perspectives, automotive incumbents and challenging new entrants will together make up a new ecosystem with high levels of interdependency, mutualism, and symbiosis.

- Profound disruption will extend far past the automotive industry. Every aspect of the modern economy based on the assumption of human-driven, personally owned vehicles will be challenged. Each company in this new ecosystem will have to determine where to play and how to win. As in any time of large-scale transformation, we can expect to see new players, with differentiated capabilities, emerge and change the fundamental dynamics of where and how value is created. Ultimately, the market, in its relentless quest for higher performance at lower cost, will decide who wins and who loses.

Deloitte will continue to periodically share insights about this evolution as part of an ongoing series. We aim to contribute to the dialogue as we all collectively wrestle with the impact and implications of the future of mobility. Our objective is to help to build a bridge between a highly uncertain futuristic vision, the realities of today’s industries, and potential pathways to alternative future realities.

The future of mobility: How transportation technology and social trends are creating a new business ecosystem is an independent publication and has not been authorized, sponsored, or otherwise approved by Apple Inc.