As Deloitte’s TMT Predictions 2021 outlines in more detail, we expect open RAN implementations to double in 2021, from 35 active deployments in 2020.1 We anticipate that momentum will accelerate rapidly as the technology matures due to the logic of its network design and strategic alignment with carrier needs. Besides opening the RAN market to new vendors, open RAN promises to lower capital and operating costs and drive greater innovation, making rural technology deployments more economically feasible.

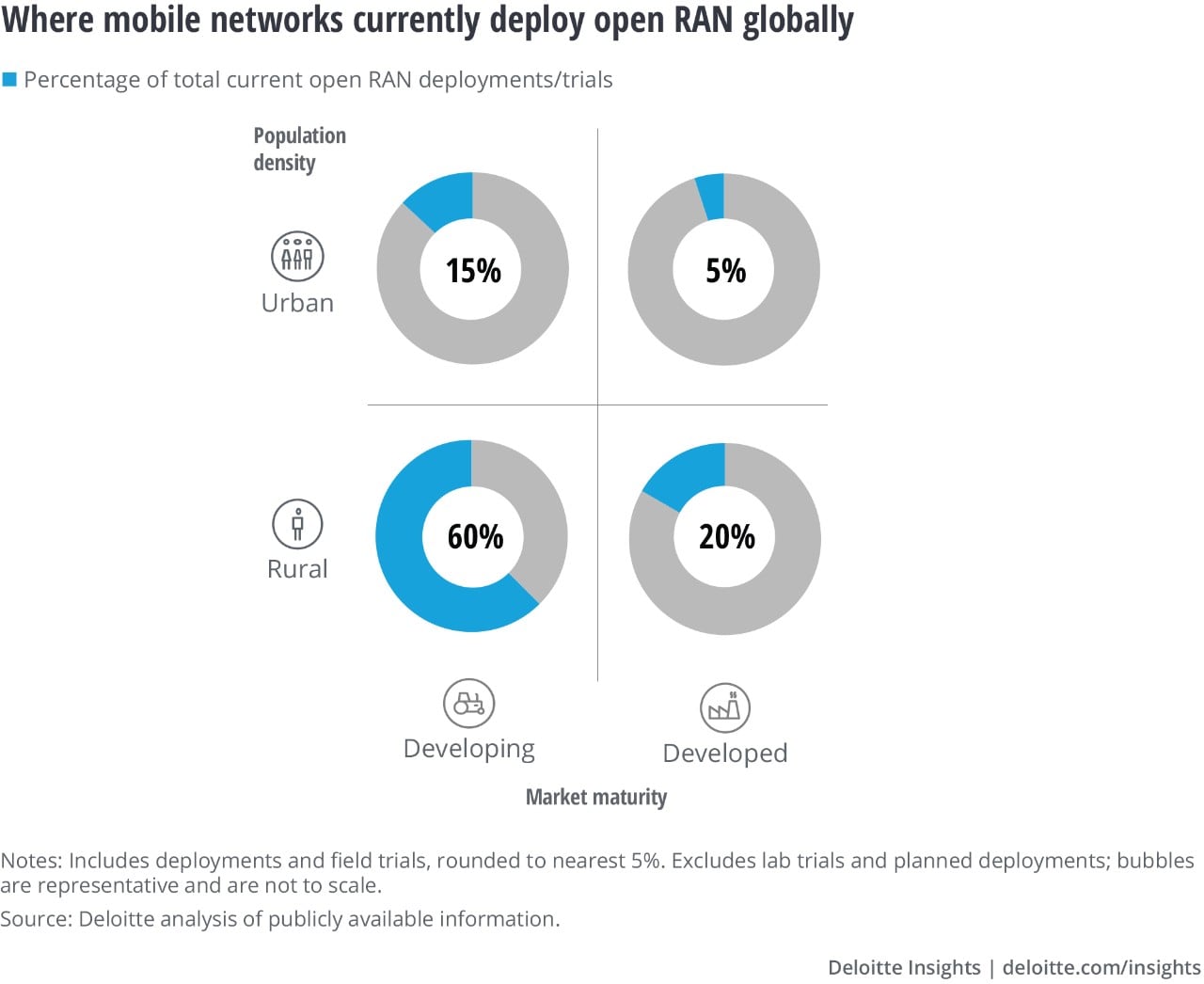

At this point, MNOs are focusing on second-tier markets—fully 60% of early open RAN deployments are currently located in developing markets, with another 20% in rural areas within developed markets.2 These observations are not wholly unexpected: MNOs are more likely to experiment with innovative new vendors and architectures in underserved areas, where the pressure for high performance and potential for stranded investment is lower. Moreover, relatively new and untried vendors are more likely to gain footholds in market scenarios where economic factors override service-level expectations. Comparatively low deployment costs make open RAN more economically feasible to enter or expand into underserved greenfield markets or rural areas with lower subscriber density.

While open RAN is gaining momentum worldwide, some operators remain skeptical—it offers many benefits, but the technology is still maturing, and there remain significant engineering and integration challenges. Open RAN also faces challenges in reaching performance parity with traditional systems, although that gap is rapidly closing. For now, issues affecting network performance and reliability are likely to give MNOs pause before introducing open RAN to core markets: The architecture’s scalability to larger networks with greater traffic loads and higher performance requirements remains unproven. Open RAN also requires a more hands-on approach by MNOs. Multivendor system integration, for example, is a significant challenge. The additional cost, time, and effort of validating new equipment vendors and testing compatible end-to-end network configurations could offset, if not completely negate, first-order benefits from vendor diversity. Understandably, some operators may prefer to postpone a potentially risky move and stick with traditional systems, in which they can look to a few trusted vendors to provide fully tested, carrier-grade solutions with turnkey deployment, maintenance, and integration support.3

As a result of these and other challenges, open RAN deployments have thus far been limited mainly to local and regional deployments. At this smaller scale, MNOs can more readily manage integration complexity and load on network functions. But as the technology matures, we anticipate more rapid acceleration in adoption and broader mass-scale deployments.

{kind=link}