A new dawn for European chips has been saved

The authors would like to thank Brandon Kulik, Christie Simons, Dan Hamling, Michel Vreedeveld, and Hilde Van de Velde for their contributions to this article.

Cover art by: Mark Milward.

Netherlands

Canada

India

United Kingdom

The European Union is mobilising over €43 billion to make itself more self-sufficient in semiconductors this decade.1 This is a critical objective, but there are multiple paths to greater resilience, each of which involves significant trade-offs. On which semiconductor technologies should Europe focus? Which parts of the value chain make the most sense for Europe to develop? If factories are built, where will demand and talent come from?

Our aim with this report is to educate and inform semiconductor buyers, as well as investors, governments and regulators. The study explains the multiple types of players and semiconductors that make up this complex and critical industry, Europe’s current role in it as well as the one it could have in the years to come. The European Union’s bold goal is to double its share of global production capacity to 20 per cent by 2030 from ten per cent in 2021.2 As the worldwide semiconductor industry is expected to double its output by 2030, if the EU were to double its share, it would need to quadruple its semiconductor output.

Deloitte will look at the possible paths for Europe within the scenario-based framework developed in 2022 and first published in The Future of the Tech Sector in Europe.3 The scenarios span from the optimistic but possible, such as European tech companies achieving trillion-dollar valuations, to the unlikely but not impossible scenario of failing to create or deploy technology effectively.

One of Europe’s big choices is deciding which generation of semiconductor technology to focus on. Deloitte believes leading-edge semiconductors will be important in the future, but chips made through older processes will remain critical to multiple core European industries. These include transportation, especially car manufacturing, health care and factories in general.

A second big choice is to determine which parts of the industry Europe should prioritise, given that no individual country or region can become fully self-sufficient in all types of semiconductors and parts of the supply chain by 2030.

Finally, Europe will need to find a balance between supply chain localisation and supply chain diversification. Not everything needs to be in Europe. Places like Japan, Singapore or the US are trusted and friendly alternatives. However, although this diversifies supply outside the current over-concentration in China, South Korea and Taiwan, they are still far away from Europe. This could have profound supply chain implications.

Most of our focus in this report will be on the EU and the EU Chips Act, which includes both direct money from the EU and member states (€11 billion in the Chips for Europe Initiative), with the balance of €32 billion coming from public-private partnerships.4 However, there are critical non-EU states still within the European zone: for the tech and semiconductor ecosystems these are notably Norway, Turkey, Switzerland, Ukraine and the UK.

European decision-makers must make many choices to optimise the continent’s semiconductor industry. Decisions will affect both the suppliers of semis and the major buyers – among them, key industries such as the automotive sector.

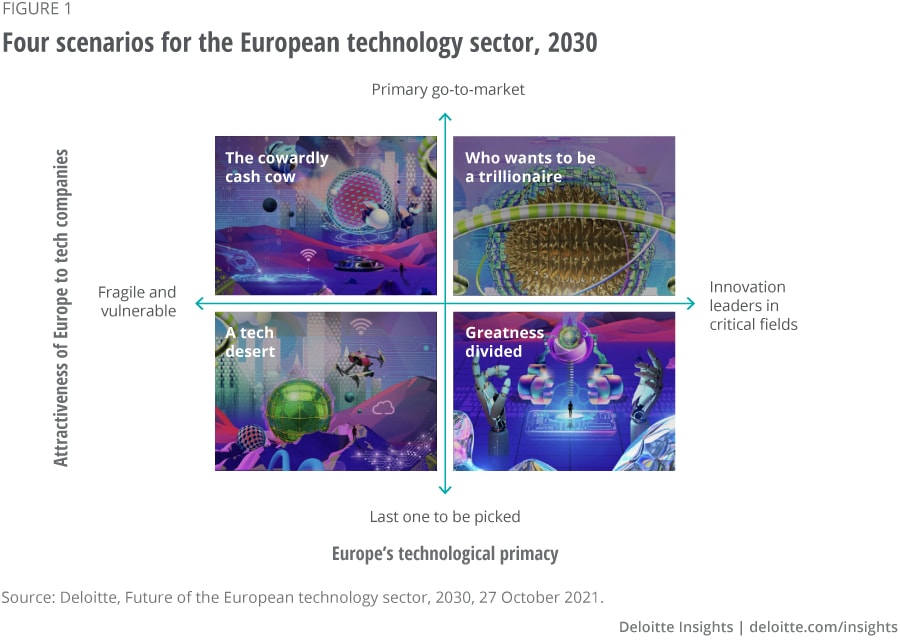

Deloitte has created four scenarios for the wider European technology sector (figure 1).

The ‘Who wants to be a trillionaire scenario’ describes a scenario in which a European-headquartered company has a trillion-dollar valuation. This is possible – and most likely for companies already in the market for decades. As of Q3 2022, there are no pure-play semiconductor companies globally that are close to a trillion-dollar valuation, but there are several with a market cap of several hundred billion dollars.

A second scenario, ‘Greatness divided’, describes a continent where a minority of countries are centres of excellence. This scenario closely describes where Europe is now, with companies such as ASML in the Netherlands being a world leader in chip-making equipment. NXP, ST Microelectronics (both also Dutch), and Infineon (Germany) are significant manufacturers of semis. ARM, headquartered in the UK, is the leading provider of processor intellectual property (IP), while STMicroelectronics factories in France are leaders in new kinds of semiconductor materials.

Were this scenario to persist until 2030, that is with a few specialist companies concentrated in a handful of Europe’s 44 countries, it may imply that other countries were unable to nurture companies of a similar scale. Given the time and resources required to, for example, create, staff and power a fabrication plant, or to develop a specialist design capability at scale, this scenario is probable in Europe as of the end of the decade.

In the ‘Cowardly cash cow scenario’, European companies are major buyers and users of technology created outside the region. As this report mentions, Europe is a net importer of semis: it consumes about 20 per cent of the global chip supply but manufactures only about nine per cent.5 Given the scale of growth in the semis industry and the pace at which new factories can be built, Europe could remain a net importer of semis as of 2030, despite the best efforts of the EU Chips Act. All inputs enable value to be created, and as has been demonstrated over the last couple of years, semis are fundamental to the automotive sector. European car manufacturers need these components, but supply may not need to come from European plants, as discussed in this report.

The final scenario, the ‘Tech desert’, describes an unlikely scenario where there is little technology supply and constraints on its application, principally because of regulation. This scenario is not currently applicable anywhere in Europe and is unlikely as of 2030, particularly given the growing recognition of the strategic importance of semiconductors. Although European regulators are looking closely at privacy and artificial intelligence (AI) and smartphone technology, they have not been proposing higher levels of regulation for chips or chipmaking.

The EU consumes twice as many chips as it manufactures. This situation has both supply chain and geopolitical risks – a situation the EU seeks to address. This section provides a general overview of the semiconductor industry, a description of the chips created and the manufacturing process before exploring the reason for the current semiconductor shortage and the geopolitical risks surrounding the current geographic concentration of semiconductor clusters.

Semiconductors (also referred to as integrated circuits (ICs), microchips, semis or simply chips) are everywhere. They have become an essential component of electronic devices, enabling advances in clean energy, communications, computing, healthcare, military systems, transportation and countless other applications in the modern world.

The global semiconductor industry is predicted to reach US$633 billion in 2022,6 up 55 per cent from 2019.7 The industry may hit US$1 trillion in revenue by 2030, which is about six per cent annual growth.8

The EU currently consumes about 20 per cent of the global chip supply but manufactures only about nine per cent.9 And it’s not catching up: in 2020 and 2021, European spending on equipment for making chips was just 3.7 per cent and 3.2 per cent of total global spending for those years respectively.10

This situation poses critical risks for Europe, which have become evident during recent shortages. Various chips have been in short supply since 2020 owing to supply chain issues caused by COVID-19 but also other factors, and the impact has been widespread.

Shortages have affected many consumer devices, notably smartphones, computers, gaming consoles and consumer appliances. Resources such as data centres, which are multiplying rapidly, have also been affected. Transportation (especially automotive, aeroplanes and trains) and healthcare have also been affected.

The situation caused an estimated global sales shortfall of US$210 billion in 2021 for the automotive industry alone.11 In the EU, new car sales in 2021 were 9.7 million vehicles, a record low since 1990 and 3.3 million lower than in 2019.12

As of March 2022, chip lead times averaged 26.6 weeks,13 with some being over 52 weeks.14 In May 2022, Intel’s CEO Pat Gelsinger predicted that the shortage would last well into 2024, making this among the longest chip shortages in history.15

New capacity is being built (see below), but it takes time to develop and scale up. That said, a combination of new plants and possibly weakening demand in the short term from higher interest rates, inflation and falling consumer confidence should bring the market back into balance.

Some chips are used for complex digital processing or memory: these tend to have billions of transistors, rely on the latest and most advanced semiconductor-manufacturing technologies and are fundamental to computers, smartphones and data centres. Other chips need more power, different materials or have circuits that need to be less binary: neither on nor off, but somewhere in between (analogue or mixed-signal chips). These work better on older and less advanced manufacturing technologies. They are found in audio and video equipment, autos, medical devices, radio and communications and industrial process controllers to control factory machines.

In 2021, the average chip cost US$0.48, with a volume of 1.15 trillion chips sold and total revenues of US$556 billion.16 However, there is a massive variation in price per chip, from over US$1,000 for innovative chips in high-performance computers to a few cents for a commodity chip with limited functions. Assuming 2026 EU vehicle sales of about 14 million and average semiconductor content of US$700 per vehicle,17 EU automotive demand for chips alone may generate nearly US$10 billion annually.

So, multiple generations of chips are produced at any given time, and each has its specific applications:

What constitutes advanced and trailing nodes changes over time. Presently, 10 nanometres (nm) and under is generally considered advanced; 65 nm and above is trailing and 14–45 nm is intermediate. These nodes do not correspond exactly to the physical size of the chips’ features, but they are currently just agreed-upon industry shorthand terms for describing manufacturing processes.

Annual advances in device performance rely on the evolution of ever smaller architectures. In general, smaller (fewer nm) is more advanced and, in some contexts, better, especially for memory or logic (processor) chips. Manufacturers can place more transistors per square millimetre, allowing chips to be faster, more powerful, use less battery life, emit less heat and be smaller or be cheaper (or some mix of all). All other things being equal, a 5 nm central processing unit (CPU) is better than a 10 nm CPU, as it uses less power and packs more transistors into a smaller area.

As well as there being multiple generations of chips, there are also multiple types of semiconductors. A high-level list includes analogue, connectivity, discrete, DRAM and NAND memory, general purpose logic, microcontrollers (MCUs), microprocessors and more. Analogue ICs, MCUs or power management chips are almost exclusively made at trailing node processes, and smaller isn’t necessarily better.

Many of the chips that European car manufacturers currently lack are trailing nodes rather than the logic and memory chips used in computers, data centres and smartphones. Trailing edge node chips are also used in health care devices and household appliances. Factories and manufacturing primarily need trailing node chips as well.

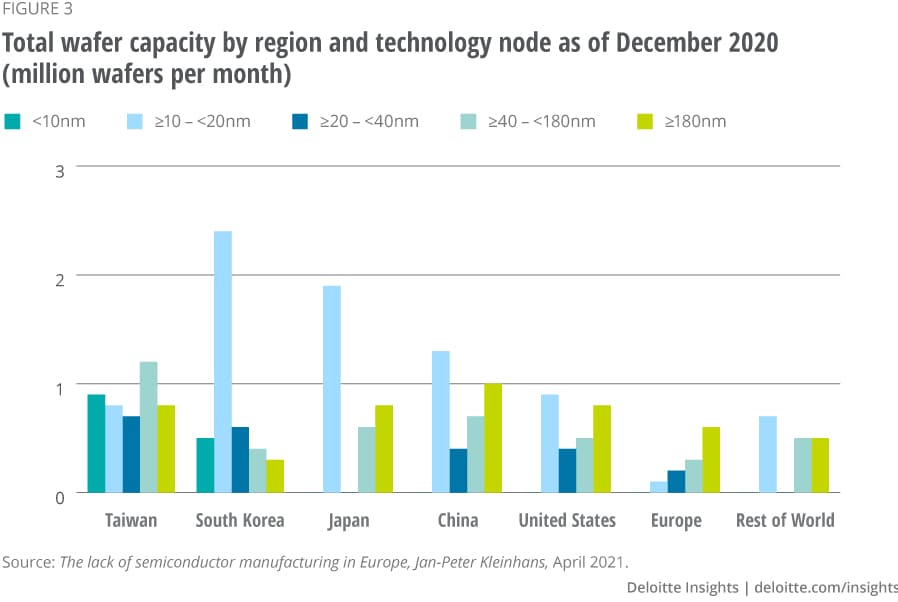

As of 2022, measured by wafer equivalents (see next section for an explanation of wafers), about 64 per cent of global chip capacity is trailing at 65 nm and above, with another 25 per cent being intermediate and ten per cent being advanced.18 Over time, this will shift.

Advanced node is forecast to grow at over 20 per cent annually for the next few years, intermediate at ten per cent, while trailing is below ten per cent. Despite this change, even in 2025, trailing is expected to represent more than half of the global chip capacity.19 This does not equate to value, however. In 2022, the 64 per cent of capacity for trailing equates to only about ten per cent of global chip revenue.

As of December 2020, the European split for capacity by node was zero per cent advanced, 33 per cent intermediate and 67 per cent trailing (figure 2).20 Taiwan and South Korea are currently responsible for 100 per cent of advanced node chip manufacturing.

All chips are made in fabrication plants, referred to as ‘fabs’. Some companies that own fabs both design and manufacture chips. These are called integrated device manufacturers (IDMs). Intel is one example. Companies that own fabs but do not design chips are called foundries. They make chips for ‘fabless’ companies that only design chips. TSMC is a foundry.

Apple is a fabless chip company that uses reference designs from UK-headquartered ARM. Some companies with fabs both design and build chips and act as a foundry. Samsung is an example, and Intel is moving toward this hybrid model.

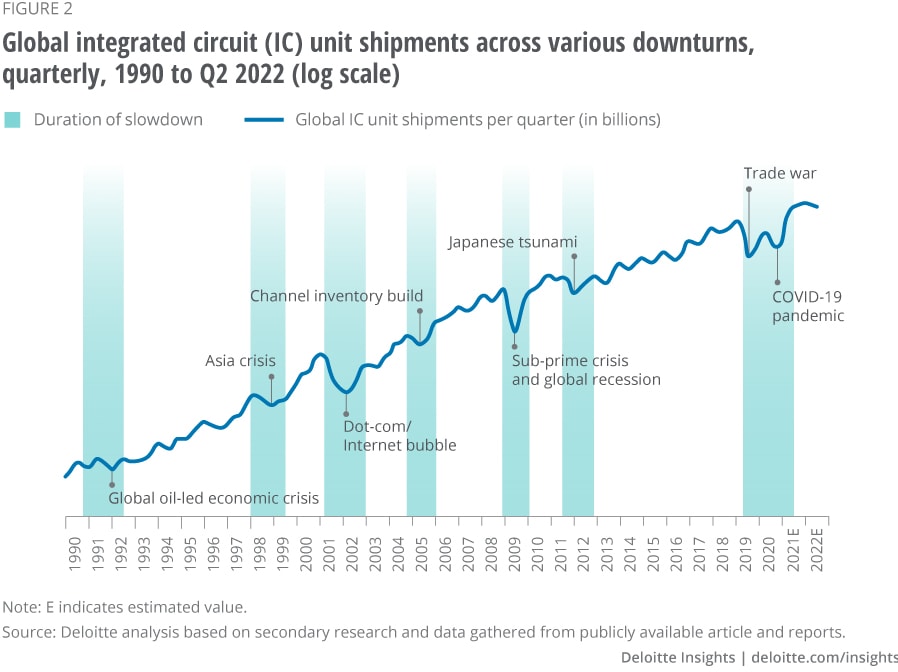

The chip-manufacturing industry and supply chains are vulnerable to disruptions, which makes shortages inevitable. Over the last three decades, there have been six shortages of roughly similar duration or magnitude to the current shortage (figure 2).21 Shortages are typically provoked by a specific event, such as a natural disaster, economic downturn or pandemic, and have often been followed by periods of oversupply.

It typically takes up to three years for a new chip plant to reach volume production. Although governments are spending tens of billions for additional capacity, the current shortage will likely be over by then (due to new capacity and concerns about the Ukraine war, interest rates, inflation and falling consumer confidence in Europe and elsewhere).

So, the current wave of incentives and investments initiated by governments is more about preparing for the next shortage, or maybe even the one after that, and remaining competitive. We don’t know what the next trigger event will be, but there will undoubtedly be one.

The manufacturing of chips is highly concentrated in East Asia. In 2020, 73 per cent of all chip manufacturing was done in four East Asian countries (China, Japan, South Korea and Taiwan).22 Furthermore, 81 per cent of third-party semiconductor wafer manufacturing (foundry) was done in just two countries (South Korea and Taiwan). Taiwan alone accounted for 63 per cent of global foundry capacity.23

The current chip shortage shows how susceptible Europe is to supply disruption. The concentration of semiconductor manufacturing in Japan, South Korea and Taiwan poses a geopolitical risk to Europe due to the potential for conflict.

Even North Korea’s short-range Nodong and Puksokgong missiles can easily reach all Japanese and South Korean semiconductor clusters. Mainland China also continues to assert territorial claims over Taiwan and has threatened to retake the island by military force.

The supply impacts of any conflict in the region could include damage (short term or long term) to or the destruction of fabrication, testing, assembly and warehousing facilities. Even if the infrastructure were undamaged, a successful Chinese takeover of Taiwan would almost certainly lead to embargoes or other restrictions on chips coming from the island.

Europe’s reliance on East Asian chip imports poses a specific geopolitical risk regarding military capabilities and vulnerabilities, as the Western response to the Russian invasion of Ukraine illustrates. As part of the sanctions imposed by the West on Russia, there has been a severeembargo on semiconductors since February, with Russian imports down by over 90 per cent.24

Semiconductors are vital for a modern military, and Russia has been reduced to using chips intended for appliances in weapons.25 European armies would be equally vulnerable to losing access to chips. Further, specific chips (high-power and radiation-hardened semiconductors) are critical for military applications.

The European Union has responded to the situation by announcing a €43 billion EU Chips Act in February of 2022, which is now going through the EU approval process. But Europe is not the only region responding.

In the US, the US$52 billion US CHIPS Act was introduced in January 2021 and passed by Congress in July 2022, it received executive approval in August 2022.26 China’s spending is substantially higher. It has been on a journey for over a decade towards greater semiconductor self-sufficiency and continues to build domestic capacity. It plans to spend US$1.4 trillion in 2020–2025 on a range of advanced technologies, including at least $150 billion on semiconductors.27

For the EU, the goal is to become more self-sufficient, as complete self-sufficiency is unattainable. President of the European Commission, Ursula von der Leyen, said in her remarks introducing the EU Chips Act: “It should be clear that no country – and even no continent – can be entirely self-sufficient.”28

This is because of the diversity of semiconductors made by multiple processes – from multiple semiconducting materials, relying on numerous other inputs (such as specialised epoxies) and a vast array of manufacturing, testing and assembly equipment. Sometimes, there is only a single manufacturer or source for a critical part. Any given plant or cluster can be shut down by drought, earthquake, fire, flood, military conflict, pandemic, power shortage or typhoon.

China’s role in chip production poses different geopolitical risks to Europe. The country is a significant source of industry concentration in the manufacturing of less advanced chips. It is trying to become more self-sufficient and catch up to other regions in making more advanced chips.

There are two immediate impacts on Europe. First, European manufacturers of semiconductor-manufacturing tools are under pressure from the US to not sell tools to China, which intensified in October 2022.29 Second, there are multiple other restrictions on technology transfer, concerns around Chinese takeovers and potential IP theft.

The previous section examined the general context of the EU’s decision to ramp up semiconductor manufacturing. This section addresses the many options and trade-offs the EU will have to consider to ensure investments are made wisely and have the greatest effect. In particular, these are 200 mm wafer vs 300 mm wafer production and the benefits and risks of localisation vs diversification.

The EU Chips Act supports growing EU capacity in advanced semiconductor manufacturing and tools, with a goal to have Europe be able to make 2 nm node chips by 2030.

Advanced node chips are essential for the latest generation of AI applications, computers, data centres, smartphones, supercomputers and memory. Meanwhile, the auto industry, consumer appliances, healthcare devices and most factory or manufacturing primarily need trailing node chips.

Given advanced node’s significantly higher value per unit, the EU’s focus on the most advanced technology is understandable. Some commentators argue that being able to play at 2 nm is a strategic necessity for Europe.30

Every approach inevitably has risks.31 Advanced node chip fabs cost up to US$20 billion to build. Operating costs are over US$1 billion per annum, and further billions in ongoing investment over a plant’s lifetime are required to remain state of the art. For an advanced node to be profitable, utilisation needs to average over 90 per cent.

Chips are made on large-but-thin wafers of ultra-pure silicon crystal that have been sliced, machined, etched, polished and manufactured from purified and processed silicon dioxide (usually from relatively pure quartzite rock). There are three standard wafer sizes: 150 mm or smaller (first made in 1983), 200 mm (1992) and 300 mm (2002). The latter is considered state of the art; 450 mm wafers have been proposed for 2025 but may be deferred even further.

At a high level, a 300 mm wafer contains twice as many dies as a 200 mm wafer: larger wafers can drive lower prices and increase yields, and most advanced node processes use 300 mm wafers. But there is no 1:1 correspondence: Manufacturers can make advanced node chips on smaller wafers or trailing node chips on larger wafers. As an example, the 2021 Bosch fab in Dresden creates 300 mm wafers but 65 nm node.33

All other things being equal, fabs for 300 mm wafers cost much more than 200 mm wafers: about five times as much in terms of initial construction and ongoing costs.

As of 2022, about five per cent of global wafer capacity (not revenues) is 150 mm or smaller, 42 per cent is 200 mm and 53 per cent is 300 mm – but the latter is growing faster. By 2024, we expect 59 per cent of capacity to be 300 mm. Europe does have some production capacity for 300 mm wafers, but it is behind Asia and the US.34

There may need to be a discussion around the right mix of 200 mm and 300 mm wafer plants in the EU. Although 300 mm is state of the art, there is a premium. It might make more sense for Europe to build two 200 mm wafer fabs than a single 300 mm wafer fab for any given node or type of chip.

One important debate globally around semiconductor self-sufficiency concerns location. The issue is the extent to which design, manufacturing, materials, talent and testing need to be located inside a given country or group of countries and which of those capabilities can be located in a nearby country (near-shoring) or in a country that is not nearby but that is considered geopolitically safe and reliable (‘friend-shoring’).

The EU/Europe and the US face the same two challenges to becoming more self-sufficient in semiconductors. Most of the world’s chips are manufactured far away and are concentrated in a small set of factories/countries. These problems are even more acute for advanced node chips and foundry manufacturing.

Building more fabs in the EU/Europe or the US is the obvious answer: this creates more diverse sources, and the supply chain is much shorter. But full localisation for EU/Europe is likely expensive and, some argue, impractical.

As the president of the European Commission said in her remarks, “Europe will build partnerships on chips with like-minded partners, for example, the US or, for example, Japan.”

For Europe to rely almost entirely on South Korea and Taiwan is unwise. But while having second or third sources of supply in Japan or the US is good for diversification, it does little for supply chain length: Silicon Valley, Taiwan and Tokyo are roughly the same distance from Europe.

Although some chips are shipped by air, lower-value chips and all the machinery necessary for building and operating fabs tend to travel by sea: as an example, TSMC chartered an entire box ship to outfit a new fab.35 Diversifying supply to Japan or the US would result in much longer shipping times for those in Europe: New York to Rotterdam is eight to ten days, while Yokohama to Rotterdam is 28 days, compared to one to two days for most intra-European transport by truck or rail.

It is important to note that, to some extent, the existing big three chipmakers may be thinking of capacity expansion outside South Korea and Taiwan in a binary way. It may be either Europe or the US: adding capacity in both regions may be unaffordable.

As a 2022 US brokerage report put it, “The demand for silicon is out there and the capacity needed is there as well. The question is where this capacity will be built – in the US or in another region … Either US chipmakers build new capacity in the US with government support or they will take it elsewhere to ‘friendlier’ regions and get the necessary financial support.”36

Partnering with Japan and the US will be necessary – Europe cannot go it alone. That said, there need to be discussions about which plants need to be inside the EU (localisation) and which can be tens of thousands of kilometres away but not in South Korea/Taiwan (diversification). Although Europe cannot be completely self-sufficient, having as much local capacity as possible is a worthwhile goal. One interesting choice will be the idea of having not just more chip plants in Europe … but having both IDM and foundry chip plants. Having foundry capacity might spur growth in Europe’s fabless ecosystem, which is much weaker than in the US.

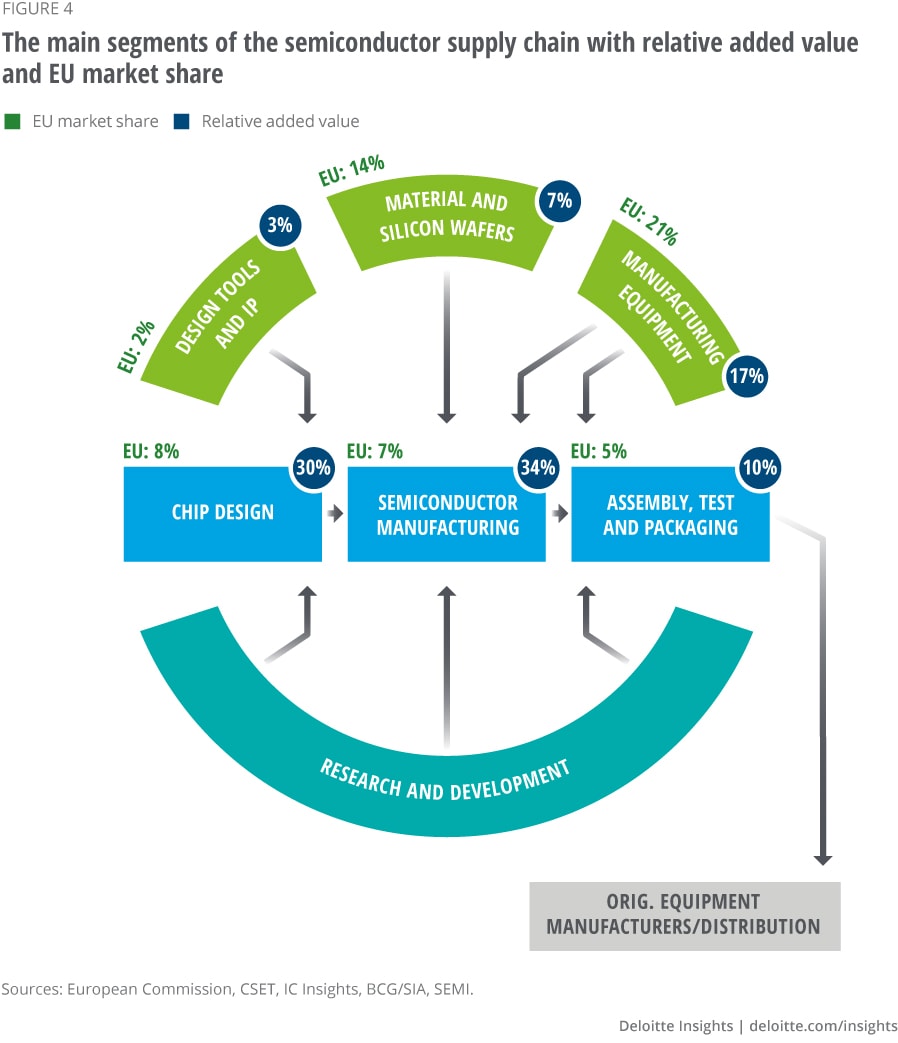

Fabs are critical pieces within the infrastructure of semiconductor manufacturing but there are many other important aspects that the EU must consider when planning for success within the industry. These include materials, equipment, substrates, and assembly, test and packing (ATP).

At US$20 billion each, it is understandable that advanced node fabs tend to dominate the discussion. But fabs are just one of the many critical elements in the creation of semiconductors. Semiconductor manufacturing requires design, equipment and materials. And once wafers are finished, they still need to be cut into dies, placed on substrates that provide physical support and electrical connections and then tested, packaged and shipped (known as the back end).

As seen in the figure 3 (from the EU), the region has several glaring areas of weakness, with rectangles shaded pink/red.37 The EU consumes about 20 per cent of chips globally, but the region’s share of chip design, design tools and IP, semiconductor manufacturing and assembly, test and packaging are in the single digits.

The situation is slightly better for materials and wafers. In terms of manufacturing equipment, the region’s share is in line with consumption. It is worth noting that some parts of the supply chain are worth more: the relative added value of each component is indicated below, with 64 per cent of value-adds coming from chip design and manufacturing.

Building new fabs in Europe but keeping all of the back-end processes in Asia lengthens supply. Chips made in Europe would need to be shipped to Asia for back-end processing, then shipped back to Europe for assembly or to final consumer or enterprise buyers.

Europe is not self-sufficient in many raw materials required to make chips. A partial list of raw and refined/processed materials needed to make various types of chips include: argon, enriched isotopes (D2 aka deuterium, boron 11), fluorspar, germanium, helium, hydrogen peroxide, high-purity solvents (IPA/PGMEA), krypton, liquid hydrogen, sulphuric acid, tantalum, neon and xenon.

Some of these are not raw materials but ultra-pure versions needed for semiconductor usage. Neon is abundant, but half of the world’s semiconductor-grade neon comes from two companies with purification plants in Ukraine.38

Europe is either not self-sufficient in many of these or relies on a handful of sources, some of which are subject to significant geopolitical or other risks, particularly around sustainability and environmental impact. Current or future military conflicts could deprive European fabs of necessary materials.

Europe is poised to be relatively self-sufficient in terms of chips made from newer materials.

Most of the semiconductors we usually discuss are made wholly out of silicon. This material has many virtues. It is especially good at running on minuscule amounts of current at low voltages. This enables billions of transistors to be concentrated in a tiny wafer and work for hours powered by a compact smartphone battery. Arrays of silicon-based semiconductors are placed in data centres without generating excessive heat.

But sometimes chips capable of handling high voltages and currents are needed for applications such as solar panels, wind turbines, military, aerospace and (especially) electric vehicles. Silicon can’t handle high voltages and currents well. New materials such as gallium nitride (GaN) and silicon carbide (SiC) can run at hundreds or even thousands of volts and are emerging multibillion-dollar annual markets.

With more than 40 million battery-operated electric vehicles expected on EU roads by 2030,39 these emerging semiconductor materials are likely to be critical for European automakers. In good news, manufacturers such as ST are building a US$3.4 billion European ‘gigafactory’ for these kinds of chips.40

Many types of tools are required to make chips and Europe is self-sufficient in only some major ones. One essential tool is a photolithography or lithography system, which is used to draw the features on the silicon wafer. Thanks to ASML, Europe is a powerhouse in photolithography.

ASML has over 60 per cent share and 100 per cent share of the equipment used for deep ultraviolet lithography (DUV) and extreme ultraviolet (EUV) lithography respectively, both cornerstones of advanced node manufacturing. In addition to lithography, many other tools are required for deposition, etching and cleaning, metrology, process control, ion implanting, plus test, assembly and material handling. In most of these, Europe is generally not self-sufficient.

Europe has a minimal share of the semiconductor design market. One of the most important and valuable parts of the semiconductor industry is the fabless semiconductor companies that create the designs for chips that are, in turn, made by the foundries, such as TSMC and Samsung (and Intel going forward).

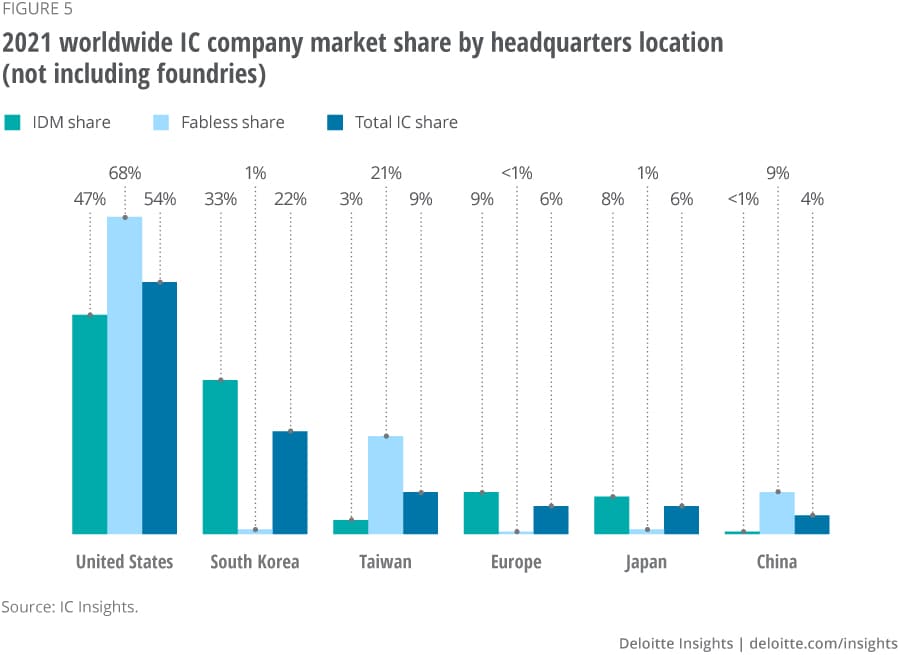

In 2020, fabless chip companies made up 33 per cent of global chip sales, up from 13 per cent in 2002.41 As of 2021, Europe’s share of fabless chip company headquarters was less than one per cent of the global total. This compares to the US at 68 per cent and Taiwan at 21 per cent (figure 4).42 As mentioned earlier, prioritising a European foundry might help strengthen this sector.

Europe currently has minimal capacity to make substrates. Increasing domestic chip-manufacturing capacity is necessary. For the chips to function, they need to be placed on substrates, which are the things that connect the chips to the circuit boards.

As of 2022, Europe has minimal capacity to make advanced IC substrates that support the most advanced package types, such as flip chip ball grid array (FCBGA) or flip chip chip scale package (FCCSP), found mainly in higher-end products. Europe has limited capacity to manufacture even lower-end wired bonded substrates. Building high-volume advanced substrate manufacturing facilities would likely cost US$1 billion each, and more than one would be needed.

These steps are vital and are either done by the integrated device manufacturer or an outsourced semiconductor assembly and test (OSAT) provider. For context, figure 5 shows the global distribution of the 475 different IDM and OSAT facilities.43

Currently, the EU share of the global back-end capacity is about five per cent, even lower than its share of chip manufacturing.44 Intel has announced a back-end facility in Italy. Still, many more are needed, requiring billions in investments.

All the new fabs in the world will not make a difference unless skilled employees are available to work in them. Europe faces a significant shortage in attaining qualified workers, a situation that could grow worse over the coming decade.

The global semiconductor industry had about 2 million direct employees worldwide in 2021,45 and Deloitte predicts that an additional 1 million skilled workers will be needed by 2030 globally – or over 100,000 annually. For context, there were only about 150,000 information and communication technologies graduates in the EU in 2018.46

There are multiple talent requirements for each step of the semiconductor process. A large fabless semiconductor company might require 100 doctorate-level designers at the design stage. A large fab needs about 4,000 workers with skills in production engineering, logistics and support and production operations, although the talent and skills required are changing as technology evolves with more automation, analytics and agility.47 Finally, a big OSAT plant might also have thousands of workers with different and lower-level skills.

The EU has talent complexities: although there is free movement of workers within the EU, language is a barrier, especially for technical work, in a way that isn’t in Japan or the US. EU labour laws are also sharply different from other jurisdictions, as are the educational systems (universities and vocational).

According to one European semiconductor industry HR expert, Henryk Schoder, X-FAB Group: “The talent shortage is the biggest challenge to semiconductor industry growth in Europe and globally.”48

Increasing semiconductor manufacturing raises questions concerning environmental, social and corporate governance (ESG), which will also need to be considered as part of the EU’s plans.

Global chip manufacturing will cause about 0.1 per cent of global greenhouse gas (GHG) emissions in 2022. That number is projected to grow to 1.5 per cent by 2030 if the industry doesn’t act.50 Further, the industry also uses a lot of water, produces waste and relies on multiple materials whose extraction has environmental impacts. Individual companies and industry associations are working hard to do better on all counts.

But localisation and diversification of semi manufacturing and supply chains mean some complex trade-offs are required. In short, the likely impact of the EU Chips Act on ESG is neither purely positive nor negative, but rather a mix of the two.

In good news, making more chips in European countries with low GHG emission intensity (France, Luxembourg and Sweden are all under 65 grams of CO2 equivalent per kilowatt hour)51 and fewer chips in a country where more than 60 per cent of electricity generation comes from coal is an ESG win.52 Equally, having more chip workers in Europe, with generally higher wages and better working conditions, suggests making Europe stronger in chip making and all parts of the supply chain would be a positive achievement. Finally, shipping chips and equipment over shorter distances will further reduce the carbon footprint of chips consumed in Europe.

But there’s bad news too. Building and operating new chip plants consumes many resources: energy, water and carbon-emitting concrete. Suppose additional capacity is added in Europe (and in the US and elsewhere) to reduce industry concentration and supply chain risk. In that case, it is a virtual certainty that the industry will fall from the current (and already unsustainable) 95 per cent utilisation level.53 That’s a good thing in some ways, but – over time – if industry utilisation falls too far, the industry will become less efficient and more wasteful.

One complicating factor is the EU’s reliance on Russian gas: semi manufacturing is energy intensive and requires ultra-reliable sources.

In line with an overall improvement in ESG factors for the chip industry, Europe will want to optimize the Chips Act and its goal of becoming more self-sufficient in chip manufacturing. That said, given the need for electricity in manufacturing, the benefit of moving more production from less green’ countries today to a ‘greener’ Europe suggests that there will be a significant ESG benefit to the EU Chips Act.

In our four scenarios for the future of tech in Europe, the most desirable is to have a trillion-dollar tech company headquartered here. The tech desert is the least desirable, while the greatness-divided option is a good outcome. The EU Chips Act and associated strategies won’t guarantee a trillion-dollar company or avoid a tech desert – but it helps. The cliché that ‘chips are the new oil’ is overused but it is a cliché for a reason.

Reducing Europe’s chips dependency is critical to ensure that European industries that rely on chips (which will increasingly be all of them) have ringfenced supply during future shortages. Making sure that Europe is the site of at least some leading-edge fabs and other critical parts of the supply chain (such as ATP and chip design) is also of paramount importance.

The EU Chips Act is an essential beginning to all these goals. Much remains to be done, choices must be made, partnerships with other countries will be necessary, and talent needs to be developed or imported. But being stronger and more resilient in chips means a stronger and more resilient tech sector in Europe, which means a stronger and more resilient Europe economically, competitively, militarily and politically.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

_ET2020.png){kind=link}