Taking a combined approach toward digital transformation by addressing business, technology, and workforce and operational considerations can enable them to be more adaptive to future supply chain-driven business disruptions.18

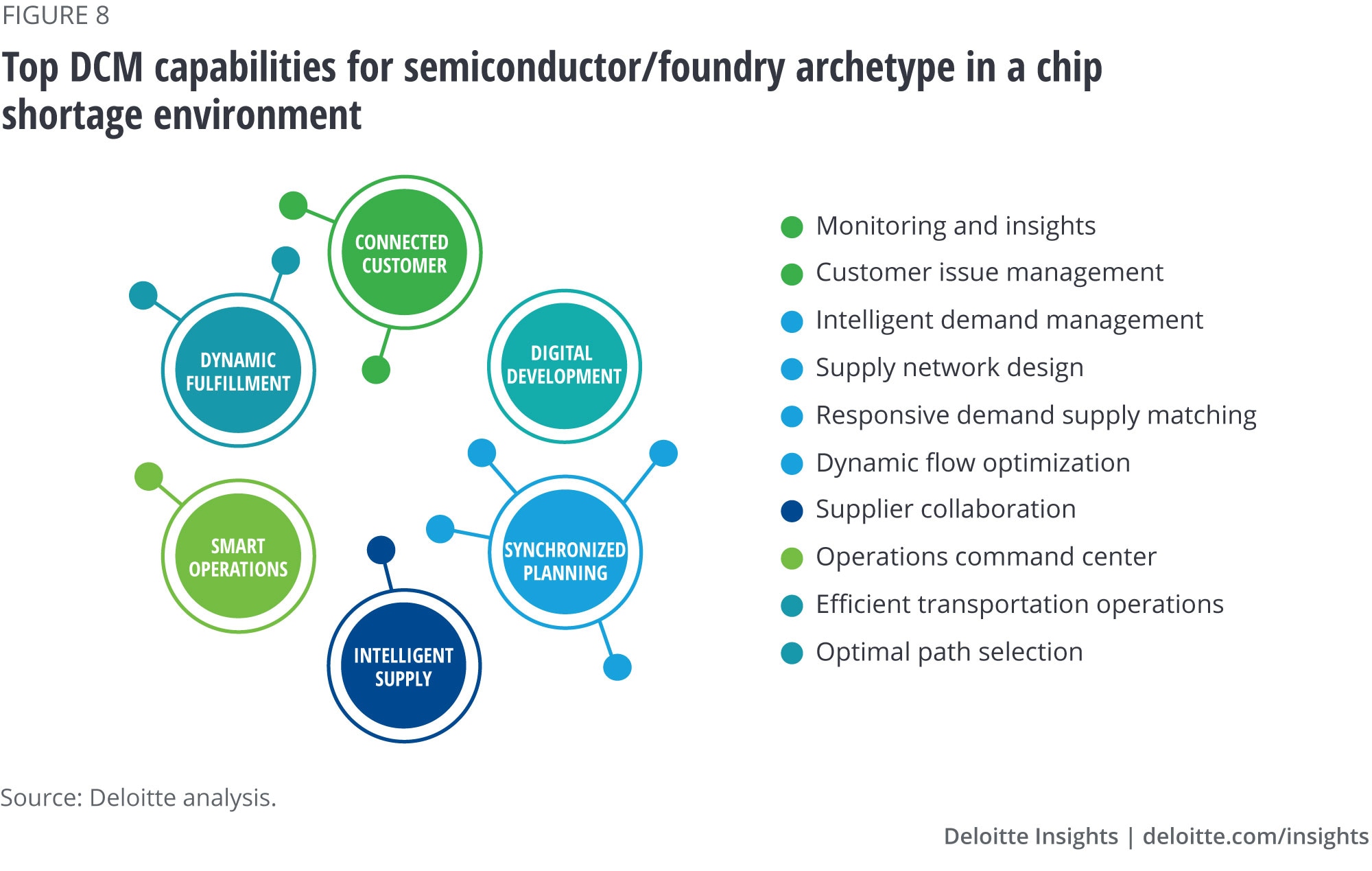

Semiconductor companies should consider keeping the end-customer demand patterns and buying experience at the core of their transformation approach, which requires working with supplier tiers (both upstream and downstream), distribution channel partners, and third-party logistics and transportation providers. By collaborating with their supply network partners, they can implement the advanced technologies they need such as blockchain, sensors, AI/ML, mobile, and broadband tech. These technologies can advance their business processes and enhance data access and analytics across their extended supply network.

This strategy-based digital/tech-enabled transformation can help them gain greater visibility and insight into demand patterns. That can enable them to proactively manage capacity, production, inventory, and shipments, which in turn lets them build measured slack into their supply chain, allowing them to adapt and thrive in the face of any future disruptions.

Conclusion

As semiconductor companies navigate through this period of shortages and prepare for future shortage events, leaders should consider the following questions:

- Can I add incremental or bulk capacity in the near term?

- Can I geographically shift my capacity footprint to reduce risk in my supply network?

- Can I adjust supply arrangements and strategic inventory buffers to improve service levels?

- Can I leverage digital supply network capabilities to achieve the agility and visibility I need?

- Will my transformation effort address this and future shortages?

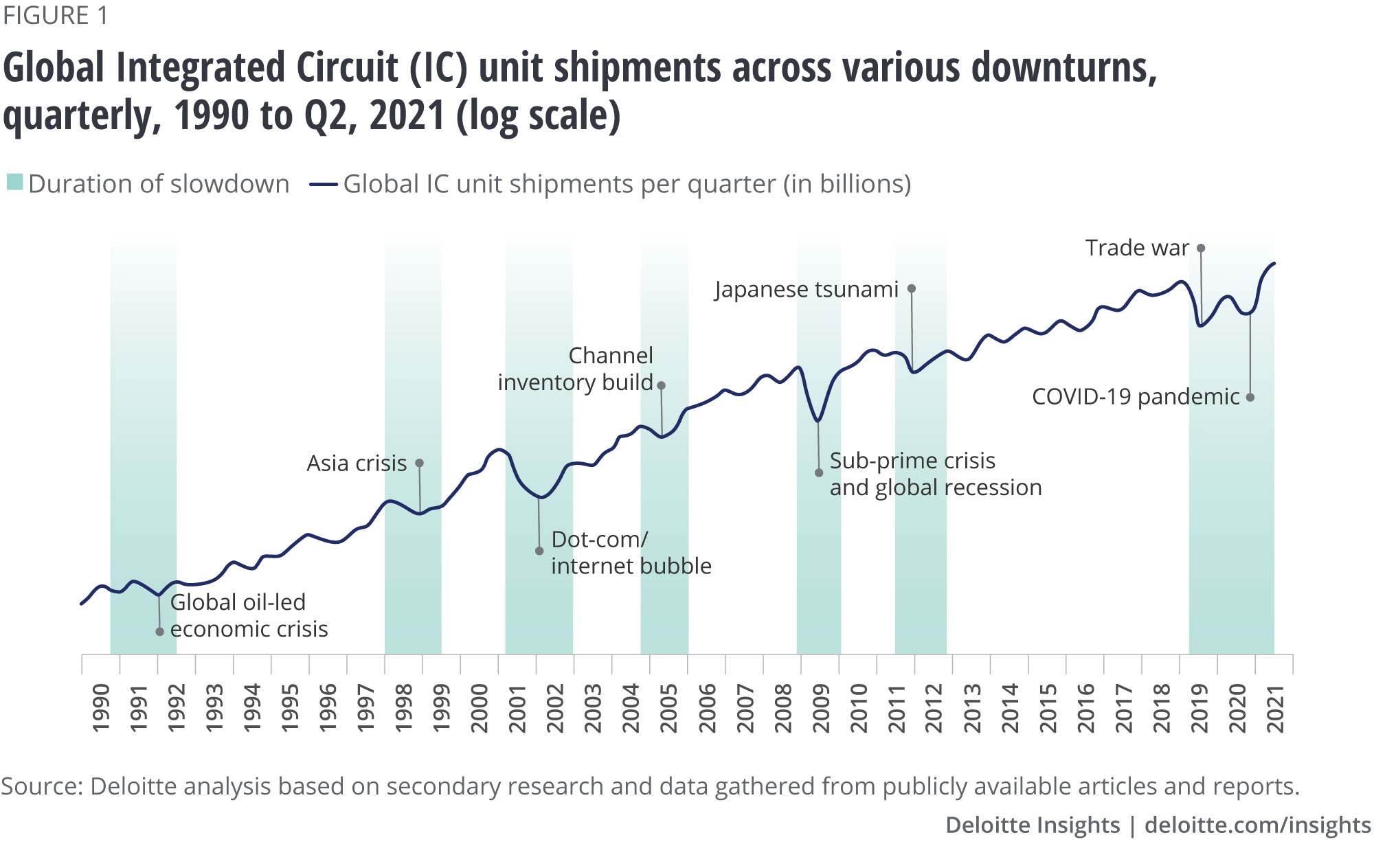

The semiconductor supply volatility which we are experiencing today will likely not be the last. To better prepare and deal with such future disruptions, companies in the broader semiconductor industry supply chain should build some measured slack into their overall supply chain to become more strategically lean. By doing so, chip players can be on a much better footing to be more agile and sustain and expand their competitive advantage in the long term.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}