Global trade and the new geoeconomic reality

How companies can evolve successfully in a global economy divided by protectionism and security concerns

Introduction: Geopolitical events are changing the global trade environment

Following the fall of the Berlin Wall and the end of the Cold War, the global economy entered a dynamic period of liberalization and trade integration. Conflict between Western democracies and the Soviet Bloc ended, with many former communist nations embracing capitalism. The World Trade Organization was created. Tariffs were lowered and non-tariff barriers were reduced. Globalization advanced rapidly.

In the past few years, however, the environment surrounding global trade has changed abruptly. The COVID-19 pandemic exposed the vulnerabilities created by complex international supply chains. Russia’s invasion of Ukraine in February 2022 has brought war back to center stage. The Israel-Gaza conflict has reignited fears of terrorism and religious conflict. Competition and rivalry between the United States and China have opened up new geoeconomic divides. Companies suddenly find themselves struggling to understand what is unfolding and how they can remain competitive in a very different market.

In this article, we examine how these geopolitical and geoeconomic shifts have changed the dynamics of global trade. We explore how companies can manage their risks effectively and uncover new opportunities in this environment.

The post-war backdrop: Integration

In three decades of globalization after the fall of the Soviet Union, companies penetrated new markets and built global supply chains in the pursuit of economic efficiency. The effort to optimize economic efficiency meant that parts and components crossed many borders before being assembled into final products. This may have resulted in individual economies becoming less distinct, but the diversity of products available to end consumers multiplied.

Following the global financial crisis between 2008 and 2009, trade growth slowed compared to the so-called hyper-globalization era of the years prior to it. Still, companies diversified their exposure across emerging markets in search of new growth opportunities. Later in the decade, however, worsening geopolitical tensions—most notably between the United States and China—began to sow seeds of doubt on the future trajectory of trade. The pandemic, and then the war in Ukraine, added to the pressure, making it urgent for companies to adopt a more strategic and cautious approach to managing global businesses.

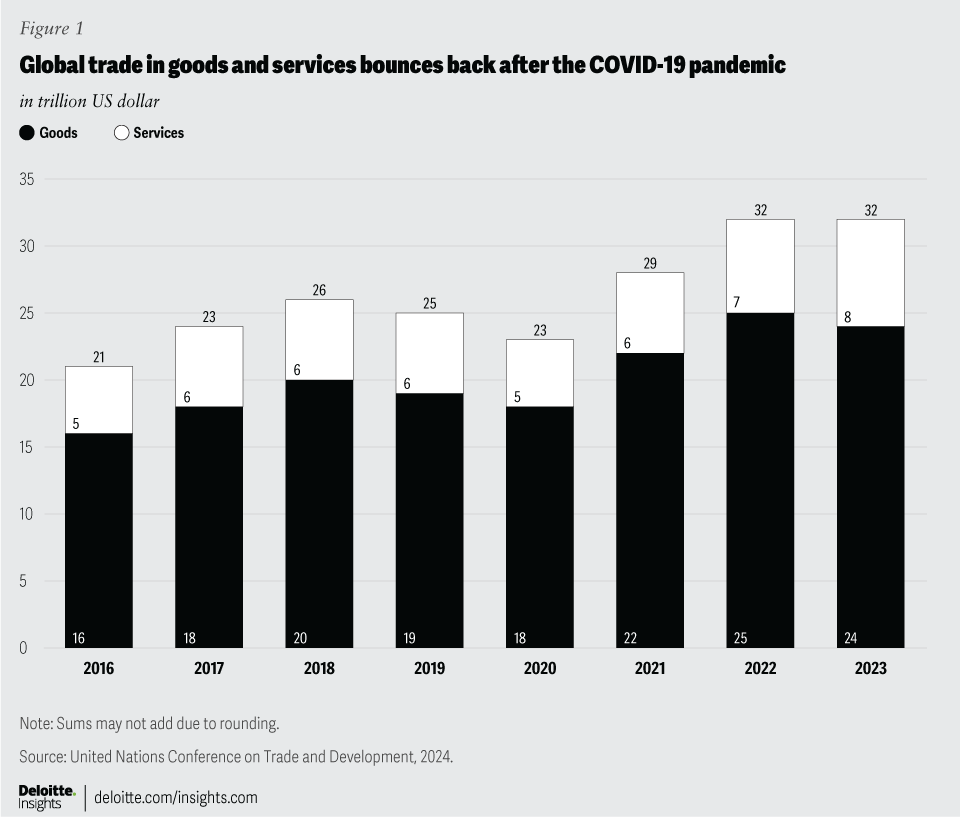

And yet it is wrong to believe that trade has taken a negative turn—at least so far. Global trade in goods and services has proven resilient, recording an all-time high of US$32 trillion in 2022, a remarkable 27% increase compared to 2019.1 Global inward foreign direct investment (FDI) stocks also rose from US$36 trillion in 2019 to a high of US$47 trillion in 2021.2 Trade and FDI did fall slightly in 2023 as inflation moderated and supply and demand stabilized, but they still remain above pre-pandemic levels in both value and volume terms.3

It remains uncertain, however, how these dynamics will affect the volume of global trade in coming years. Conditions supporting trade growth were previously extremely strong; new obstacles to that growth are relatively recent. Moreover, as we discuss this later in this article, further trade restrictions are possible as security and protectionist concerns preoccupy global leaders.

Table of contents

Part I: The new geoeconomic environment, shaped by national security,

technological development, and the green agenda, brings new challenges

The present resilience of global trade and investment is probably a testament to the rapid economic integration that has taken place over the last few decades. But the global economy is undergoing a profound structural change, shaped by increased competition and rivalry between countries. How trade volumes will be affected is uncertain. Three significant dynamics are at play:

- The convergence of national security and economic policy

- The race for technological dominance

- The green agenda

In this section, we explore each of these trends in depth and consider their implications for trade.

1. The convergence of national security and economic policy leads to more complexity

The international security environment has deteriorated significantly in the last few years. Russia’s invasion of Ukraine has cast a dark cloud over European and global security. Military rivalry and economic competition between the United States and China have intensified. These developments have compelled nations worldwide to increase defense spending and look to bolster their military alliances. In Europe, Sweden and Finland have joined the North Atlantic Treaty Organization (NATO). NATO is also in talks to strengthen cooperation with Japan, where the government has announced plans to double its defense spending to 2% of GDP, the target to which NATO countries are committed.4

The nexus of national security, economic development, and trade has been closely studied since the days of the Cold War. In the ensuing three decades of globalization, the level of economic interdependency grew far deeper and more complex. With security concerns now heightened, however, any product embedded with advanced technologies—smartphones equipped with high-end semiconductor chips or industrial machinery used in chip development—is scrutinized to assess its potential defense vulnerabilities. Economic policies are being crafted with a keen eye on security implications, marking a significant shift in policymaking.

The United States has been particularly assertive in aligning its national security interests with economic policies, most notably by utilizing restrictive policy tools. Strict licensing requirements have been imposed on some foreign companies in sectors such as telecommunications and electronics. Export controls have also been placed on the sales of advanced semiconductor equipment to rival countries. These efforts are aimed at preventing transfers of technology that might endanger US security.

The European Union and Japan have developed and are continuing to strengthen economic security strategies that extend from bolstering supply chain resilience to ensuring cybersecurity. These include measures to mitigate risks through rigorous screening of FDI and enhanced export controls, as well as patent classifications to safeguard intellectual property.5 The similarities between the policies of the European Union and Japan suggest close coordination among allies to protect mutual interests.

One of the challenges posed by this new security environment is the uncertainty about precisely what constitutes a national security issue. Determining this remains the discretion of national governments, leaving scope for significant variations in policies and approaches—this also creates complications and risks for trade.

If national governments take different approaches to what is or is not sensitive, a complex array of non-tariff barriers could be woven, reversing the growing openness which characterized the three decades of rapid globalization. The risk overall is that trade policies could become increasingly restrictive.

2. The race for technological dominance leads to more protectionism

Recent advances in emerging technologies, such as artificial intelligence, quantum computing, and biotechnology, are also reshaping the global economic landscape. Their applications in robotics, next-gen telecommunications, and green technologies are already reaping enormous benefits for the economy and society at large.

Today, countries leading in innovative technologies are poised to gain significant economic and geopolitical advantages.

To secure competitiveness in this new environment, governments are formulating new industrial policies that define areas in which to pursue technological leadership. The United States, European Union, and Japan have all identified AI, renewable energy, and semiconductors as priority industries. This strategic alignment is no coincidence as these sectors are positioned at the crossroads of industrial competitiveness and national security.

Accordingly, governments have wasted no time in deploying trillions of dollars to fund private sector activities, including R&D and manufacturing, in the priority sectors. In the United States, US$369 billion has been approved for energy- and climate-related programs under the Inflation Reduction Act,6 and an additional US$52.7 billion for the semiconductor industry under the CHIPS and Science Act.7 Meanwhile, the European Union anticipates mobilizing 43 billion euros through public and private investments under the European Chips Act,8 designed to strengthen the European semiconductor industry.

The renewed focus on industrial policy highlights a strategic shift from the pursuit of economic efficiency and comparative advantage to higher value added and absolute advantage. This state-led approach to industrial development is not without its critics, who view these policies as protectionist, expensive, and counterproductive to the free-market principles that have underpinned economic growth for the last three decades. However, the policies have so far proven to be effective in promoting new investments. A plethora of groundbreaking projects have been announced across developed markets, including the United States, Europe, and Japan.

3. Green agendas lead to new dependencies

Another imperative driving change in global economy is the need to limit the rise in global average temperatures to no more than 1.5 degrees Celsius above pre-industrial levels. Decarbonization and the clean-energy transition have emerged as pivotal factors for countries as they seek to maintain or achieve economic and industrial competitiveness. While fossil fuels continue to account for the majority of energy production today, they are gradually being replaced by renewable sources like solar, wind, and hydrogen, as well as alternative sources like nuclear and geothermal power.

Recent geopolitical events—most notably the war in Ukraine—have raised alarms about energy security and created more urgency for countries to pursue energy independence by adopting renewables.

As the world moves toward a green economy, there has also been a notable upsurge in the demand for minerals that are vital for manufacturing batteries, solar cells, and wind turbines, as well as other advanced technology products. The increase in demand for such raw materials, however, poses a significant challenge, as their supply—including processing capacity—is often concentrated in a handful of countries. This supply bottleneck creates a “green dilemma,” where the push for sustainable technologies inadvertently leads to new dependencies on a few resource-rich countries.

This dynamic is changing the balance of power in global trade and investment, with resource-rich countries increasing their influence. China’s dominance in the production of solar panels and wind turbines is a result not only of strategic policymaking but also its access to critical metals and minerals, such as silicon for solar panels and rare earths for wind turbines.

Indonesia, home to some of the world's largest nickel ore reserves, is attracting significant investment in its downstream industries in a bid to transform the country into a hub for electric vehicle battery production.9

Global trade and investment patterns are shaped by the availability and sourcing of raw materials and flow of finished goods and services. While companies may be able to spread their downstream manufacturing and assembly operations across multiple regions, it is much more difficult to achieve diversification in upstream resource procurement. The reality is that dependence on resources vital for the green economy has implications for the ability of nations to advance technologically and guarantee their national security. This shows the complexity of the interplay between the various forces driving change today in the global economy and in trade.

Part II: Emerging trade corridors, digital transformation, and value-driven growth bring opportunities as well as hurdles

The dynamics described in previous sections on national security, technological development, and the clean-energy transition are beginning to have profound effects on the flow of goods and services across borders. Three significant shifts are emerging that reflect changes in the pattern of global trade.

- The formation of new trade corridors

- The rise and fragmentation of digital trade

- Prevailing asymmetries in the critical minerals trade

In this section, we delve deeper into each of these shifts, which are poised to have important implications for corporate strategy in the coming years.

1. Formation of new trade corridors: More expensive, but more resilient

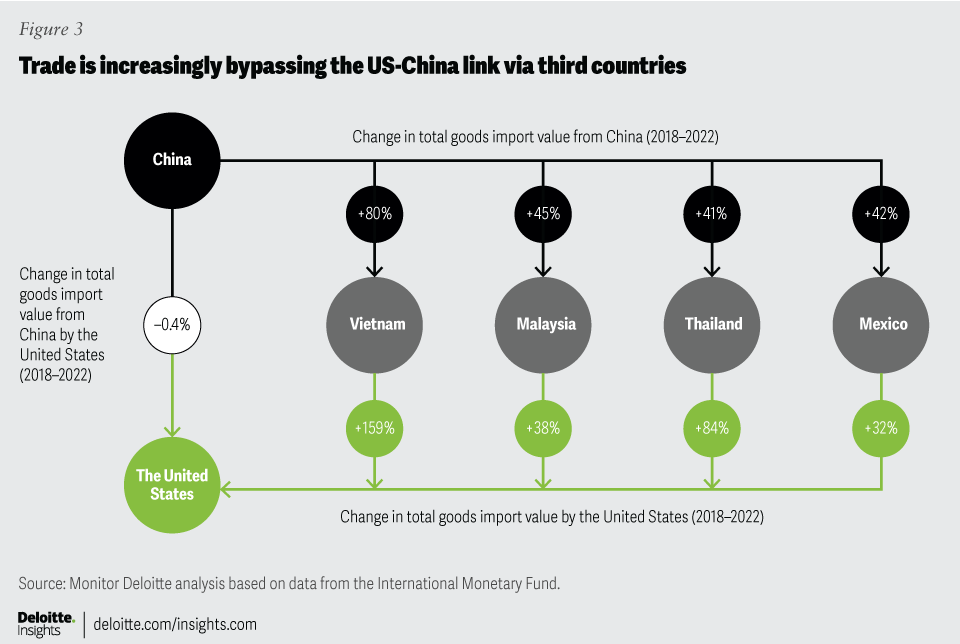

One of the defining characteristics of global trade in recent years has been the development of new trade corridors influenced by geoeconomic competition. A prime example of this is the emergence of what we would describe as “horseshoe-shaped” trade corridors linking China and the United States via other countries. This can be considered as a byproduct of the US-China trade conflict, which has compelled some companies to strengthen their production capacity outside China to be able to serve the US market.

The most striking example of this dynamic has been Vietnam, which borders the manufacturing-rich provinces in China’s south. Between 2018 and 2022, Vietnam’s imports from China increased by 80% while its exports to the United States rose by 159%.10 This is most notably the result of an increase in Vietnam’s imports of intermediate goods from China and its exports of finished goods to the United States. Similar patterns can be seen in other emerging markets with a strong industrial base, including Thailand, Malaysia, and Mexico.

These new trade corridors suggest that more complex supply chains, with goods transiting through more locations before reaching the final consumer, have played a significant role in the recent expansion of global trade.11 While longer and more diverse supply chains may entail higher costs, they also generate more resilience by building in additional capacity and inventory dispersed across multiple locations. Companies anticipate that this will help them overcome the challenges posed by an increasingly uncertain geoeconomic environment.

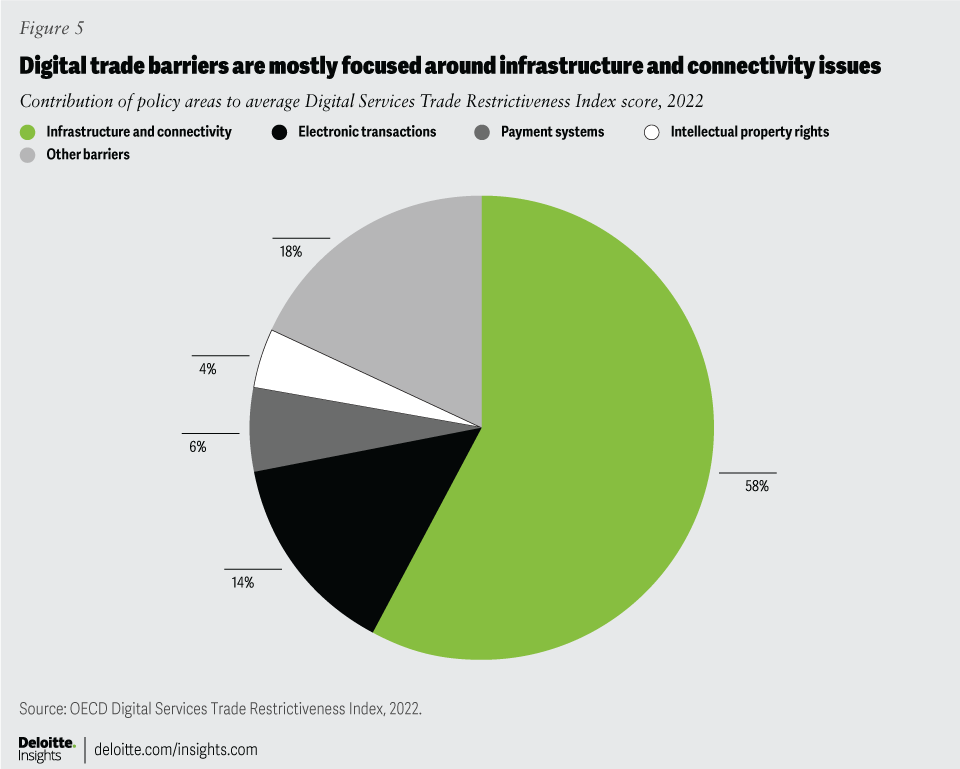

2. Digital trade: Rising, but also fragmenting

The rise of digital trade is another phenomenon that has emerged from the global race to secure competitiveness in new technologies. The most salient example of this trend is the boost in digitally deliverable services, whose share of services exports exceeded 60% for the first time between 2020 and 2021.12 This growth has been propelled in no small part by investments in emerging technologies such as AI or the metaverse, leading to the innovation of groundbreaking services for consumers and businesses.

Growth has also been strong in digitally enabled purchases of goods, or e-commerce. In China alone, cross-border e-commerce rose by 95% between 2018 and 2022,13 substantially more than the 37% increase in all goods traded by China over the same period.14 This expansion can be taken as the result not only of the rise in consumer demand but also of digital transformation in the supply chain. In other words, digital solutions, like data-driven inventory optimization or AI-powered automation, are generating productivity gains that further accelerate the expansion of trade.

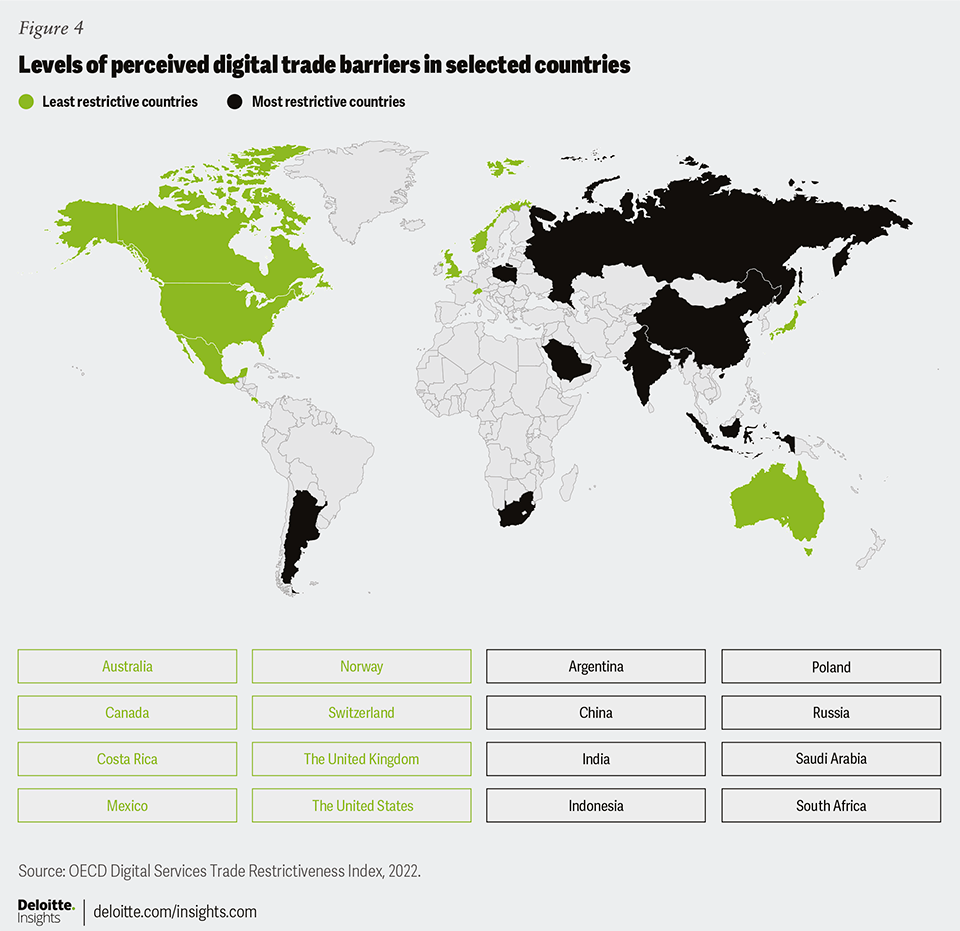

Meanwhile, the fact that the digital trade environment is already showing some signs of fragmentation should not be overlooked. As data becomes increasingly tied to economic growth and national security, countries are both competing and collaborating to develop digital standards, data governance models, and cybersecurity protocols that serve their interests.

The global demand for digital trade is unlikely to dissipate, but new “digital borders” shaped by geopolitical and security concerns may become increasingly significant in the future.

3. Critical minerals trade: Asymmetries prevail, but alliances can help

The third dynamic in global trade patterns is the growth in prominence of the critical minerals trade. Between the last quarter of 2019 and the second quarter of 2023, critical minerals exports rose by 46%—significantly higher than the rise of 20% for world trade in all products.

Notably, growth was higher for semi-processed (49%) and processed (43%) than for raw (32%) critical minerals, which could be pointing to the strength in demand for materials used in products at the center of technological competition and the green transition, such as batteries for electric vehicles.15

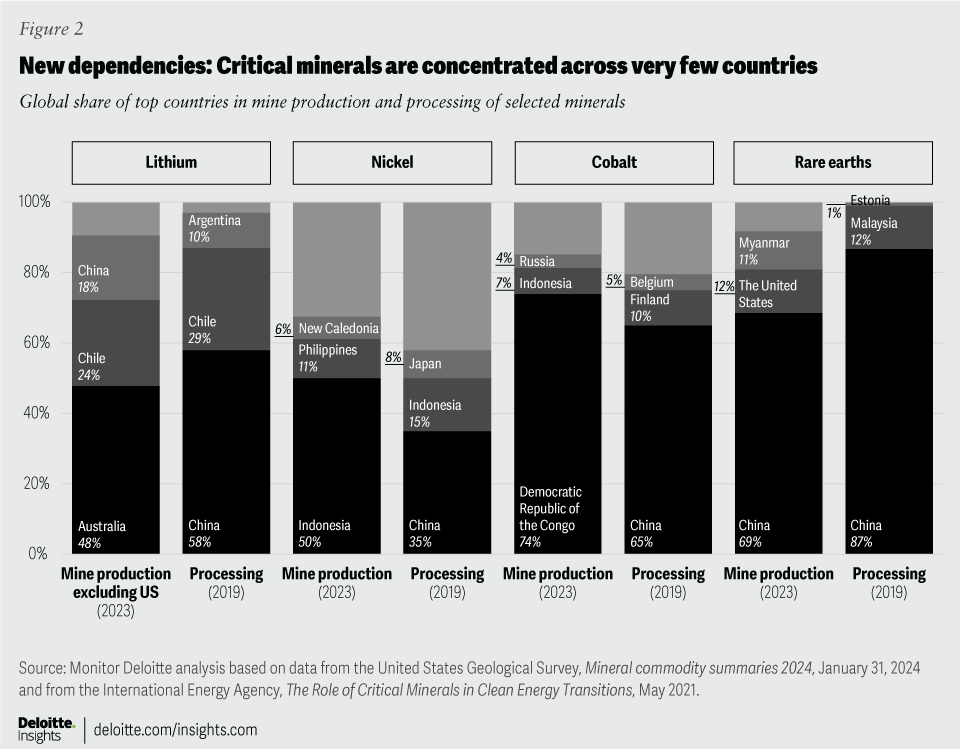

An important distinction in the critical minerals trade is the asymmetry owing to the geographic concentration of raw material ores and processing capacities. For instance, Australia and Chile together account for 79% of all lithium ore and brine exports, while China accounts for 73% of global lithium imports. Likewise, the Democratic Republic of Congo accounts for 64% of global cobalt hydroxide exports, of which 96% is imported by China.16 Lithium and cobalt both play an important role in the clean energy supply chain, and their demand is likely to increase in the long run. Nonetheless, the market concentrations of these critical minerals leave them vulnerable to disruptions such as price volatility and supply and demand shocks.

Countries have stepped up efforts to cooperate in diversifying supply chains to reduce short-term risk exposure and establish long-term resiliency. The Mineral Security Partnership, a collaboration between 14 countries and the European Union to promote investment in critical minerals supply chains, is one such example.17 Meanwhile, resource-rich countries, such as China and Indonesia, are increasingly restricting exports of some critical mineral products or mandating processing in domestic facilities. These dynamics in the market mean that that the global trade in critical minerals is likely to grow but remain volatile, influenced not only by market forces but also by geopolitical factors.

Part III: Corporate strategies to navigate the new geoeconomic environment

It is apparent that the global market environment is undergoing a structural transformation. Thriving in this new environment requires not only a robust growth strategy to maintain a competitive edge but also a strategic approach to risk management. This involves being proactive rather than reactive, ensuring a company can withstand and adapt to geopolitical shifts and the uncertainties they bring.

To tackle these challenges, companies should take three key measures relating to their supply chain, digital, and business strategies:

- Take the long view on geopolitical risks

- Prepare for increased regulatory pressures

- Make product-level decisions

In this section, we explore the ways in which organizations can incorporate geopolitical perspectives into both their strategy and risk management, thereby building resiliency and flexibility.

1. Take the long view on geopolitical risks: Geographic diversity is not enough

The first measure that companies should take is to manage their supply chain–diversification and market-expansion efforts wisely by taking a long view on the likely role to be played by geopolitics. In the previous section, we noted how new “horseshoe-shaped” trade corridors are emerging as companies establish production or logistics operations in new locations. Such geographic diversification helps to reduce a company's dependence on specific countries and ensures business resilience in the face of potential military conflicts or trade wars. Those efforts, however, are themselves liable to be undermined if the political risks in the countries to which companies diversify are not also given due consideration.

For companies with a global footprint, it will come as no surprise that emerging markets often have heightened domestic political risks which can upend business strategies. For example, while many emerging countries benefiting from the recent rise in foreign investment are electoral democracies, some of their leaders have been criticized for undermining democratic institutions and dampening the appetite for more investment. There is also no shortage of examples in recent memory in which investment euphoria has been followed by political upheaval—for example, in Myanmar. A business strategy that depends heavily on tax incentives or government subsidies could backfire in case there is a sudden about-face in policy direction introduced without due regard for proper legislative processes.

Business leaders also need to be aware of the implications of evolving relationships between various countries and international organizations. In recent years, for example, China's relationships with many countries in Asia, Africa, and Latin America have intensified, thanks to loans and investments included in the Belt and Road Initiative. Some of the same countries have also been heavily dependent for years on other powers—such as the United States or Russia—to provide military equipment.

These overlapping and potentially conflicting relationships add to the challenge of developing supply chains in “like-minded countries,” an idea that has gained traction in some decision-making circles in recent years. Geographical diversification does not necessarily equal geopolitical diversification. The same developments may apply at the same time in different geographies.

Given these complexities, it is important for companies to formulate a well-informed and regularly updated long view of the prospects for its global supply chains and target markets.

2. Prepare for more regulatory pressures: Pay close attention to the digital sphere

The second measure companies should take is to prepare for stricter regulations governing global trade, especially in the digital realm. We have already seen how digital trade is evolving rapidly but starting to show signs of fragmentation as countries seek to protect their economic and security interests.

With the emergence of new technologies like AI, the focus of digital trade governance is expanding from data to algorithms, suggesting rising regulatory pressures in coming years.

Corporations have grappled with the challenge of complying with restrictions on data processing, in particular storage and transfers for many years already, but the recent growth of digital trade has made the efforts required far more sophisticated. As companies have increased their exposure to digital consumers in more markets, the back-end architecture supporting digital services has been optimized by leveraging cloud-based services. This means that the decision on the location and management of data centers is often reduced to the selection of cloud services providers and regions or zones. To comply with a multitude of data localization requirements, companies may be forced to utilize unique data centers or regional cloud solutions in each market or forgo operations altogether, undermining the scalability, reliability, and efficiency that cloud service providers can offer.

In coming years, companies will likely face new rules and regulations governing emerging technologies like AI. Given the difficulties involved in ensuring the accuracy or transparency of algorithms used in such technologies, specific services or companies with national security concerns may be at risk of being banned altogether in the near term, as already visible in some markets like the United States. It will become increasingly important, therefore, for the chief information officer in consultation with the chief strategy officer in any company to make IT strategy decisions based on a common understanding of geoeconomic trends likely to impact their future ability to offer digital services across borders.

3. Make product-level decisions: Thinking small will help manage the bigger geopolitical picture

The third measure companies should take is to make product-level business decisions. As we have discussed, the degree to which businesses are impacted by geoeconomic competition differs at the product level, with those involving technologies essential for both national security and economic growth being subject to the largest impact. Such high-value-added products have an outsize influence on global trade.

As companies expand their global reach, their product portfolio is likely to become more diverse to address the needs of customers in each market. This suggests that even products in the same business segment may face different levels of geoeconomic impact based on their technological sophistication. In the semiconductor sector, for instance, the smallest chips with possible defense vulnerabilities are already subject to strict trade restrictions, whereas larger chips used in consumer electronics face fewer obstacles.

Meanwhile, the uncertainties surrounding what constitutes a national security risk will continue to complicate decision-making for companies. For instance, a widely traded product that does not involve any high-end technologies may suddenly be put under the national security microscope based on other, more sophisticated, products offered by the same company. Having a product-level decision-making mechanism will help companies to adapt with agility in such cases, minimizing the impact on other areas of their business.

Conclusion: The new economic and trade environment is not about taking sides but anticipating risks and diversifying

A new geoeconomic order is taking shape, replacing the environment that had evolved during three decades of rapid globalization. National security, technological development, and the green transition agendas are now becoming intertwined. Governments around the world are turning to industrial policies with a protectionist flavor to both safeguard national security and to protect competitive advantages. Global trade continues to grow, but its composition and orientation are changing.

The Cold War era was about choosing sides—The Western Bloc and Eastern Bloc had two different economic systems and trade between the two was limited. Globalization has changed this equation, however. Today, the United States and China are part of one global economy. Rivalry and competition between them and among other countries are intensifying. More and more countries will decide to remain “strategically neutral” as they seek to retain bargaining power. In such an environment, companies will no longer have the luxury of choosing sides. Instead, they will need to build resiliency and prepare for contingencies. This should involve diversifying markets and supply chains, anticipating regulatory changes by taking a long view of trends and risks and building an agile decision-making structure.

Navigating this new environment will no doubt be challenging. Geopolitical forces will continue to create obstacles in the market economy that entail higher costs and barriers to trade. Companies should bear in mind, however, that such market inefficiencies also generate new value-creation opportunities. Engineering a successful business strategy in the new geoeconomic reality should not only be about managing risks but also about capitalizing on opportunities.

You can also find this article in Japanese here.

If you would like to find out more about our views on geoeconomic resilience, please visit our pages on Deloitte.com (in German only).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}