AVOD’s resurgence is healthy for the wider television industry. For SVOD providers, it unlocks an additional revenue stream and could reduce churn; for broadcasters, it raises the profile of a service they’ve been offering for years; for consumers, it enables continued, lower-cost access to their favorite content, albeit with the (minor) wrinkle of having to watch ads. While AVOD is not for every viewer, it’s likely to appeal to the majority, even in the wealthiest of markets.

The transition to AVOD won’t however be a walk in the park. Consumers should be migrated gracefully. SVOD providers may need to restructure, add sales capabilities, reformat existing content, commission differently, measure ad impact, and change culture.

One of the biggest challenges will to be make ad breaks as enjoyable as possible. This isn’t just about a low volume of ads per hour; variety is critical. Repetitious ads, even in small quantities, are tedious. The range of commercials shown should be similar or superior to that for traditional television. For this to happen, content providers should replicate the ad sales organization and culture that traditional broadcasters have had for decades. For some SVOD players with a traditional broadcaster heritage, this should be easier; for streamers that have never sold advertising, the learning curve will likely be steeper.

Content that was commissioned for an ad-free service may require reediting to identify natural breaks to show ads. By contrast, library content that was originally edited to include ad breaks at regular intervals may not require any changes. Some licensed content may not permit the insertion of ads, so agreements may need to be revised. Content providers may also need to replicate the episodic release of content that broadcasters have perfected over the decades such that their tentpole releases are popular enough to drive the national conversation. For this to happen, new content should be teased and released at regular intervals, rather than a season at a time.

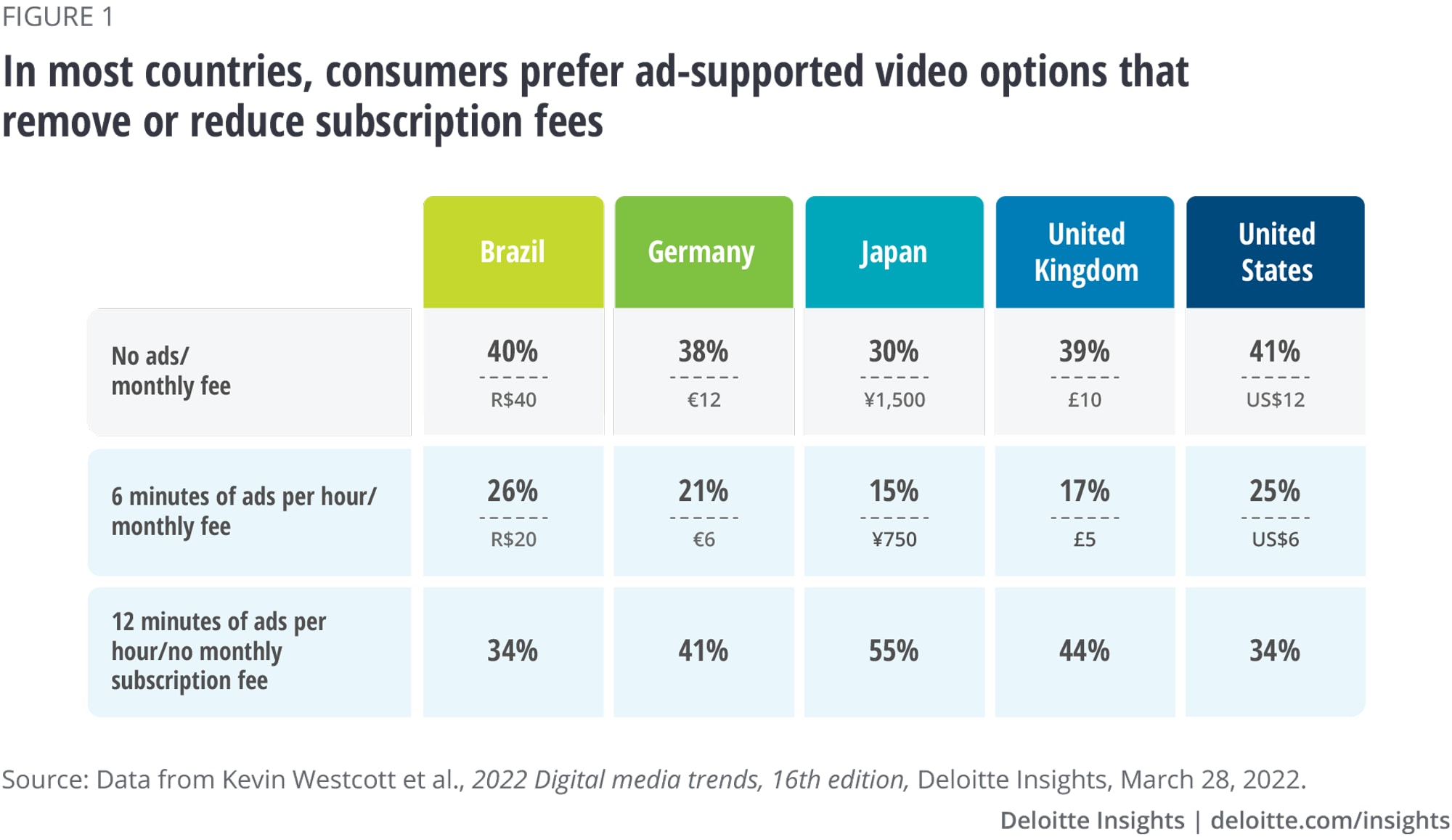

New arrivals to the AVOD market should note that its size will vary by market, with the United States leading in the long run, as it’s the largest TV ad market globally. The US TV ad market, at a forecast US$70 billion in 2022, is 10 times bigger than the United Kingdom’s.7 Furthermore, in markets such as the United Kingdom, SVOD-to-AVOD converts will compete with existing ad-funded services from national broadcasters whose outputs have for many years driven the national conversation.

The introduction of ads into services that previously lacked them should be considered a progression, not a step backward. In the long term, funding the content that consumers want to see requires a blend of subscription and advertising revenues. This has long been the norm—not the exception—for almost all media. The virtue of the AVOD model is that it is inclusive of everyone, regardless of income. People may well love an ad-free experience, but not if it makes content unaffordable.

{kind=link}

{kind=link}

{kind=link}