Brazil economic outlook, July 2023

Though benefits of a strong agriculture sector might be wearing off, a dovish central bank and slow recession might give citizens and government some respite.

Brazil’s economy continues to be resilient in the face of headwinds. Real GDP growth was exceptionally strong in Q1, thanks to strong crop yields. But though the effects of the agricultural sector’s outperformance have spilled over to other parts of the economy, the benefits are beginning to slow down. Domestic demand remains relatively weak, and parts of the economy, such as manufacturing, are contracting already. Fortunately, inflation is coming down relatively quick, which should likely elicit rate cuts from the Banco Centrale do Brasil (BCB), the nation’s central bank. Easing financial conditions are expected to eventually support consumer spending, which has been constrained by expensive debt service. Governments and businesses may also benefit from the drop in rates.

Underlying weakness

Real GDP grew 8% on an annualized basis in Q1.1 This impressive growth rate was a result of strong agricultural output, most notably a record soybean harvest. That strength has been carried over into Q2, with agricultural real value adding up 22.9% year over year in April.2 The rest of the economy, however, remains considerably weaker. For example, real domestic demand fell by an annualized 1.9% in Q1.3 Despite strength in the farming sector, real exports declined modestly over the same period, highlighting the weakness in demand from the rest of the world.

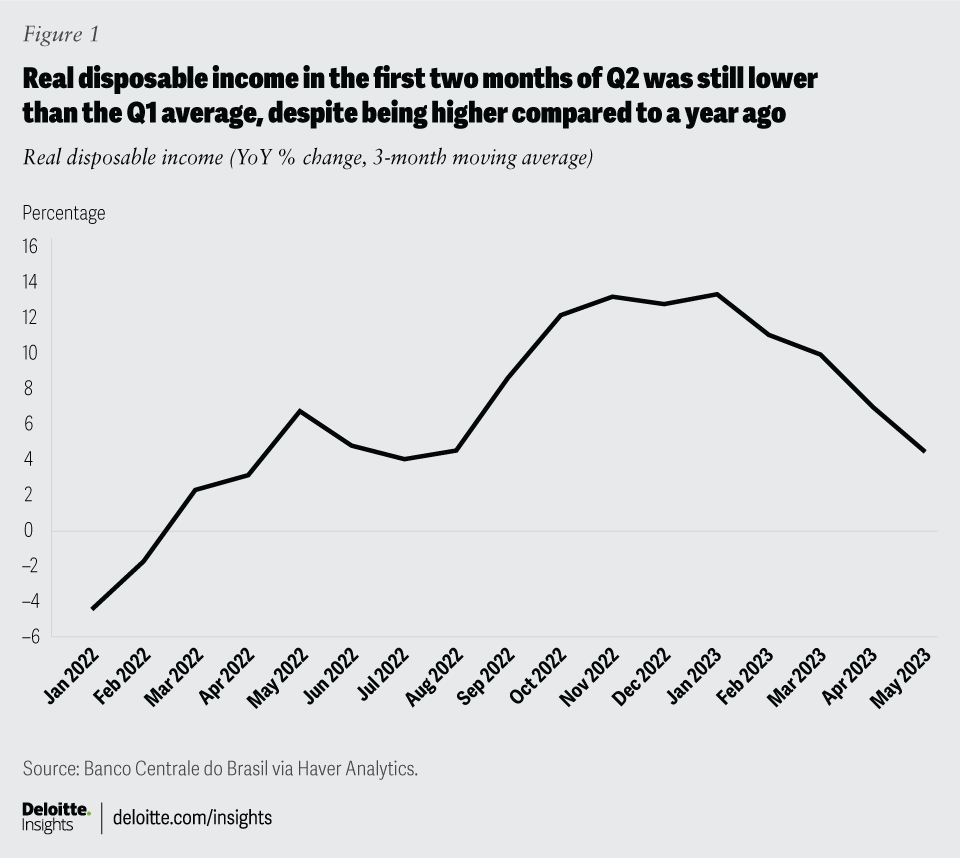

The benefits from the agricultural sector are beginning to slow down. Although real disposable income in May was still up 4.5% from a year earlier (figure 1), the data shows that it was lower in the first two months of Q2 relative to the Q1 average.4 Similarly, real wages fell in April and May, and employment growth has slowed dramatically since the start of the year.5 The volume of retail sales also fell in April and May, exhibiting a similar pattern to disposable income and wages.6 This mimics the monthly GDP data, which also shows a decline in activity for April. All of this points to a more constrained consumer, which helps with inflation but likely raises the risk of recession.

The manufacturing sector has been struggling since the end of 2022, with the purchasing managers’ index clearly pointing to contraction.7 Manufacturing production was just 0.3% higher than a year ago in May.8 Even this number likely overstates the sector’s growth, due to expected tax breaks for the auto sector. Motor-vehicle production spiked by 7.4% in May alone,9 as automakers prepared for a rise in auto sales when tax breaks took effect in June. Auto sales have otherwise been weak amid high interest rates. This suggests that the jump in manufacturing production is unlikely to be repeated in subsequent months.

The manufacturing sector is also struggling amid weak foreign demand. Goods exports were down 8.5% in June from a year earlier, though they fell a more modest 1.7% for Q2 as a whole.10 Agriculture and mining are pulling export data in different directions. Agricultural product exports were up 9.2% year over year in Q2, thanks to strong soybean yields. However, mining exports were down 8.5% over the same period as lower prices for commodities, such as crude oil, pushed growth further down. After removing these forces from the data, manufacturing exports alone were down 5.0% year over year in Q2.11 Although the value of exports remains relatively strong by historical standards, weaker foreign demand is clearly weighing on growth for Brazil-made goods.

Disinflationary tailwinds

Fortunately, tailwinds are now materializing for the economy. Spillover effects of the boom in agricultural output likely prevented a contraction in Q2, while strong crop yields and lower energy prices have put a lid on food inflation. Lower food and energy inflation is expected to give consumers some extra spending power for discretionary items. In addition, disinflation has been faster than expected, which could allow the central bank to cut rates this year, providing much-needed support to the economy.

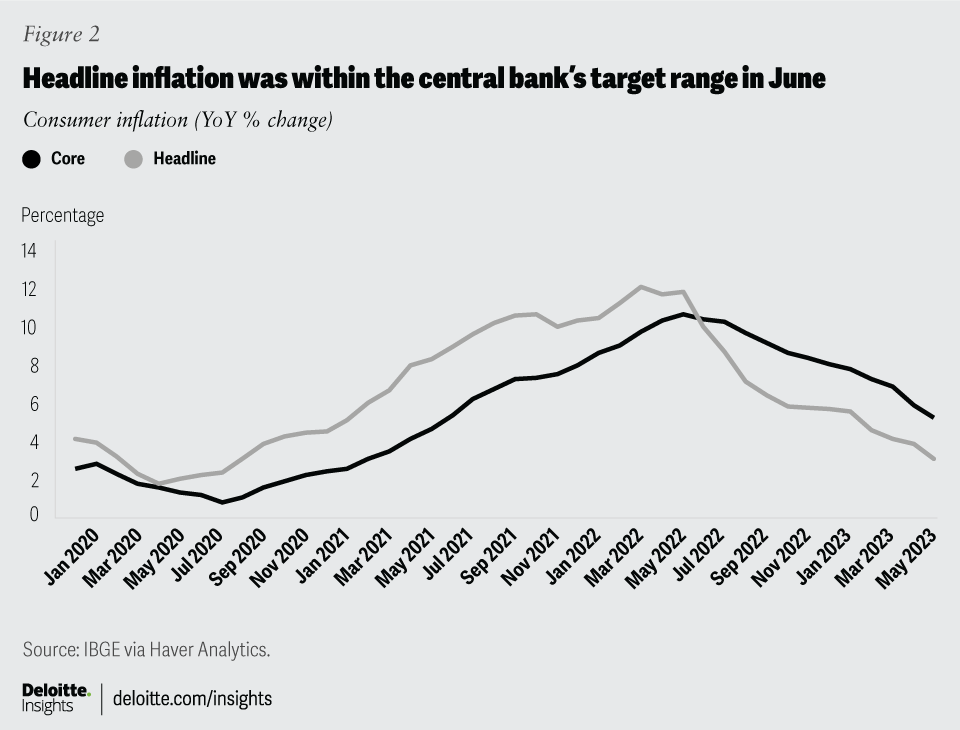

In June, headline inflation fell slightly, contracting -0.1% over the month.12 This brought the year-ago rate down to 3.2%—right in line with the central bank’s target for the year (figure 2). Inflation drivers have clearly eased. Producer prices have been falling since July 2022 and were -9.2% lower in May compared with a year earlier.13 Commodity prices have fallen, with the composite commodity price index standing 19.9% lower in June year over year.14 In addition, June inflation expectations were the lowest they have been since August 2021.

Improvement in the inflation picture is expected to allow the central bank to cut rates before the end of the year. The August meeting now seems likely for the first rate cut. In the statement from its most recent policy meeting, the BCB removed any mention of the possibility of further rate hikes. In addition, the minutes of the meeting revealed that policymakers were eyeing the August meeting for a rate cut.16 Those central bank communications occurred before the June inflation data was available. Given the strong disinflationary bent to that data, central bankers will likely feel emboldened to cut rates at the next meeting.

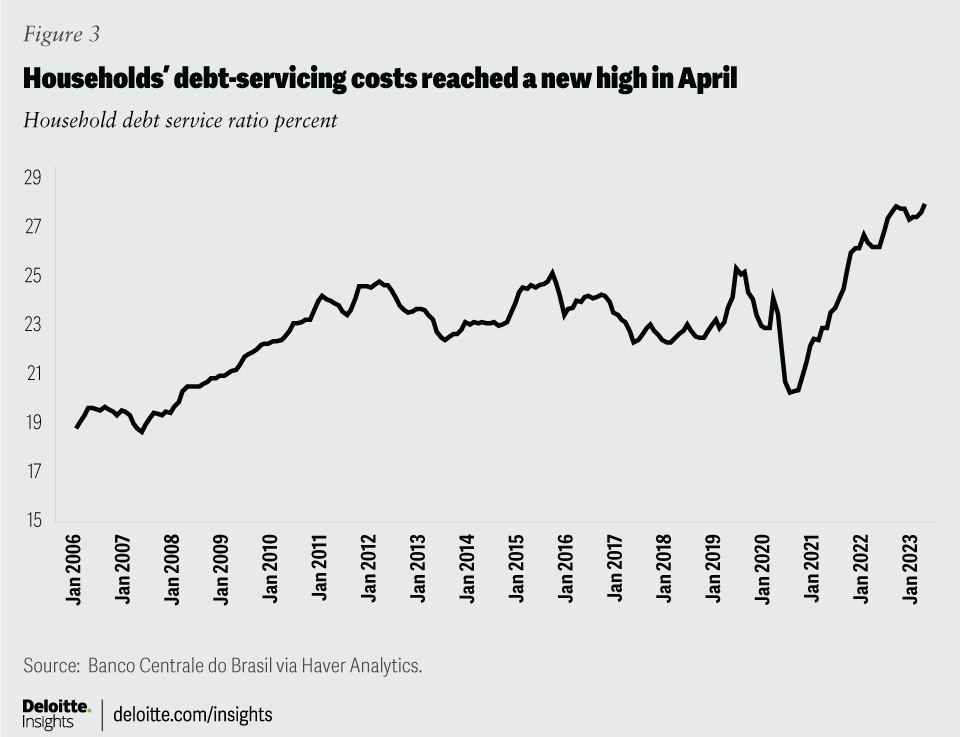

The expected fall in rates could not come at a better time. As the benefits from strong agricultural output fade, the underlying weaknesses in the economy are becoming more apparent. For example, consumers are struggling with elevated debt burdens. Households spent 27.9% of their disposable income on debt service in April, the highest reading since data began in 2005 (figure 3).17 Interest expense alone took up nearly 10% of disposable income.18 A respite from high interest expenses will potentially provide some much needed support to households.

Government finances have also been constrained, partly due to high interest expense. As a result, the government came up with a fiscal framework to bring calm to financial markets and prevent its borrowing costs from rising further.18 Policymakers are also working on tax reform. With the fiscal framework in place and the central bank headed for rate cuts, the 10-year government bond yield has fallen substantially to 10.8% in June from 12.9% in February.19 Faster rate declines will give the government more room to implement spending efforts promised on the campaign trail.

However, the central bank is not entirely out of the woods just yet. Core inflation has come down markedly but is running at a 5.3% year-ago rate, which is well above the central bank’s target. Services inflation continues to run hot.20 Prices of services related to health, recreation, education, and personal care were each up at least 7.0% from a year earlier in June.21 Getting services inflation under better control may require weaker economic activity or recession.

Brazil’s economy is at an inflection point. Real growth is slowing after the benefits from the agricultural sector fade. Fortunately, slower inflation is restoring consumer purchasing power. Plus, a more dovish central bank is expected to provide much-needed stimulus in Q3. Lower rates will take pressure off of households and government, both of which have excessive debt burdens. However, the challenge for the central bank will be to provide enough stimulus to prevent a recession without reinvigorating inflationary pressures.

{kind=link}

{kind=link}

{kind=link}