Mexico economic outlook, 2023

The Mexican economy is firing on—thanks to nearshoring, public investment, and private consumption—but productivity and public policies need to catch up.

Mexico is on a stronger foot

Trailing only India, China, Indonesia, and Turkey among the G20, Mexico’s GDP grew 3.7% year over year in the first half of 2023 (figure 1). This expansion can be attributed to: first, the United States, which shared a good first half (2.2% YoY) with Mexico, is helping the nation through trade and remittances; second, a boom in private consumption, thanks to increases in real wages and a strong labor market; third, gains due to nearshoring, observable through the recovery of business confidence and private investment; and, fourth, big infrastructure projects (new refineries, train, and other such projects), now clearly seen in government expenditure and construction.

A key factor driving Mexico’s growth is private consumption, which has remained resilient even during a period of high inflation. What’s behind this unexpected performance? First, employment is growing at a fast pace. Last June, unemployment rate reached 2.7%, the lowest level since records started in 2005 (although 55.5% of the economically active population works in informal sectors). Second, the Mexican wage policy is also encouraging consumption. Since taking office in 2018, the current administration has been significantly increasing the minimum wage.1 Real wage income has grown significantly over the past several years2 (21% from the end of 2018 to July 2023). This has effected a gradual reversal of a decades-long economic trend—of labor’s share in the national income declining steeply (0.6% from 2004 to 2017) (figure 2).

Later in this article, we will also delve into how nearshoring and public investment are causing economic data to continue exceeding expectations. Given all these factors, Deloitte’s growth forecast for Mexico increased to 3.5% for 2023 (2.8% before), and to 2.5% for 2024 (2.4% earlier). Also, we expect that some of these factors will not be around by the time we enter 2025, and as a result, we have revised our forecast for 2025 to 1.3%, from 1.8% previously.

Unfortunately, inflationary pressure will continue, making it hard to reach the central bank’s goal of 3% in the near term (we expect headline inflation to be at 4.7% by year-end 2023 and at 4% by year-end 2024). These factors and their impact on each other will affect the path of monetary policy.

During its August meeting, the Mexican Central Bank (also known as Banxico) kept interest rates unchanged for the sixth consecutive month.3 While policymakers acknowledged that the disinflation process is underway, they downplayed the space for policy rate cuts in the short term. Also, as developed markets continue to restrict their monetary policies, especially the Federal Reserve, the case for easing policy in Mexico in the fourth quarter of 2023 is losing shine. Therefore, we have decided to delay the start of the normalization cycle to February 2024, from November 2023, followed by intermittent actions over the next year (–225 basis points), with the rate standing at 9% by year-end 2024 from the 8.5% we had previously anticipated.

Fiscal policy in a presidential election year

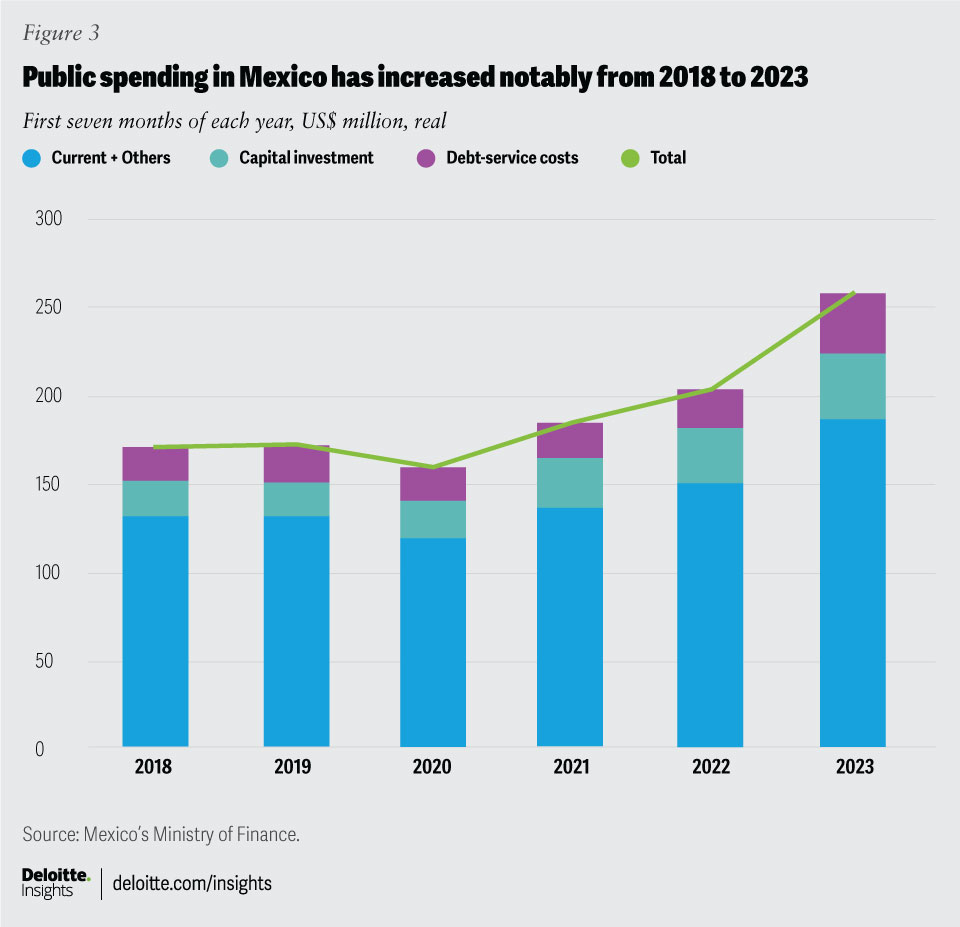

Another source of growth in the first half of the year has been government expenditure, particularly on capital goods (figure 3). Total real government expenditure grew 4.9% YoY in real terms over the first seven months of the year,4 a much higher rate than the 1.3% average rate of the first four years of the present administration. Government transfers through elderly pensions (6.2% YoY), students’ scholarships (10.7% YoY), and other social programs (6.3% YoY), as well as capital investments (11.7% YoY) in big infrastructure projects, are stimulating Mexico’s growth.

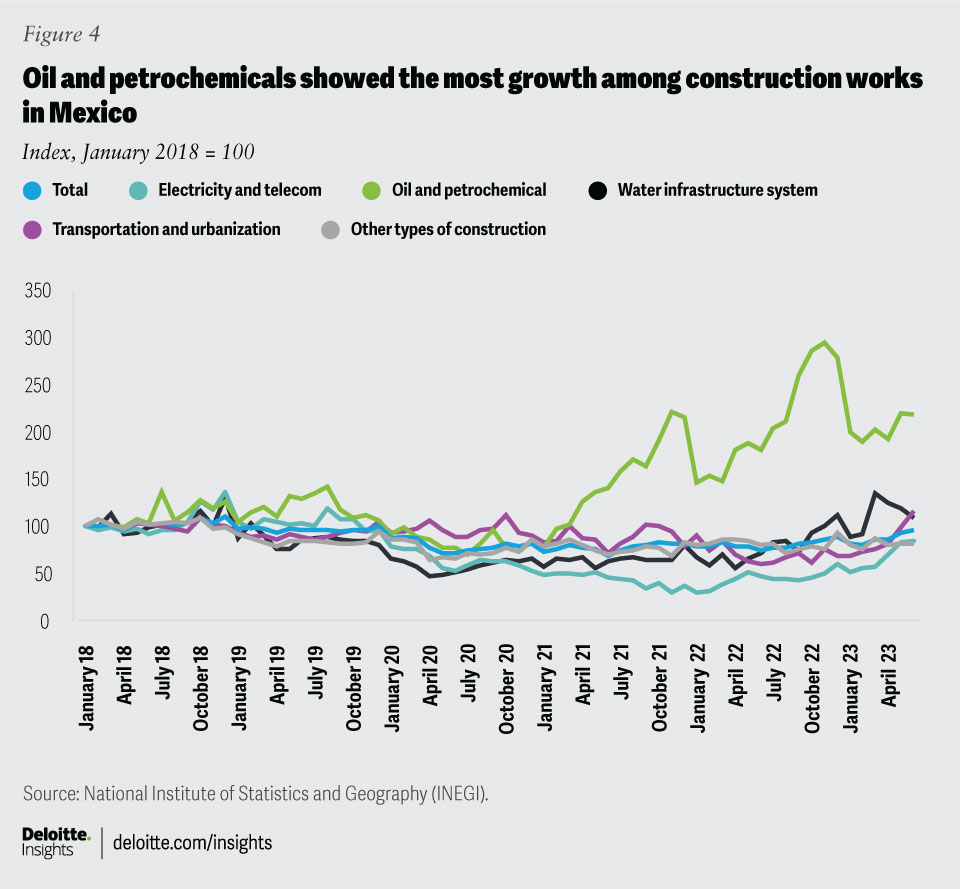

Here’s an illustration of how much public investment is growing: The value of building construction projects in Mexico grew 6.7% in June 2023 compared to May 2023 and 27.8% compared to June last year.5 Leading this growth was civil engineering works—growing 55% annually—reflecting the current administration’s push to complete its big infrastructure projects. Within this subsector, transportation and urbanization works grew 92% YoY. The Mayan Trains6(railway line that surrounds the Yucatán Peninsula and connects five states in the Mexican southeast) and the Isthmus Train7 (runs from the Pacific Ocean to the Gulf of Mexico) are examples showing commendable growth. Oil and petrochemical works grew 20% YoY, including the construction of the Dos Bocas refinery (figure 4).

Debt-service costs have also triggered public-spending increases (figure 3), going from 11% in 2022 as a share of total expenditures to 14% in the first half of 2023, reflecting a sharp rise in domestic and global interest rates over past years. Short- and long-term interest rates have been increasing since 2021 (in Mexico, the interest rate went from 4% in 2021 to 11.25% currently), but the impact has taken time to show up in the financial costs, given the maturity structure of the federal government and the composition of its debt portfolio among short-, medium-, and long-term instruments. Hence, interest-rate growth materializes through higher financial costs as government bonds mature.

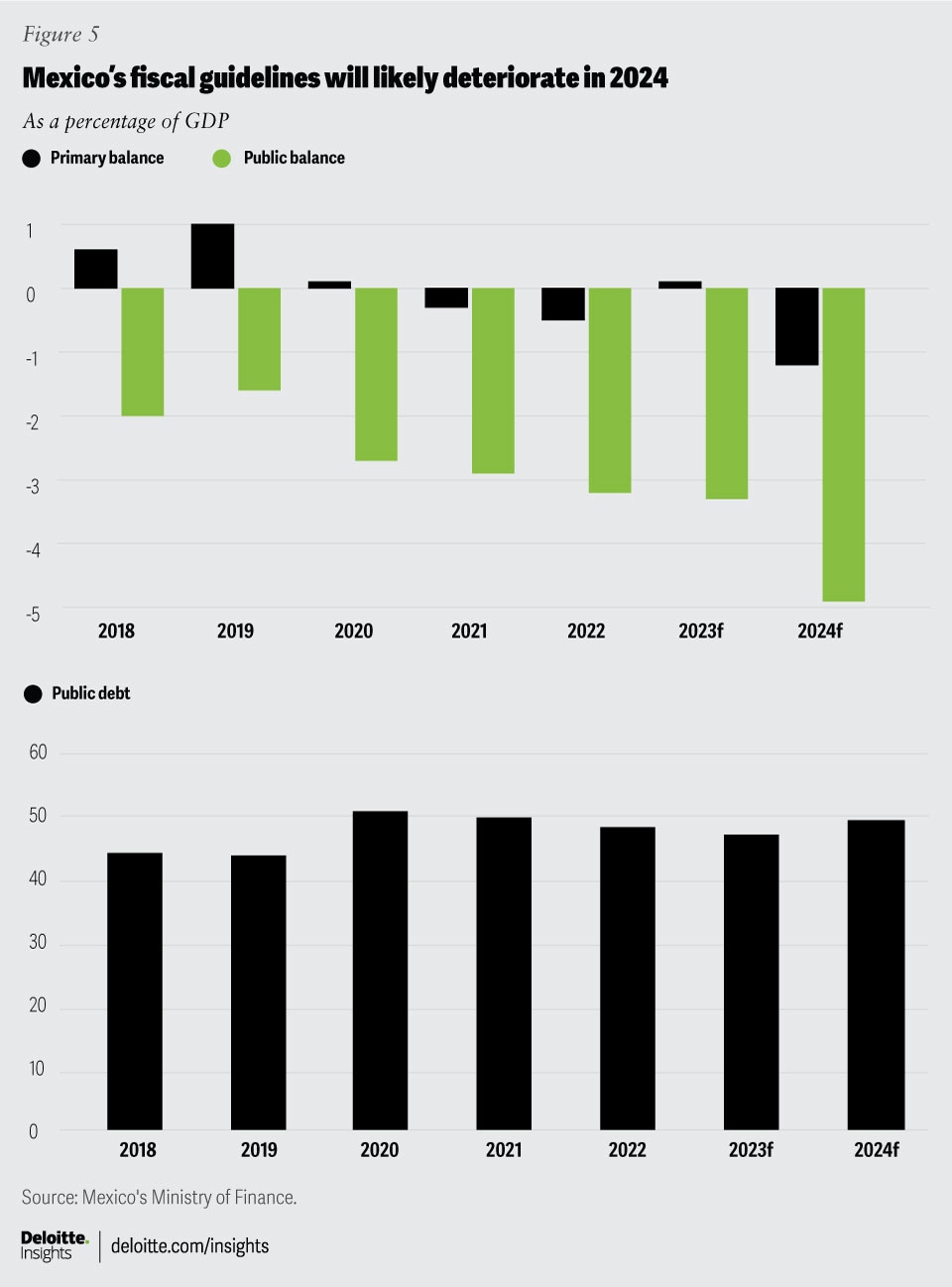

Despite these higher expenses, income tax collection has increased in line with better performance of the economy, and thus, the government plans to achieve a primary surplus equivalent to 0.1% of GDP this year, and the public debt/GDP ratio8 will fall to 46.5% from 47.7% in 2022 (figure 5). The strong peso has been particularly helpful in this regard, as it has reduced the local currency value of external debt (30% of total debt is external).

For 2024, the government plans to loosen its purse strings as it ramps up spending ahead of next year’s presidential elections. It projects a real growth of 7.8% in public spending compared to 2023, while public revenues will only rise 0.8% YoY. This largely reflects the increase in social and financial spending, as well as in construction to complete their priority projects. So now the government expects a primary deficit equivalent to 1.2% of GDP—the largest since 1990—and a fiscal deficit equivalent to 4.9% of GDP—also the largest in 33 years. For its part, public debt as a percentage of GDP will rise 230 basis points from 46.5% in 2023 to 48.8% in 2024—the highest jump in the last eight years—only after the shock in 2020 due to the pandemic (although it remains much lower than the Latin American average of 68% in 2022). On the positive side, since spending on pensions and subsidies will increase significantly (7.3% and 12.2% YoY in real terms, respectively), we expect this to have a positive effect on private consumption.

The nearshoring phenomenon

As we mentioned in our July report on nearshoring, the relocation of manufacturing plants to Mexico could reconfigure the Mexican economy through the arrival of foreign investment, new and specialized jobs, expansion of manufacturing activities, and a boost in productivity and R&D, among other things. This phenomenon, while still in its nascent stages in Mexico, is emerging rapidly.

Although manufacturing activity has decelerated lately, it remains well above prepandemic levels (6% above 2019 levels). Apart from this, private investment is also recovering fast (18% YoY in the first half of 2023) after a long period of weakness.

The construction of industrial facilities in the country has grown 19% in the first six months of 2023, compared to the same period last year, and has finally exceeded the highest level, which was reached in 2017. However, when observing the volume of foreign direct investment in the first half of 2023, we find that, out of the total of US$29,041 million registered, only 7%—just over US$2 billion—corresponds to new investments while almost 80% relates to reinvestments. Although these numbers cast doubt on whether new companies are moving to Mexico or not, we think this is happening because several of these nearshoring announcements are in their initial phase, and that the largest investment disbursements will occur in the following years.

In addition to the nearshoring story, the US-Mexico-Canada Trade Agreement (USMCA) has increased regional value-content requirements for products commercialized in the region,9 which has served as another incentive to relocate to Mexico. For example, in the automotive industry, 75% of auto products should be made in North America, compared to 62.5% under the North American Free Trade Agreement.10 By setting up factories within Mexican borders, manufacturers are able to affix the coveted “Made in Mexico” label on their goods and pay zero duty on a large number of products. These two events could serve as a path to greater US-MX integration. In fact, since March 2022, Mexico has become the largest commercial partner of the United States, exceeding China for the first time in 20 years (figure 6).

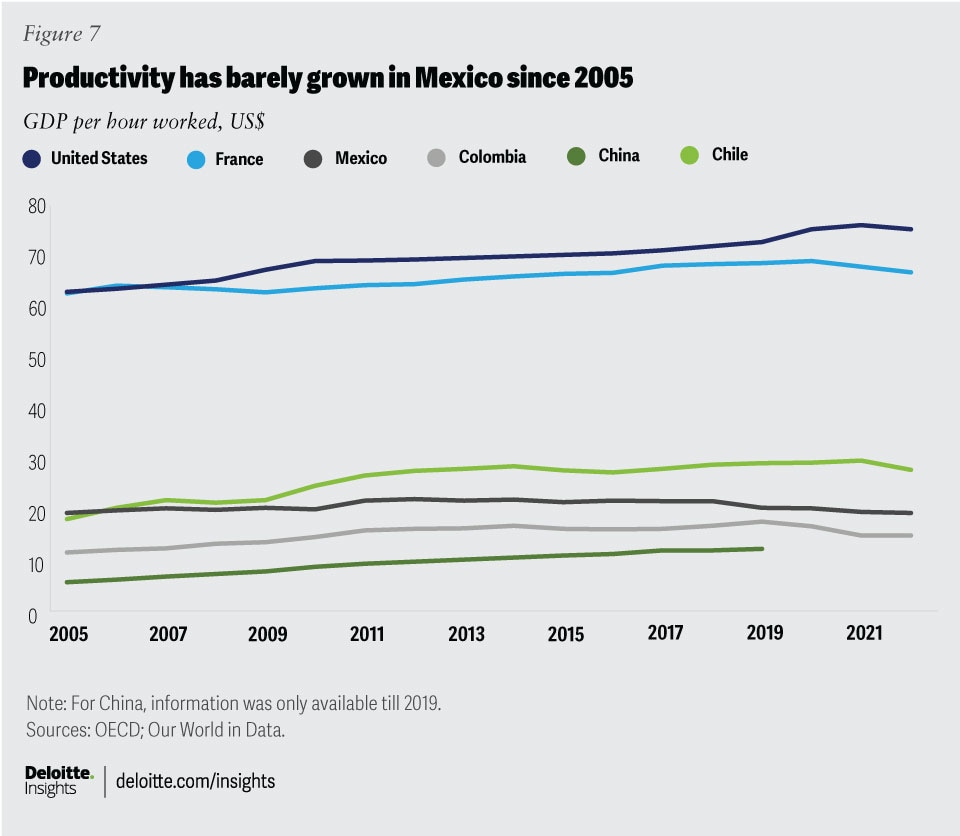

Although the current situation (nearshoring, higher real wages, USMCA, etc.) has been successful in boosting the observed growth, investments needed to improve productivity remain a challenge. Productivity in Mexico, which measures output per labor hour, has remained practically unchanged since 200511 (figure 7). This trend seems to be changing in the manufacturing sector where productivity grew 4% in 2022 compared to 2021, and it is now 10% above 2005 levels. In fact, investment in machinery and equipment—something that increases efficiency and production capacity—is growing in a manner not seen since 2011. In the first half of 2023, it grew 20% compared to the same period last year.

However, there is still a lack of public and private resources to capitalize on the “Mexican moment” such as energy structures, water and natural gas infrastructure, technological centers, skilled labor force, and improved security among other factors that, if improved, could boost productivity and improve long-term growth trends. Policies promoting stability and ensuring fair application of the law would be essential, however.

Considering our assumptions, the nearshoring in Mexico may increase manufacturing production by 5% each year, exports by up to an additional US$50 billion a year, and FDI would rise 10% each year. All these factors would add an extra 2.9 percentage points to Mexico’s GDP in the next five years.12

The “super peso”

Over the last couple of months, the MXN has been a hot topic in all business conversations in the country. Having appreciated by 19% in nominal terms since mid-2022, the peso has become one of the most attractive currencies among its emerging peers.13 Remittances, foreign investment, the rebound in tourism, and, specially, the attractive yield of Mexican assets, are driving the currency appreciation.

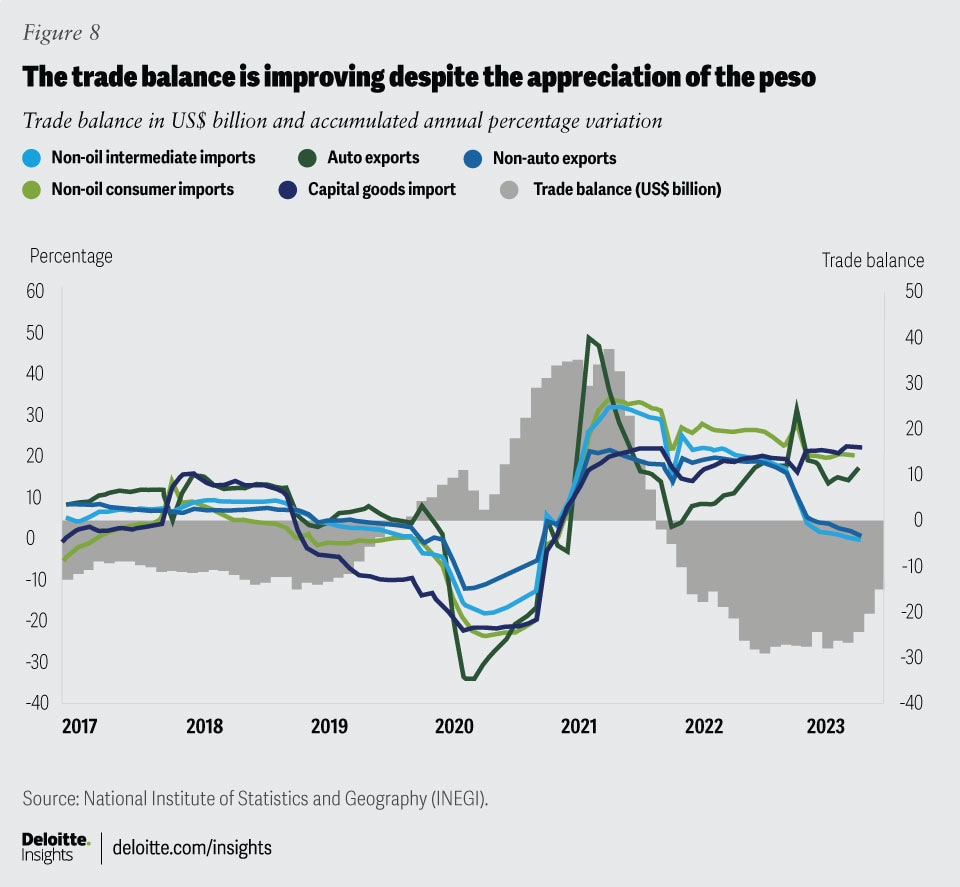

However, if this behavior continues, it will start to weigh on the economy, especially on exports that will become more expensive. But what we have seen in the last few months is that so far trade balance has improved despite significant currency appreciation (figure 8). Since July last year, the 12-month accumulated trade deficit has improved from US$28.1 billion to US$15 billion in July 2023, enhancing despite capital imports (22% in the first seven months of 2023 compared to the same period of last year) and nonoil consumer goods (20% YoY) expanding rapidly.

So, what is happening? Manufacturing exports are growing faster than nonoil intermediate imports. Mexico is a manufacturing country, and more importantly, it is a reassembler. It imports intermediate goods that it transforms into semifinal or final products, which are then largely exported. This phenomenon is quite significant in Mexican commerce, as manufacturing exports represent almost 90% of total exports, while nonoil intermediate imports represent 70% of total imports.

Auto production and exports have normalized as shortages of critical items like microchips have eased. Automotive exports have increased 17.3% in the first seven months of 2023 compared to the same period last year, while nonoil intermediate imports have decreased by 0.1% in the same period. This is the key reason why trade balance is still improving despite an appreciating currency. However, this trend would likely not last for a long time and as soon as auto exports finish catching up, we believe total manufacturing exports will start to decrease. In fact, nonauto manufacturing exports are weakening (maybe due to a more expensive currency), as they have only surged 1.2% YoY in the first seven months of the year, from 19.3% one year ago.

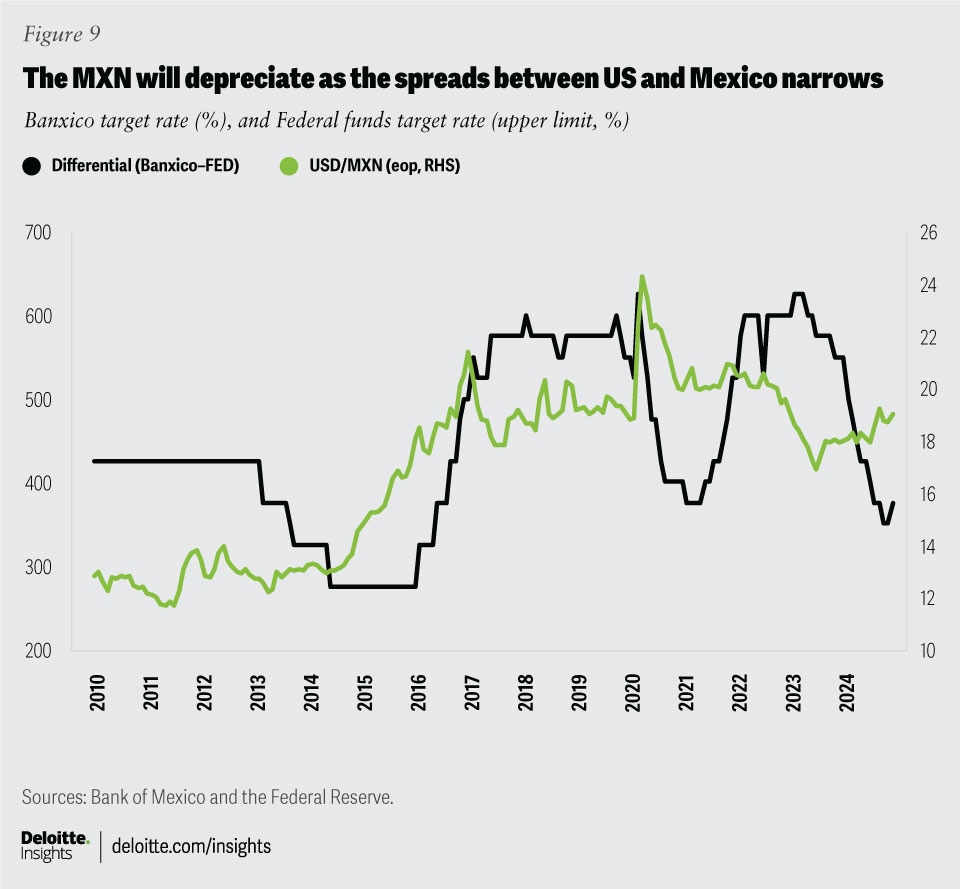

From our point of view, Banxico will not be able to start cutting interest rates this year, which will extend the period of wide spreads between Mexico and the Federal Reserve—that is, the MXN will continue to be attractive for a while. As a result, we expect this appreciation to persist for longer than we initially anticipated. We now expect the peso to stand around 17.9 by year-end 2023 (being 18.8 previously) and around 19.0 by the end of 2024 (being 19.7 previously).

By 2024, as we expect Banxico to start cutting rates before the Federal Reserve (February and September, respectively), the spread between the US and Mexican interest rates will begin to narrow (from 550 basis points in December 2023 to 400 basis points by the end of 2024). As this differential tightens, the Mexican currency will gradually depreciate.

Furthermore, as the upcoming presidential elections in June 2024 approach,14 volatility will increase, amplifying the depreciation of the peso. This would fade the current effects of the currency on the external sector including trade flows, remittances, and tourism flows.

Closing remarks

To sum up, Mexico took some time to grow after the pandemic (ranked 12th out of 16 Latin American countries in terms of postpandemic recovery), but it is now catching up. The country stands in a unique position to prolong this tendency, attract investment, boost productivity, and raise income and employment in a sustainable way. However, this opportunity comes with big challenges, since the country needs to invest more in public infrastructure, working capital, new technologies, and public policies. It is desirable that the new administration that comes into office next year may bring new proposals to really move forward toward the “Mexican moment.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}