What might be expected of business investment in a post-COVID-19 world? Economics Spotlight, May 2020

9 minute read

29 May 2020

The recession is here; now let’s talk about recovery—and more specifically, how business investment will fare in a post-COVID-19 world. We look at the recessions and recoveries of the past to better understand trends in business investment.

The focus on slackening consumer demand is giving way to talk of recovery. And when the recovery starts, business investment will play an important role. After all, it won’t really be a recovery until businesses are willing to bet on the future in the form of purchases of capital goods.

In this article, we look at how business investment fared during the previous recessions. While this recession is very different from those before it, looking at the past will give us a better idea of how businesses might behave once the worst is behind us.

What do businesses invest in?

The Bureau of Economic Analysis (BEA), the US government’s economic measurement arm, classifies business investment into three main types:

- Structures: Investments in buildings—for example, commercial buildings, factories, oil rigs, and power plants and cell phone towers

- Equipment investment: Includes machine tools, computers, transportation equipment such as trucks and trains, and other equipment such as office furniture

- Intellectual property (IP) products: Includes software purchases and development; business research and development; and movies, artworks, books, and similar products

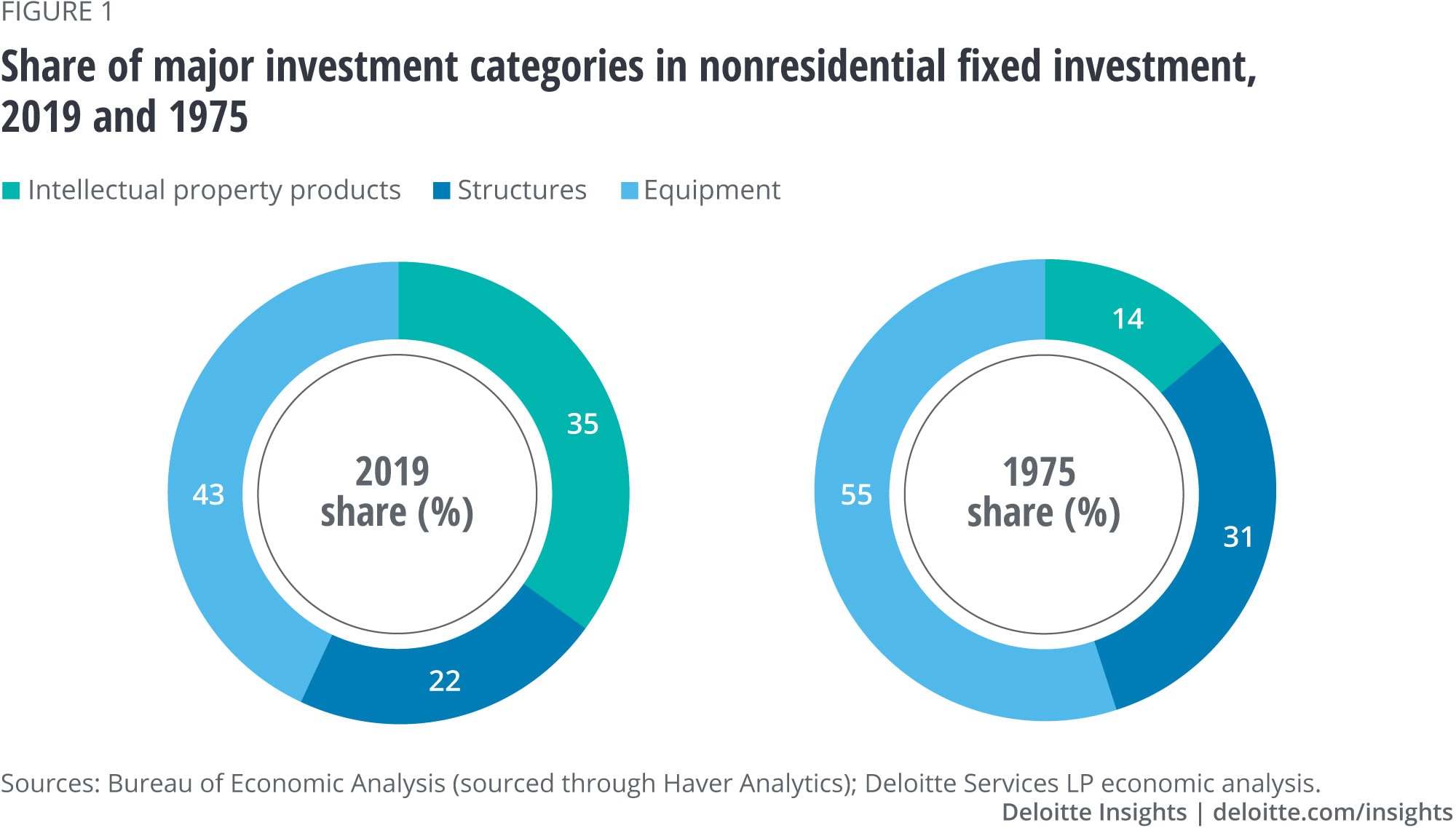

The composition of business investment has changed over time. Figure 1 shows shares of each of the three main types of investment in total nonresidential investment in 1975 and 2019 (the last full year available). The share of IP in business investment has gone up significantly since 1975, while investment in structures and equipment has declined during the same period.1

The duration of the investment recovery may be long and the pace of investment in businesses may be modest during the coming recovery

Learn more

Learn how to combat COVID-19 with resilience

Explore the Economics collection

Learn about Deloitte’s services

Go straight to smart. Get the Deloitte Insights app

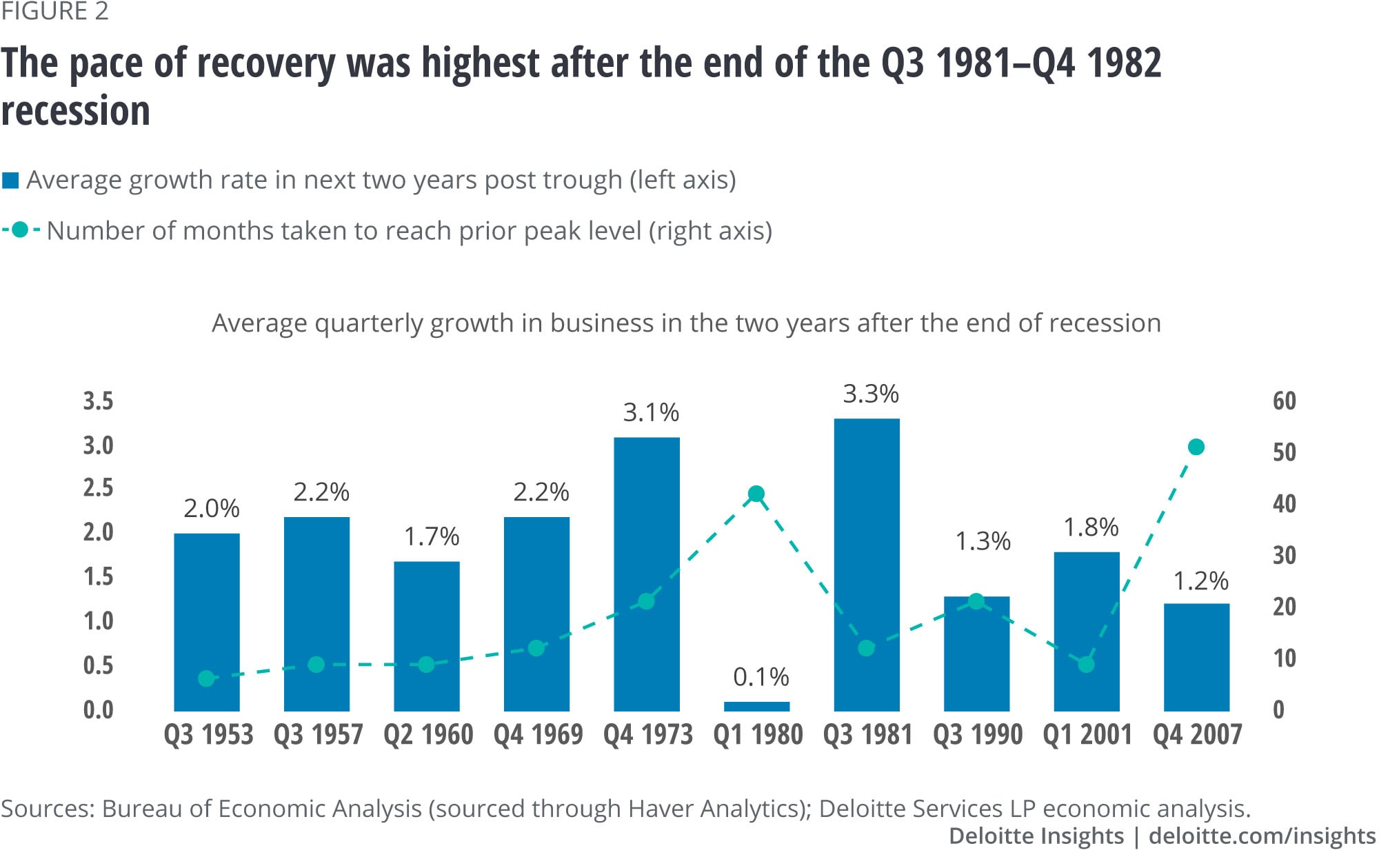

Businesses often start investing as soon as three months after a recession ends.2 However, on average, it takes more than two years to reach the pre–peak level of investment. And more recent recoveries have seen weaker investment growth post-recession. For example, after the 2007–2009 recession, business investment took 51 months—more than four years—to reach the previous peak (figure 2). Given the nature and scale of disruption and the accompanying uncertainty of the current downturn, investment is unlikely to pick up swiftly and may take a longer time to eventually return to pre-COVID-19 levels.

IP investment has been less affected by previous recessions and has recovered faster than equipment and structures in the past 10 business cycles. This suggests that businesses tend to prioritize investments on software and R&D even during recessions. Equipment recovers faster than structures after downturns. For structures, however, the average pace of recovery has been quite weak as demand for all types of structures has stagnated over the years. Recessions amplify the slow growth of this type of investment.

The past three business cycles offer insights on the current one

The past three recessions are most relevant than previous recessions for understanding how this recovery might look. This is because today’s economy is quite different than the economy of the 1950s, 60s, and 70s. Manufacturing is less important than it was, and information processing plays a much larger role in business investment.

Here’s how the main categories of business investment fared during and after recent recessions.

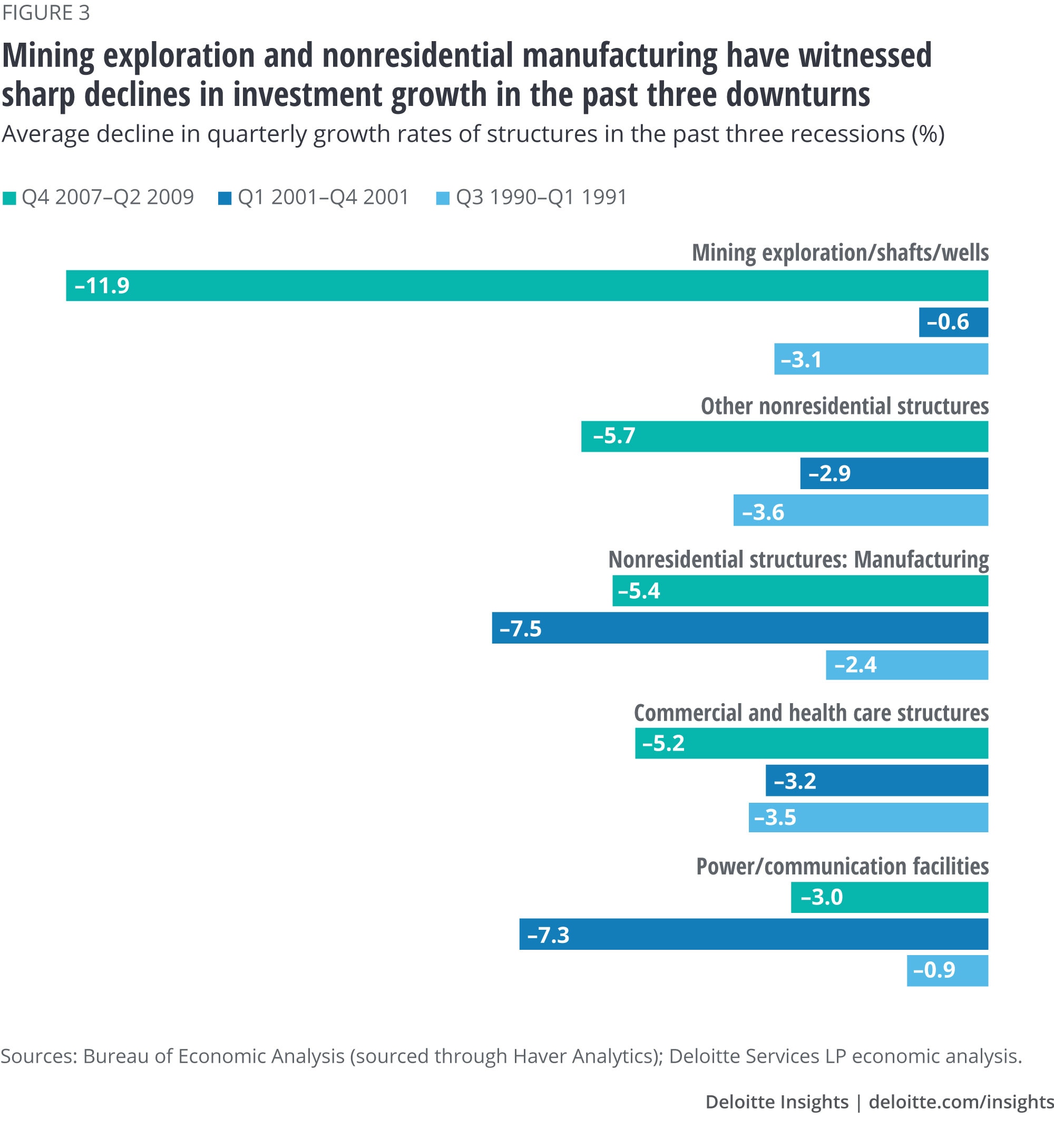

Structures: Investment in structures bottomed out much later than the official National Bureau of Economic Research (NBER) trough. Among its five subcomponents, mining exploration and manufacturing structures suffered more on an average during the past three downturns (figure 3). Investment in mining exploration is driven by the prices of oil and natural gas, the largest share of this type of investment. Mining recorded the highest decline in the most recent recession of 2007–2009 compared to other subcomponents. The other main cyclical components of structures are commercial and manufacturing structures. Both these components have also typically experienced longer downturns than the official (NBER) dating scheme shows for the aggregate economy. Businesses tend to cut back on such investments quickly and hold back their re-investing decisions for longer time periods.

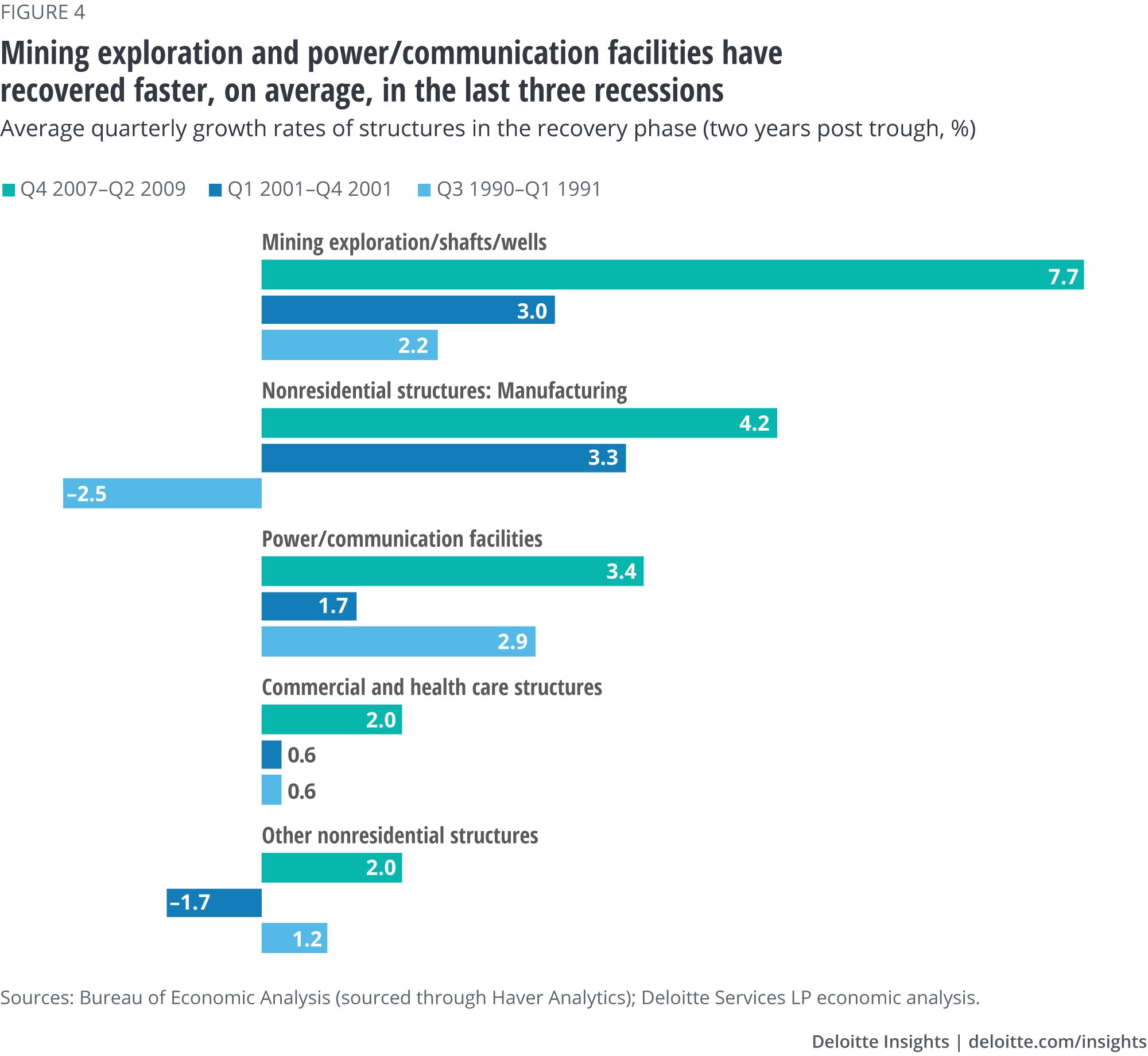

Mining exploration and power facilities have seen faster recoveries than other types of structures (figure 4). The average quarterly growth rate for mining and power facilities during recoveries was 4.3% and 2.7%, respectively, while both manufacturing and commercial structures recorded growth rates below 2%.

Equipment: Transportation and industrial equipment witnessed steep declines in the past three downturns (figure 5). A large share of transportation equipment is motor vehicles; purchases of these can easily be postponed as businesses experience excess capacity. However, transportation equipment also recovers very fast after downturns (figure 6). Industrial equipment on the other hand experienced weaker recoveries than transportation. This reflects the falling share of industrial equipment in total equipment from nearly 16% in 1975 to 9% in 2019. Investments in this area are likely to fall in the current recession and recover weakly afterward.

Information-processing equipment tend to experience only a limited impact during downturns compared to the other components of equipment investment. This is because the price of information-processing equipment has fallen over time, and investment in this type of equipment has been growing quickly over time, reducing the decline in spending in downturns and accelerating spending during recoveries.

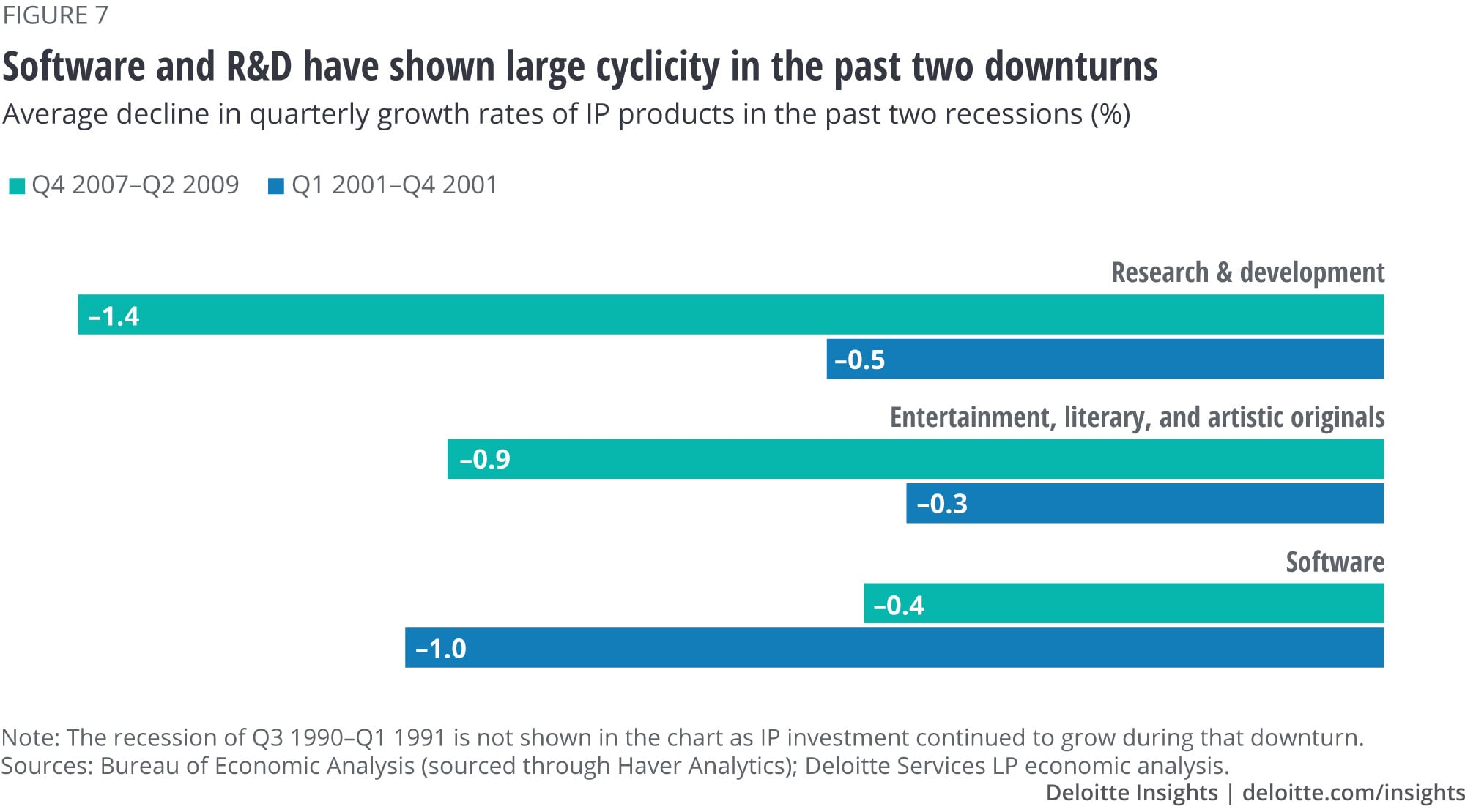

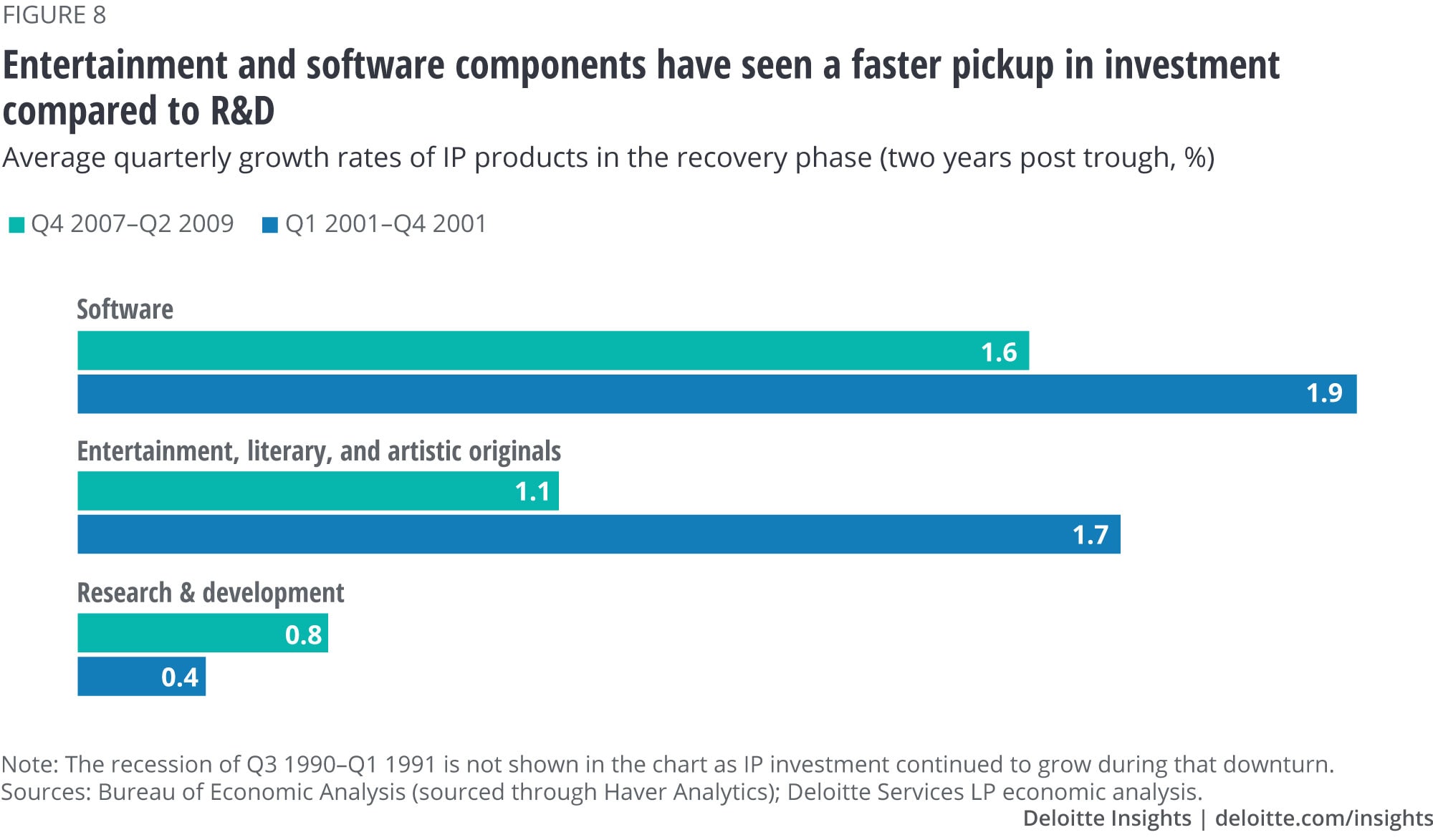

IP products: Overall investment in IP has comparatively been less affected by recessions than structures and equipment. There are two possible reasons for this. First, IP is growing relatively quickly, suggesting that long-term demand may be less affected by the cycle. Second, IP is often easier to finance than structures and equipment, so it is less affected by credit conditions. However, the past two recessions reveal that investment in IP has been more affected than in past downturns. Figure 7 shows that among its subcomponents, software and research & development (R&D) have shown significant declines in the past two downturns. However, investment in software bounced back faster after the downturn. R&D, on the other hand, witnessed tepid growth during the past two recoveries. This may be a matter of some concern as R&D is a key element in driving future productivity growth.

The post-crisis recovery

The scale of this recession will likely be much larger than recent ones, and credit conditions during the recovery may be very different. Business investment, however, will likely continue to follow the pattern set in other recent recoveries. These patterns reflect long-term shifts in the economy overall. Structures will likely experience a weak and late recovery. Investment in commercial structures may experience a particularly slow recovery due to increased adoption of work-from-home practices and a smaller need for retail space because of the growth of e-commerce among consumers. Equipment will pick up faster than structures. However, the overall recovery for equipment could be longer than usual, given weak manufacturing activity. Transportation equipment will likely see a faster recovery, while industrial equipment may not recover as quickly. And software will experience a strong recovery, while R&D may see only weak growth.

One possible difference is the potential for onshoring of production in reaction to the specific experience of this downturn. In some industries (such as health care), policymakers are already suggesting that the United States should reinvest in production capacity to reduce dependence on foreign sources.3 In other industries, business leaders are beginning to consider the desirability of duplication to create more robust supply chains.4 Such considerations may cause relatively fast growth in categories such as manufacturing structures and industrial equipment compared to the recent past.

Deloitte Global Economist Network

The Deloitte Global Economist Network is a diverse group of economists that produce relevant, interesting and thought-provoking content for external and internal audiences. The Network’s industry and economics expertise allows us to bring sophisticated analysis to complex industry-based questions. Publications range from in-depth reports and thought leadership examining critical issues to executive briefs aimed at keeping Deloitte’s top management and partners abreast of topical issues.

Learn more

Get in touch

- Dr. Daniel Bachman

- Senior manager

- Deloitte Services LP

- dbachman@deloitte.com

- +1 202 220 2053

© 2021. See Terms of Use for more information.

Explore our Covid-19 content

-

COVID-19 insights Collection

COVID-19 insights Collection -

Embedding trust into COVID-19 recovery Article4 years ago

Embedding trust into COVID-19 recovery Article4 years ago -

Confronting the COVID-19 crisis Podcast4 years ago

Confronting the COVID-19 crisis Podcast4 years ago -

The heart of resilient leadership: Responding to COVID-19 Article5 years ago

The heart of resilient leadership: Responding to COVID-19 Article5 years ago -

The Deloitte US economic vulnerability index Article4 years ago

The Deloitte US economic vulnerability index Article4 years ago -

COVID-19 and the investment management industry Article5 years ago

COVID-19 and the investment management industry Article5 years ago