Amid a recovery, consumers face off against inflation has been saved

Cover image by: Jaime Austin

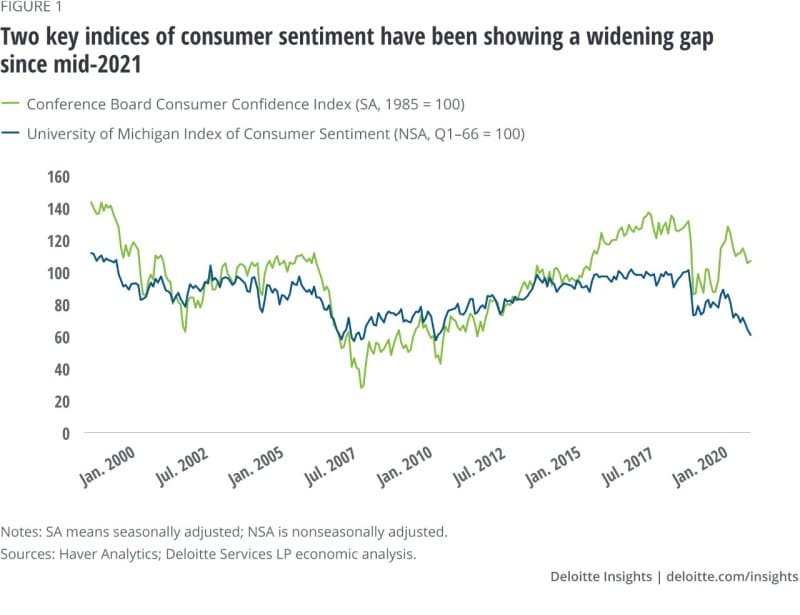

Consumers have been at the forefront of the postpandemic recovery, with real consumer spending growing by 12.1% in 2021.1 Sustaining this recovery in the medium term, therefore, depends much on their ability and willingness to raise their purchase volumes. So, it’s worrying to see different moods in two key measures of consumer sentiment. As figure 1 shows, the University of Michigan’s Index of Consumer Sentiment Index (ICS) has been trending much lower than the Conference Board’s Consumer Confidence Index (CCI) since early 2021. That’s unprecedented as the two measures have never given such different signals. Does that mean we don’t really know the pulse of US consumers? Thankfully, that’s not the case. The gap between the two measures is mostly due to inflation and its greater role in the ICS than in the CCI. This leads to a more important question: Does high inflation threaten growth in real consumer spending? The answer is yes. Rising inflation weighs on consumers’ purchasing power by slowing or even reversing gains in real wages and wealth. It often forces households—especially low- and medium-income ones—to pull back on discretionary spending. Worse, any higher-than-expected rise in inflation may force a stronger dose of monetary tightening, further weakening the impetus for consumers to spend. Inflation also hurts low-income households more than others, thereby widening income inequality.

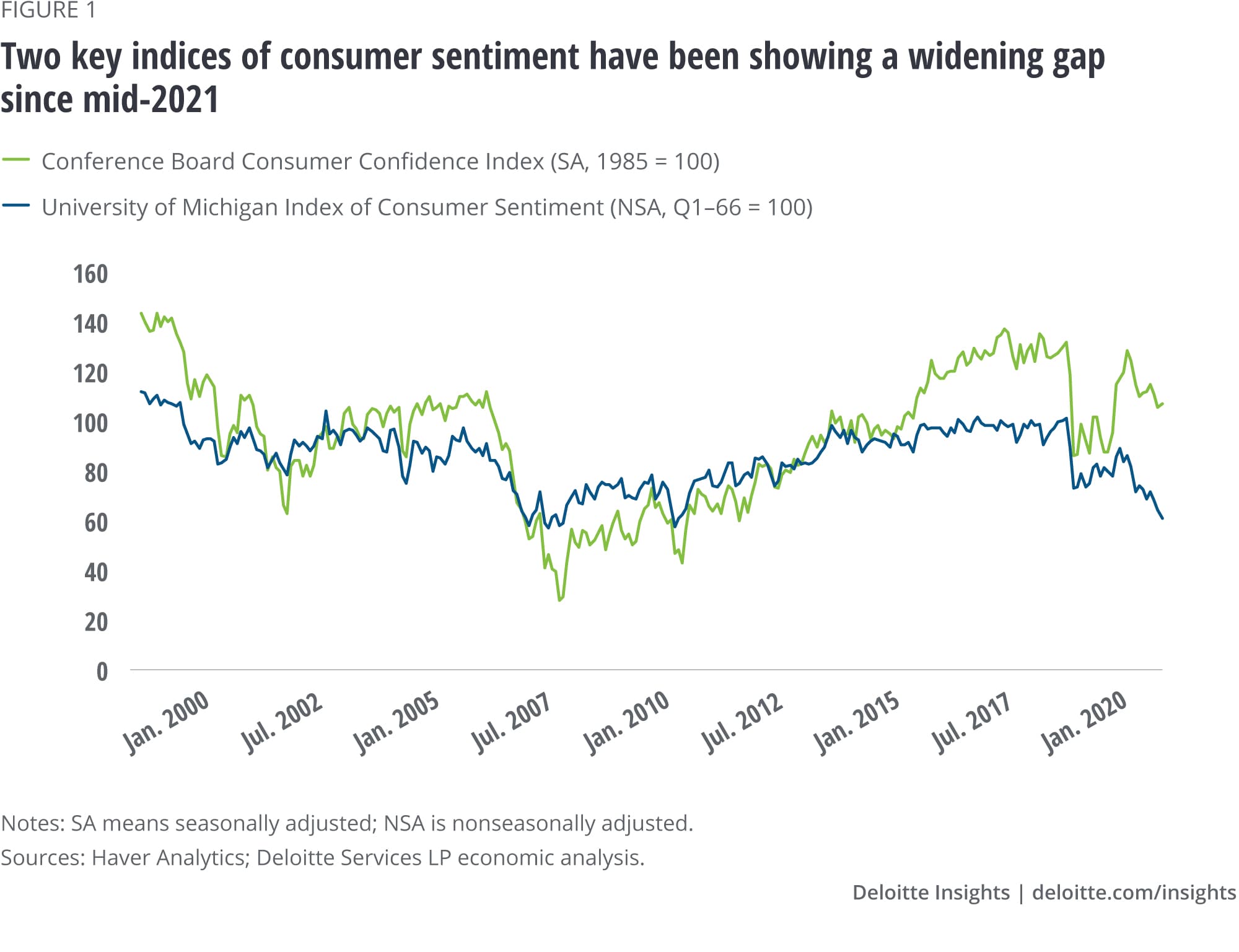

The ICS fell to 59.4 in March—the lowest reading in more than 10 years—with inflation dominating people’s worries about personal finances and economic growth. In the survey, expectations about inflation a year from now have edged up steadily since last year, to 5.4% in March. That’s not surprising given that headline inflation went up to 8.6% in March, the highest since the early 1980s. Core personal consumption expenditures (PCE) inflation, a gauge for prices that is tracked closely by the United States Federal Reserve (Fed), was at 5.4% in February and has been above the Fed’s target of 2% since April 2021 (figure 2).

Worries about inflation—as is overwhelmingly evident in the ICS data—do not find their way as much into the CCI, which puts greater emphasis on the labor market. That is a key reason behind the higher numbers for the CCI compared to the ICS. The labor market has been steadily improving since the deep shock in the first half of 2020 when the pandemic first hit US shores. While unemployment is now low at 3.6%, the employment-to-population ratio is closing in on prepandemic levels. It’s worth noting that the CCI does include a section on the impact of inflation. Its sub-index of consumer expectations has been trending down since last year because of concerns about future inflation, contrary to the sub-index of confidence in the current situation, which remained elevated during this period (figure 3).

High inflation and improving labor market conditions are opposing forces influencing real consumer spending. While strong job creation and declining unemployment have aided income growth, and hence spending, rising inflation can dent consumers’ momentum through three key effects.

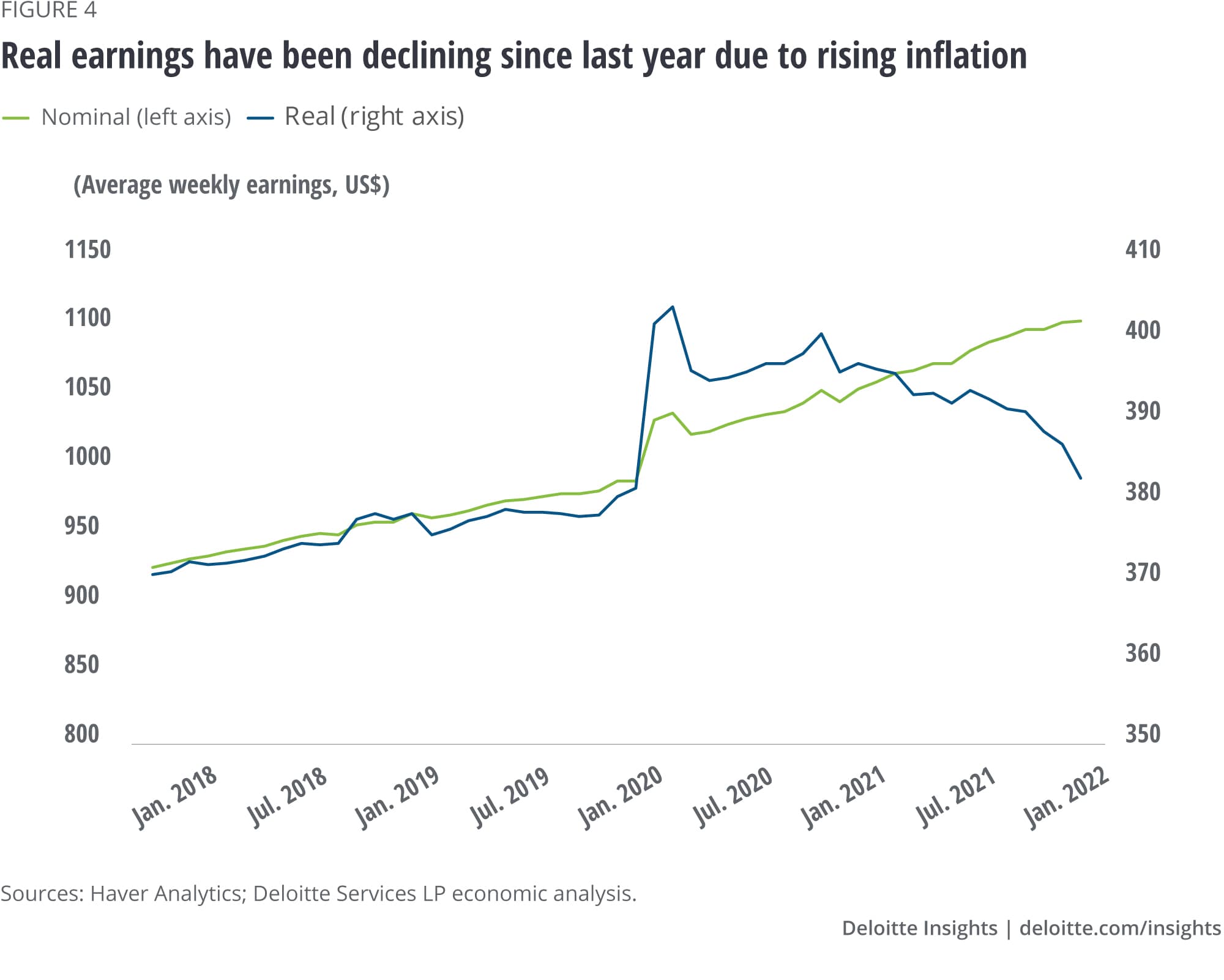

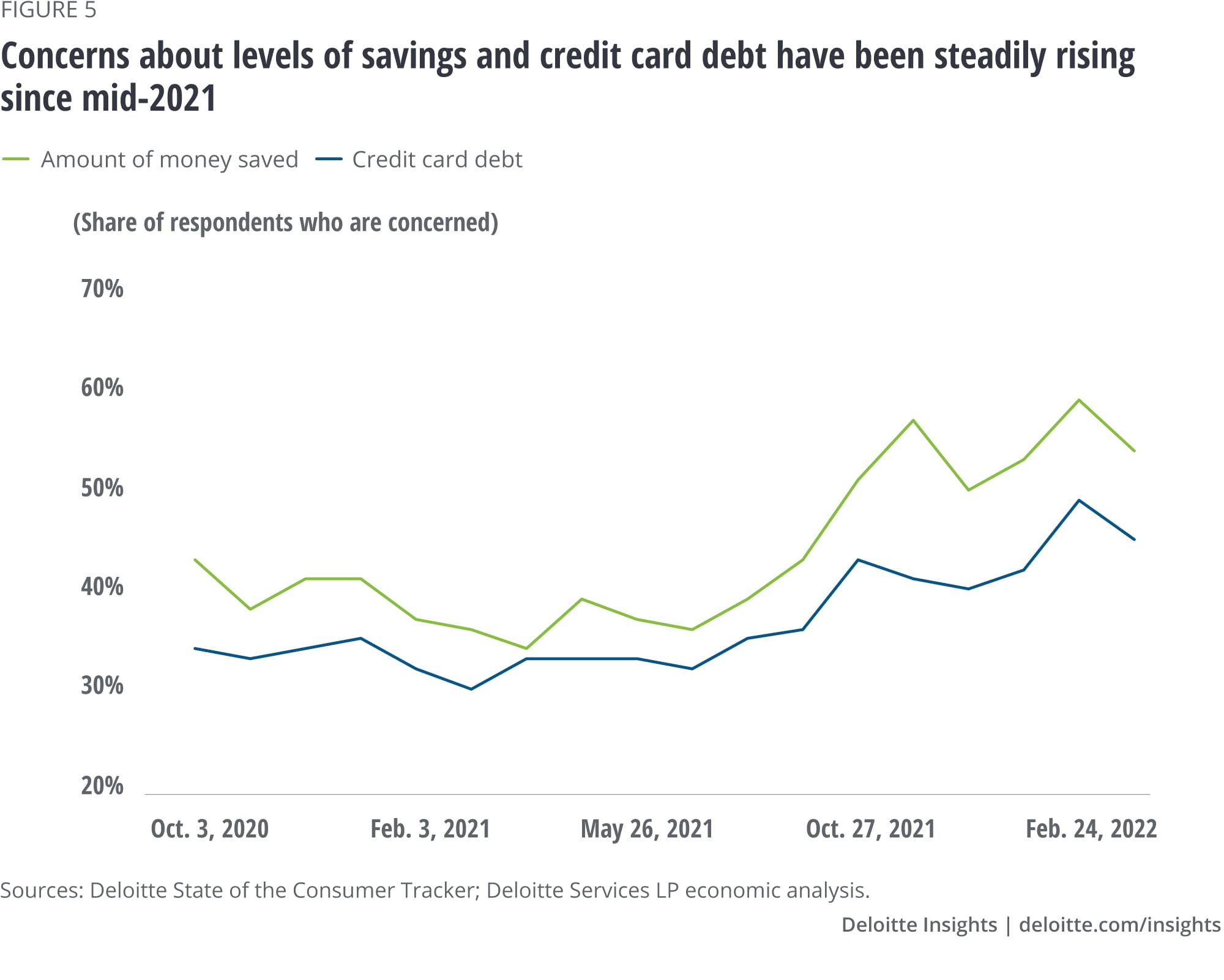

First, inflation has affected growth in real income, thereby curtailing consumers’ purchasing power. While nominal earnings continue to rise due to labor market tightening, real earnings have been on a broad downward trend since last year (figure 4). Since January 2021, as inflation has gone up, real average weekly earnings have fallen 4.5%, even while nominal earnings rose 4.8% in this period. No wonder then, that, consumers appear worried about their finances despite strong job growth. Deloitte’s survey of consumers reveals that as COVID-19 infection cases recede, concerns about personal finances are rising.2 In March, 54% of respondents expressed concern about the amount of money they were saving; this share has been rising since June 2021 (figure 5). It’s not just income that inflation dents but also gains in real wealth, which, in turn, has the potential to weaken the positive “wealth effect” on consumer spending. Real net worth3 of households in the United States grew 9.5% last year, slower than the 14.6% gain in nominal net worth. This differential will continue to widen if inflation remains high.

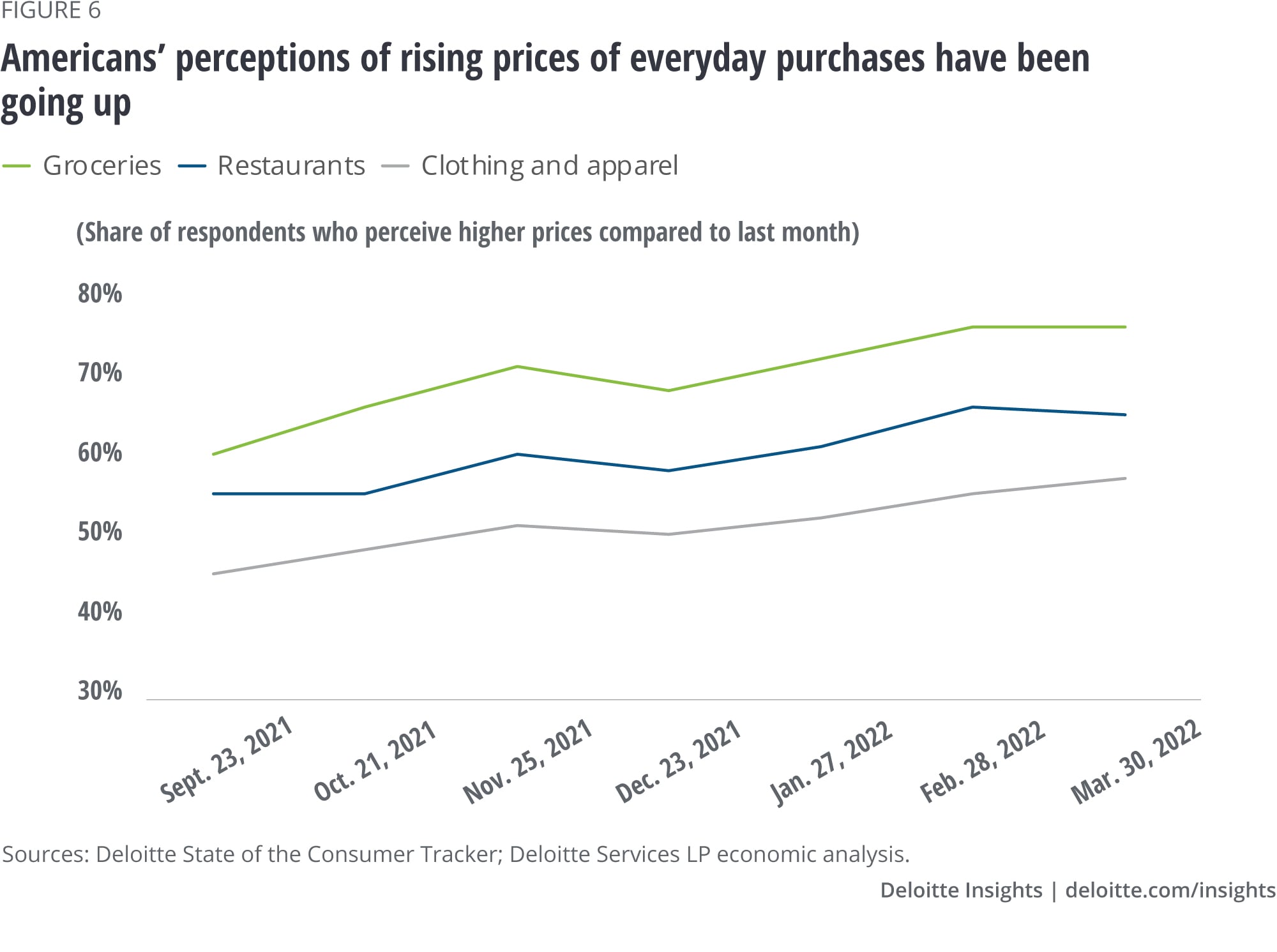

Second, as inflation percolates down to specific spending categories, consumers will increasingly substitute some items for cheaper ones, while reining in spending on discretionary items. Since essential items such as groceries are more difficult to substitute and with the prices of even cheaper substitutes going up, consumers—especially low-income ones—will need to cut other types of purchases. According to Deloitte’s survey of consumers, three in four Americans in March cited higher prices for groceries compared to the month before; the figure has gone up over the past six months (figure 6). Rising nominal value of purchases will weigh on personal savings and stretch credit card debt. The personal saving rate (6.3% in March) is now below prepandemic levels and worries about credit card debt, as figure 5 shows, have been rising steadily since the middle of last year.

Third, if high inflation persists, monetary tightening may turn out to be more than expected. This will impact credit growth and cost of borrowing. Those with high levels of credit card debt already paying high interest rates have much to worry as those rates are generally tied to the prime rate, which moves with the federal funds rate. Mortgage rates have also been rising since the beginning of 2021, with the 30-year mortgage rate reaching 4.95% by April 1.4 That is much higher than rates in February 2020 (monthly average of 3.66%), just before the pandemic started. Rising mortgage rates also come at a time of sharp rise in home prices. According to the Federal Housing Finance Agency house price index, home prices grew 18.2% year over year in January; price growth has been in double digits since October 2020.5 The twin effects of rising home prices and higher mortgage rates may turn off potential buyers and soften the housing market, which will then weigh on the value of housing in household balance sheets. More than others, households at the lower half of the wealth ladder are likely to be impacted by any housing slowdown as real estate has a larger share in their total assets. Real estate accounted for 53.4% of total assets held by households in the bottom half of wealth distribution, much higher than the shares for the 11–50 percentile cohort (34.6%) and the 2–10 percentile one (20.5%).6

While rising inflation poses risks to real consumer spending and hence, economic growth, its potential impact on income inequality is also worrying.

For consumers, inflation often leads to a wait-and-watch game as they adjust to rising prices and wait out the near-term impact of counter-inflationary policy on the economy. This year, that wait may turn out to be a tad longer. Oil prices, already rising in 2021, got a new boost due to the conflict in Ukraine. Producers struggling with rising input costs will now find it even more difficult not to pass on a part of that cost to consumers. And added to that, there may be more disruptions in global supply chains owing to COVID-19–related lockdowns and mobility restrictions such as the recent ones in Shenzhen and Shanghai in China.11

Unfortunately, it takes time for hostilities to end and businesses to clear backlogs. Until such time, US consumers will continue to feel the pinch of inflation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}