United States Economic Forecast

The Q1 2024 forecast indicates an optimistic outlook for the economy, buoyed by a strong job market, consumer spending, and exports. However, geopolitical risks and inflation concerns persist.

The US economy continues to surprise to the upside. Despite persistent fears around high interest rates, high inflation, slowing growth, and unsustainable consumer spending, the economy continues to deliver month after month. It is looking increasingly as though policymakers have managed to create the conditions for the mythical “soft landing,” where inflation is brought down to target without causing a recession.

Deloitte’s baseline forecast remains optimistic, and we expect the US economy to continue to perform well in the short term thanks to strength in the job market, consumer spending, and exports. For the first time since the pandemic, we have also included a scenario that is more optimistic than our baseline, as we see room for positive structural changes in labor markets and productivity.

But there is a reason why economics is called the “dismal science,” and economists are rarely comfortable with unalloyed optimism. We have, therefore, developed a scenario highlighting the short- and medium-term downside risks still clouding the outlook. Geopolitical risks are top of mind. Conflicts in Europe and the Middle East are already increasing the costs of shipping and some commodities. Depending on how they resolve, they could further threaten trade and the economic fortunes of American allies. Although inflation has come down significantly, it is stubbornly resisting moving into the 2% range.1

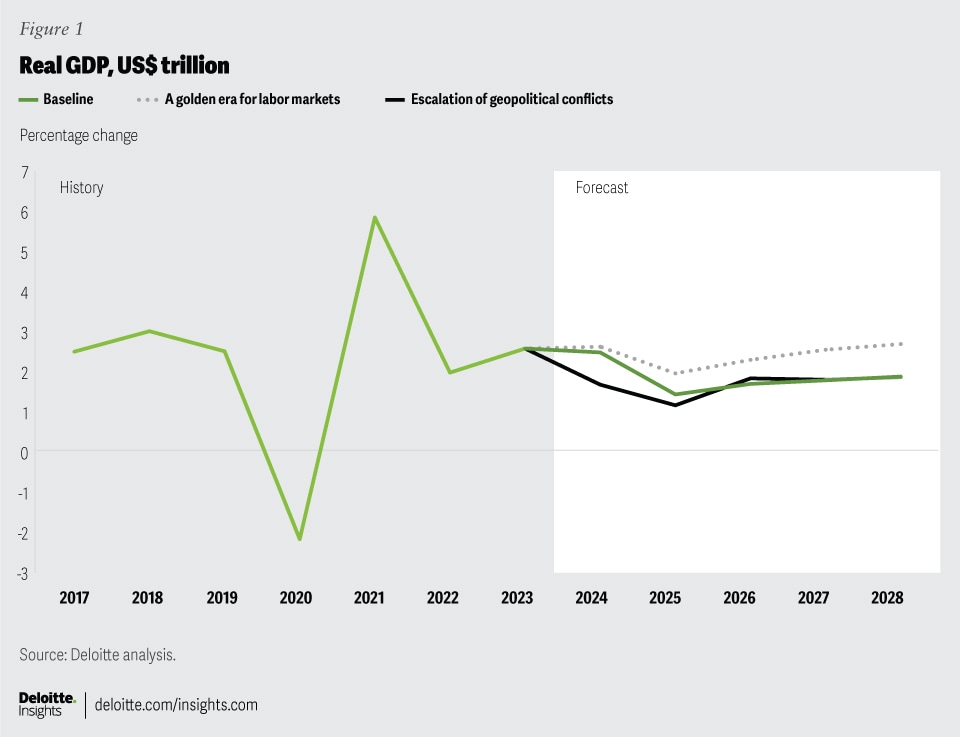

Scenarios

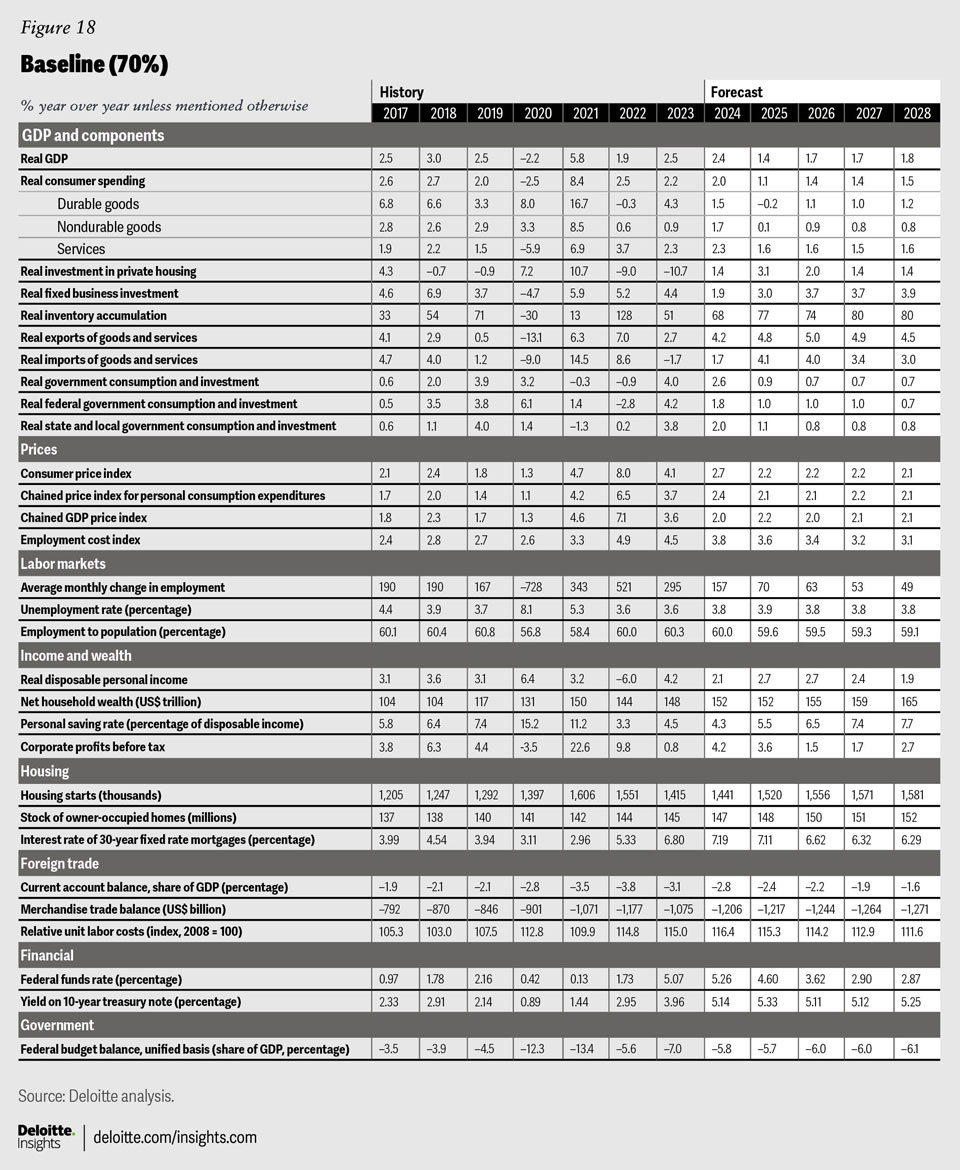

Baseline (70%): The economy’s strength in recent months is broad-based, with strong growth in all subcategories of GDP. We expect that strength to moderate a bit in the coming months, but the story is still positive overall. Consumer spending, investment, and government spending will all grow by at least 2% in 2024; exports will grow by more than 4%. Consumer price index inflation falls below the 3% threshold in the first quarter of 2024, though it remains close to that level for the first half of the year. The Federal Reserve succeeds in walking the tightrope to a soft landing by cutting rates twice in the second half of 2024 and continues with cuts until reaching the neutral rate of 2.5% to 3%. Job growth slows because current levels of job formation are not sustainable, given demographics and labor force participation. The unemployment rate peaks at 3.9% in 2024 before gradually declining, thanks to persistently tight labor markets. Major investments prompted by the Inflation Reduction Act provide a boost to manufacturing at home.2 Abroad, current geopolitical risks simmer but do not explode into larger regional conflicts.

Overall, despite an expected slowdown in the coming quarters, we expect the US economy to post real growth of 2.4% this year and 1.4% in 2025. Over the entire forecast, economic growth averages 1.8% per year, slightly higher than the long-term potential of 1.5% per year.

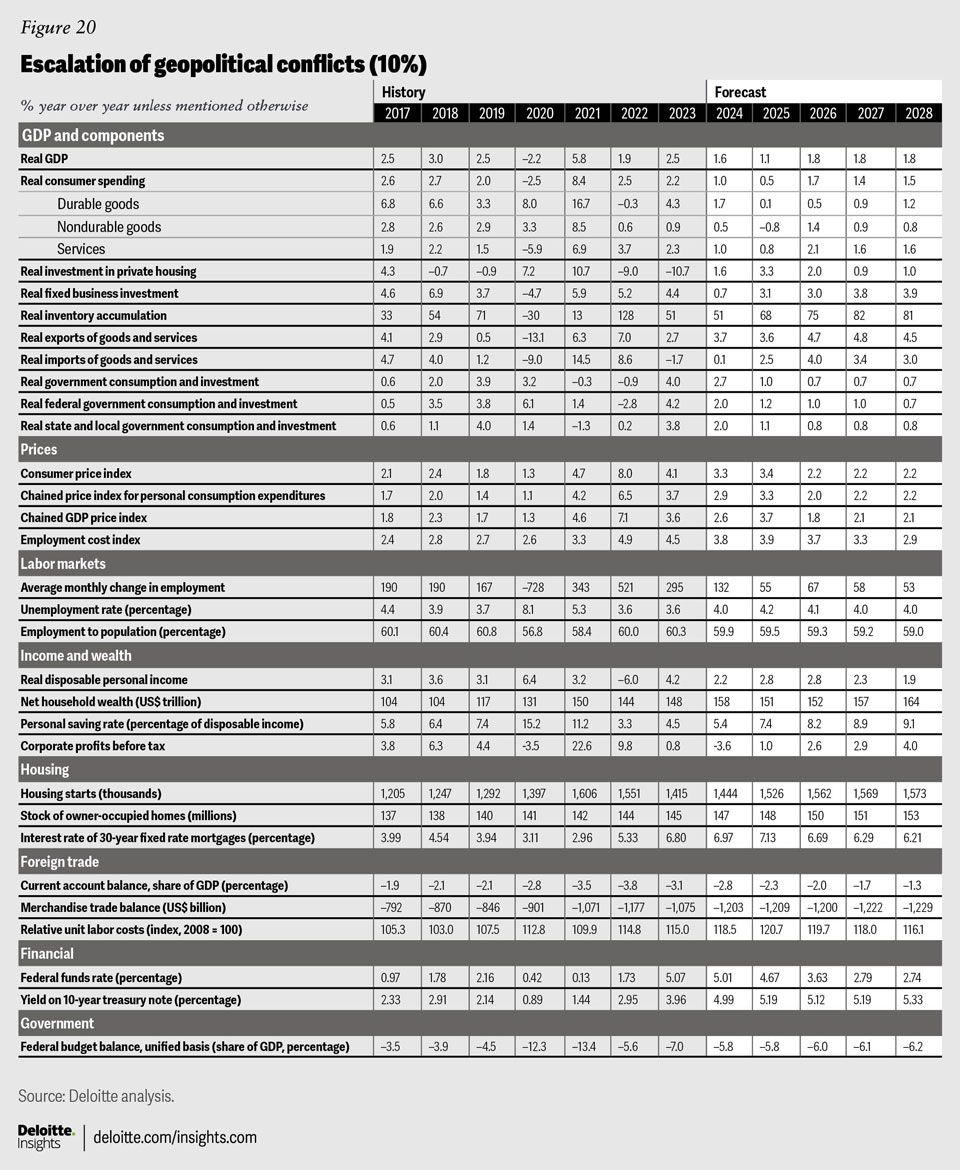

Escalation of geopolitical conflicts (20%): While today’s global conflicts have not yet resulted in direct engagement of significant American military forces, there is heightened risk that the United States could be brought into a significant conflict before the end of the decade. We appear to be entering an era of heightened geopolitical risk as conflicts involving American adversaries flare up in different regions of the globe. We have, therefore, included a scenario that examines the impact of geopolitical conflict on the American economy.

Geopolitical tensions increase as wars in Europe and the Middle East escalate, resulting in disruptions to trade and economic activity in the second half of this year. In this scenario, Eurozone GDP is flat in 2024 and declines by 0.3% in 2025. This, in turn, impacts the US trade balance as fewer American exports flow to one of its major customers. The escalating conflicts also lead to a significant increase in the price of oil. As a net oil exporter, the United States stands to benefit in some ways from oil price increases. But the magnitude of the increase has a knock-on effect on firms and households, and it helps to hold inflation higher for longer.

As the United States gets brought into the regional conflict, defense spending receives a boost. This acts to counteract some of the negative impacts from the Eurozone economic downturn and higher oil prices, as the defense spending is economically stimulative. While this mitigates the magnitude of the downturn, economic growth slows. Adjustment costs to the new circumstances and higher capital costs, as the US government borrows for defense spending, reduce capital formation over the forecast horizon. From 2024 through 2028, GDP will increase by an average of 1.6% per year, 0.2 percentage points slower than in the baseline forecast but still above the long-term potential—albeit barely.

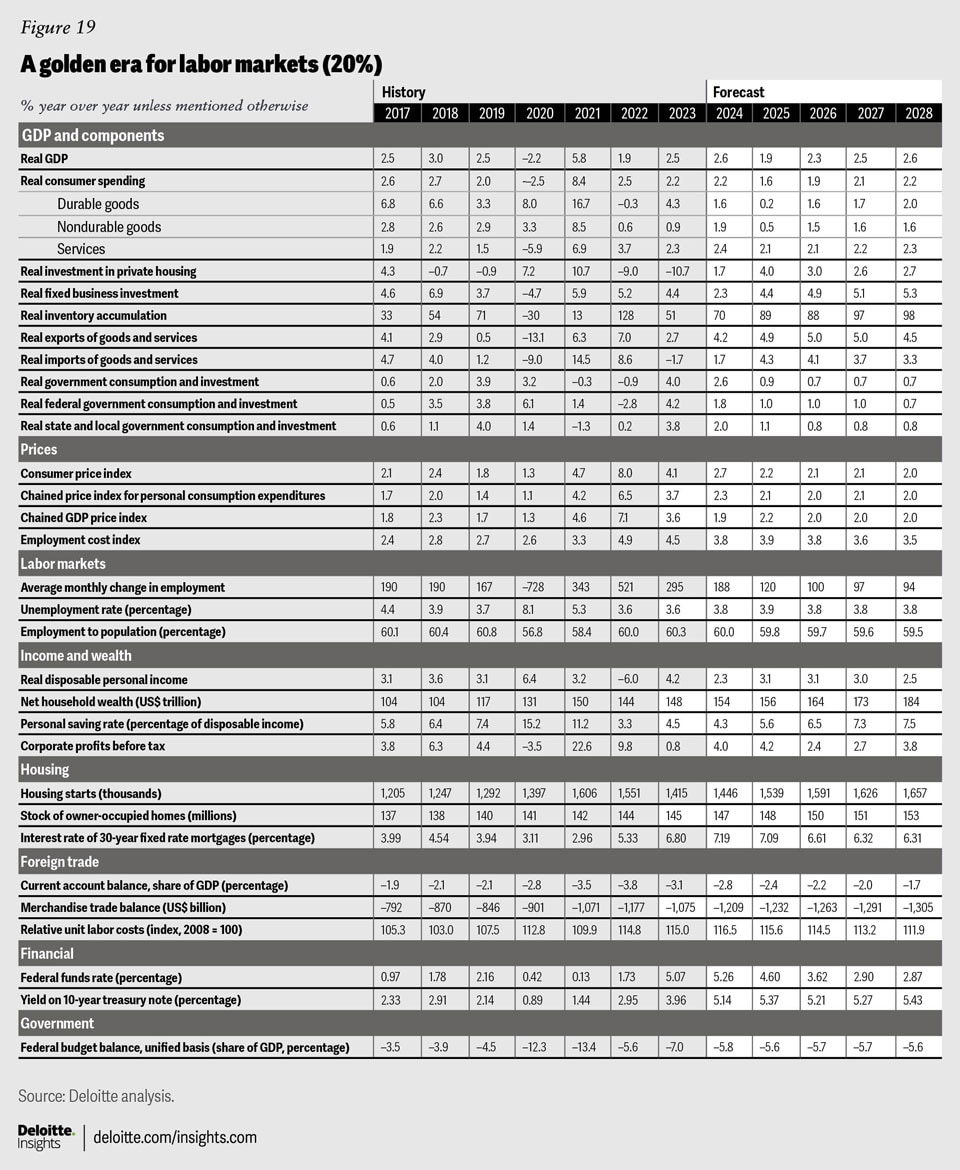

A golden era for labor markets (10%): Artificial intelligence is today’s popular buzzword, but the increasing sophistication and availability of technology and software has already been replacing some jobs and creating new ones. This kind of transformation will continue—and since technological change is not always linear, there is always the possibility of fast changes that help boost productivity significantly. In this scenario, the average annual growth of labor productivity grows at an average annual rate of 1.9% per year from 2024 through 2028, compared to 1.6% in the baseline.

In addition to the productivity dividend, population growth increases from an average of 1.6 million per year in the baseline to 2.1 million per year. As a result, the population will be 2.4 million larger by 2028. Labor force participation rates will be higher than in the baseline as older workers postpone retirement. With a larger population base, as well as a workforce working longer over time, there will be more people looking for employment—and with demand remaining strong, they will find it. Total employment levels will rise, with faster growth in the outer years of the forecast.

In this scenario, GDP will rise faster than the baseline forecast over the entire forecast horizon. From 2024 through 2028, GDP will increase at an average annual rate of 2.4% per year, 0.6 percentage points higher than the baseline forecast. This scenario also results in higher long-term potential for the economy at 2.3%, compared to 1.5% in the baseline. In that sense, this scenario shows what it would take to make recent rates of economic growth sustainable in the long run.

Sectors

Consumer spending

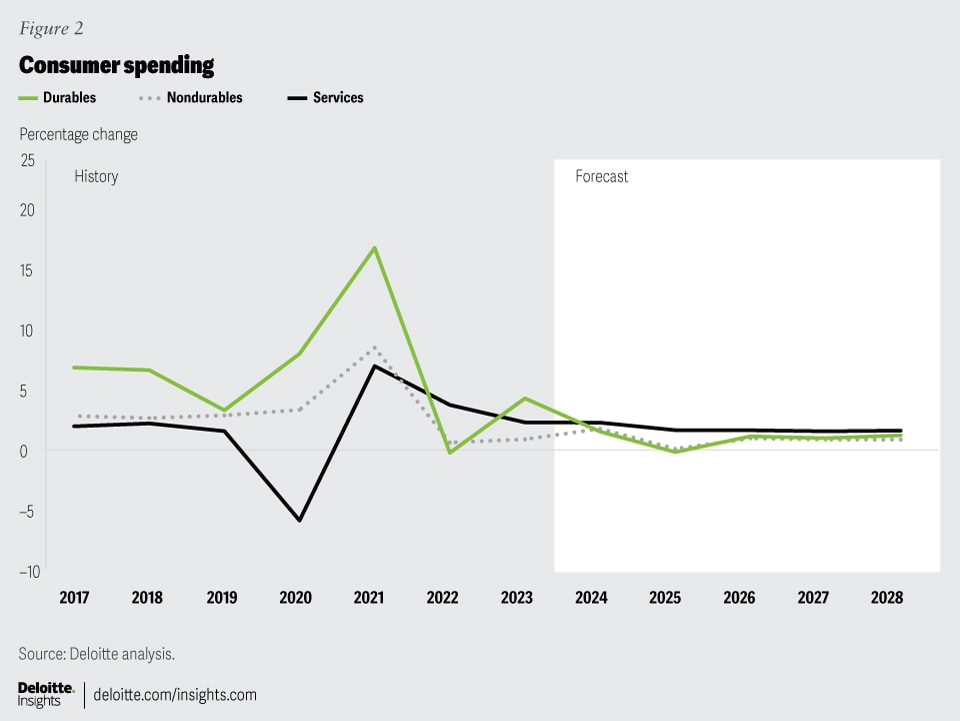

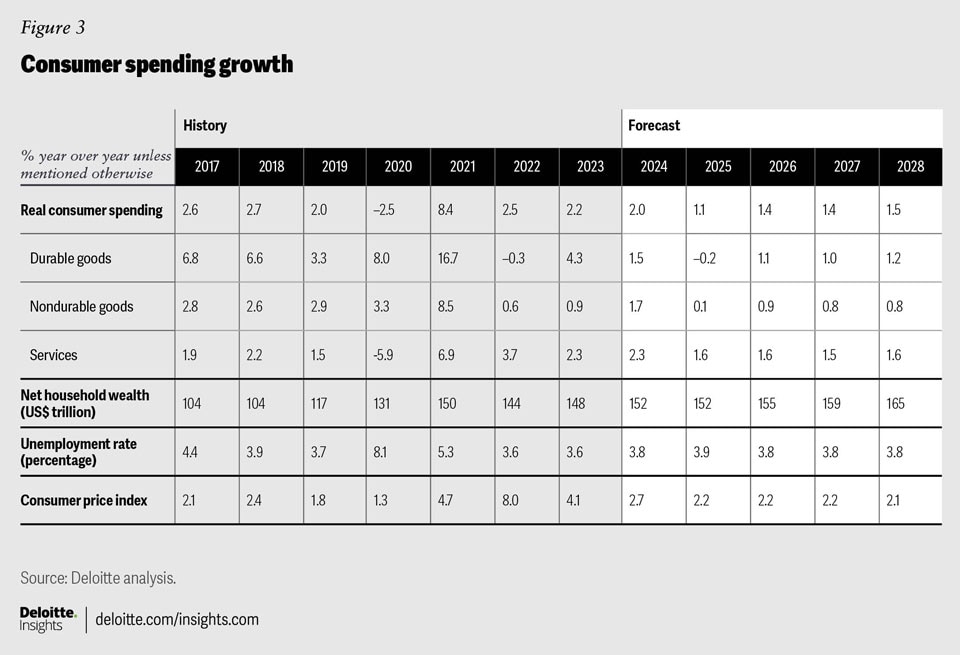

Real consumer spending has consistently exceeded expectations. The current pace of growth is buoyed by households adding new debt and spending the savings they built up during the pandemic. That means this pace of spending is not sustainable in the long run: Eventually, households will run out of excess savings and/or reach a ceiling on their ability to borrow. The precise timing of when that will happen—or whether that point has already come—is not a straightforward question to answer.3 Likewise, the amount of debt households can accumulate depends on other variables, not least of which is the interest rate. Interest rate cuts this year may, therefore, provide more room for consumption to run. In our forecast, consumer spending continues to hold up strongly, but grows a bit slower than overall economic growth. This should bring spending back to sustainable levels over the next couple of years.

There is a big divergence in the forecasts for durables and nondurables. With fewer opportunities during the pandemic to spend money on nondurables and services—like travel or meals out—spending on durable goods saw a historic increase. Now that households have already bought their new televisions and ovens, they don’t need to repeat that spending, so we project durables spending will rise by just 1.5% this year before declining by 0.2% in 2025. Thereafter, durables spending is fairly flat throughout the forecast. On the other hand, we project nondurables spending to grow by 2.1% this year and by 1.3% in 2025. Growth in nondurables spending remains much stronger over forecast than for durables. Services spending will grow by 2.3% in 2024 and 1.6% in 2025.

Our headline numbers are already in real (inflation-adjusted) terms, but inflation has an impact on the composition of spending baskets. Recent data from the US Department of Agriculture suggests that the percentage of their income that households spend on food is now at its highest level in three decades.4 That reflects both the fact that food prices have increased faster than other prices, and that households prioritize essentials when having to make cutbacks due to higher prices. As price levels stabilize and wages are adjusted for past inflation, this effect may recede. But, in the meantime, these distributional changes have impacts on the amount of disposable income households have to spend on other items.

Housing

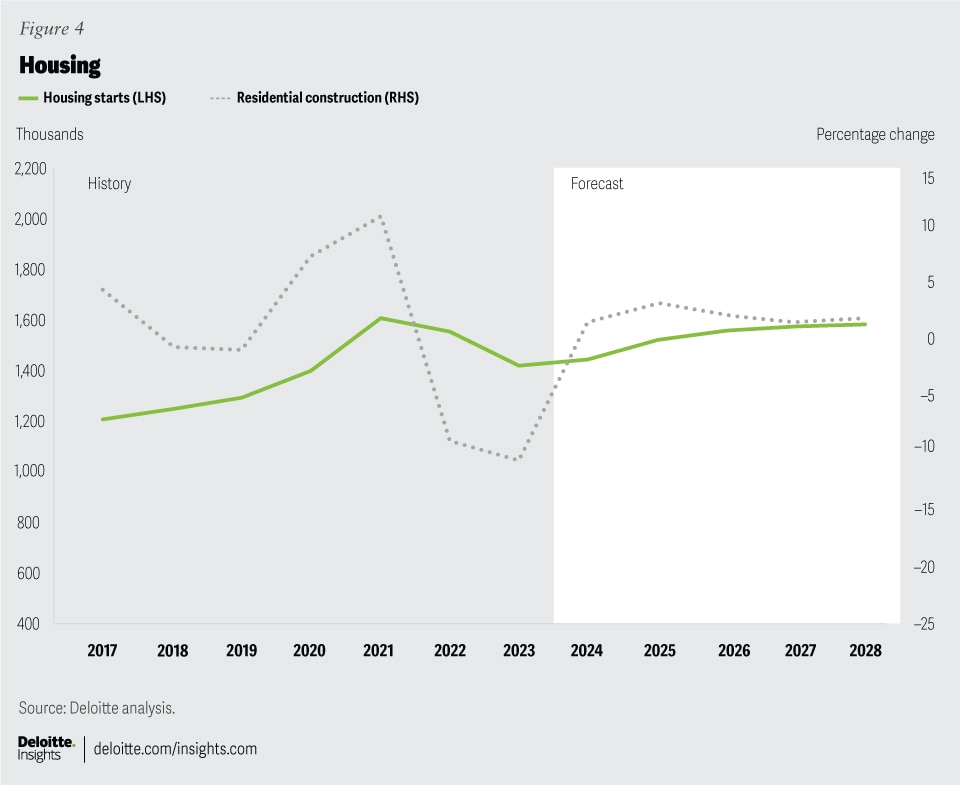

A limited inventory and lack of turnover have been pushing housing prices up. According to the National Association of Realtors, the median sales price for single-family homes was US$372,000 at the end of 2023, up 42% from the end of 2019. With interest rates elevated, families who can remain in place are avoiding selling their current homes as they wait for a more favorable borrowing environment.

The good news is that high home prices should lead to higher starts as builders respond. We project that the level of housing starts will stabilize at just over 1.5 million homes per year over the forecast horizon. This is above the pace of building from 2008 to 2019, and about in line with what we have seen since the pandemic. This level of construction is positive; after accounting for depreciation, it means the housing stock will be growing slightly faster than the total population over the forecast period. But to have a real impact on affordability, a higher proportion of these homes will need to be “starter homes” and be built in parts of the country experiencing the strongest population growth and population inflows. We think this will continue to be a challenge, and as a result, we have benchmark housing prices rising faster than inflation through the forecast period at a rate of around 3% per year.

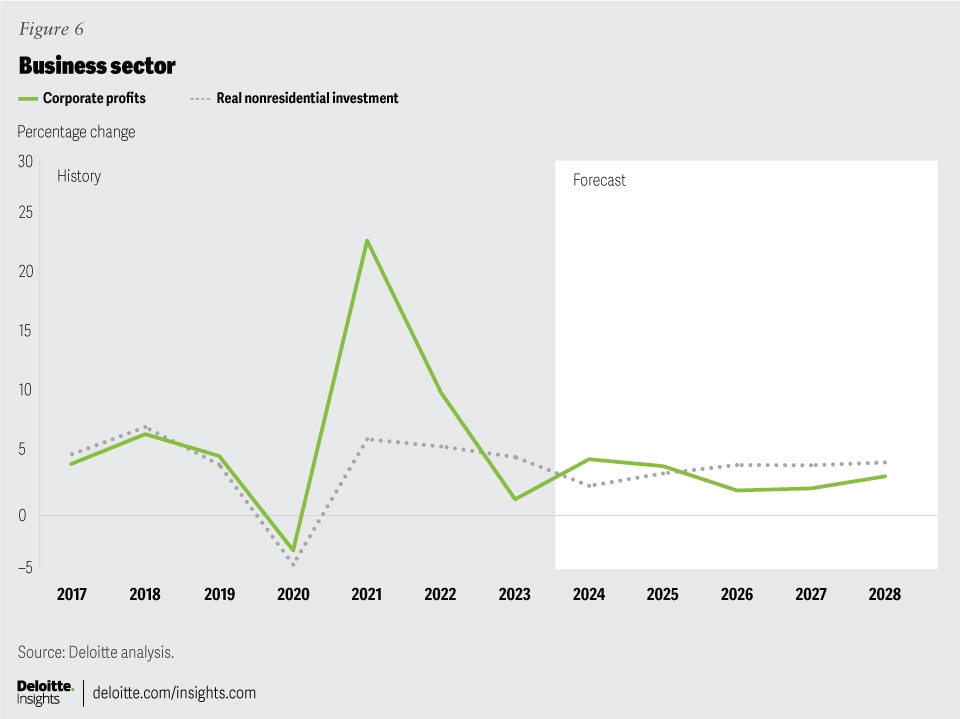

Business investment

Investment is spending that helps grow the long-term productive capacity of the economy and, as such, is the most important sector for understanding an economy’s potential. One of the challenges of higher interest rates is that while high rates help rein in inflation in the short term by bringing down demand, they can paradoxically cause inflationary pressures to persist for longer by making it more expensive for firms to invest in the capacity to produce more and relieve supply pressures. The average corporate borrowing rate has shot up to nearly 7% by the end of 2023, up from a low of 2.3% in 2020. The cost of borrowing will come down in line with the policy interest rate, albeit not until the second half of 2024, and consequently, we predict investment will be weak this year before picking up in 2025.

Like all countries, the United States will have to face the challenges caused by a rapidly changing climate. Some of these challenges are from a higher prevalence of extreme weather events such as hurricanes and drought, which lead to loss of life and property from flooding, wildfires, and damage to farmland. Other challenges are related to the need for increased economic investment to prevent even the worse effects of warming going forward.

The forecast shows spending on machinery and equipment growing by 1.3% this year and 3.2% in 2025. Machinery and equipment expenditures have rebounded to their prepandemic levels but have plateaued there. This type of spending—which captures everything from plant machinery to computers and office supplies—typically has had a strong upward trend over time, and we expect that strong trend growth to return in the outer years of forecast.

Investment in structures, which include both buildings and engineering structures such as power plants and oil platforms, has typically been much more cyclical. Spending here is driven by commodity price booms and economic cycles. Structures construction is still below its prepandemic peak, which in turn is below the all-time peak in 2008. We expect structures investment to grow by 3% this year and by a further 2.1% in 2025. This is a tale of two different fortunes: Some sectors are seeing strong investment in structures, but others are dragging down the total. Mining structures investment will be strong due to elevated oil prices, especially if geopolitical upheaval increases. Likewise, manufacturing factories will be a big contributor to growth, thanks to the investments of the Inflation Reduction Act and the CHIPS and Science Act.

On the other hand, the office and commercial building industries face grim outlooks. Although many companies have taken steps back from pandemic-era work-from-home policies, the supply of offices is still well above demand, and it is difficult to see how significant new construction could occur over the next few years.

The final major category of investment is investment in intellectual property, which includes software purchases, research and development spending, and, the smallest category, entertainment and literary and artistic originals. There was a considerable amount of investment in software during the pandemic as firms scrambled to adapt to new remote work realities. Those investments have already happened, so without some other kind of shock, we expect slower growth in this area in the next year or two. Over the longer term, the growth in investment in intellectual property will revert to the prepandemic rate as software and R&D continue to provide very high returns for US firms.

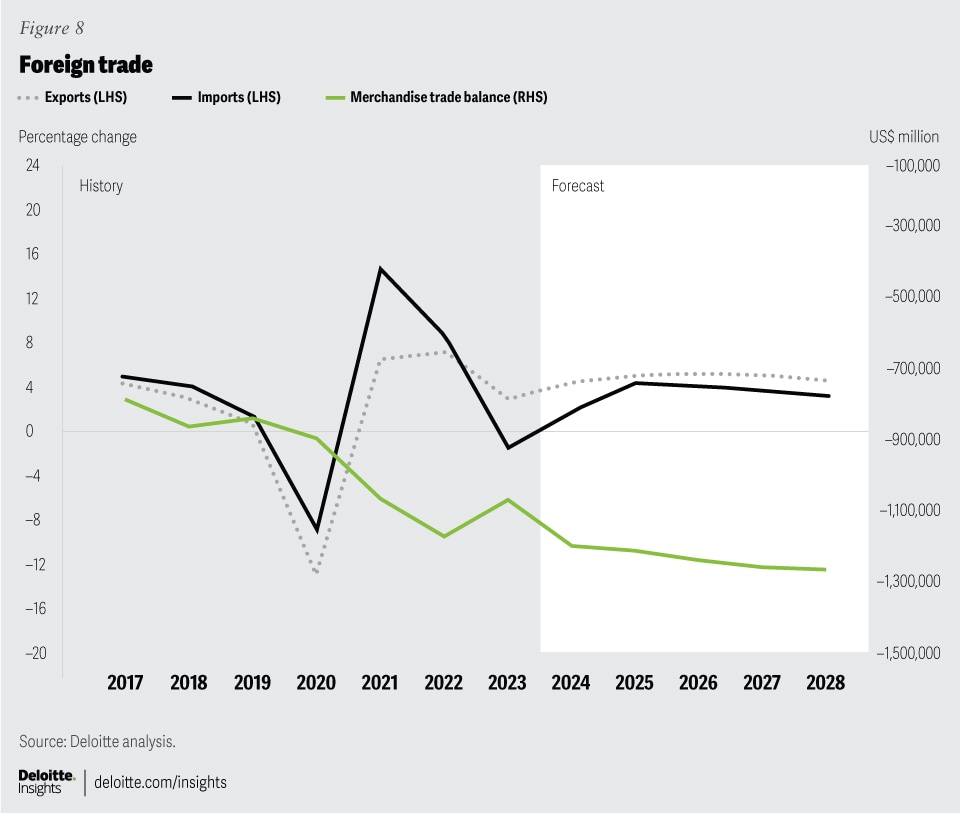

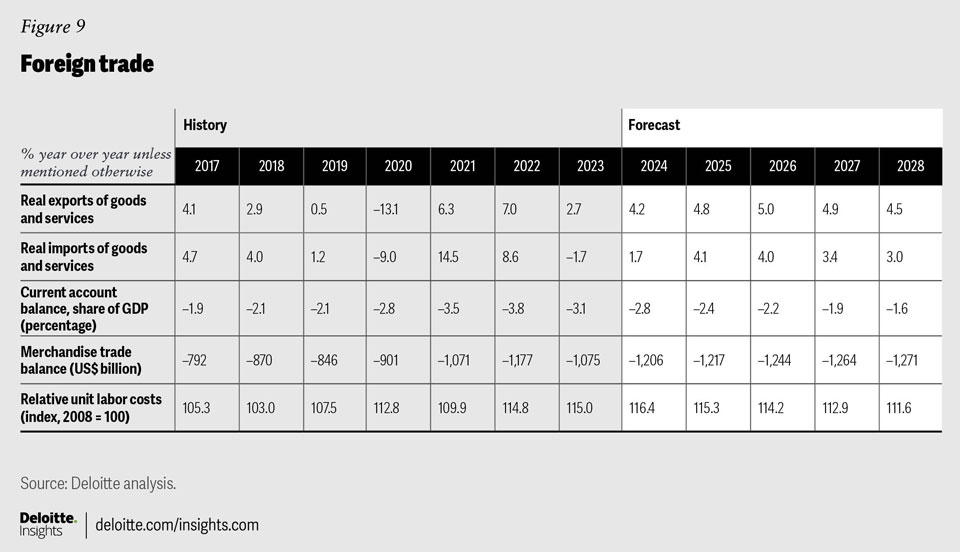

Foreign trade

Over the past two years, US export volumes have hovered around their prepandemic levels, while imports well exceeded prepandemic levels by the end of 2021. However, those dynamics have shifted in recent quarters, with imports falling in volume terms and exports rising.

Globally, the major stories on the trade front are disruptions in the Red Sea and Panama Canal. Since the beginning of the conflict in Gaza in October 2023, Houthi forces in Yemen have launched more than 30 attacks on vessels in the Red Sea.5 Operators have responded by rerouting traffic from this route to the (much longer) route around the Cape of Good Hope, which increases the travel time between East Asian and European ports by around 35%.6 While the Suez Canal route is less relevant to US exports and imports, the increased transit time on these routes has weighed on global shipping capacity and has resulted in an increase in shipping costs and timelines around the world.7

More directly relevant to American trade is the situation at the Panama Canal, where drought has forced the canal authority to reduce daily transits by a third.8 The Panama Canal route is very important to trade between Asia and the East Coast, and between Europe and the West Coast. Alternatives would require offloading cargo on the “wrong” coast and finding transcontinental rail capacity to move goods. Otherwise, the only alternative is to take the much longer route around Cape Horn.

In our baseline forecast, Red Sea disruptions won’t get worse but won’t get better either. Likewise, Panama Canal restrictions will remain at current levels and will not tighten further. The combined effects of these restrictions will put upward pressure on prices and prevent inflation from falling as quickly as it otherwise could this year.

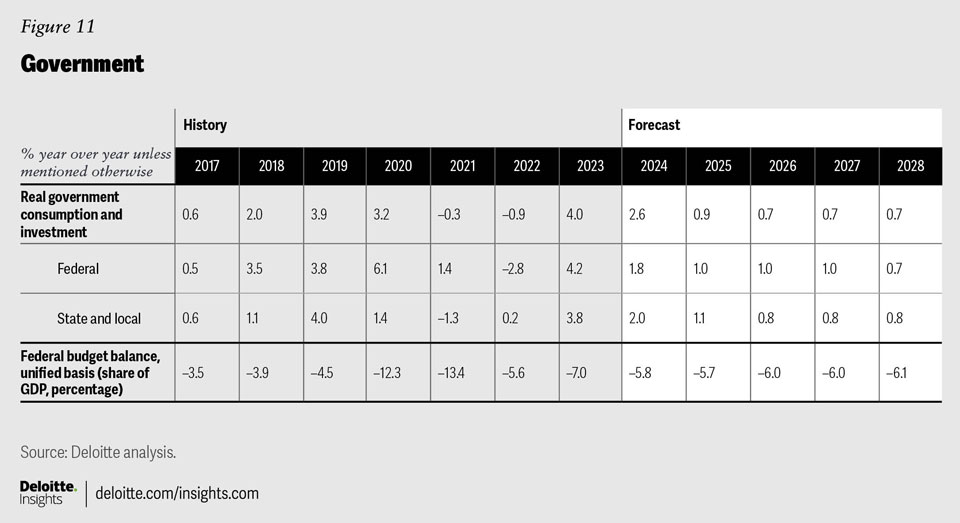

Government policy

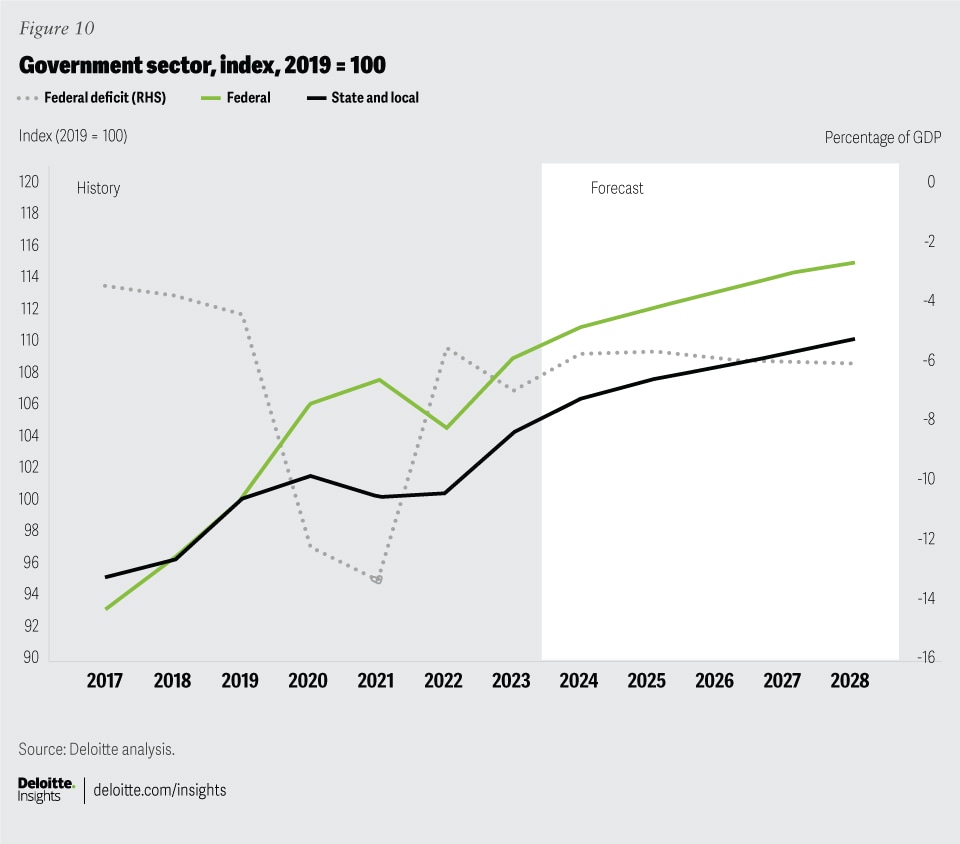

From a macroeconomic perspective, the most important government policy in recent years has been the Inflation Reduction Act. This piece of legislation has provided significant government backing for investments over the next 10 years to address climate change. The act also includes significant revenue provisions (totaling about US$864 billion), and the Congressional Budget Office projects that, by the end of its 10-year life, it will have reduced the federal accumulated deficit by US$77 billion.

Our baseline forecast projects the federal deficit will slowly rise relative to GDP over the forecast horizon. Even beyond this forecast horizon, the deficit is projected to continue growing, meaning that normal economic dynamics will not balance the budget without policy changes. The continued ability of the federal government to borrow at these levels will depend on investor confidence and global excess savings. Global excess savings are already in much shorter supply than in recent decades due to economic troubles in China. Against this backdrop, our forecast assumes that the 10-year federal bond rate will fluctuate between 5.1% and 5.3% in the outer years of the forecast. These would be the highest borrowing costs faced by the federal government since 2000, a reflection of the factors just mentioned.

While our baseline forecast projects that a government shutdown will likely be avoided, the repeated political wrangling over government funding is a source of risk for the economy. The constant threat of such a shutdown is a disruption to the business of government and a distraction from more important priorities.

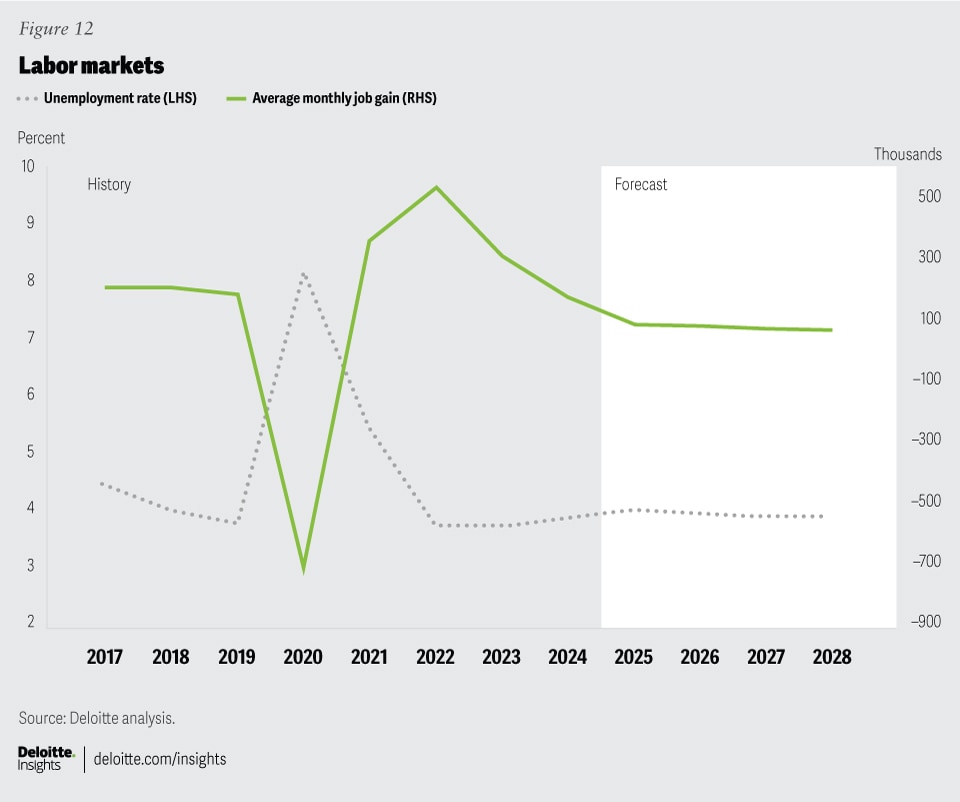

Labor markets

The labor market continues to surprise. In January, the economy added 354,000 jobs, an order of magnitude more than the 33,000 jobs it would take to keep up with trend labor force growth. While labor markets are not as tight as they were during late 2022 and early 2023, the pace of recent jobs growth sets labor markets up well for the year. In the forecast, these kinds of jobs numbers are unsustainable; a slower pace of employment growth lets the unemployment rate rise to a peak of 3.9% in our baseline forecast.

Employment stood above its prepandemic peak in January 2024. The participation rate is also now approaching its prepandemic level. This answers a question that many economists have been mulling over: whether pandemic-era declines in labor force participation were transient or reflect a “new normal.” With the help of the tight labor markets of recent years, the answer seems to be that they were transient.

In the longer term, demographic transformation will be the main driver of labor supply. Like many developed countries, the United States has an aging population and slowing population growth. Unlike some other countries, though, the United States is not yet at the point where the population growth rate is negative. But the slower rate of growth will act as a restriction on the supply of workers and will force difficult decisions for governments as the share of the population working and paying taxes shrinks. As the population ages, people are moving upward into age brackets with lower rates of labor force participation. At the same time, within most age groups, we are seeing participation rates climbing; the trend is particularly strong among older age groups, who appear to be working into their golden years in greater numbers. For now, aging is outweighing the secular increase in participation rate, and we expect the overall participation rate to fall in the long run.

The new demographic realities mean we have to recalibrate our expectations for the labor market in the longer term. Relatively low rates of job growth no longer reflect economic weakness so much as a lack of available workers. Between 2000 and 2019, the labor force grew by an average of 0.7% per year. Over the forecast horizon, we are projecting labor force growth of just 0.2% per year. This is a new reality that employers and policymakers will have to learn to grapple with.

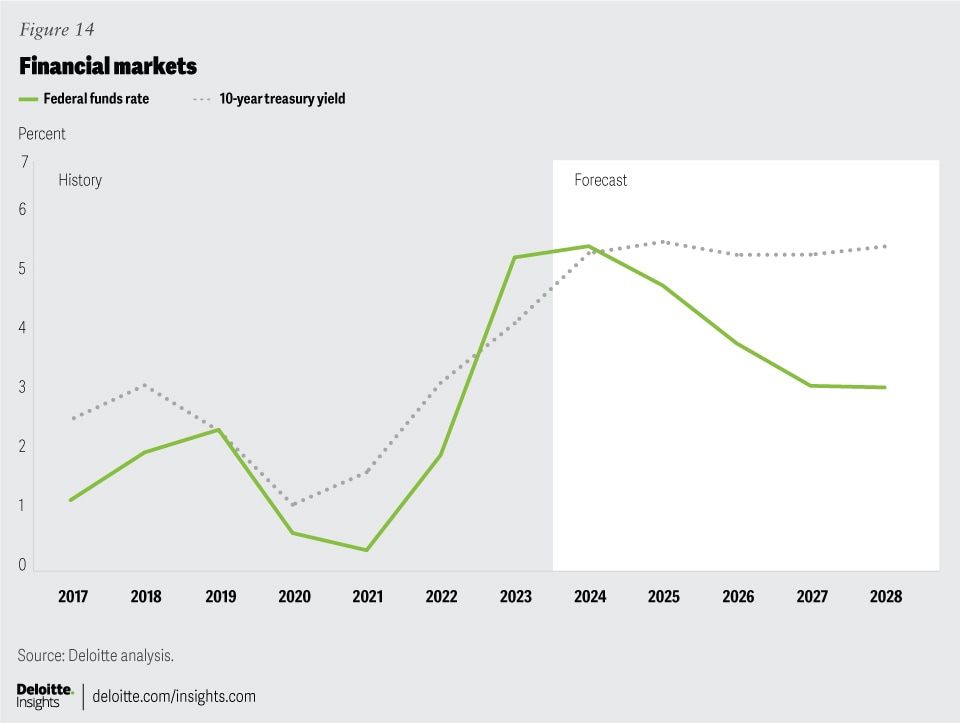

Financial markets

The forecast has the Federal Open Market Committee cutting the target rate beginning at the July 2024 meeting. We are forecasting two quarter-point cuts in 2024, bringing the Fed’s target rate range to 4.75% to 5% by December. Our view is consistent with the general sentiment in markets that the pace and timing of interest rate cuts will not be as aggressive as was once expected. We expect rate cuts will continue at a faster clip in 2025 and 2026 as inflation comes down in earnest, with rates finally turning neutral by the first quarter of 2027. Modelling from the New York Fed, and recent comments from the heads of several regional Feds, suggests the neutral rate now rests around 2.5% to 3%.9 Our forecast projects rates will settle at an average of 2.875% once the rate tightening cycle ends.

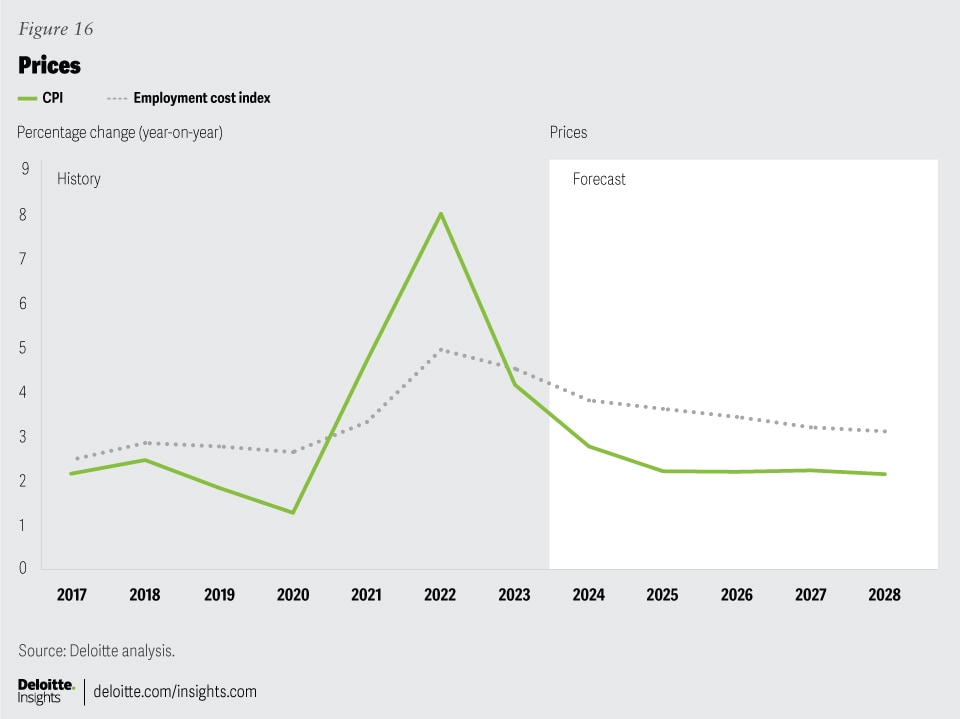

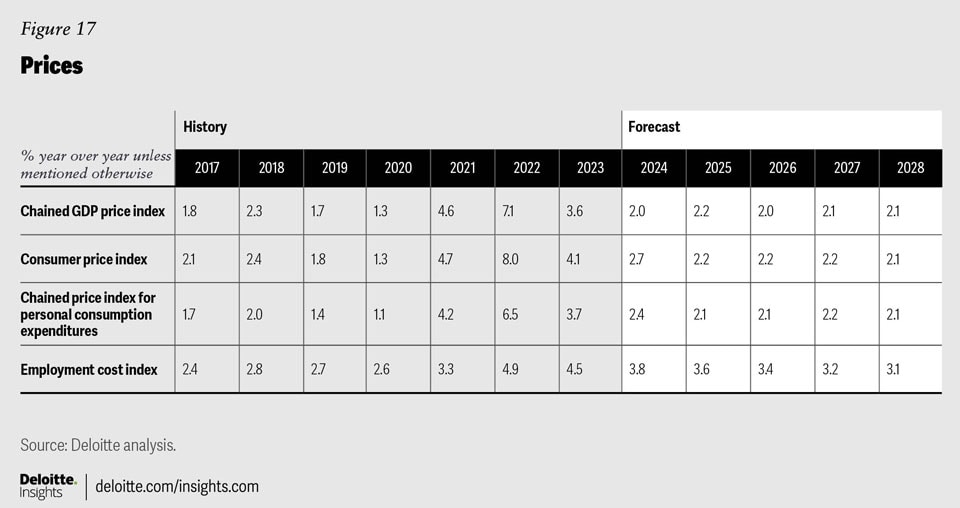

Prices

Policymakers have been remarkably successful so far at reducing prices without harming the economy and are on track to achieve the vaunted “soft landing.” As of January 2024, 12-month consumer price index inflation was running at 3.1% and core inflation was running at 3.9%. The Federal Reserve’s preferred measure, PCE inflation, is lower still: 2.6% as of December 2023. These are big decreases from the above-8% inflation we saw during the first part of 2022, but they are still above the Federal Reserve’s target of 2%, and the pace of decrease in inflation has slowed. Getting inflation down near 2% will require more time.

Our forecast, therefore, assumes that headline inflation will remain close to 3% for the first half of 2024, driven in part by temporarily elevated oil prices, before declining steadily starting in the second half of the year. Core inflation, on the other hand, will decline into the target band beginning in the second quarter of 2024, giving the Federal Reserve room to begin cutting rates.

Our forecast is also based on the assumption that long-term trend inflation will converge to 2%. We do believe the Fed will do everything necessary to make inflation converge to 2%, even if it means a slower pace of cuts—or further rate hikes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}