United States Economic Forecast has been saved

The author would like to thank Bhavna Tejwani for her contributions to this article.

Cover image by: Sofia Sergi

The great debt-ceiling debate/negotiation ended in something of an anticlimax. While debates about who “won” and “lost” will probably continue for years in both parties, there was at least one clear winner—the United States (and by extension, the global economy). Of course, this episode raises questions on the US Treasury’s ability to repay debt in the future, when Congress will have to raise the debt ceiling again. But for now, a breach of the debt ceiling—with the potential for throwing global financial markets into chaos—is off the table for the next two years. And a US government shutdown—with the potential for throwing the economy into a recession—is lot less likely. Given the high level of ill will in today’s US politics, the negotiators from both parties should be praised for their handling of the problem.

The agreement reduces the trajectory of Federal spending by a small amount, small enough to have little impact on the economic outlook.

This success does not pave the way for a perfect economy. The Deloitte forecast still shows the economy slowing substantially in the second half of 2023. The mixed nature of incoming economic data supports this forecast.1 This slowdown is not, however, a recession. There’s too much positive news, particularly in the labor market. The Sahm rule is a useful indicator of whether the economy is entering a recession. And there is no indication that we are anywhere near the threshold indicated by the Sahm rule.

The Sahm rule2 is a quick, real-time indicator of whether an economy is in recession.3 According to the Sahm rule, a recession is likely to have started when the three-month average of the unemployment rate is half a percentage point above the recent low level. Given the low level of the unemployment rate, and continued high level of job gain, things would have to turn around very quickly to trigger the Sahm rule by the end of 2023. That seems particularly unlikely when job openings are still far above the number of unemployed.

Although most of the economic data looks positive enough, the Fed’s earlier aggressive tightening cycle poses some risks. One risk, the need to mark low interest rate securities to market, has already appeared. So far, the Fed’s efforts to limit the impact of this problem appear to have succeeded. Although there is some evidence that lending standards are tightening (such as the results of the Fed’s most recent Senior Loan Officer Survey4), the volume of lending by small banks started to grow again after the shocks in March. Current lending conditions remain consistent with a slowing economy, not one that is entering a recession.

Soft business investment is another cause for concern. Business investment in equipment has fallen in the last two quarters, and investment in intellectual property products has also slowed. This may be a sign that businesses’ need for equipment and software to adjust to remote work is over, and that businesses are becoming unwilling to increase capacity. With business investment in structures (except for manufacturing structures) likely to remain weak over the five-year forecast horizon, overall business investment is likely to remain soft, with a potential impact on the wider economy. That is one reason that we expect very slow growth. But if investment falls substantially more than we expect, employment and consumption could follow.

Foreign growth is likely to remain problematic. Europe has, so far, managed surprisingly well. But the potential for further problems remains, as it may be difficult for European countries to maintain the necessary inventories of natural gas next winter. And then, there are questions about China’s growth.5

The US economy may still suffer some stiff headwinds over the next year. But at least they won’t be created by our own government.

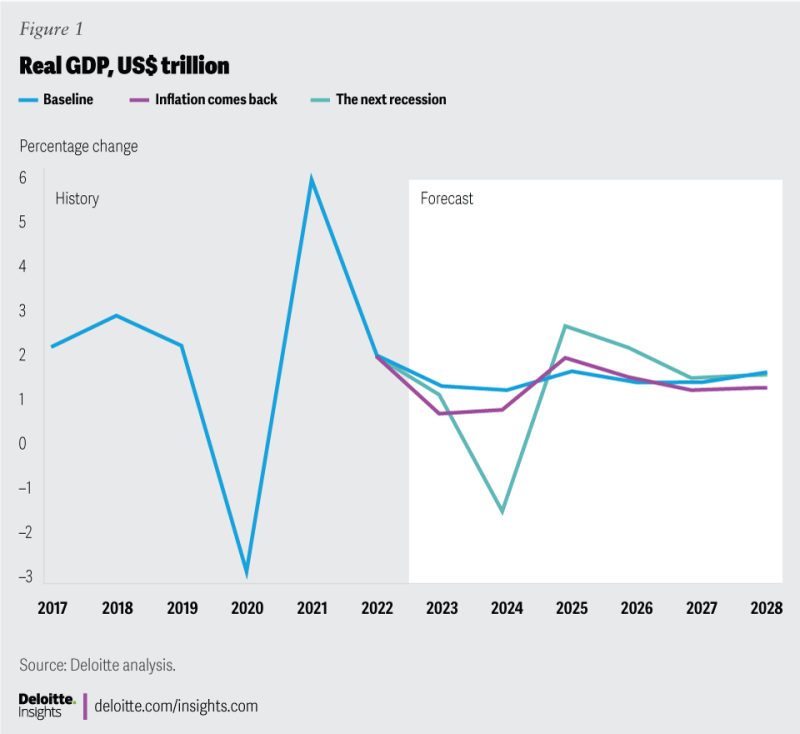

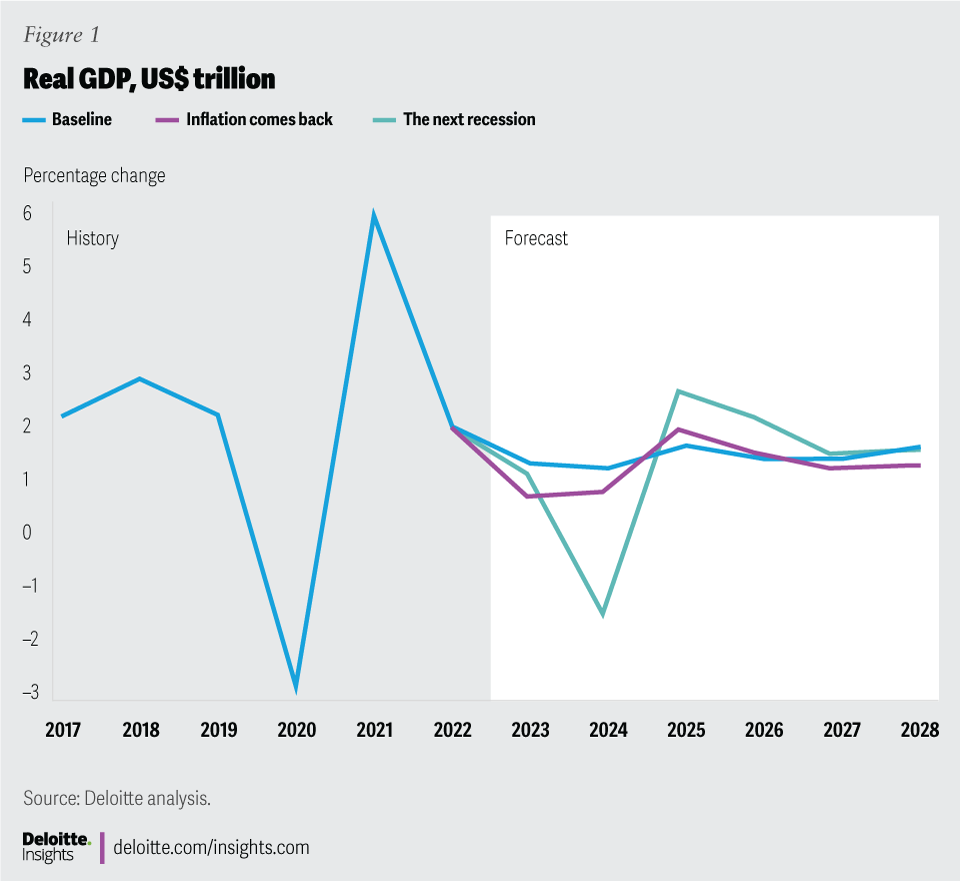

Baseline (60%): Economic growth slows to a crawl in 2023, but never really declines enough to merit the label of recession. Tighter monetary policy, slow growth in Europe and China, higher energy prices, and an expensive dollar are significant headwinds for the economy. However, households continue to increase spending on pent-up demand for services such as entertainment and travel. Business investment continues to grow, particularly in information-processing equipment and software. Investment in nonresidential structures remains weak, however, as the oversupply of office buildings and retail space weighs on the market. And the housing market slump really is a recession for that sector. Inflation settles back to the 2% range by late 2023 as demand for goods slows and remaining supply chain issues are resolved.

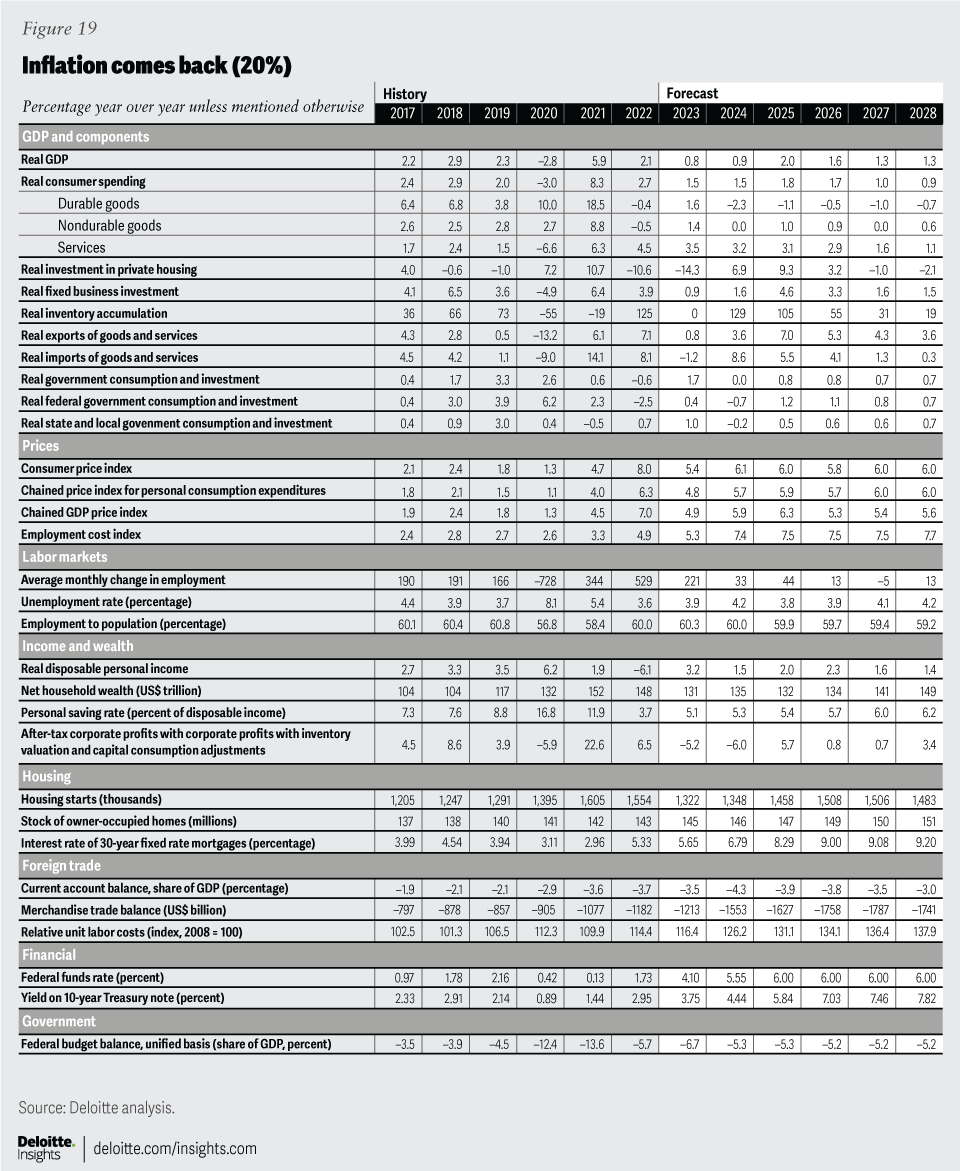

Inflation comes back (20%): The decline in inflation due to slackening supply chain pressures proves to be temporary. Continued strength in the labor market pushes wages up, leading to higher costs and prices. The Fed, having attempted to slow inflation through shock therapy in 2022, proves reluctant or unable to slow the hot labor market enough to matter, and inflation settles in at about 6%. Nominal interest rates reach levels that would have been punishing just a few years ago, but economic activity remains relatively strong.

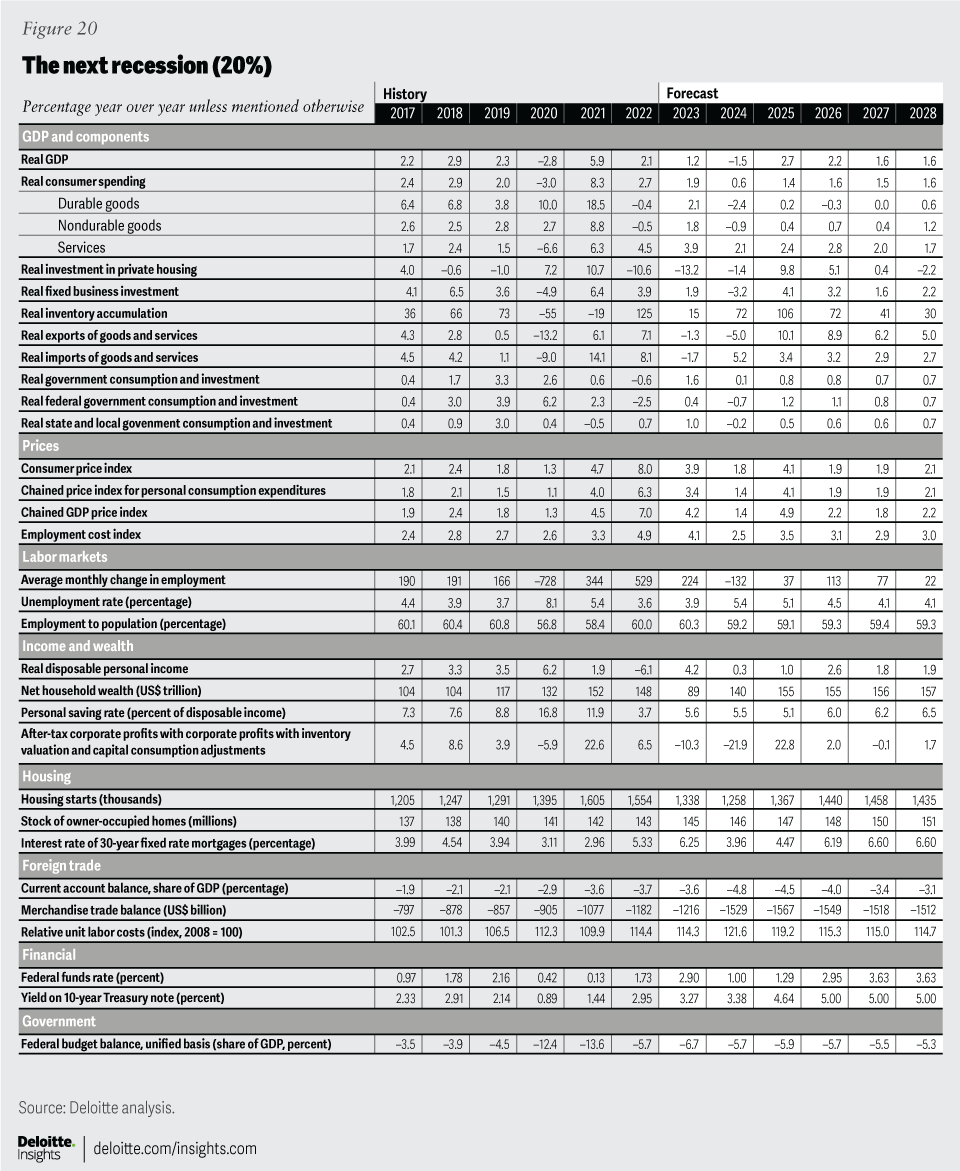

The next recession (20%): The Fed’s focus on inflation leads it to minimize risks to the economy until it’s too late. Although the financial shock is smaller than in 2008, the already-weak economy contracts a substantial 2.4% by the middle of 2024. The unemployment rate rises to 5.5%, which alleviates some—but not all—of the pressure on the job market. The Fed eases monetary policy and the economy starts growing by the second half of 2024.

The near-term outlook for consumer spending turns on two big questions:

1. What will happen when consumers finish running down their pandemic savings?

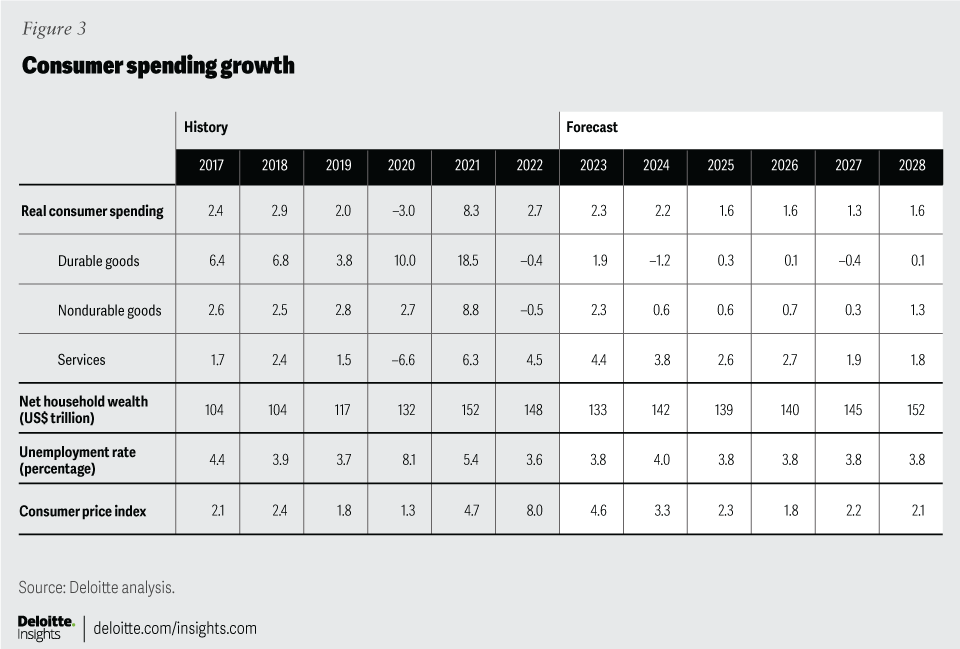

In 2020, during the height of the pandemic, we estimated that households saved about US$1.6 trillion more than we forecasted before the pandemic. Most of that money has been spent, as the savings rate has dropped from an average of around 9% before the pandemic to around 3% in the final quarter of 2022. Many households still have more cash on hand now than they normally would want, but how much of that will they spend as the economy slows? One possibility is that many consumers will remain cautious and hold on to those savings even as they are able to go out and spend. Another possibility is that spending booms for a while longer as postpandemic “revenge spending” on travel and consumer services continues to grow. The baseline Deloitte forecast assumes that continued job and income growth will support sustained growth in consumer spending, but spending will slow as the savings rate eventually rises back to the 6% range.

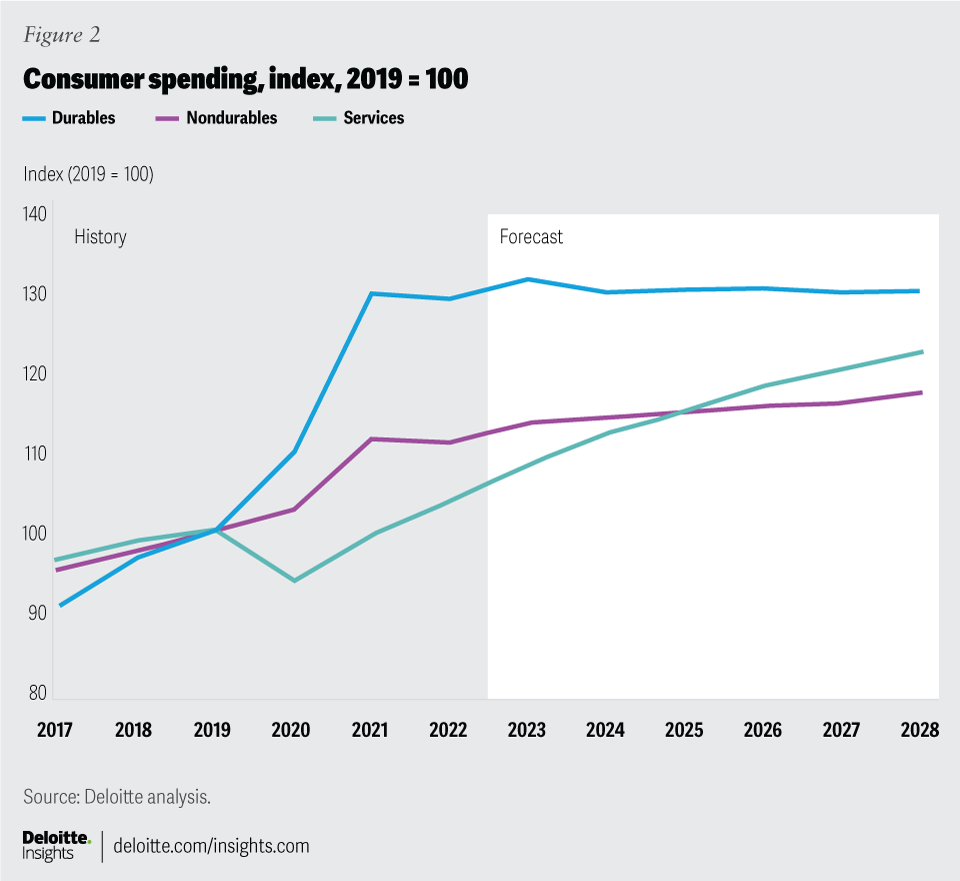

2. As consumer services recover, what happens to durable goods?

The pandemic sparked a remarkable change in consumer spending patterns. Spending on durable consumer goods jumped US$136 billion in 2020, while spending on services fell US$473 billion over the same period. Households substituted bicycles, gym equipment, and electronics for restaurants, entertainment, and travel. Once households can again purchase services, will they begin buying fewer goods? That may be happening, as by Q4 2022, durables spending was down 11% from the peak in Q2 2021. In Q1 2023, durable goods accounted for over 12% of total consumer spending, up from 10.5% in 2019. If consumers just return to their prepandemic spending patterns, durable consumer goods sellers will be looking at a 20% fall in spending. And consumers could conceivably spend even less since the durable goods they previously bought aren’t going to wear out that quickly.

Deloitte’s forecast assumes that consumer spending grows more slowly than income over the forecast horizon as households return to previous savings patterns. Durable goods spending continues to fall over the next few years as consumer spending “renormalizes” and consumers resume spending on services.

There is a silver lining for some households in the tight labor-market/high-inflation environment of the past couple of years. Low-wage workers have actually seen real wages go up, while high-income workers have experienced the greatest erosion of the value of their pay.6 It remains to be seen whether this reduction in inequality will continue, but it’s certainly welcome news to lower-wage workers. Retirement remains a significant concern for many workers: Even before the crisis, fewer than four in 10 nonretired adults described their retirement as on track, with a quarter of nonretired adults saying they had no retirement savings.7 As the population ages, many people are likely to find it difficult to afford the retirement they expect.8

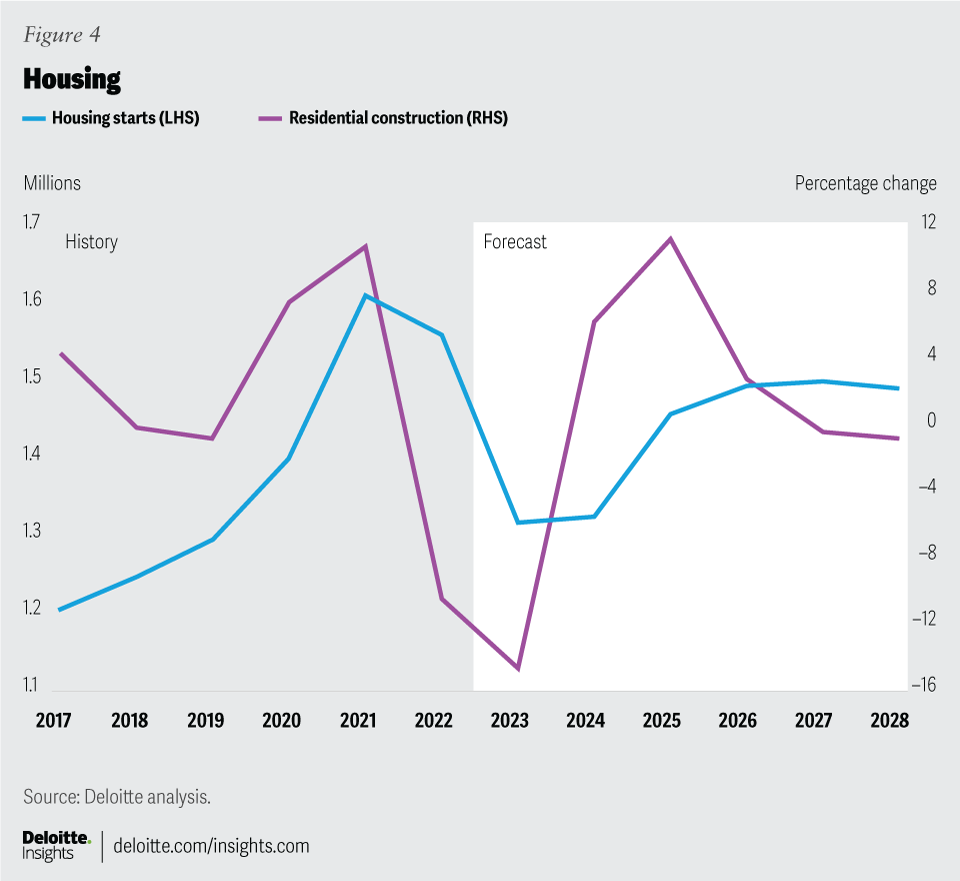

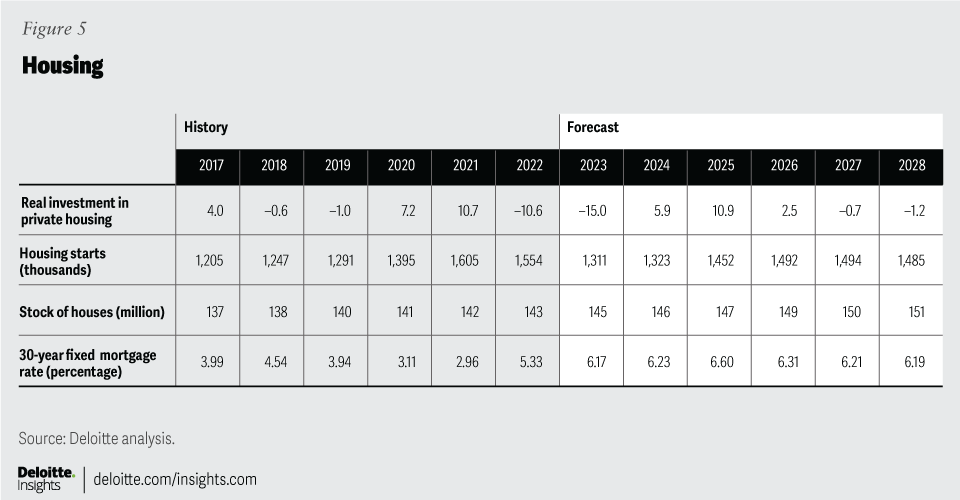

The housing sector outperformed the broader economy in the wake of the pandemic, as buyers and sellers found ways to navigate the pandemic’s restrictions. But then the tables turned. As the Fed raised interest rates and inflation appeared, long-term interest rates moved up dramatically. The result was a decline in housing starting from 1.7 million (at an annual rate) in Q1 2022 to 1.4 million Q1 2023. And house prices, which rose sharply starting in the middle of 2021, have stabilized and even started to fall in some places. Lower house prices will not be able to solve the affordability problem, however, because of the jump in mortgage rates.

Deloitte expects the fall in construction to continue through the end of this year. Housing construction is then forecast to bounce back, but only modestly; by 2025, housing starts reach our estimated equilibrium of about 1.5 million units per year.

Demographics suggest that housing is not likely to become a key driver of economic growth in the foreseeable future. Population growth appears to have slowed to less than 0.5% per year (compared to over 1% during the housing boom in the 2000s). The baseline forecast assumes that, after the recovery from the current housing downturn, housing starts will eventually begin to fall. Faster medium-term growth in housing would require faster population growth, most likely from immigration. Otherwise, the heightened demand for housing during the pandemic is likely to be a short-term phenomenon.9

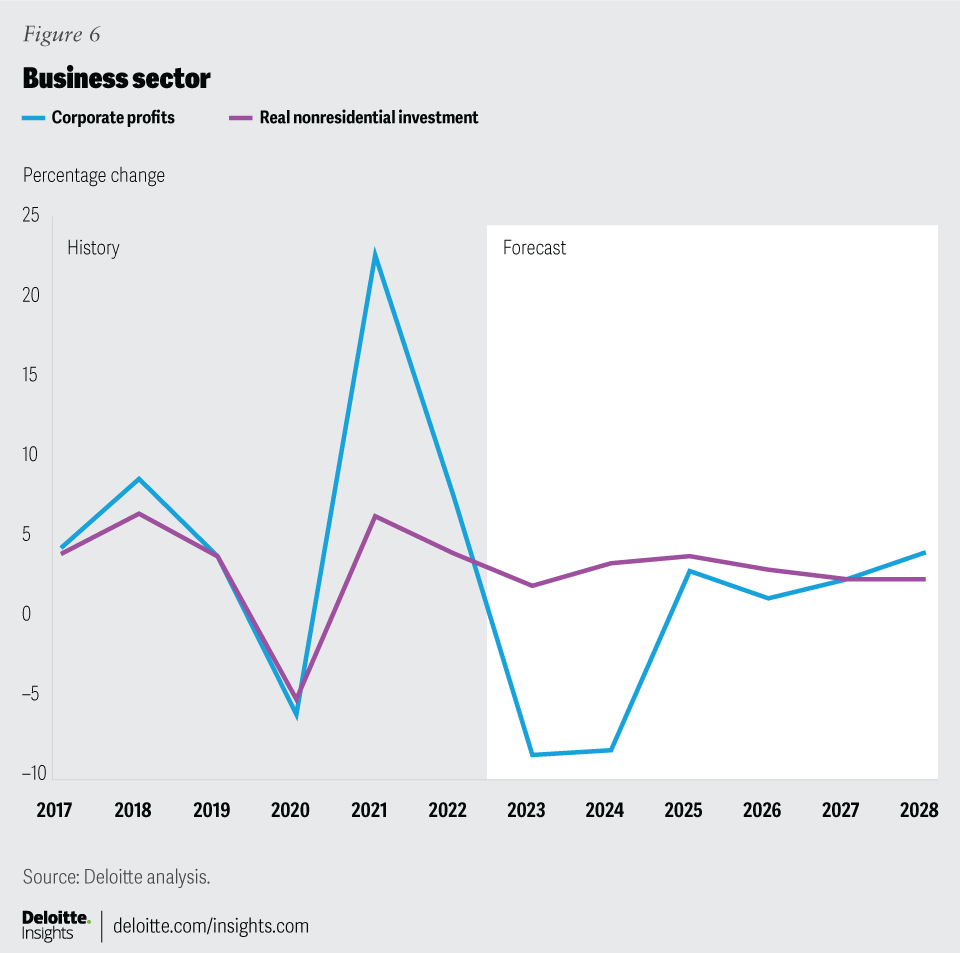

Businesses have ramped up investment since the initial impact of the pandemic, but they have been selective about what they are investing in.

Investment in nonresidential structures grew in Q1 2022 for the second straight quarter, but it’s still down more than 20% from just before the pandemic and prospects in many nonresidential building sectors remain grim. The business case for office buildings and retail space has collapsed, with online shopping and the shift toward working at home. Current talk of converting office buildings to residential spaces suggests that real estate experts don’t see a lot of room for growth in office demand.

Mining structures also took a big hit because of the decline in oil prices during the pandemic. As mining structures are dominated by energy mining, it would be reasonable to expect a ramp-up in response to historically high energy prices. But the response was delayed, for two reasons. First, many investors in this sector have been whipsawed in the past 10 years as prices dropped from over US$100 in 2013 to below US$50 in 2015, and then back up to over US$100 in 2021. Those investors are now less likely to react to what might be a temporary price increase. Second, the long-term prospect for fossil fuel investments looks weak, as consensus develops about fighting climate change.

The one positive development for nonresidential structures is the ramping up of government spending inherent in the Inflation Reduction Act. That act has provisions for a significant level of investment in alternative energy sources and other climate change remediation activities, which should take up some of the slack in construction capacity.

Investment in equipment was growing at a fast rate but fell in the last two quarters. Equipment investment has been dominated by transportation equipment and information technology (IT) equipment. Remote work makes IT equipment (and software) a substitute for buildings, and so the counterpart to weak investment in commercial structures is a lot of investment in IT. That need was particularly strong as companies moved to more virtual work over the past few years. But now that the initial investments have been made, demand may dampen a bit over the next few years. And transportation equipment was pushed up by the need for delivery vehicles for virtual commerce, since eventually products have to be delivered to consumers. This may stay strong, although it is very sensitive to the preferences of consumers for different types of shopping. If consumers prefer to return to brick-and-mortar shopping, business demand for light vehicles could weaken.

Investment in intellectual property (which consists primarily of software and R&D) accelerated during the pandemic. That’s mostly because of investment in software, and it likely reflects in the investments needed for teleworking. We expect this category to remain strong over the next few years as businesses continue to require software to accompany their investments in information-processing equipment.

Financing investment is becoming a bit pricier as long-term interest rates rise. However, nonfinancial businesses are sitting on a pile of cash, and interest rates are still relatively moderate. In our baseline forecast, the AAA corporate bond rate rises just under 6% and stays there through the end of the forecast horizon. Although that may appear high, historically it is low. In fact, the cost of capital is likely to remain low enough to boost businesses’ ability to pay for all those new computers and servers, not to mention the software to run them. But even with easy financing terms, office and retail space will likely be unable to generate sufficient returns to entice businesses to increase capacity.

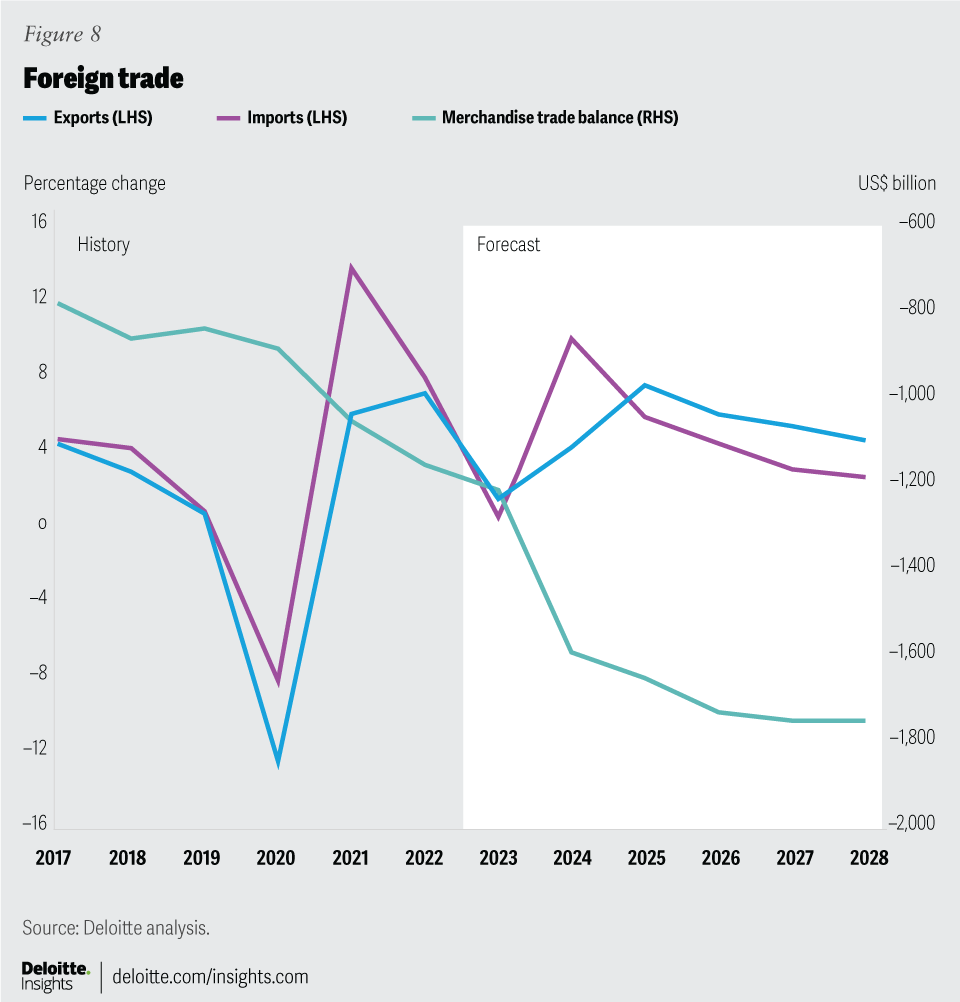

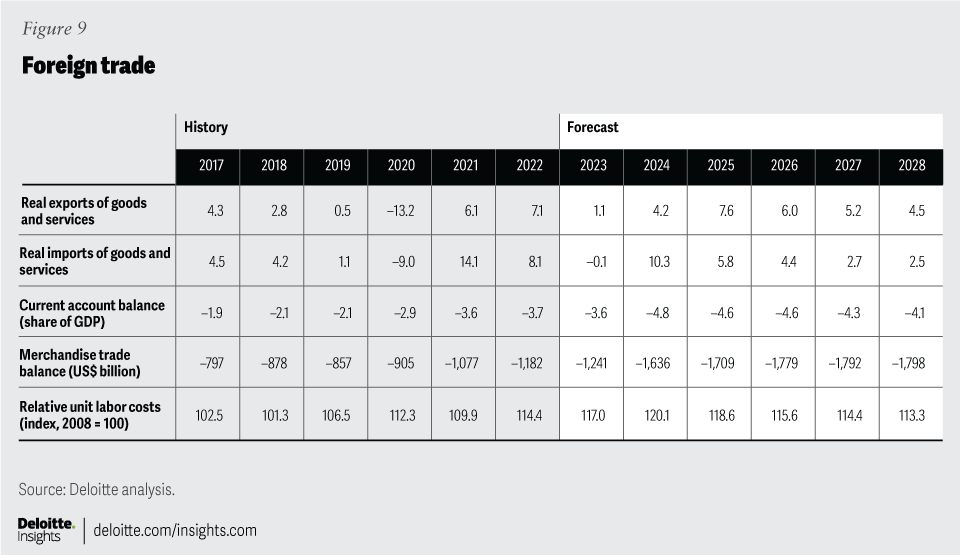

The Russian invasion of Ukraine continues to produce headwinds for US exporters. Lower demand from Europe (market for 15% of US exports) and a higher dollar because of greater global risk created some short-term challenges. Yet, net exports have been a positive contributor to GDP in the last four quarters. Real exports have grown 8.5% over the past four quarters. Petroleum products are part of the story, as US energy producers have helped to fill Europe’s need for energy to replace Russian sources. But exports of automobiles and related products, consumer goods, and capital goods have all grown surprisingly fast over the past year. That’s an even more impressive showing considering the strength of the dollar and weakness in the global economy this year. Our forecast shows US exports growing quickly over the five year horizon as the dollar falls (due to a reduction in global risk) and growth picks up abroad.

Real imports, in contrast, have fallen in the past year. That’s not due to petroleum imports; it’s a reflection of lower demand for durable goods of all types (except automobiles). Real imports of consumer goods, in particular, have fallen some 13% over the past year. Although this trend is unlikely to continue, we expect the dollar to gradually depreciate, and consumer spending to remain relatively slow, which will restrain import growth going forward.

There is a lot of talk about “deglobalization,” meaning a reversal of the dramatic increase in international trade that occurred in the past few decades. Global exports grew from 13% of global GDP in 1970 to 34% in 2012, and have stabilized at that level. More recently, the pattern of trade has changed. US imports from China have fallen, and US imports from other Asian countries are growing. This suggests that, while trade patterns may be changing, the United States remains as fully connected to the rest of the world as it has been.10 In 2022, exports accounted for 8.6% of GDP, above the 8.2% average in the five years before the pandemic. The Deloitte forecast projects that both exports imports will grow faster than overall US GDP growth over the five-year horizon. Supply chains will remain global, but business are likely to attempt to reduce their dependence on a single country or supplier, buying insurance against disruptions like COVID-19.

Reengineering supply chains will inevitably mean a rise in overall costs. Just as the “China price” held inflation in check for years, an attempt to make supply chains more robust (by, for example, finding suppliers in more than once country) might create inflationary pressures in the later years of our forecast horizon. And if markets won’t accept inflation, companies may to have to accept lower profits to diversify supply chains. Globalization offered a comparatively painless way to improve many people’s standard of living. The new approach will involve some painful cost increases and may limit income growth in the next five to 10 years.

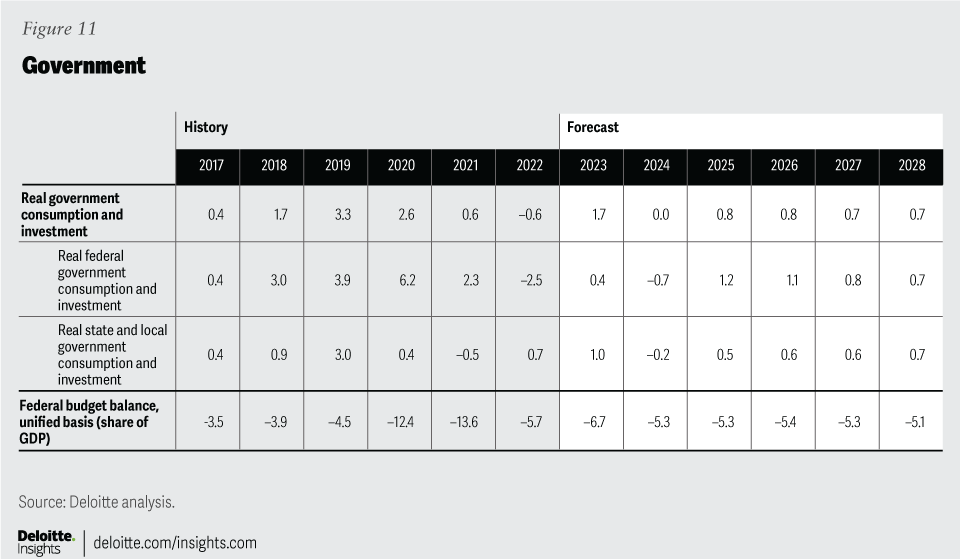

The budget deal between President Biden and Speaker McCarthy takes a lot of near-term risk off the table. It’s not just raising the debt ceiling, although that was important. The agreement on the overall size of the budget should allow the Federal government to avoid shutting down over the next two years. Without the agreement, a divided government in Washington might have led to a failure to pass the appropriations bills necessary to fund the government. This now seems unlikely for the next two years. Unfortunately, the problem will arise once again, probably not long after the 2024 election.

Although the Congressional Budget Office (CBO) officially “scored” the reduction in the deficit to be about US$1.5 trillion over the next 10 years, that relies on the assumption that the spending caps remain in place for the entire period.11 This appears unlikely. In any event, the reduction amounts to about 1% of the CBO’s forecast for outlays in 2024 and about 1.5% of outlays in 2025. These relatively small budget changes are unlikely to have much impact on the overall economy.

Looking beyond the immediate problems of finance, the earlier Infrastructure and Jobs Act and Inflation Reduction Act will boost government spending over the next 10 years. This spending will increase the capacity of the economy, although it might not show up as faster productivity growth.12 However, much of this additional spending comes toward the end of our forecast horizon, and consequently, the short-term impact on the forecast is minor. And the total spending impulse will be moderated by higher inflation. Also, the amount of spending is relatively modest compared to the economy as a whole. According to the CBO, in 2026, the peak year of spending, the Infrastructure and Jobs Act will add about US$61 billion to the federal deficit.13 That amounts to about 0.2% of projected GDP. These initiatives are likely to have a positive and significant impact on public capital in the United States, but they are not a large fiscal stimulus by any means.

Our baseline forecast assumes deficits will rise to US$1.7 trillion by FY28. That’s a hefty amount, one that inevitably raises the question of whether the US government can continue to borrow at such a pace. The answer is that it can—at least until investors lose confidence. At this point, most investors show no sign of concern about the ability of the United States Treasury to repay US debt.

The US government will face a crisis if it does not eventually find ways to reduce the deficit and consequent borrowing. The crisis may be many years away, and current conditions may argue for waiting. It would, however, be a bad idea to wait too long once those conditions lift.

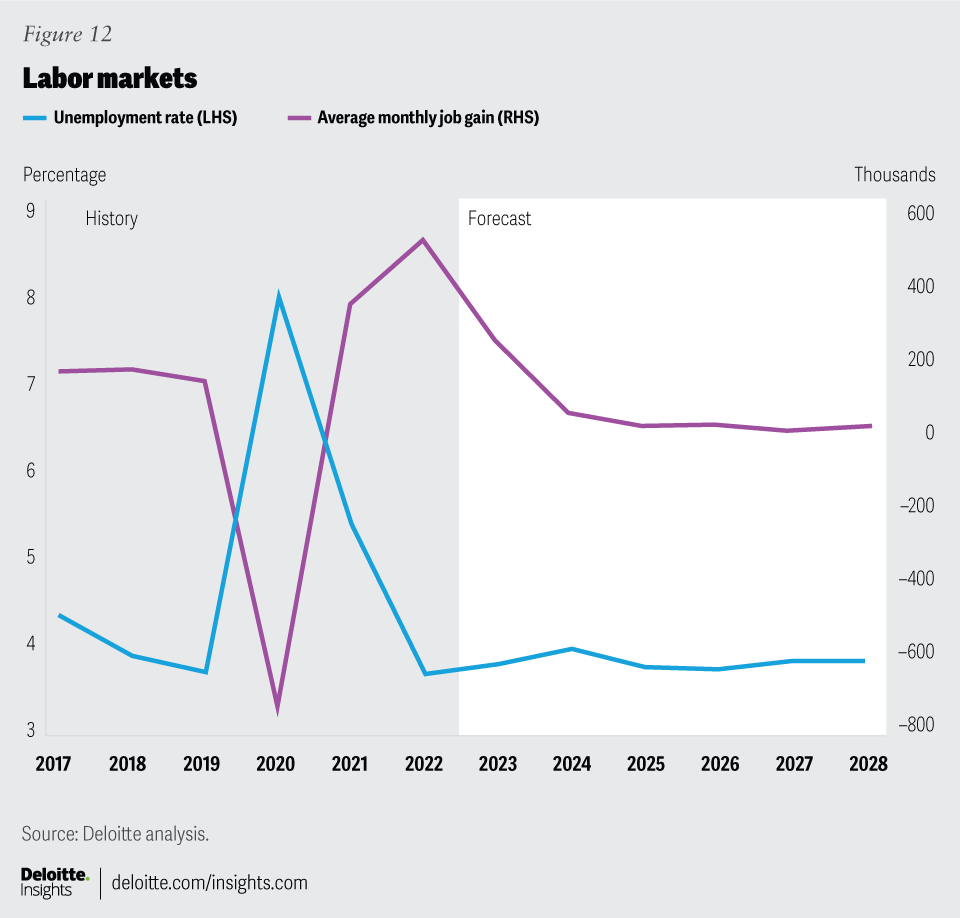

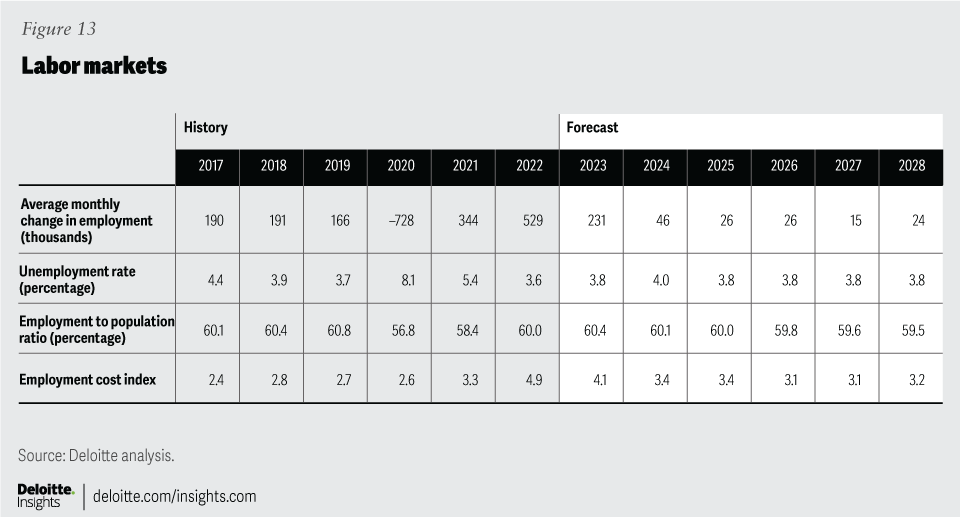

First, employment fell by over 20 million, and the main question was how difficult it would be to get all those workers back on the job. Then employment recovered quickly, and business commentary was full of talk about labor shortages and stories about employers struggling to find workers. Now, the labor market is slowing—but is still very hot. It’s hard to argue that the economy is experiencing a recession when the unemployment rate remains low, job growth is strong, and the ratio of job openings to unemployed people remains far above normal levels. The labor market has remained surprisingly strong, even as indicators of demand and production weakened. The three-month average rate of job growth was 283,000 in May, substantially above the 50,000 jobs that we estimate would meet the long-run growth of the labor force.

While employment has fully recovered from the pandemic, total labor force participation has not. However, the labor force participation rate for people under the age of 65 hit the prepandemic level in April. Most of the workers who left the labor force are older Americans. Many of these people have probably retired, in the sense of expecting to remain permanently out of the labor force, but some can likely be enticed back with the right compensation packages and flexible working hours and conditions.

As is the case in many areas, the pandemic accelerated trends that were evident even before it started. Slow labor force growth and continued high demand had already created conditions that required companies to offer higher wages to lower-skilled workers and to be more imaginative about hiring. In the post–COVID-19 world, companies that make extra effort to find the workers they need and provide conditions to attract those workers will have an important competitive advantage.

Deloitte’s baseline forecast assumes that job growth slows to sustainable levels in the next few years. It’s important to remember that job growth is likely to slow simply because there aren’t enough workers. That means slowing employment growth—if the unemployment rate remains low—is not necessarily a signal of an economic downturn. In the forecast, the unemployment rate rises a bit as growth slows in 2023, but the job market remains relatively tight. Over the longer horizon, labor force growth slows to just 0.2% per year, presenting continuing challenges for employers. It’s a demographic fact that employers will have to learn to live with.

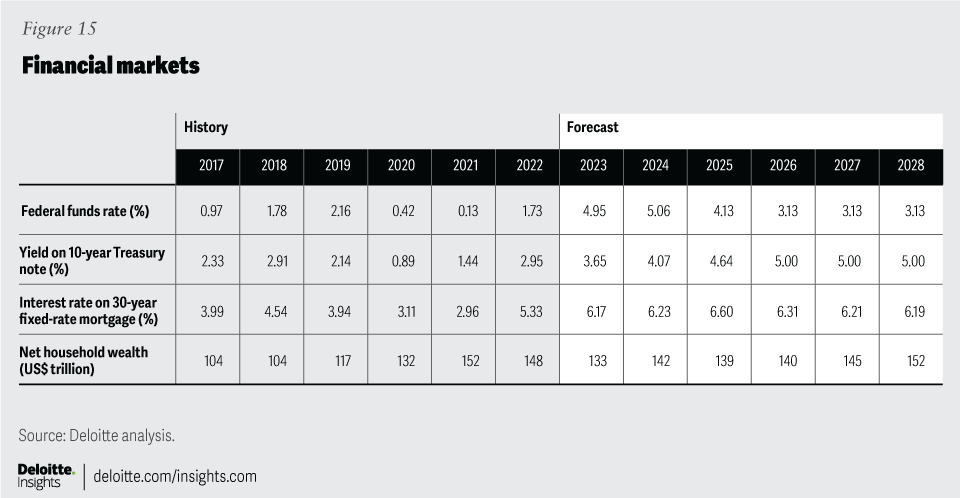

Have authorities successfully prevented rising interest rates from creating a financial crisis? The failure of three regional US banks and one large Swiss bank certainly got the attention of central banks, including the Fed and regulators including the Federal Deposit Insurance Corporation. So far, the economic impact looks to be modest. But the problems that showed up in March demonstrate that the economy is currently fragile, and that a financial disturbance could easily throw it into a recession. A failure by the US government to raise the debt ceiling could be such a disturbance, and that’s one of the reasons we currently estimate the probability of a recession to be significant.

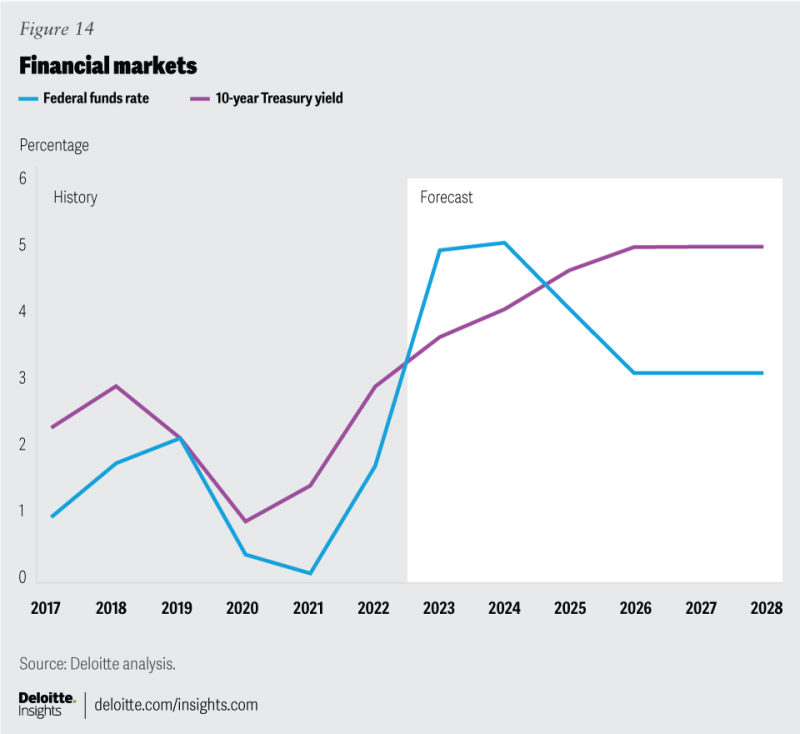

In the medium term, the key question is whether long-term interest rates will once again settle in at a relatively low level, or whether they will return to levels consistent with the experience before the global financial crisis. Those arguing that interest rates will return to low levels point to fundamentals such as demographics (the aging global population).14 Those arguing that interest rates will return to previous behavior point to the slowing of savings growth from China and the need for large investments (whether public or private) to reduce the impact of climate change.15 The Deloitte forecast assumes that long-term interest rates remain relatively high, as demand for capital remains strong while global savings grow more slowly over the coming years.

Our baseline forecast assumes that the Fed hiked the funds rate for the last time in May. Given our relatively optimistic forecast for GDP and employment, in the baseline, the Fed does not start lowering the funds rate until late 2024, and then gradually eases until it reaches 3.25%, which is our estimate of the long-term neutral rate. Demand for capital for investment (including significant government and private outlays on climate change) keeps the 10-year rate from falling, and it reaches its long-run value of around 5% by 2025. This is consistent with the historical relationship of these rates under moderate inflation: Should inflation continue to be high, the spread between the 10-year note and the Fed funds rate could continue to rise (as investors account for expected inflation in the later years of the note’s period). Investors should watch out for the possibility of higher interest rates—although by the standards of the 1970s and 1980s, these rates are still quite low.

Of course, interest rates are always the least certain part of any forecast: Any significant news could—and will—alter interest rates significantly.

Rising interest rates create a problem for anybody with a portfolio of fixed-income securities. The market value of a fixed-income security varies inversely with the market interest rate, and so a portfolio of fixed-income securities would lose value. The Fed’s aggressive interest-rate hikes over the past year pushed the yield on the 10-year Treasury note up to almost 4%. That would reduce the market value of a 10-year note issued at 2% by almost half. And yet, 2% is the average auction rate (the rate at initial purchase) in 2021 and 2022. That means that 10-year notes purchased would fetch just close to half of what they cost originally.

That such “latent” losses existed was no secret. The question was when and how they would show up.16 And they did show up in March, when it turned out that some large regional banks had stuffed their portfolios with such bonds, without marking them to market as their values fell. Eventually, large depositors become concerned, and a modern bank run began. Nobody had to stand in line to get their cash; instead, electronic withdrawals drained these banks’ liquid reserves until they had to be closed and, eventually, sold or closed down.

The Federal Reserve reacted quickly to try to reassure depositors in other banks that these issues were isolated, and that there was no need to be concerned about the safety of deposits. And, in fact, the Fed’s efforts appear to have worked. But there will be some modest damage to the economy.17 As of late May 2023, deposits at small banks had stabilized (resuming the slow but controllable declining trend before March), indicating that depositors were satisfied with the safety of their deposits. Bank lending remains under the microscope because a pullback in lending could have a significant impact on economic activity.

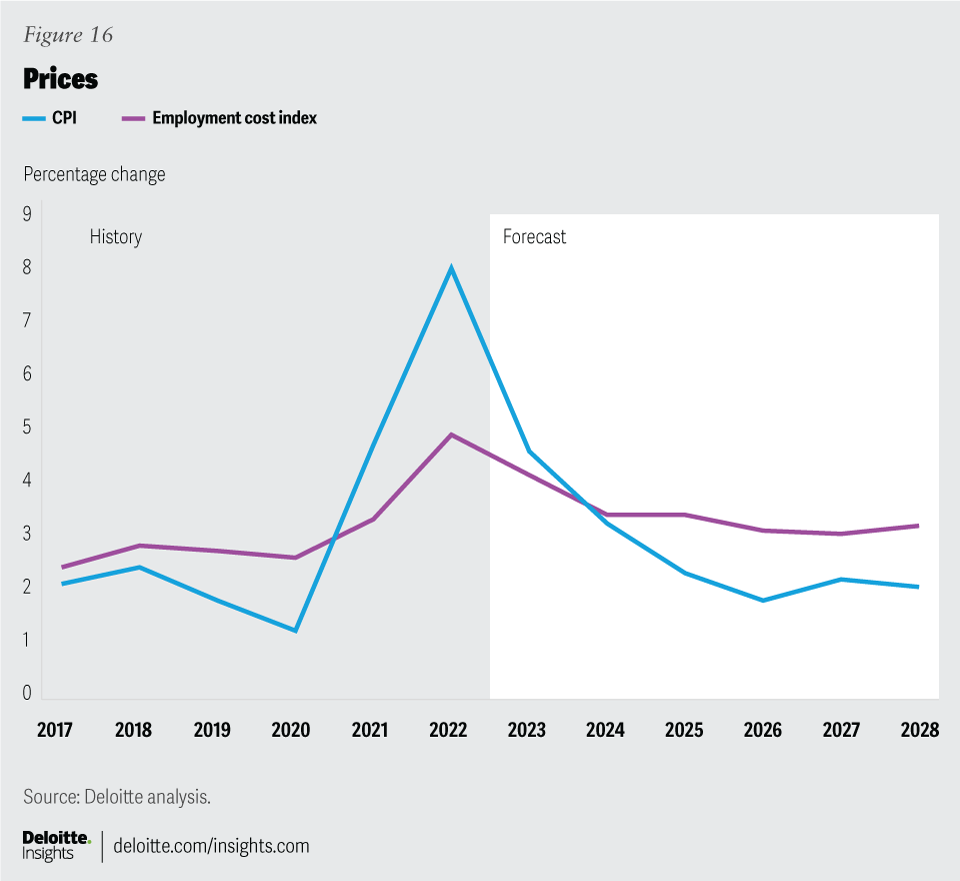

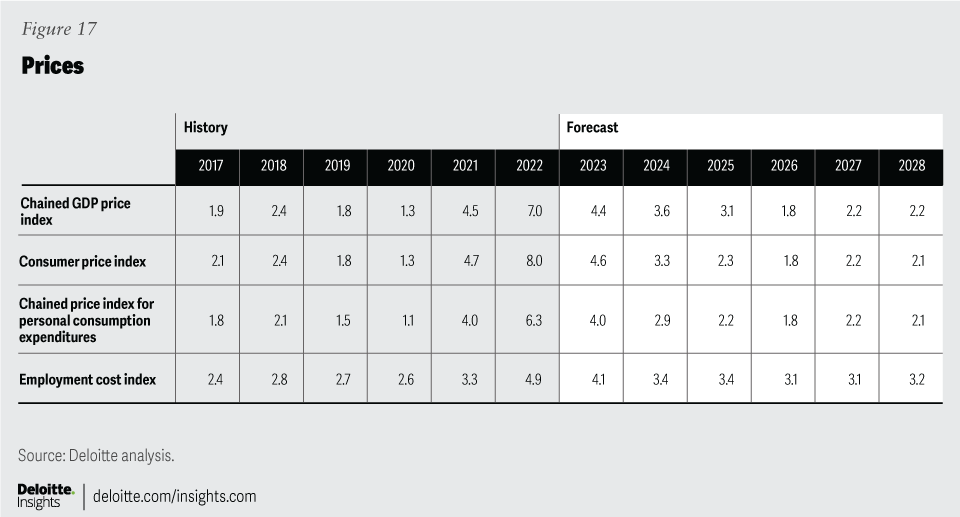

Inflation remains stubbornly high, although it’s come down quite a bit over the past year. The year-over-year inflation rates often cited in the press don’t capture this very well because the period they cover is too long, and monthly inflation rates are too volatile. But the three-month inflation rates show a decline from the rates of 8%–9% registered in late 2021 and the first half of 2022 to about 4% over the last six months. However, core inflation tells a different story; food and energy prices contributed to the earlier high inflation, and falling energy prices, in particular, are now contributing to the decline in the all-items consumer price index (CPI) inflation. Core inflation remains at about 5% (annualized) when measured over the past three months and has even accelerated a bit.

Two characteristics of the current inflation provide some room for optimism. First, shelter remains an important contributor to overall inflation, but that’s likely to reverse as the decline in rental costs shows up in the CPI.18 Second, outside of shelter, CPI growth tends be dominated by a different product or service each month. This looks very different from systemic inflation, when prices of all products and services tend to rise together. This, along with the prospect of a slowdown that is likely to reduce demand pressures, should help to put a lid back on price inflation.

The Deloitte forecast continues to assume that the current inflation is “transitory” in the sense that it will dissipate over time. Our baseline forecast shows CPI inflation falling to below 3% by late 2024. We remain optimistic that today’s households and businesses will avoid the unpleasant experiences of the long inflation and painful disinflation that their predecessors experienced during 1970–1985.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}