/primary/US164917_Banner.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

United States Economic Forecast has been saved

The author would like to thank Bhavna Tejwani for her contributions to this article.

Cover image by: Sofia Grace Sergi

Is a recession on the horizon? That’s been a key question for the US economy for the past six months. So far, it’s safe to say that the recession is mostly in people’s minds. Sentiment data has been very negative even as actual economic activity—as measured by job gains, industrial production, and retail sales—are still indicating growth.1 But the question about whether there might be a recession is not really the right question to ask. The Fed has hiked the funds rate by 300 basis points since March of this year, and 10-year bond yields are 4%, over twice the level at the beginning of the year. This suggests that economic activity will continue to slow over the next six months. The Deloitte forecast shows very slow growth in the first half of 2023—but not enough to rouse the NBER Business Cycle Dating Committee to declare a peak in economic activity (see “Defining recessions (and the danger of revisions)” below).

When the first estimate of GDP in the second quarter was negative, some commentators declared that the economy must be in a recession. After all, it was the second negative quarter in a row, and two negative quarters define a recession, right? Actually, this definition of recession has never been used in the United States. The idea was first proposed in 1974 by the then Commissioner of Labor Statistics, Julius Shiskin.2 But economists decided to approach the problem differently. The nonprofit National Bureau of Economic Research (NBER) maintains a committee of distinguished economists who determine business-cycle dating.3 They track a broad range of economic indicators and normally make determinations about turning points some time after a business cycle peaks (when the economy starts contracting) or troughs (when the economy begins expanding again).

Many business cycle economists believe that GDP is too narrow to define a downturn. Also, GDP is subject to considerably large revisions. In some cases, contemporary GDP showed a decline of two quarters in a row, but subsequent revisions have changed the picture. The NBER Committee’s definition of recession is based on a wider set of indicators, so data revisions are less important.

Of course, any definition of recession is arbitrary. The economy may avoid an “official” downturn even while some sectors may feel quite a bit of pain. It’s always good to remember the old saying: It’s a recession when your neighbor loses their job, and a depression when you lose your job.

There are plenty of reasons to expect a slowdown. The vulnerability of Europe to Russian energy sanctions, China’s housing market problems, and the impact on global food supplies because of continued war in Ukraine are all significant headwinds. But the US economy is not as exposed to these problems as many analysts assume. International trade is a modest share of the US economy, with much of the trade taking place within North America. And the substantial US energy and food sectors stand to gain from higher prices for commodities. (In the case of energy, global oil prices are already coming down.)

The real case for a recession in the United States involves the Federal Reserve’s actions to slow the economy. And there are a couple of reasons why the slowdown is not as likely—as some analysts claim—to turn into a full-fledged recession:

That’s why Deloitte’s Q4 US Economic Forecast does not include a recession in our baseline. The baseline shows very slow GDP growth, if only because of the impact on the housing market. But our assumption that inflation is likely to moderate suggests that the Fed will stop tightening at a level quite a bit below what’s necessary to create a recession solely from high interest rates.

Of course, interest-sensitive sectors will feel very differently. Housing, in particular, has already started to decline. In our forecast, the continued fall in residential construction activity helps to slow GDP growth in 2023, especially in the first half of the year.

There is old term—“growth recession”—that may describe what 2023 will feel like. The unemployment rate will rise slightly; job growth will moderate but won’t turn negative; and GDP growth will be below 1% in three quarters. Many parts of the economy will continue to grow, and employers will continue to face a relatively tight job market. That is likely to suggest to the NBER Business Cycle Dating Committee that the US economy never reached a peak in 2022 or 2023; continued growth means no recession. But the difference between that story and the story in which growth slows just a bit further, and the unemployment rate hits 4.5% or even 5% briefly, and the NBER Committee eventually declares a peak (perhaps in late 2023) is not much. Even forecasters who expect a recession don’t expect it to be very strong; the October Wall Street Journal survey of forecasters found an average 63% probability of a recession in 2023, but most forecasters expect the unemployment rate to remain below 5%. Such a mild recession would likely not derail the plans of many companies.

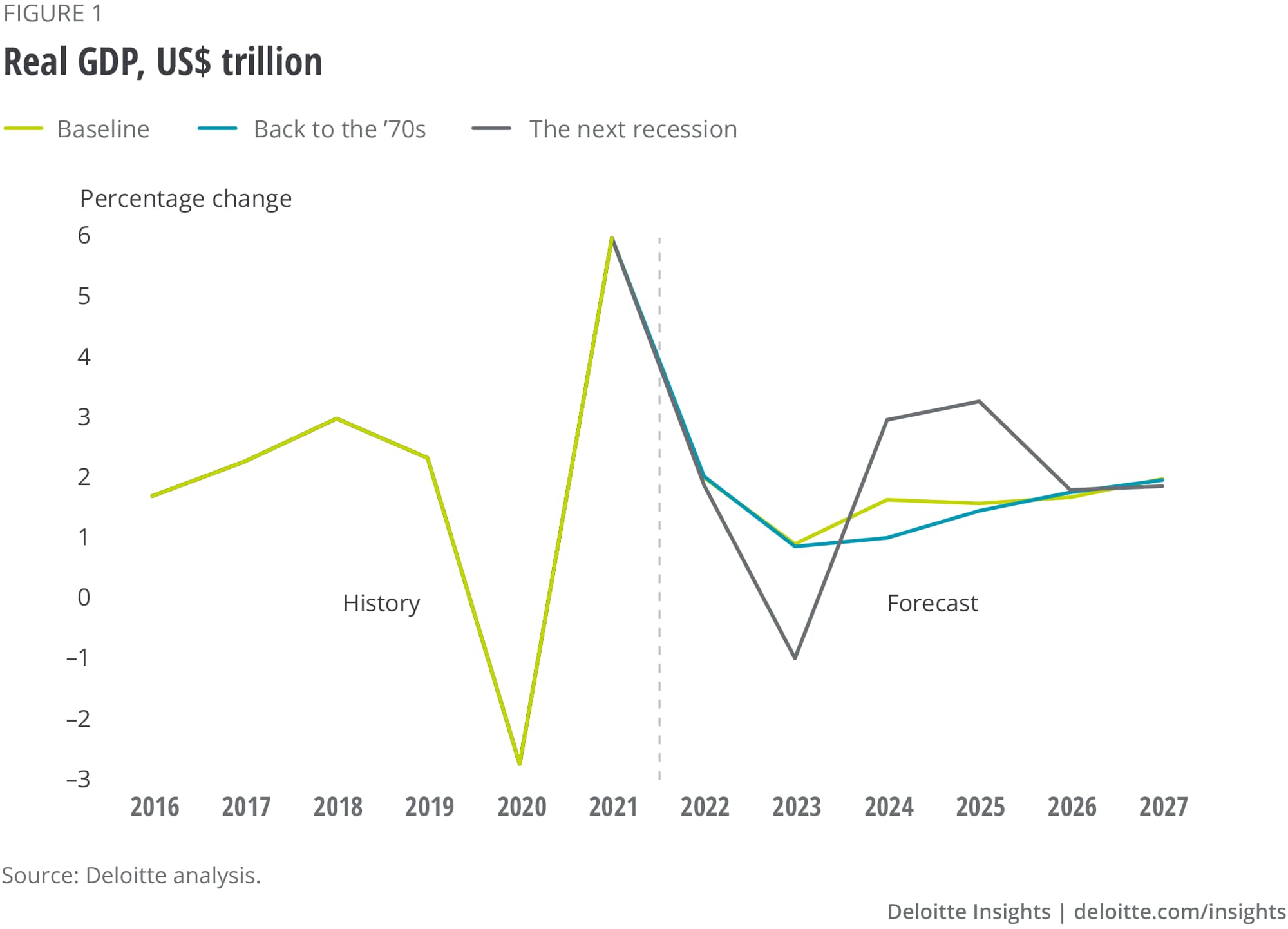

But … the chances of a real recession are significant. Against a background of geopolitical tensions, and a Fed that wishes to communicate its willingness to fight inflation, even a small financial shock could wreak havoc. As interest rates rise, investing institutions like insurance companies and pension funds may need to revalue assets—and not in a good way. A corporate bond or mortgage paying 3% loses a lot of value when equivalent returns on newer assets are 6%. Suppose a systemically important financial institution finds too many of these low interest rate assets on its balance sheet. The problem isn’t that the assets are unsound, it’s simply the need to mark to market that could cause the type of problems that would lead to a full-scale recession. In our “Next Recession” scenario, GDP falls significantly with a relatively high probability. We think that chances of such a recession are less than even. But businesses may wish to take action to guard against a potential hurricane even before one is sighted far off at sea.

Baseline (55%): Economic growth slows to a crawl in 2023, but never really declines enough to merit the label of recession. Tighter monetary policy, slow growth in Europe and China, higher energy prices, and an expensive dollar are significant headwinds for the economy. However, households continue to increase spending on pent-up demand for services such as entertainment and travel. Business investment continues to grow, particularly in information-processing equipment and software. Investment in nonresidential structures remains weak, however, as the oversupply of office buildings and retail space weighs on the market. And the housing market slump really is a recession for that sector. Inflation settles back to the 2% range by late 2023 as demand for goods slows and businesses solve their supply chain issues.

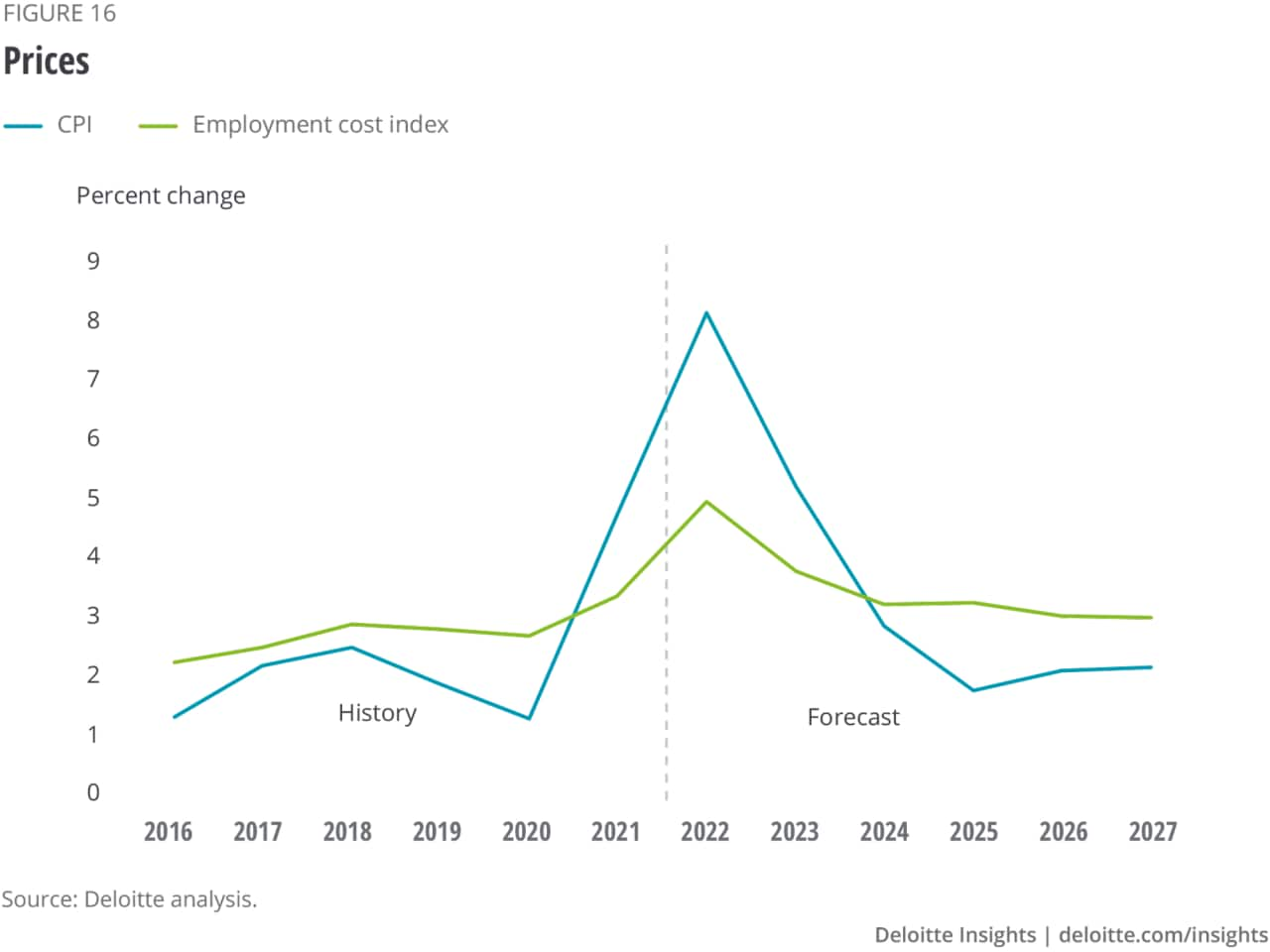

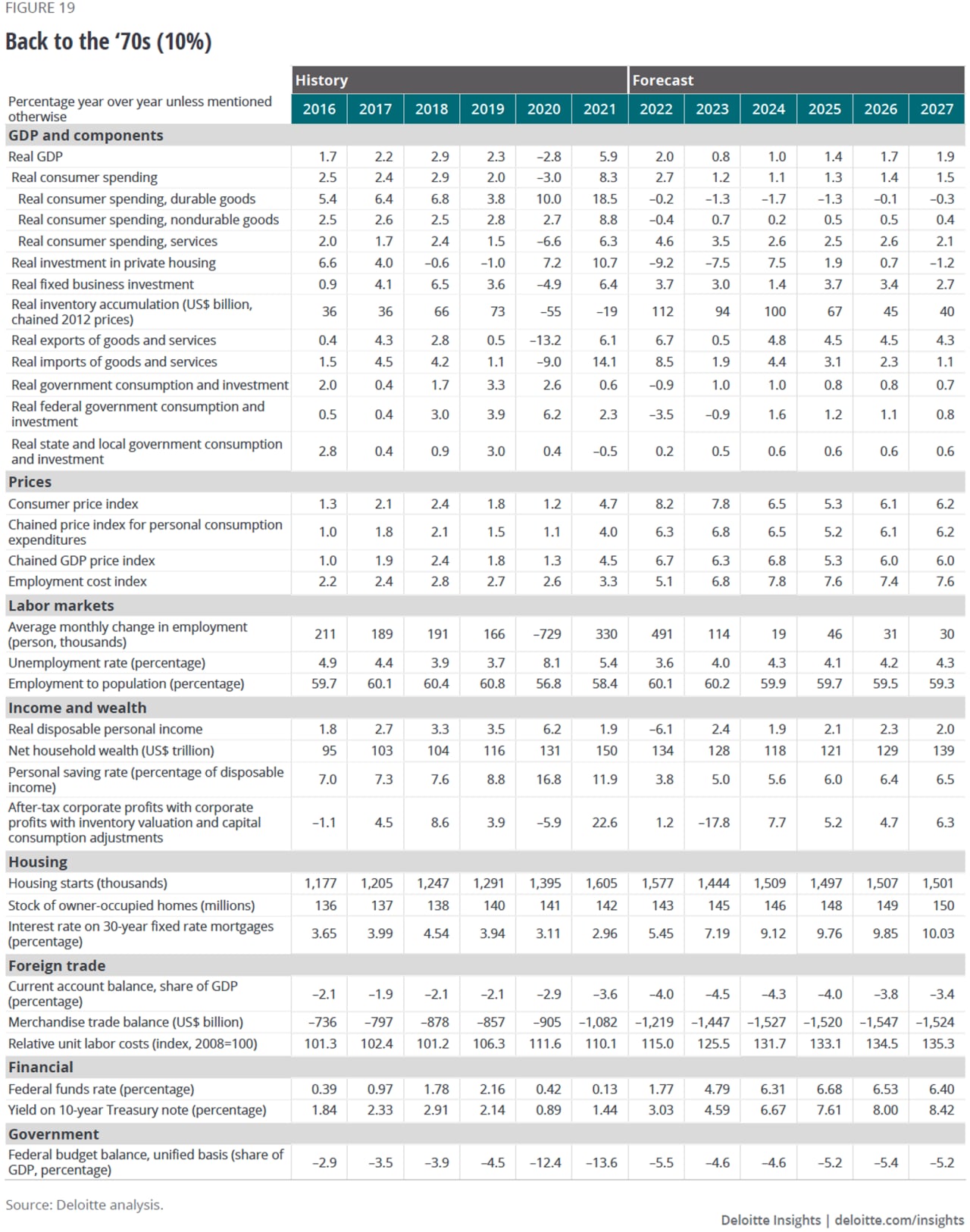

Back to the ’70s (10%): Households and businesses start to build anticipations of inflation into wage and pricing decisions. This reaction creates an inflationary spiral. The Fed is reluctant to engineer an actual recession and allows inflation to stabilize at a relatively high rate of 6%. However, tighter monetary policy slows the economy a bit, and the unemployment rate drifts upward.

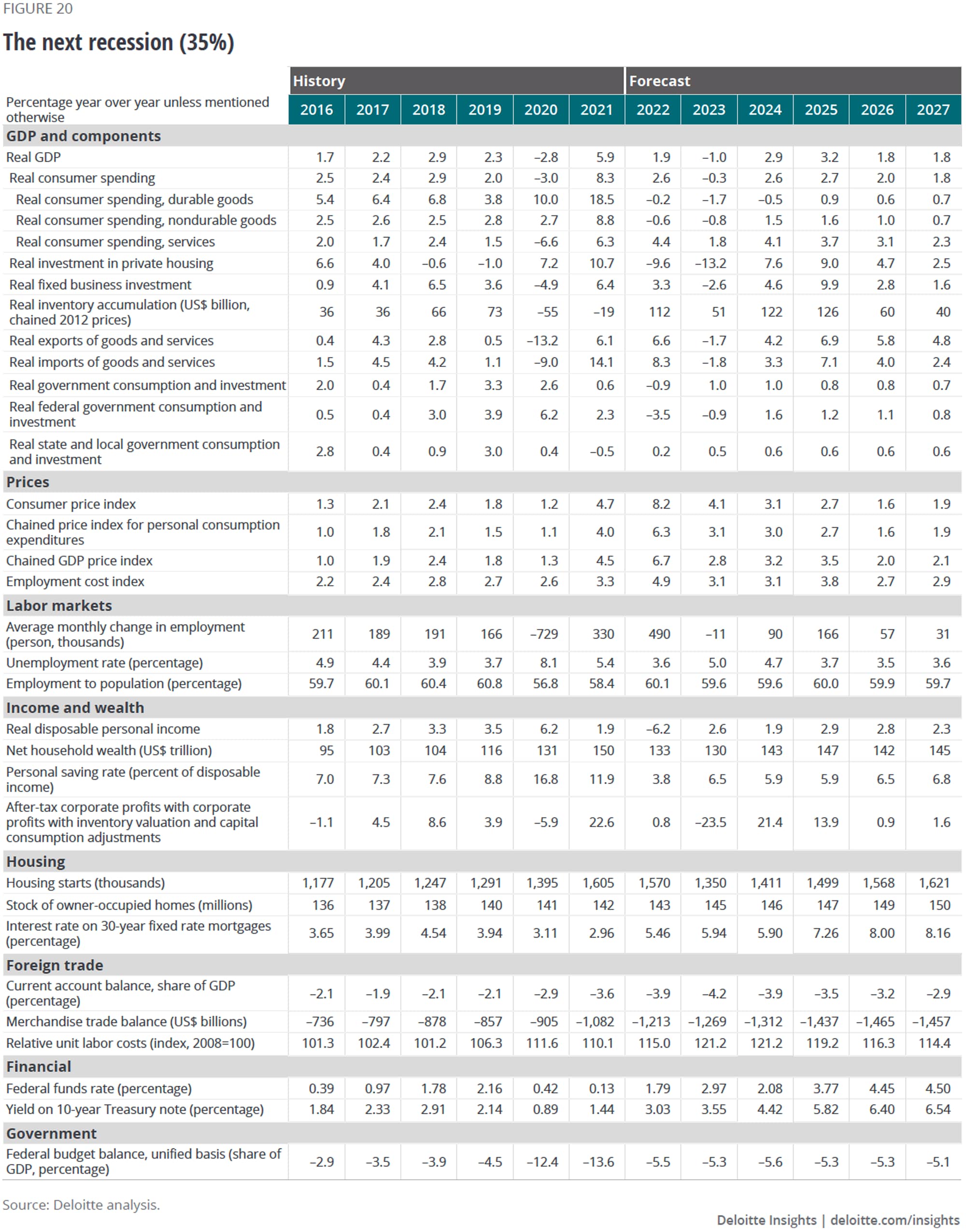

The next recession (35%): The Fed continues aggressive tightening as the economy slows. The fast rise in US interest rates eventually reveals significant problems for some systemic financial institutions. The Fed’s focus on inflation leads it to minimize the financial market issues until it’s too late. Although the financial shock is smaller than in 2008, the already weak economy contracts a substantial 2.0% by the end of 2023. The unemployment rate rises above 5%, which alleviates some—but not all—of the pressure on the job market. The economy bounces back in 2024.

The near-term outlook for consumer spending turns on two big questions:

1. When will consumers finish running down their pandemic savings?

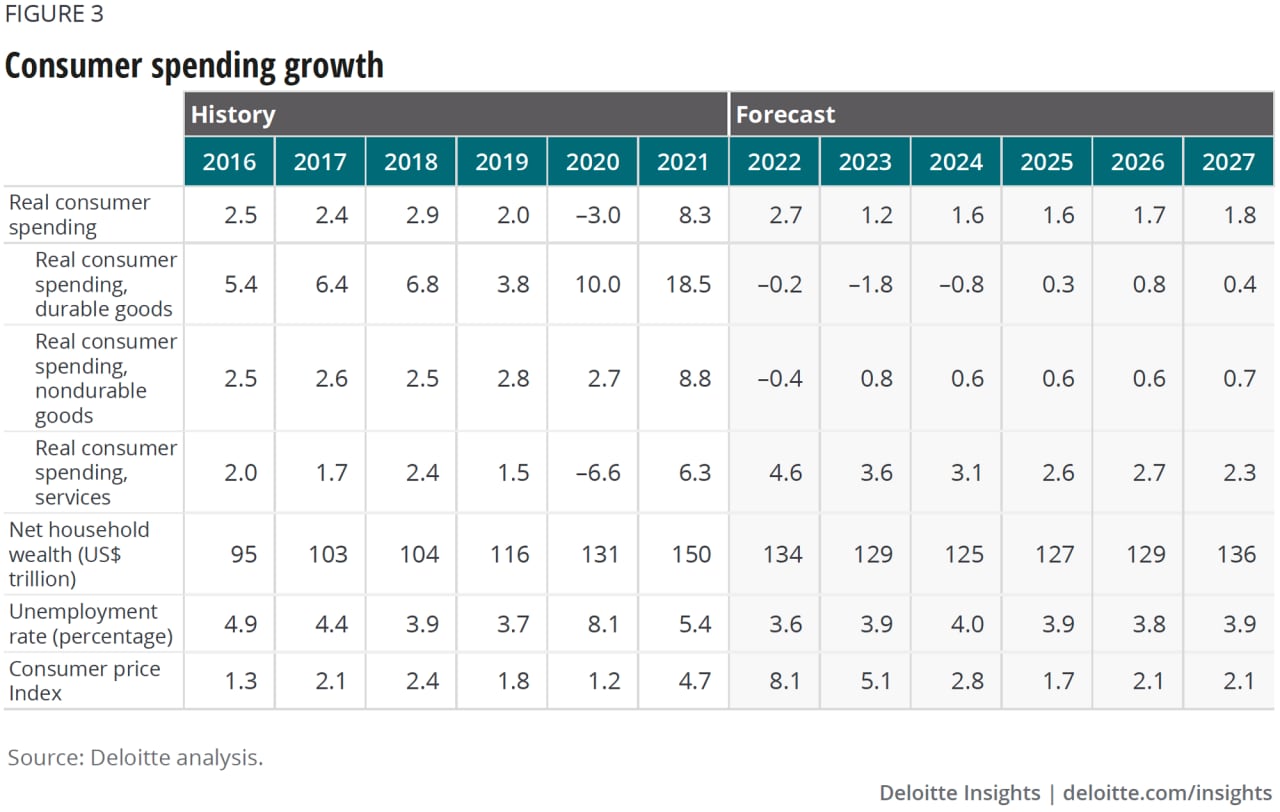

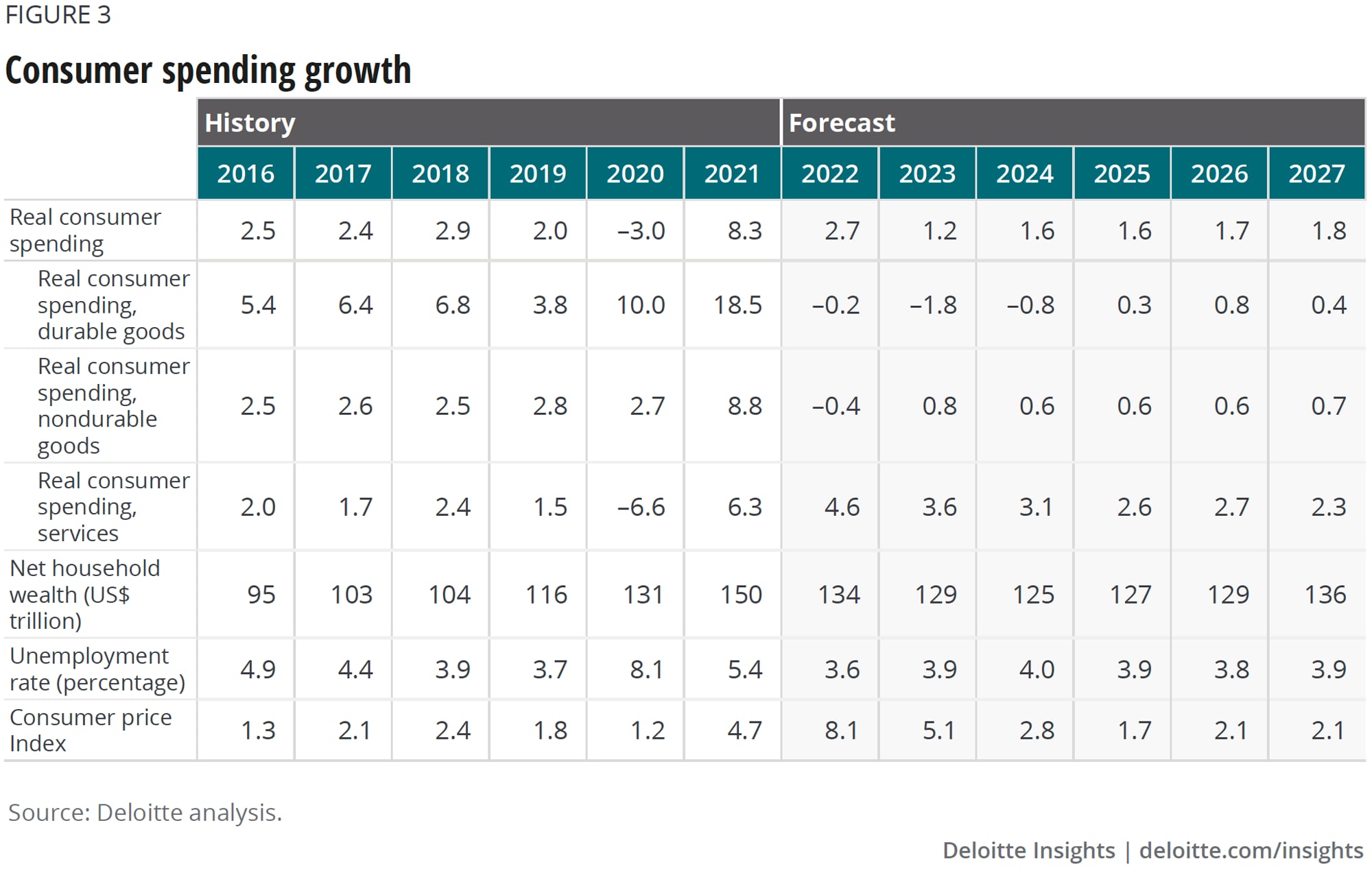

In 2020, during the height of the pandemic, we estimated that households saved about US$1.6 trillion more than we forecasted before the pandemic. Many households still have a lot more cash on hand now than they normally would want. How much of that will they spend as the pandemic impact wanes? One possibility is that many consumers will remain cautious and hold on to those savings even as they are able to go out and spend. Another possibility: Spending booms for a while longer as the impact of COVID-19 continues to wane. We’ve already started to see that happen, as the savings rate has fallen to about 5% (compared to 7% before the pandemic). The baseline Deloitte forecast assumes that the savings rate will eventually rise back to the 6% range, but that continued job and income growth will support continued growth in consumer spending. Spending could be even stronger if households decide to cash in more of those savings—and weaker if they decide to hold onto more of those pandemic savings.

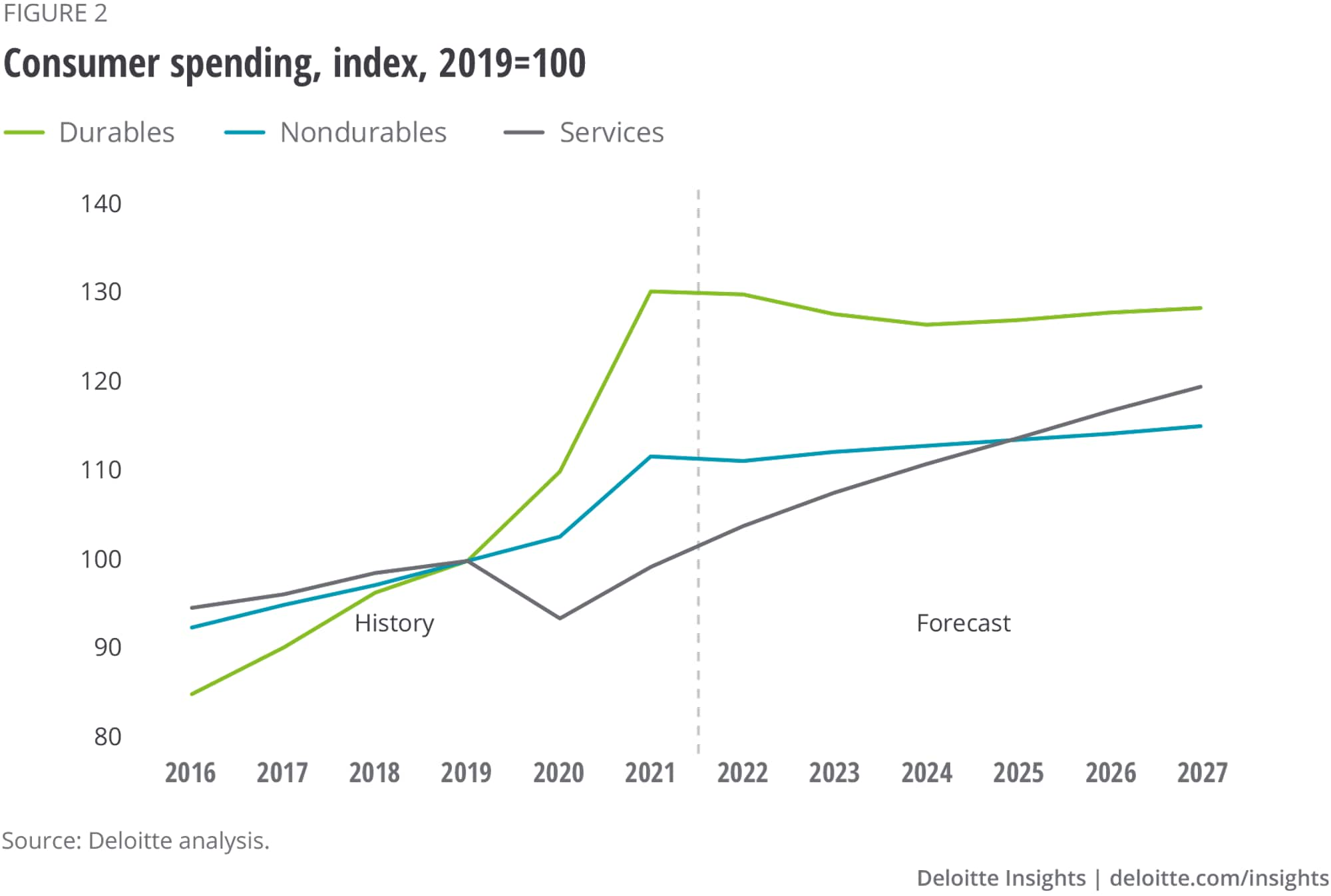

2. As consumer services recover, what happens to durable goods?

The pandemic sparked a remarkable change in consumer spending patterns. Spending on durable consumer goods jumped US$103 billion in 2020, while spending on services fell US$556 billion over the same period. Households substituted bicycles, gym equipment, and electronics for restaurants, entertainment, and travel. Once households can again purchase services, will they begin buying fewer goods? That may be happening, as, by Q2 2022, durables spending was down 6% from the peak in Q2 2021. In Q3 2022, durable goods accounted for 12.5% of total consumer spending, up from 10.5% in 2019. If consumers just return to their prepandemic spending patterns, durable consumer goods sellers will be looking at a 20% fall in spending. And consumers could conceivably spend even less, since the durable goods they previously bought aren’t going to wear out that quickly.

Deloitte’s forecast assumes that durable goods spending continues to fall over the next few years as consumer spending “renormalizes” and consumers resume spending on services.

In the longer term, we expect the pandemic to exacerbate some existing problems. It has thrown the problem of inequality into sharp relief, straining the budgets and living situations of millions of lower-income households. These are the very people who are less likely to have health insurance—especially after layoffs—and more likely to have health conditions that complicate recovery from infection. And retirement remains a significant issue: Even before the crisis, fewer than four in 10 nonretired adults described their retirement as on track, with a quarter of nonretired adults saying they had no retirement savings.5 The stock market boom will have little impact on most people’s balance sheets, leaving many people still unable to afford retirement as they age.6

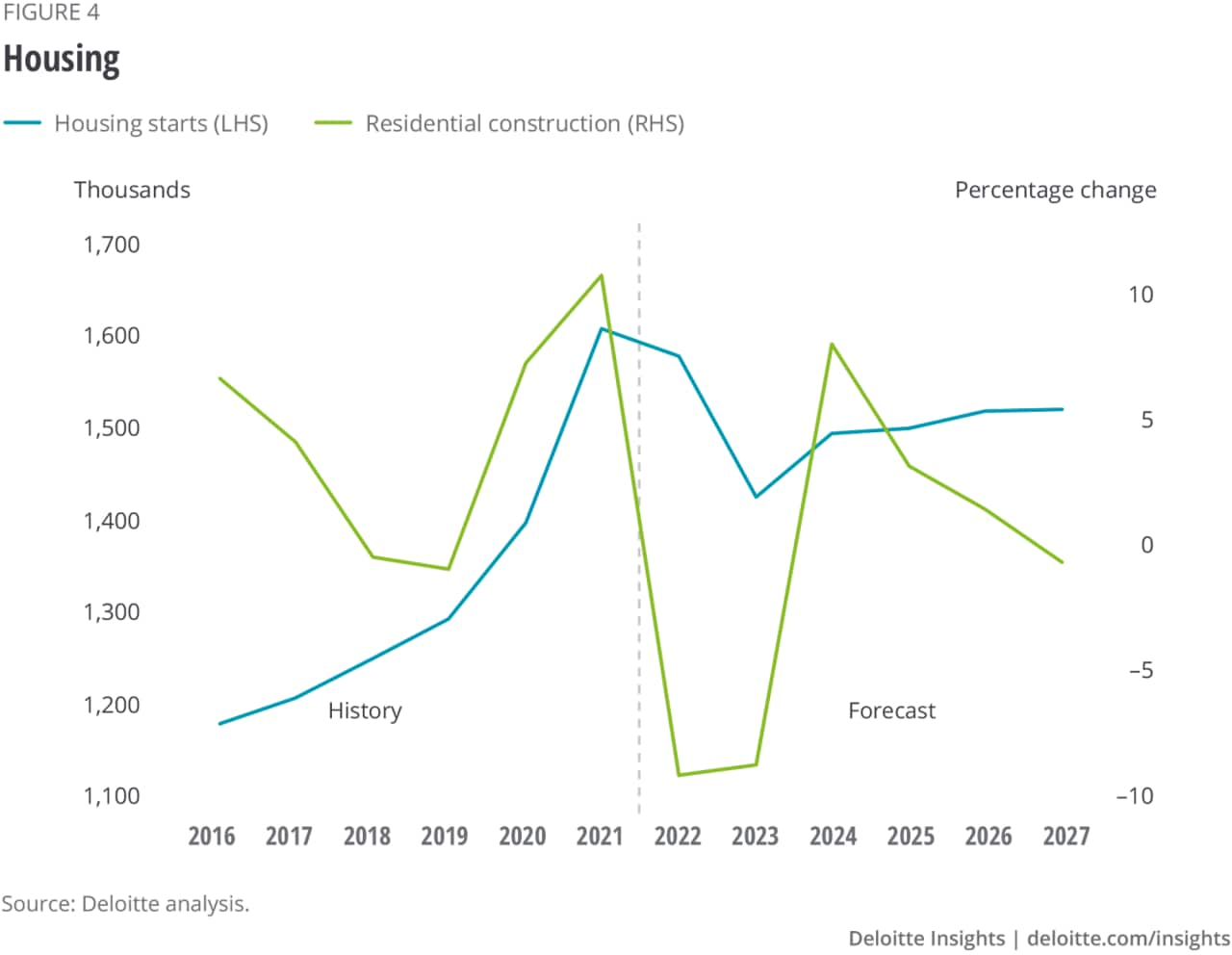

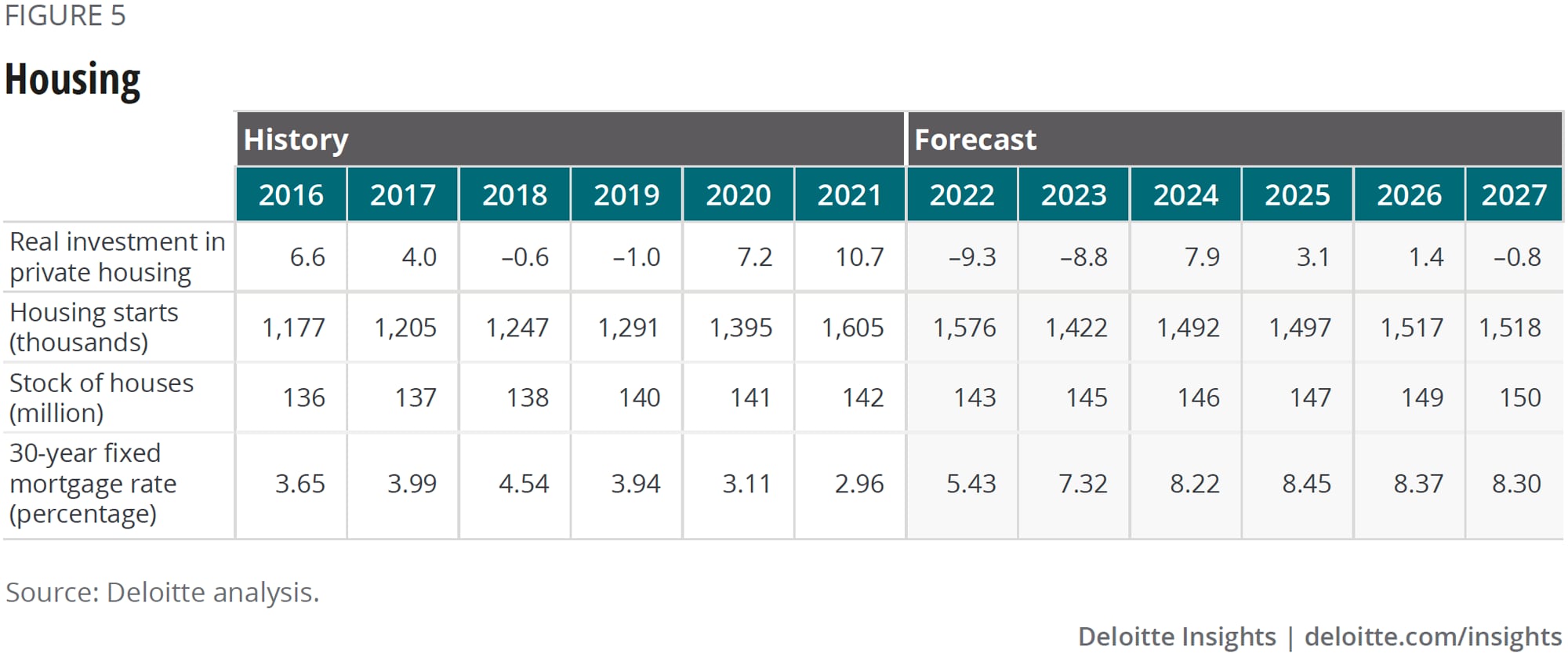

The housing sector outperformed the broader economy in the wake of the pandemic, as buyers and sellers found ways to navigate the pandemic’s restrictions. But the tables have turned. As the Fed has raised interest rates and inflation appeared, long-term interest rates have moved up dramatically. The result is a decline in housing starts from 1.7 million in Q1 2022 to 1.5 million in Q3—with more expected to come. And house prices, which rose sharply starting in the middle of 2021, have now declined for two months straight. Lower house prices will not be able to solve the affordability problem because of the jump in mortgage rates.

Deloitte expects construction to fall for the remainder of this year and in 2023. Housing may bounce back for a year or two after the current downturn runs its course.

Demographics, meanwhile, suggest that housing is not likely to become a key driver of economic growth in the foreseeable future. Population growth has slowed to about 0.5% per year (compared to over 1% during the 2000s housing boom). The baseline forecast assumes that, after the recovery from the current housing downturn, housing starts will eventually begin to slowly fall. Faster medium-term growth in housing would require faster population growth, most likely from immigration. Otherwise, the heightened demand for housing during the pandemic is likely to be a short-term phenomenon.7

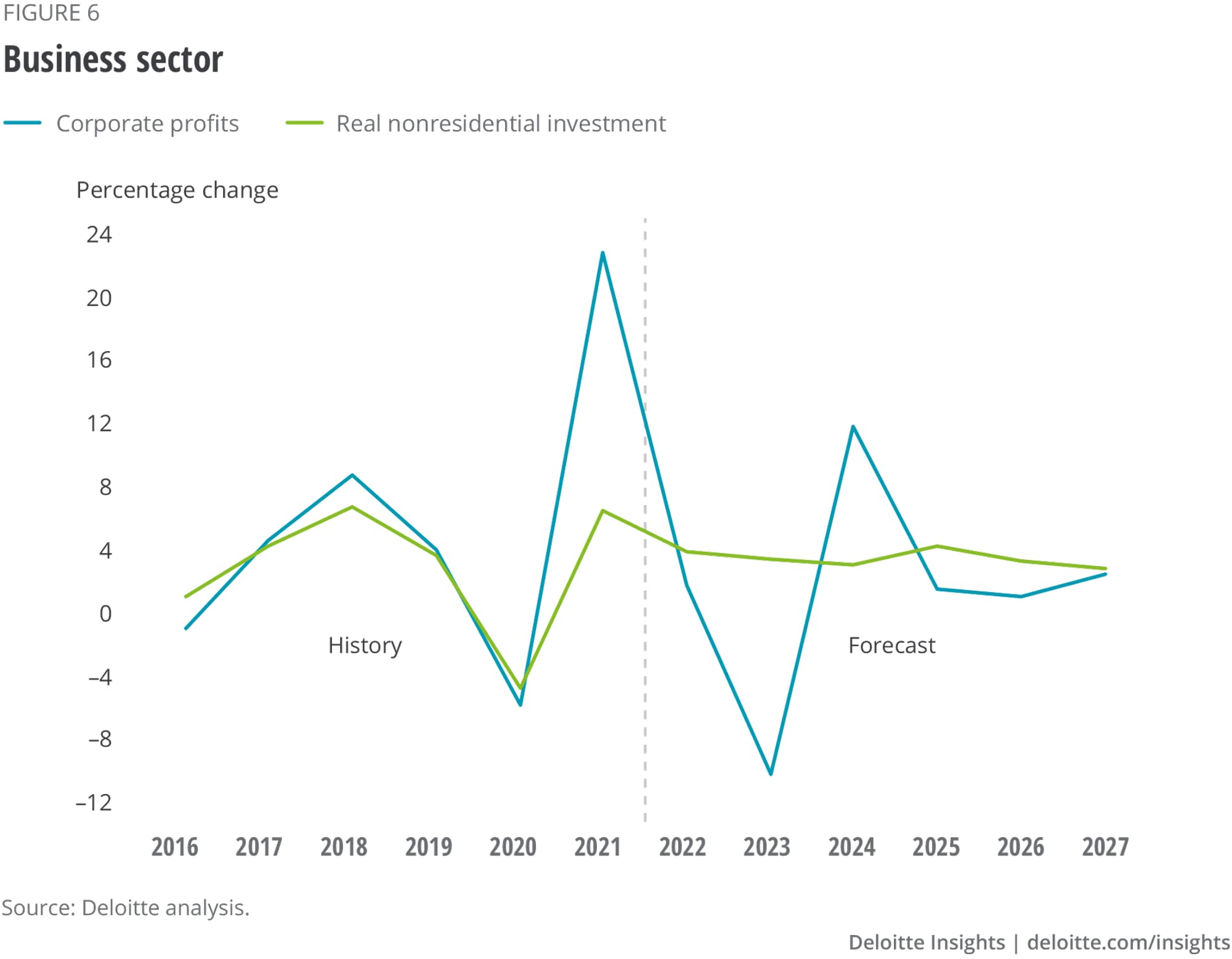

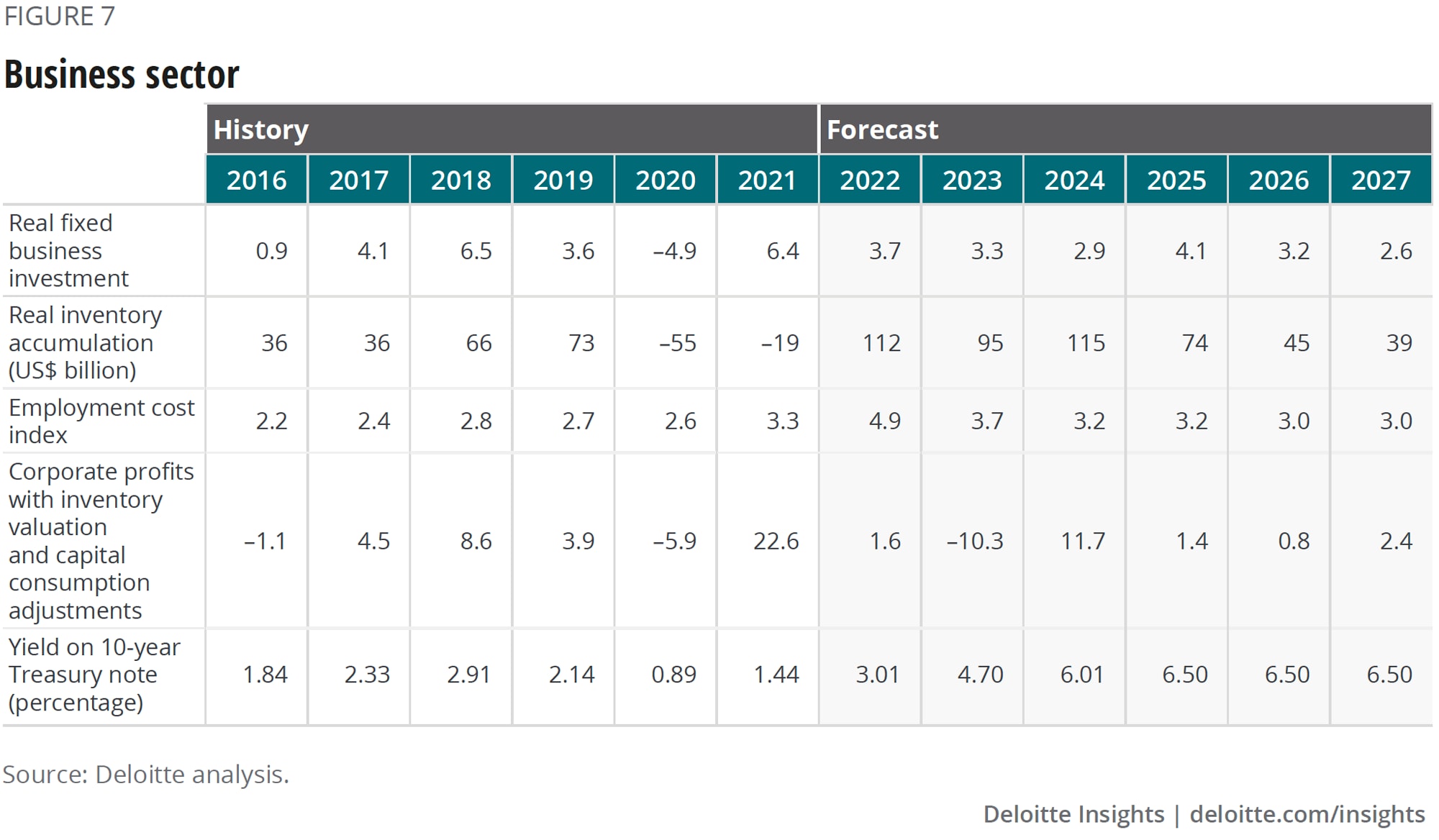

Businesses have ramped up investment since the initial impact of the pandemic, but they have been selective about what they are investing in.

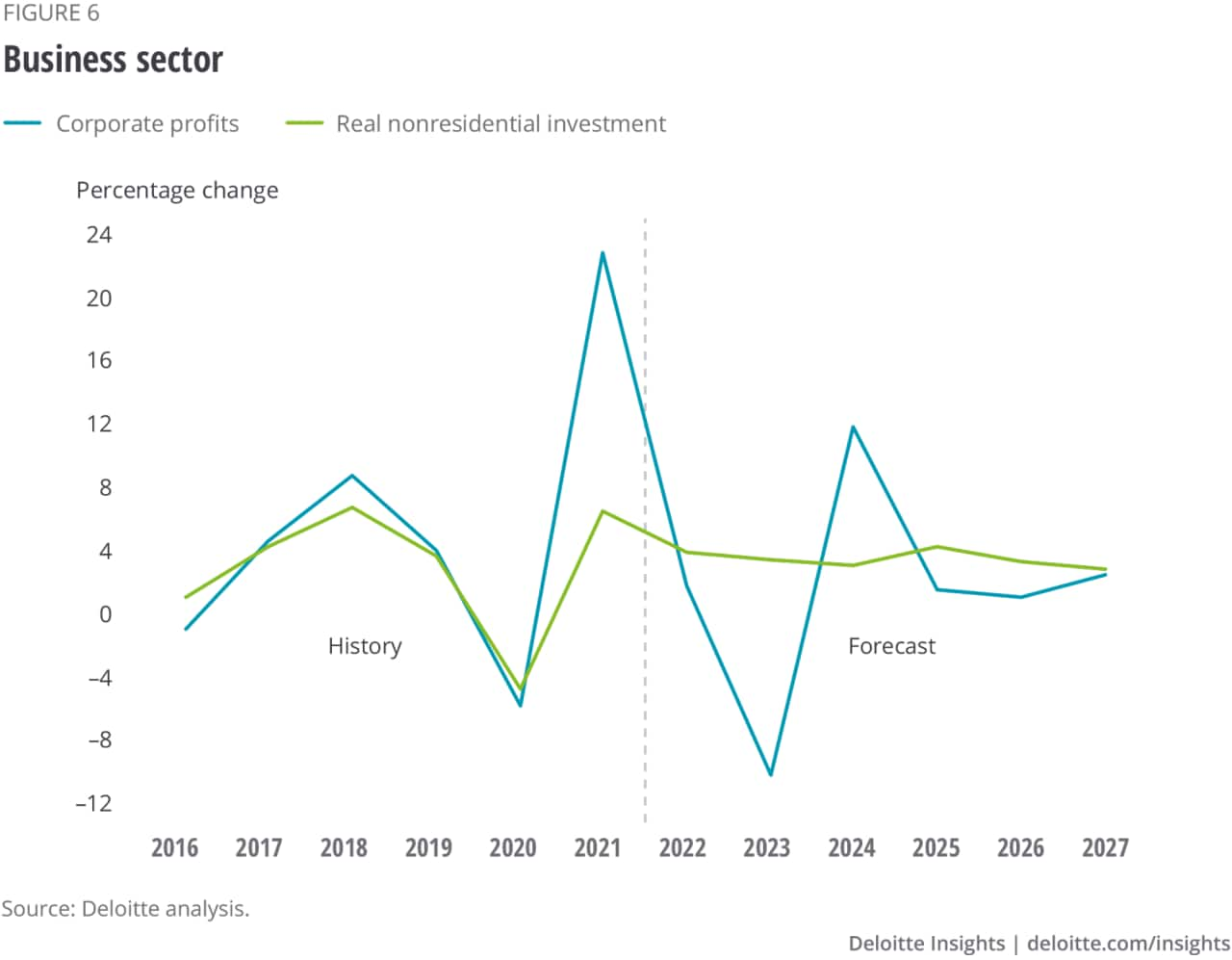

Investment in nonresidential structures continues to fall from the prepandemic level. It’s now down more than 20% and shows no signs of picking up again. The business case for office buildings and retail space has collapsed with online shopping and the shift toward working at home. The overall recovery in nonresidential construction is likely to be limited by the continued low demand for office and retail space.

Mining structures also took a big hit because of the decline in oil prices earlier in the pandemic. As this is dominated by energy mining, it would be reasonable to expect a ramp-up in response to the historically high energy prices. But that hasn’t been the case, for two reasons. First, investors in this sector have been whipsawed in the past 10 years as prices dropped from over US$100 in 2013 to below US$50 in 2015, and then back up to over US$100 last year. Those investors are now less likely to react to what might be a temporary price increase. Second, the long-term prospect for fossil fuel investments looks weak, as a consensus develops about fighting climate change.

Investment in equipment has been growing at a fast rate. This is dominated by transportation equipment, especially information technology (IT) equipment. Remote work makes IT equipment (and software) a substitute for buildings, and so the counterpart to weak investment in commercial structures is a lot of investment in IT. The Deloitte forecast assumes continued growth in equipment investment as both sources of demand are likely to remain strong.

Investment in intellectual property (which consists primarily of software and R&D) accelerated during the pandemic (after dropping in the first quarter of 2020). That’s mostly because of investment in software, and it likely reflects the investments needed for telework. We expect this category to remain strong over the next few years as businesses continue to require software to accompany their investments in information-processing equipment.

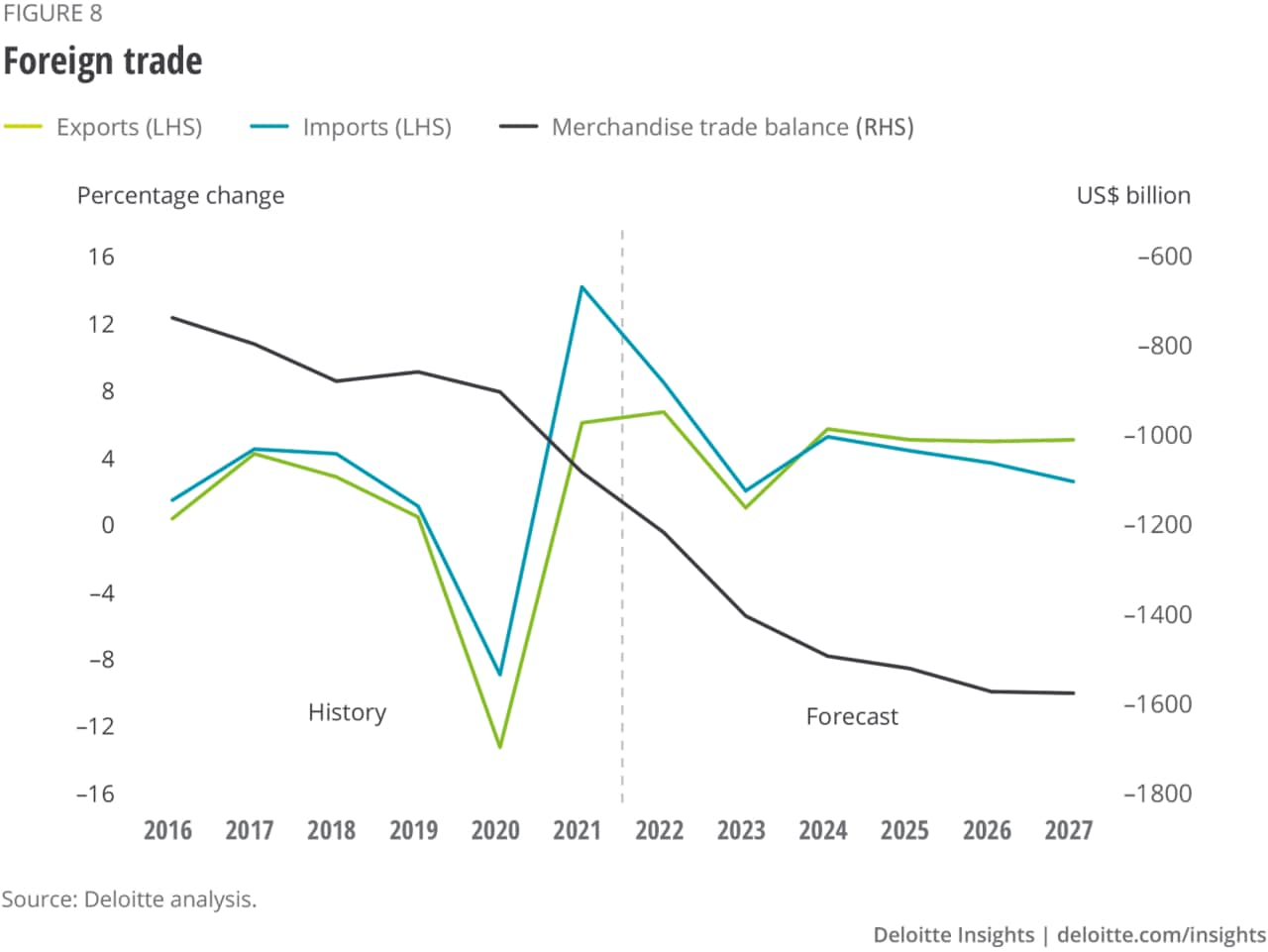

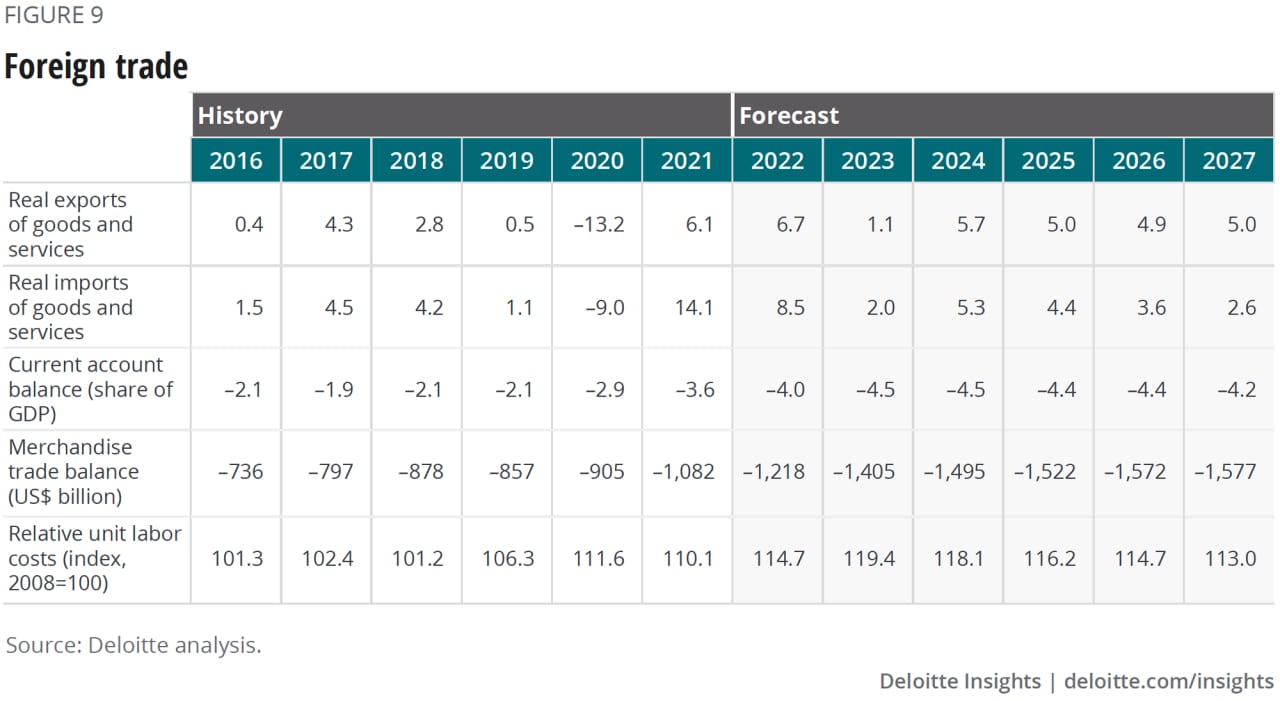

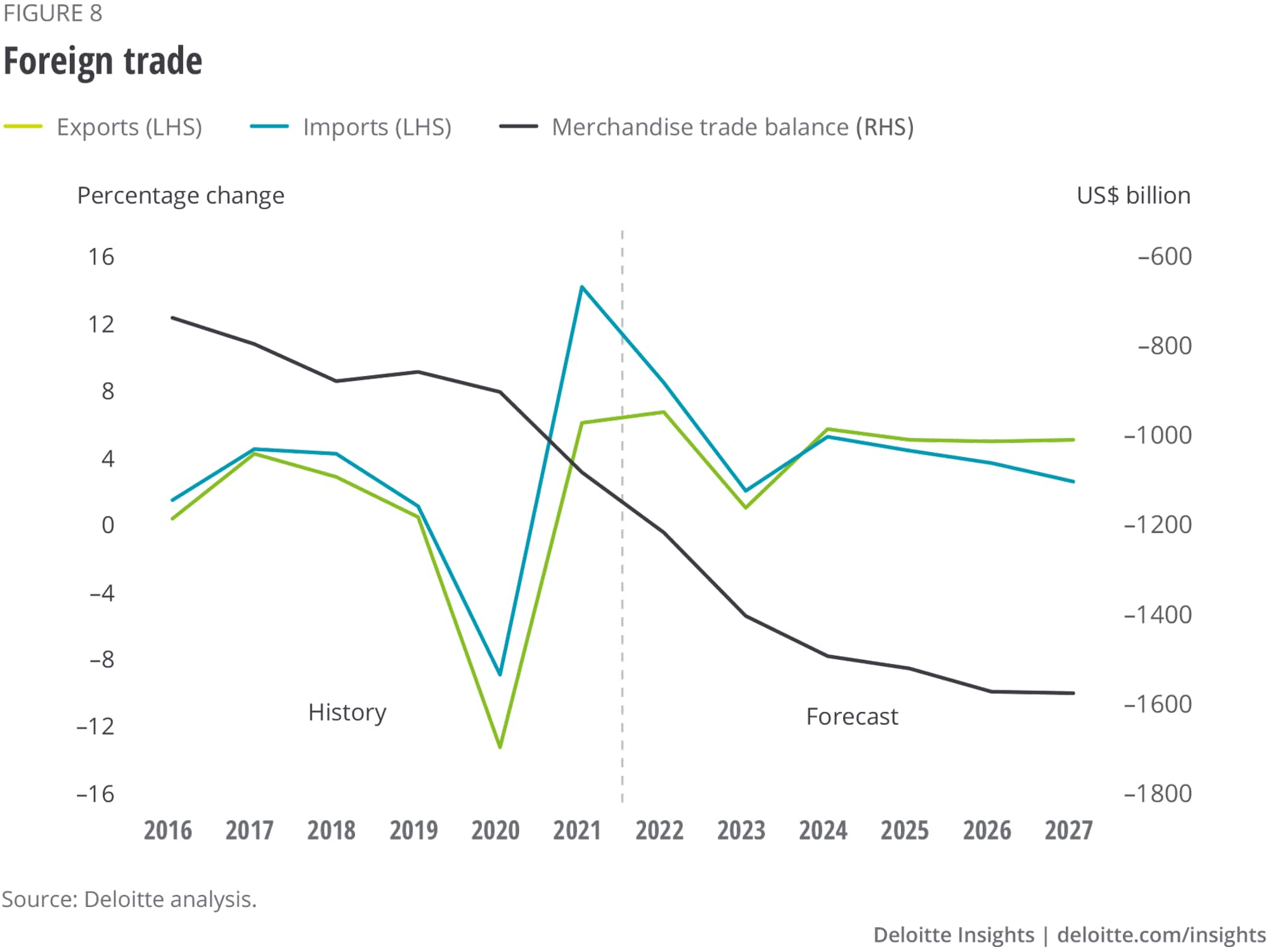

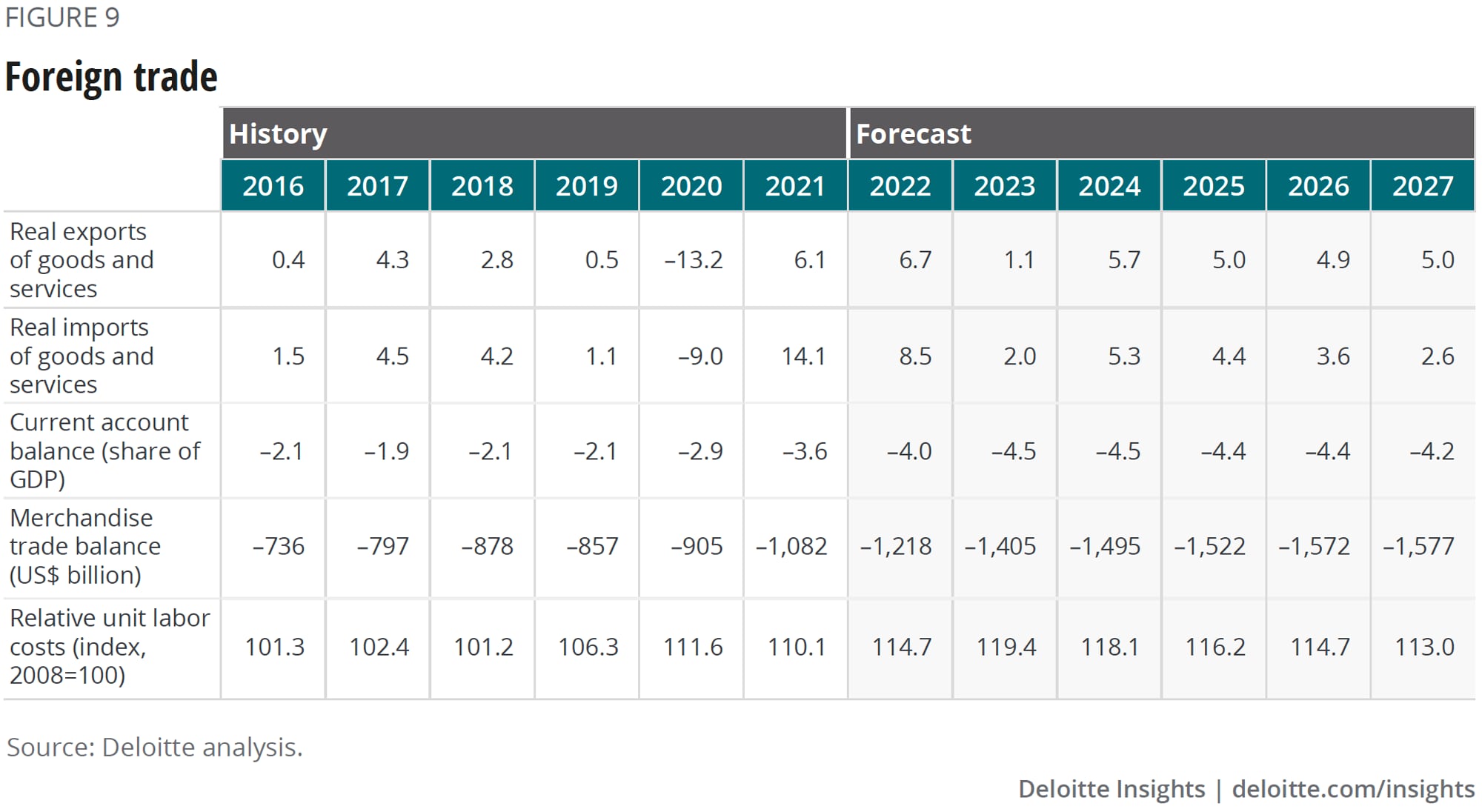

The Russian invasion of Ukraine is making things more difficult for US exporters. Lower demand from Europe (market for 15% of US exports) and a higher dollar create some short-term challenges.

Beyond the Ukraine crisis, things look more positive. Real US exports remain substantially below the prepandemic level, and real imports are now higher than they were in late 2019. This, however, may eventually translate into opportunities for the United States as global financial and economic conditions normalize. More normal financial conditions would create more opportunities for investment outside the United States and less desire to hold dollars to avoid risk, lowering the dollar and making the United States more competitive globally. And demand for US goods is likely to rise in the medium term as the global economy recovers from the pandemic. Deloitte’s baseline forecast therefore assumes that exports will grow more quickly than imports over the five-year horizon. As a result, there is a modest improvement in the current account deficit.

But there is another trend that is critical to consider. Over the past few years, many analysts have begun to expect a move toward deglobalization. Global exports grew from 13% of global GDP in 1970 to 34% in 2012. But since then, the share of exports in global GDP started to fall as globalization stalled, and opponents of freer trade started to gain more political influence. All this points to an unraveling of the policies that fostered the earlier globalization.

COVID-19 may have accelerated this shift. Although COVID-19 is a global phenomenon, leaders made major decisions about how to fight it—in both health and economic policy—on a country-by-country basis. Examples of this are the US withdrawal from cooperation in the World Health Organization in 2020 (although the United States has since rejoined) and the unilateral decisions of both China and Russia to deploy their own vaccines before the completion of phase 3 trials. And countries with vaccine-manufacturing facilities rushed to vaccinate their own citizens rather than cooperating on a global vaccination plan. All this was in stark contrast to the joint global approach that public health professionals might have recommended.

On top of this, the US-China trade conflict continues. The White House has shown some interest in returning to a multilateral approach to trade—for example, by supporting Ngozi Okonjo-Iweala for the World Trade Organization director-general. However, US Trade Representative Katherine Tai has made a point of stating that trade policy should be aimed at helping US workers. And many of the Trump-era tariffs remain in place, with little prospect that the tariffs on China, in particular, will be withdrawn.

On top of this, many businesses are considering rebuilding their supply chains to create more resilience in the face of unexpected events such as the pandemic and changes in US trade policy. The imperative for such changes has become stronger with the increasing supply chain issues and port delays facing importers of key components and consumer goods. It’s impossible, of course, to simply and quickly refashion supply chains to reduce foreign dependence. American companies will continue to source from China in the coming years. But companies will likely accelerate attempts to reduce their dependence on China (a process they had begun before the pandemic). Building more robust supply chains may mean moving production back to the United States, or perhaps to Mexico or some other, closer source. Or it may mean a portfolio of suppliers rather than a single source—even if the single source is the cheapest.

Reengineering supply chains will inevitably mean a rise in overall costs. Just as the “China price” held inflation in check for years, an attempt to avoid dependency on China might create inflationary pressures in the later years of our forecast horizon. And if markets won’t accept inflation, companies will have to accept lower profits to diversify supply chains. Globalization has offered a comparatively painless way to improve many people’s standard of living; deglobalization will likely involve painful costs and may limit real income growth during the recovery.

Financing investment is becoming a bit pricier as long-term interest rates rise. However, nonfinancial businesses are sitting on a pile of cash, and interest rates are still relatively moderate. In our baseline forecast, the corporate bond rate rises to over 7% and stays there through the end of the forecast horizon. Although that may appear high, historically it is relatively low. In fact, the cost of capital is likely to remain low enough to boost businesses’ ability to pay for all those new computers and servers, not to mention the software to run them. But even with easy financing terms, office and retail space will likely be unable to generate sufficient returns to entice businesses to increase capacity.

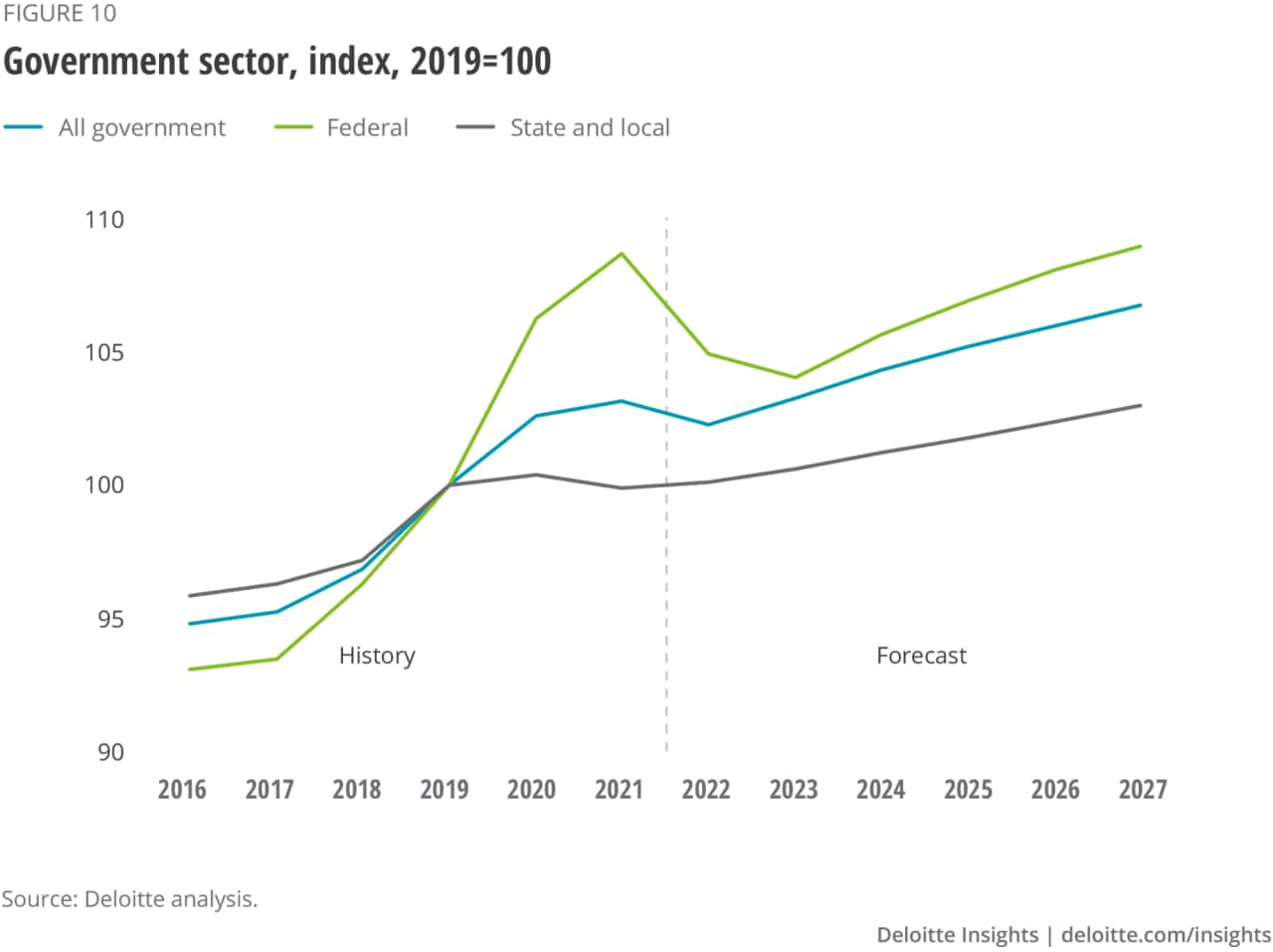

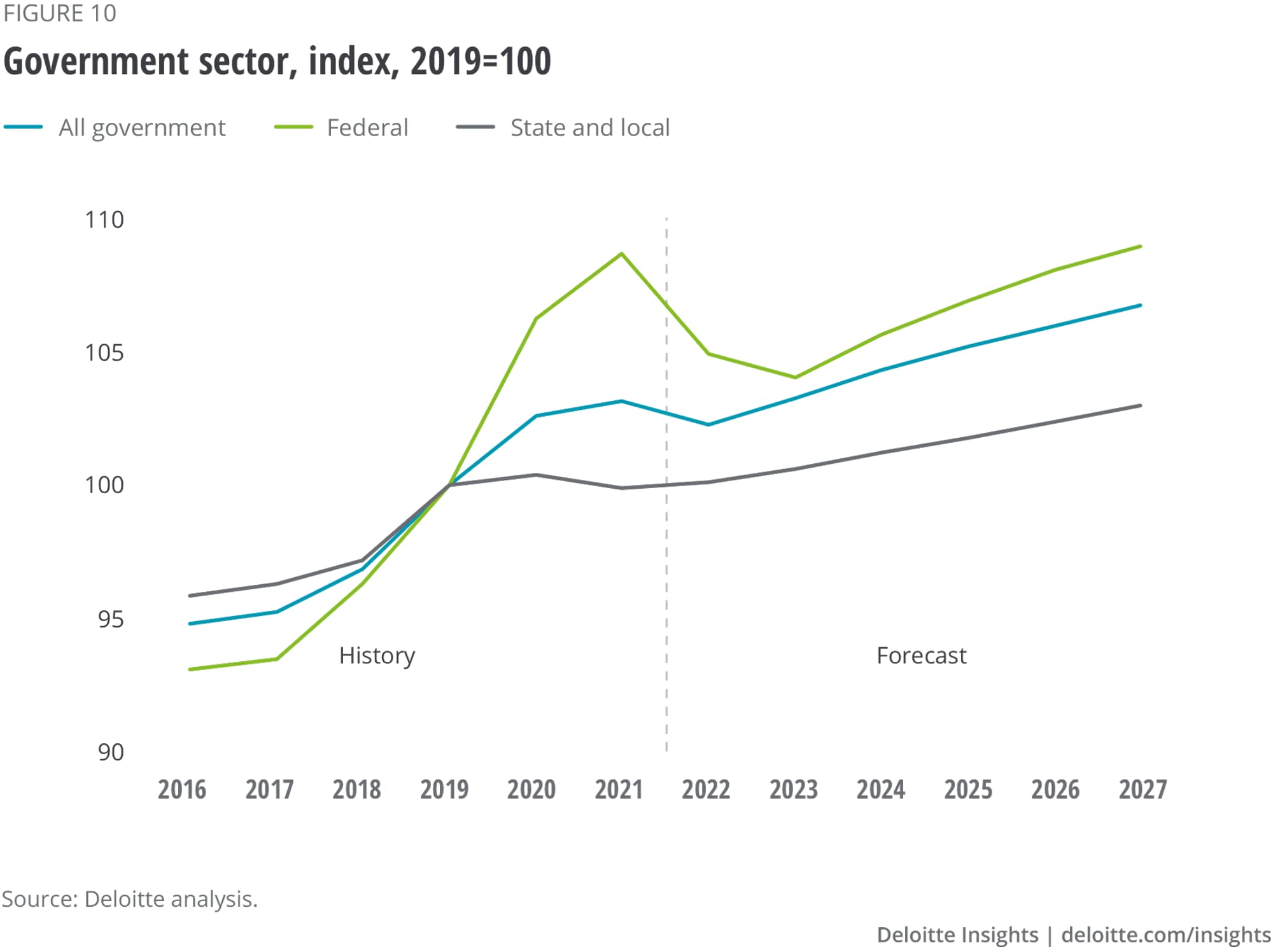

The big fiscal impulse from COVID-19–related spending has been largely reversed. The federal deficit is back to the prepandemic share of GDP (4%–5%). This has played a role in weakening demand, especially as federal transfer payments to individuals are now closer to the prepandemic level.

The Inflation Reduction Act will likely have only a modest impact on inflation. Despite the name, the main impact of the bill will be felt years from now, not in the inflation numbers of the next few months. The bill’s main impact will likely be through the energy/climate change provisions, and those will take years to have an impact. The tax provisions, while very important to certain taxpayers, are not likely to change overall tax collections or incentives for investment that much. And many people who buy health insurance through the Affordable Care Act exchanges will be helped by the extension of subsidies for medical insurance. But the overall impact on the deficit is likely to be modest. The Congressional Budget Office scoring showed a net decrease of US$90 billion over 10 years. In the context of a federal budget with almost US$7 trillion in outlays this year, US$9 billion in one year is just not a lot of money.

The infrastructure spending bill—already in place—will boost government spending over the next 10 years. This spending will increase the capacity of the economy and likely help to drive some additional productivity growth. Much of this additional spending comes toward the end of our forecast horizon, however. The total spending impulse will be moderated by higher inflation. And the amount of spending is relatively modest compared to the economy as a whole. According to the Congressional Budget Office, in 2026, the peak year of spending, the bill will add about US$61 billion to the federal deficit.8 That amounts to about 0.2% of projected GDP. The infrastructure bill is likely to have a positive and significant impact on public capital in the United States, but it’s not a large fiscal stimulus by any means.

Split government makes the likelihood of a significant fiscal change unlikely (although not impossible). It creates two risks. First, as agreement among the President, the Senate, and the House of Representatives becomes more difficult, the possibility of a federal government shutdown rises. A shutdown is not likely to change the overall trajectory of the US economy (unless it lasts quite a long time), but it would inject some additional uncertainty into the forecast. Second, the split government brings up the possibility of breaching the debt limit. That could potentially have a significant impact on financial markets and the economy. See the sidebar, “The looming debt ceiling problem,” for an explanation of the debt ceiling and what might happen if it is not raised in time.

Our baseline forecast assumes deficits will rise to US$1.6 trillion by 2027. That’s a hefty amount, one that inevitably raises the question of whether the US government can continue to borrow at such a pace. The answer is that it can—until investors lose confidence. At this point, most investors show no sign of concern about US debt. In fact, very low interest rates on US government debt indicate the world wants more, not less, American debt. We anticipate no problem over the forecast horizon, beyond the risk that Congress won’t raise the debt ceiling.

But the US government will face a crisis if it does not eventually find ways to reduce the deficit and consequent borrowing. The crisis may be many years away, and current conditions may argue for waiting. It could, however, be a bad idea to wait too long once those conditions lift.

Recent press reports on the possible goals of a Republican Congress in 2023 have mentioned the problem of the US debt limit. This is a significant issue that could lead to a global financial crisis. The good news is that this is one crisis that has an easy solution. What’s the problem?

The US Treasury regularly borrows money to cover the federal deficit, but it must receive authorization from the Congress (a rise or suspension of the debt limit) to do so. In the recent past, this has become a contentious process. Indications are that it will become even more contentious. Kevin McCarthy, the likely future Republican House speaker, has indicated that a Republican-led House would insist on “undoing” some of the recent spending passed in the current Congress. Others have discussed “reforming” social security. Would this be symbolic, or would it be intended to reverse much of the legislation of the past two years? Much depends on how weak the Republicans in Congress believe the President to be, and the willingness of the administration to accept a period of time when the debt ceiling prevents federal borrowing.

One key to understanding why the debt ceiling is likely to become a problem is that Democrats have changed their perception of their “payoff matrix”—the expected values of different strategies (compromising or not compromising) since similar battles during the Obama administration. President Biden and Senate Majority Leader Schumer demonstrated a willingness to permit the debt ceiling suspension to expire in 2021. If Republican perceptions of Democrats’ views are still shaped by their previous experience, the Republicans may misjudge how much leverage they have. This makes the possibility that the combined result of both sides’ strategies (in game theory terms) will be letting the current debt ceiling suspension lapse.

Suppose the debt ceiling suspension does lapse, and Treasury can no longer borrow above the statutory level. The US Treasury has determined that it cannot prioritize payments, so its ability to pay bills on any given day would depend on that day’s cash flow. There would almost certainly be days when the Treasury would have to miss interest payments on Treasury securities. Some analysts have described this as “default,” although it’s very different from a true default or insolvency. But it’s not just interest payments. Treasury is likely to miss payroll payments for federal workers and social security payments for retirees, depending (noted) on a particular period’s cash flow.

The initial outcome of missing a Treasury payment might be relatively muted. At first, prices of specific Treasuries (those scheduled to pay interest on a date when Treasury would not be expected to have cash) would rise. But a longer period of time when Treasury payments stop might create difficulties for the global financial system, which depends on Treasury securities as its foundation. Nowhere else can financial market players find such a large supply of low-risk assets, so Treasuries will not be easily replaced.

The good news is that, over time, the political pressure to solve the problem will grow. Missed social security checks should get the attention of enough members of Congress to allow a bipartisan fix. And Wall Street will certainly be pressuring those members of Congress who are business-friendly. The United States has no fundamental inability to make debt payments, like Argentina or Greece. It’s just a matter of passing the law to allow the Treasury to do so.

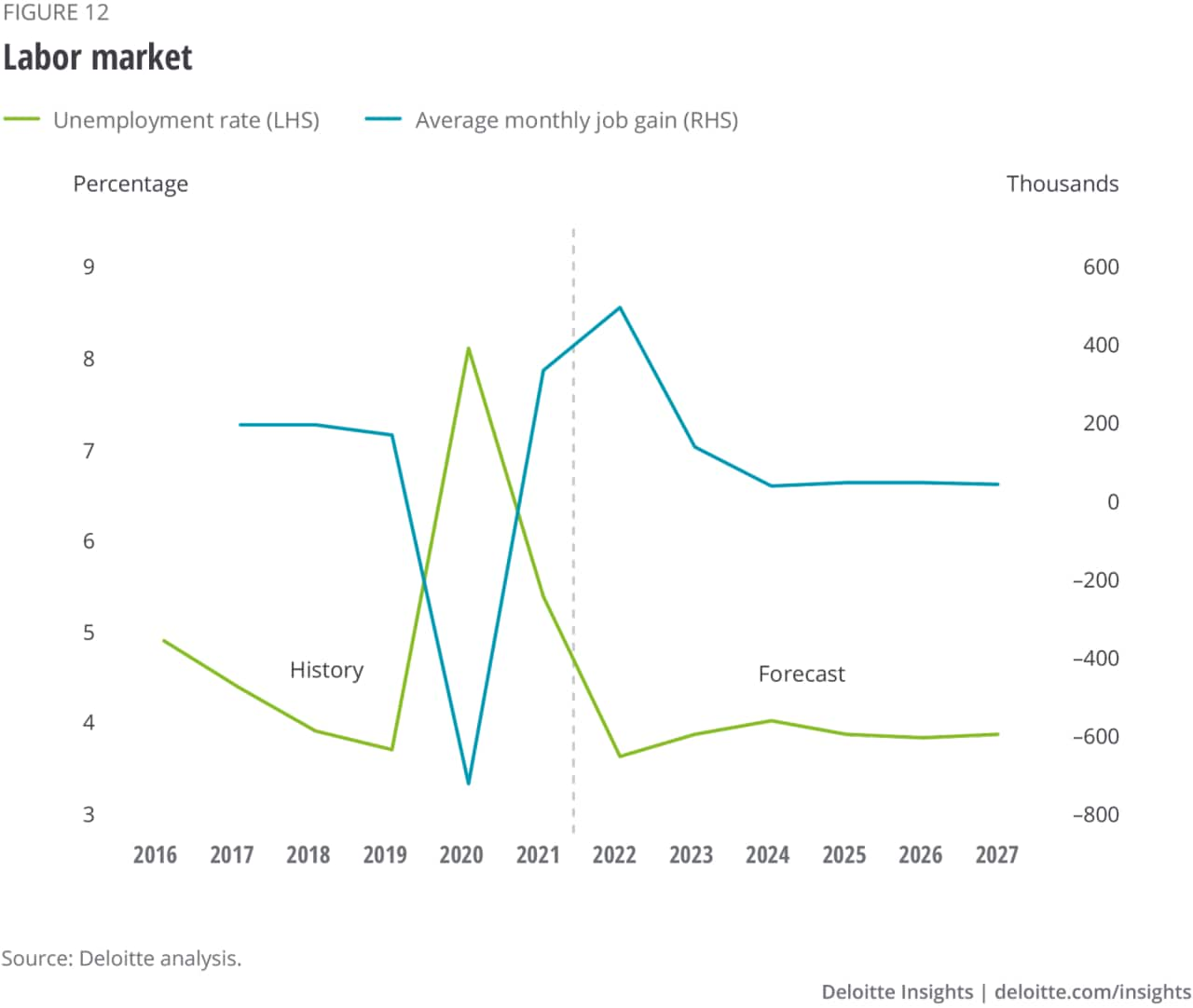

The conversation on labor markets has switched—and fast. Not long ago, employment was millions below the prepandemic level, and the main question was how difficult it would be to get all those workers back on the job. Now employment is above the prepandemic level and business commentary is full of talk about labor shortages and stories about employers struggling to find workers. It’s hard to argue that the economy is experiencing a recession when the unemployment rate remains low, job growth is strong, and the ratio of job openings to unemployed people remains far above normal levels.

While employment has fully recovered from the pandemic, labor force participation has not. The October labor force participation rate was 1.2 percentage points below the rate in February 2020. That amounts to about 3.4 million people who are missing from the labor market. Who are those people? They are mostly older Americans. The labor force participation rate for ages 16–64 has been at the prepandemic level for most of this year. But the rate for people over 65 has fallen quite a bit. Many of these people have probably retired, in the sense of expecting to remain permanently out of the labor force, but some can likely be enticed back with the right compensation packages and flexible working hours and conditions.

As is the case in many areas, the pandemic accelerated trends that were evident before it started. Slow labor force growth and continued high demand had already created conditions that required companies to offer higher wages to lower-skilled workers and to be more imaginative about hiring. In the post–COVID-19 world, companies that make extra effort to find the workers they need and provide conditions to attract those workers will have an important competitive advantage.

Deloitte’s baseline forecast assumes that job growth slows to sustainable levels (less than 100,000 jobs per month) in the next year. The unemployment rate rises a bit as growth slows in 2023, but the job market remains relatively tight. Over the longer horizon, labor force growth slows to just 0.2% per year, presenting continuing challenges for employers. It’s a demographic fact that employers will have to learn to live with.

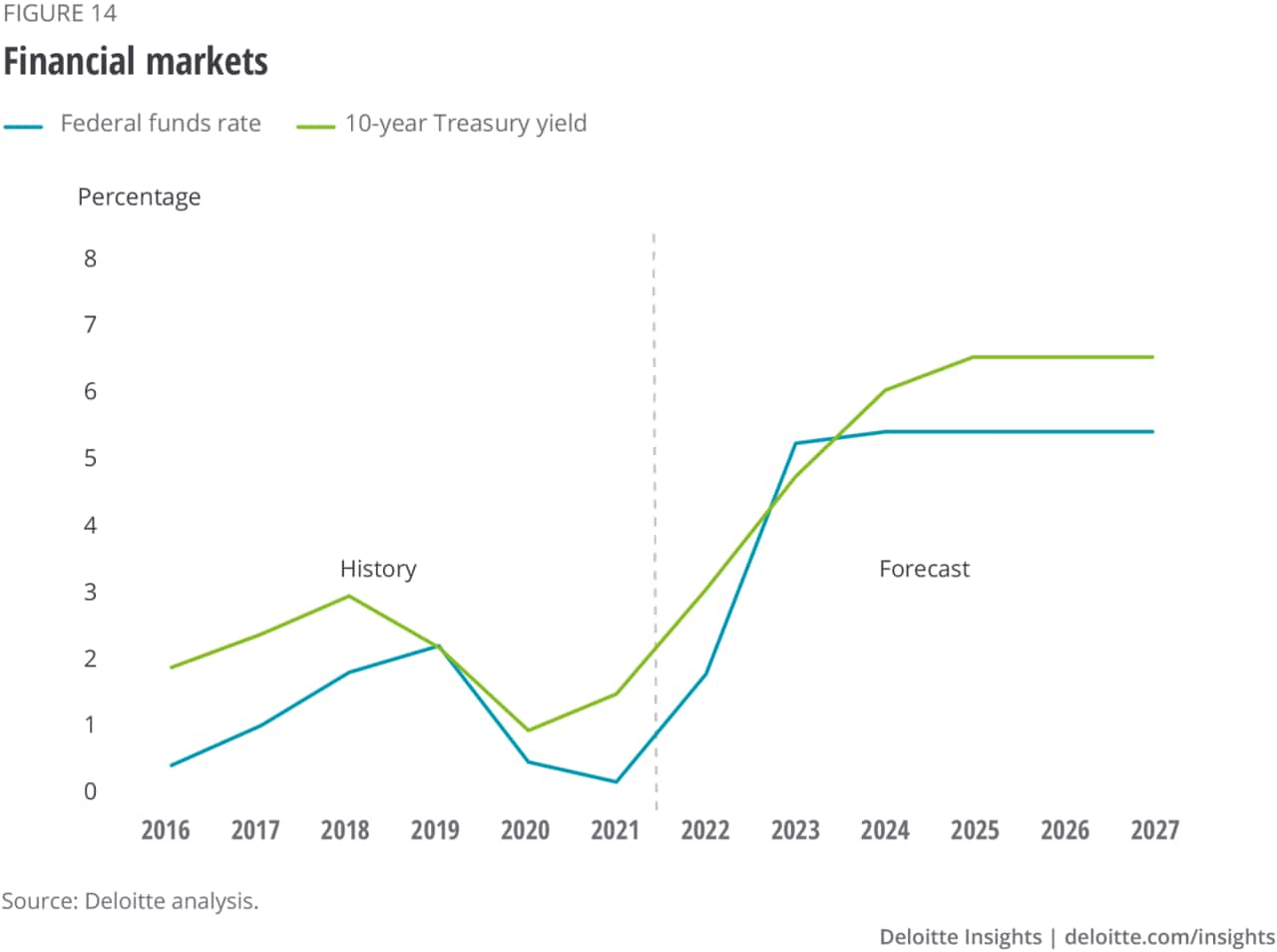

For over a decade before the pandemic, interest rates were unusually low. An inflation rate of around 2% suggests a neutral Fed funds rate of around 4%, but the funds rate remained close to zero for 10 years after the global financial crisis. The pandemic seems to have jolted the financial system in a manner that requires higher interest rates—and the Fed is willing to oblige. Four 75-basis-point hikes suggest that Fed officials feel quite a bit of urgency in returning the Fed funds rate to something like a neutral position.

Although it seems extreme, the current policy is nowhere near as tight as the anti-inflation actions the Fed undertook over 1979–1982. At that time, the nominal rate went over 19%, and the real Fed funds rate hit almost 10% in one month. The current policy, on the other hand, seems to be aimed more at just getting the funds rate back to some neutral level, so that the Fed is not being so accommodating.

That’s cause for some optimism, but it doesn’t mean that interest rate hikes can’t cause pain. Long-term rates are rising, again to levels that would have been considered normal in the past. But if the corporate bond rate goes above 7%, as implied by our baseline forecast, holders of past corporate bonds issued at the low rates of the past 10 years will have to eventually take a loss. Exactly how the loss is recorded depends on the accounting and regulatory environment of the investor. Could this create systemic problems for the financial system? So far, it looks like investing organizations have managed to prevent any significant impact from the repricing of low-return bonds. The success of US bank stress tests is an additional sign that the financial system is in good shape. But this remains an important potential problem for individual investors, and for the financial system.

Our baseline forecast assumes that the Fed will slow the size of interest rate hikes. We assume that the Fed funds rate will hit a maximum “terminal” rate of 5.325% by the middle of the year. Should inflation continue to be strong, as in our “Back to the ’70s” scenario, the Fed will push the funds rate even higher.

A Fed funds rate of 5% implies a significantly higher long-term rate. Our baseline forecast has the 10-year Treasury note yield rising to 6.5% in the later years of our forecast. This is consistent with the historical relationship of these rates under moderate inflation: Should inflation continue to be high, the spread between the 10-year note and the Fed funds rate could continue to rise (as investors account for expected inflation in the later years of the note’s period). Investors should take care to watch for the possibility of higher interest rates—although by the standards of the 1970s and 1980s, these rates are still quite low.

Of course, interest rates are always the least certain part of any forecast: Any significant news could—and will—alter interest rates significantly.

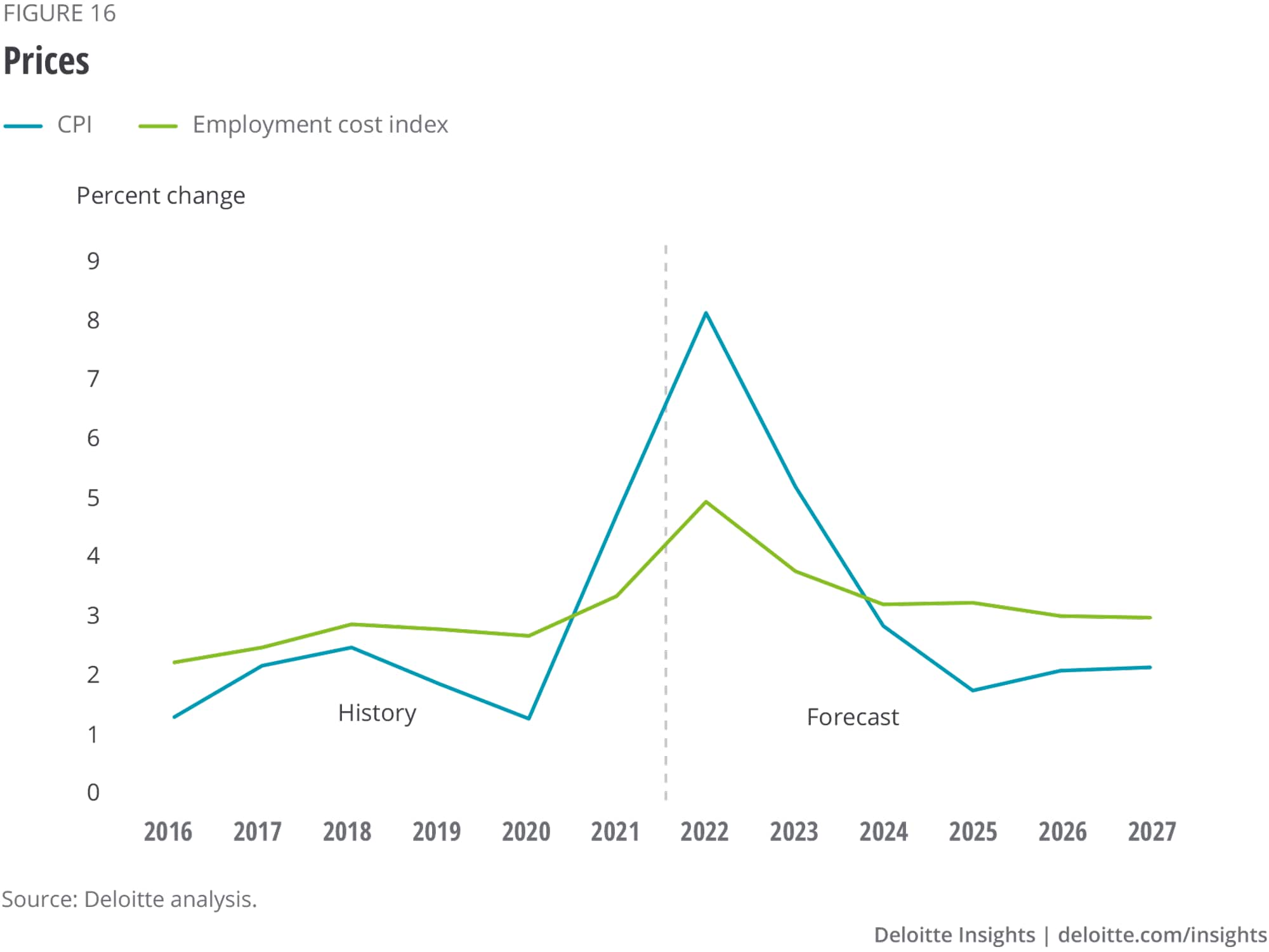

Some welcome signs of softening inflation have begun to appear. Core and headline CPI inflation were down in October. This isn’t the first month of low core inflation; we have had occasional months of moderate inflation mixed in with the more worrisome high inflation. But the overall slowdown in demand, and signs that supply chain issues have been largely resolved give room for some hope that the slowdown will continue this time.

At this point, the Fed will be examining the details of each price release to determine whether inflation is really softening enough to slow or stop the rate of monetary tightening. Core inflation is an important measure, in this case. But other details—such as the fact that the shelter component of CPI tends to lag housing prices9—will also play a role.

The Deloitte forecast continues to assume that the current inflation is “transitory” in the sense that it will dissipate over time. Companies are already finding ways around many of their supply chain problems, as evidenced by falling transportation prices and growing inventories. And our forecast of declining demand for consumer durables suggests that the need for expanded production will gradually decline, reducing the bottlenecks that are currently frustrating producers and leading to higher prices. Our baseline forecast shows CPI inflation spiking to over 8% in 2022. But by 2023, total inflation falls to 5.2%, and, by 2024, 2.8%. We remain optimistic that today’s households and businesses will avoid the unpleasant experiences of the long inflation and painful disinflation that their predecessors experienced during 1970–1985.

Unless otherwise indicated, all economic data comes from the US government or, where indicated, private sources as reported by Haver Analytics.

View in ArticleJulius Shiskin, “The changing business cycle,” New York Times, December 1, 1974.

View in ArticleNational Bureau of Economic Research, “Business cycle dating,” accessed September 5, 2022.

View in ArticleSee, for example: Jonathan L. Willis and Guangye Cao, “Has the US economy become less interest rate sensitive,” Kansas City Fed Economic Review, Q2 2015, pp. 5–36.

View in ArticleBoard of Governors of the Federal Reserve System, Economic well-being of US households in 2021, May 2022.

View in ArticleIbid.

View in ArticleLester Gunnion, Why is the housing sector booming during COVID-19?: Economics spotlight, November 2020, Deloitte Insights, November 20, 2020.

View in ArticleCongressional Budget Office, “Senate Amendment 2137 to H.R. 3868, the Infrastructure and Jobs Act, as proposed on August 1, 2021,” August 9, 2021.

View in ArticleXiaoqing Zhou and Jim Dolmas, “Surging house prices expected to propel rent increases, push up inflation,” Federal Reserve Bank of Dallas, August 24, 2021.

View in ArticleThe author would like to thank Bhavna Tejwani for her contributions to this article.

Cover image by: Sofia Grace Sergi