Help wanted: Job postings continue to far outnumber available workers has been saved

Cover image by: Jaime Austin

Whether countries experiencing the highest inflation rates seen in decades can manage a soft landing remains in question, as central banks act to slow demand by tightening monetary policy. But whether this ends in a slowdown or outright recession, one of the outcomes will likely be a reduced demand for workers in the near to medium term. This report considers the labor markets of three countries: Canada, the United Kingdom, and the United States—countries that are similarly situated with very tight labor markets and aggressive monetary policies.

Indicators currently suggest that any economic slowdown or downturn in these countries should be short and shallow. When these economies recover, however, the question becomes will they return to the situation where needed workers are difficult to find, or will a slowdown reset labor demand and supply?

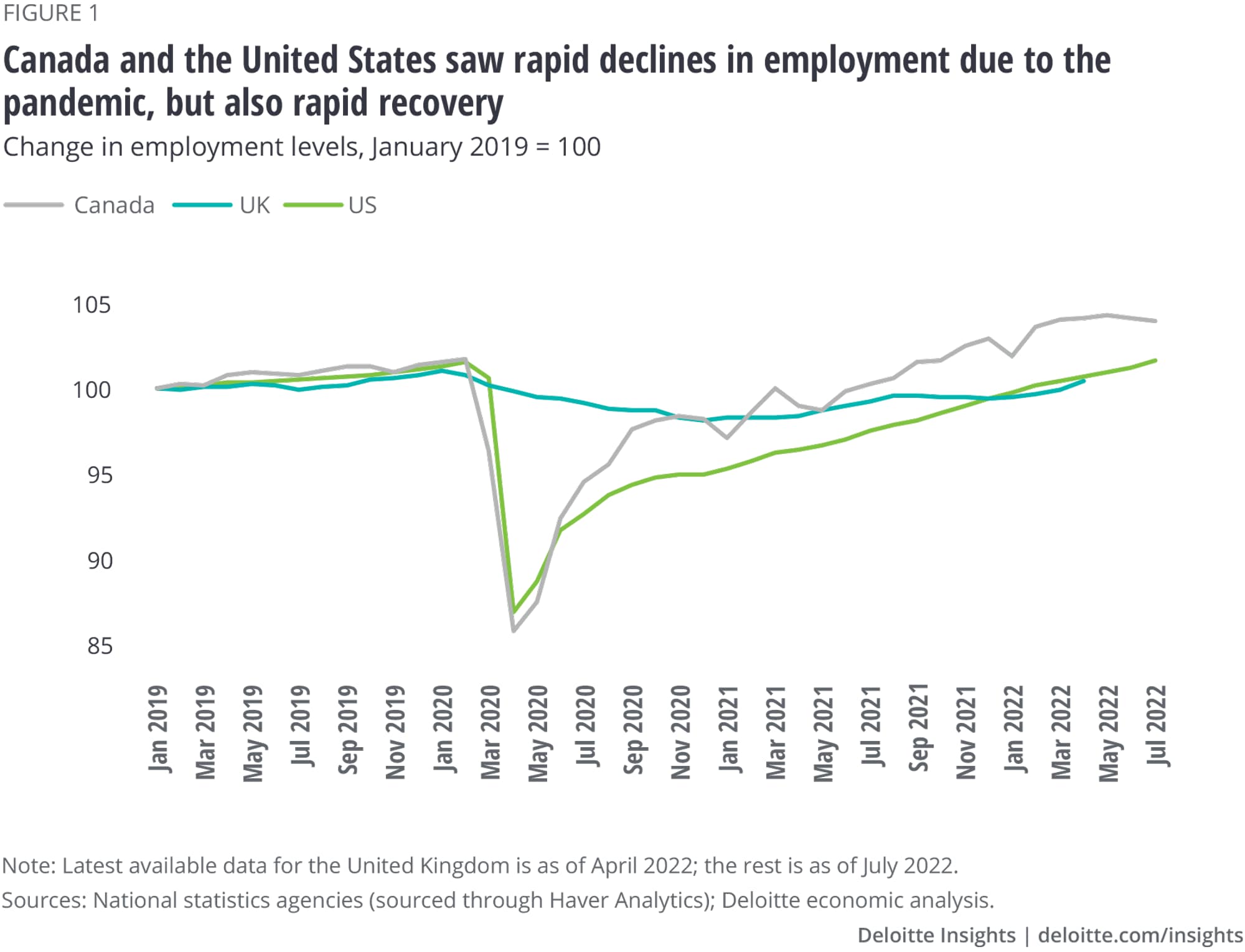

Prior to the eruption of the COVID-19 pandemic in early 2020, employment levels in Canada, the United Kingdom, and the United States were increasing at rates faster than the labor force, allowing unemployment rates—already at low levels—to continue to decline. When the pandemic hit, the impact on businesses in the three countries was similar but differing policy responses resulted in different labor market results. The United Kingdom, like most other European countries, used a furlough scheme to compensate business establishments so that they could continue to pay idled workers, while Canada and the United States provided supplementary payments directly to the large number of workers laid off. As shown in figure 1, employment levels in Canada and the United States plunged almost 15% relative to their prepandemic levels in just a couple of months, while immediate declines in employment in the United Kingdom were muted.1

Figure 1 also illustrates the differences in the behavior of these labor markets as the pandemic wore on. Even with the furlough programs in place, employment levels in the United Kingdom experienced a gradual decline before starting to rebound in early 2021; however, it still has fewer workers relative to its prepandemic level. Canada’s labor markets showed remarkable resiliency, with employment quickly bouncing back and surpassing prepandemic levels by September 2021. Immediate gains in the United States were nearly identical to the Canadian experience, but then the pace of job gains slowed, and only recently did employment reach its prepandemic level.

The fact that employment has been slow to recover in the United Kingdom and the United States is remarkable, given that the demand for workers is very high. However, while demand is high, supply is not—these countries have very low unemployment rates. Even in Canada, although employment growth has been strong, the unemployment rate is at a low not seen since 1970.

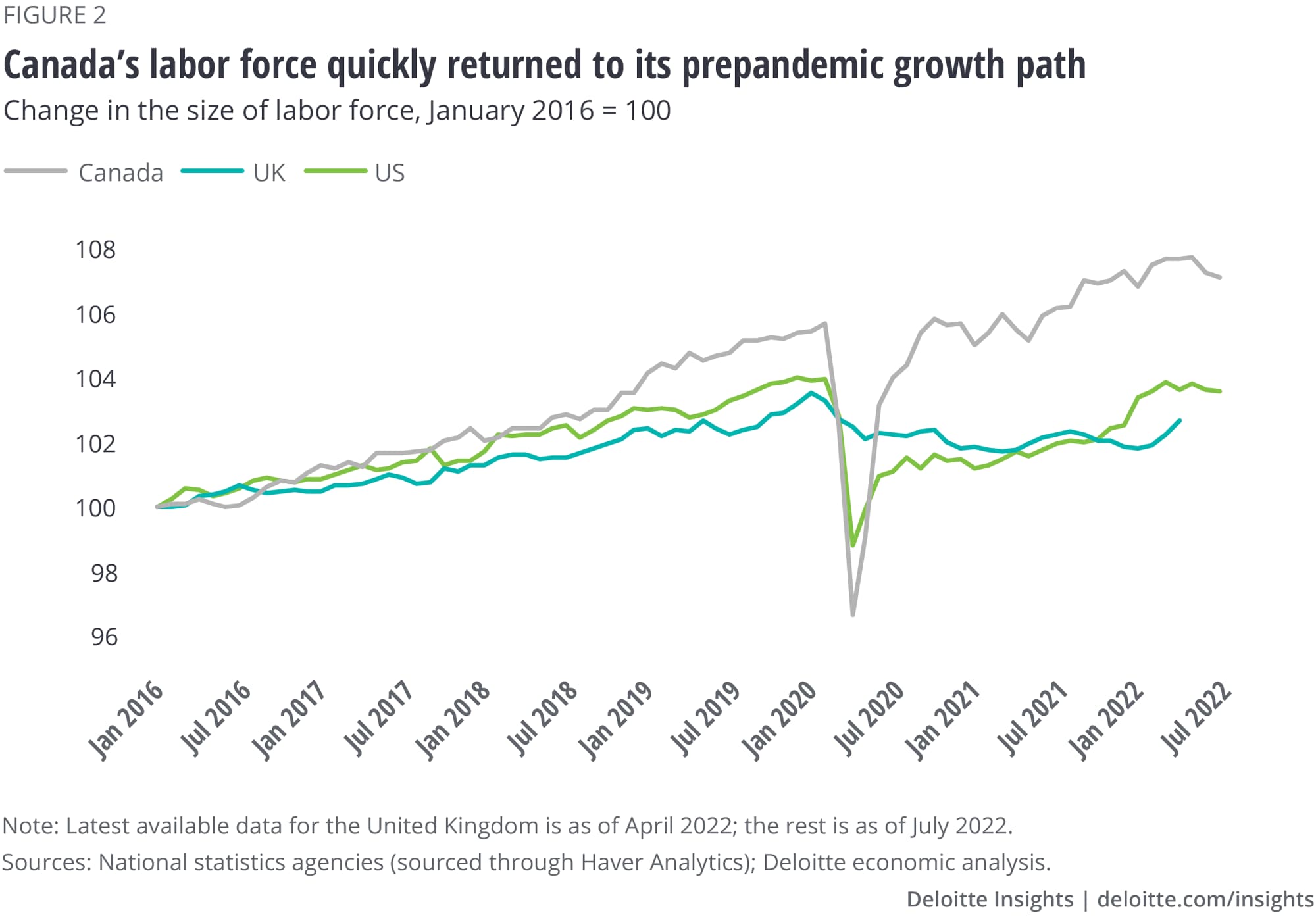

The labor force defines the pool of readily available workers—those with a job (the employed) and those looking for a job (the unemployed). As shown in figure 2, the size of Canada’s labor force quickly rebounded—as those who left the labor force early in the pandemic returned—and resumed growing at a rate similar to the prepandemic rate. The experience of the United Kingdom and the United States has been very different. The size of the UK labor force has continued to remain depressed, while the size of the US labor force has only recently surpassed its prepandemic level. So, the pool of available workers in the two countries has definitely not kept pace with the needs of a growing economy.

The primary drivers of change in the size of the labor force are changes in population, the age distribution of that population, and the labor force participation rate (LFPR), i.e., changes in the proportion of the population who work or want to work.

The size of the Canadian labor force gets a strong boost from its fast-growing population. Between 2016 and 2021 (Canadian census years), Canada’s population grew by 5.2%—the fastest rate of any of the G7 countries—while the populations of the United Kingdom and the United States only grew by 2.9% and 2.6%, respectively. Statistics Canada attributed 80% of the growth in the Canadian population over this period to immigration.2 The United Kingdom and the United States, on the other hand, are unlikely to register a similar boom any time soon.

Although Canada’s net international migration fell between 2019 and 2020, the numbers recovered and reached near-prepandemic levels by the end of 2021.3 This is in stark contrast to the United States, where the number of immigrant visas issued in the fiscal year 2021 was 40% lower than that issued in 2019.4 In the United Kingdom, the twin effects of the pandemic and Brexit combined to reduce the number of immigrants, with Her Majesty's Revenue and Customs reporting that between June 2019 and June 2021, the number of EU nationals on UK payrolls fell by more than 170,000.5

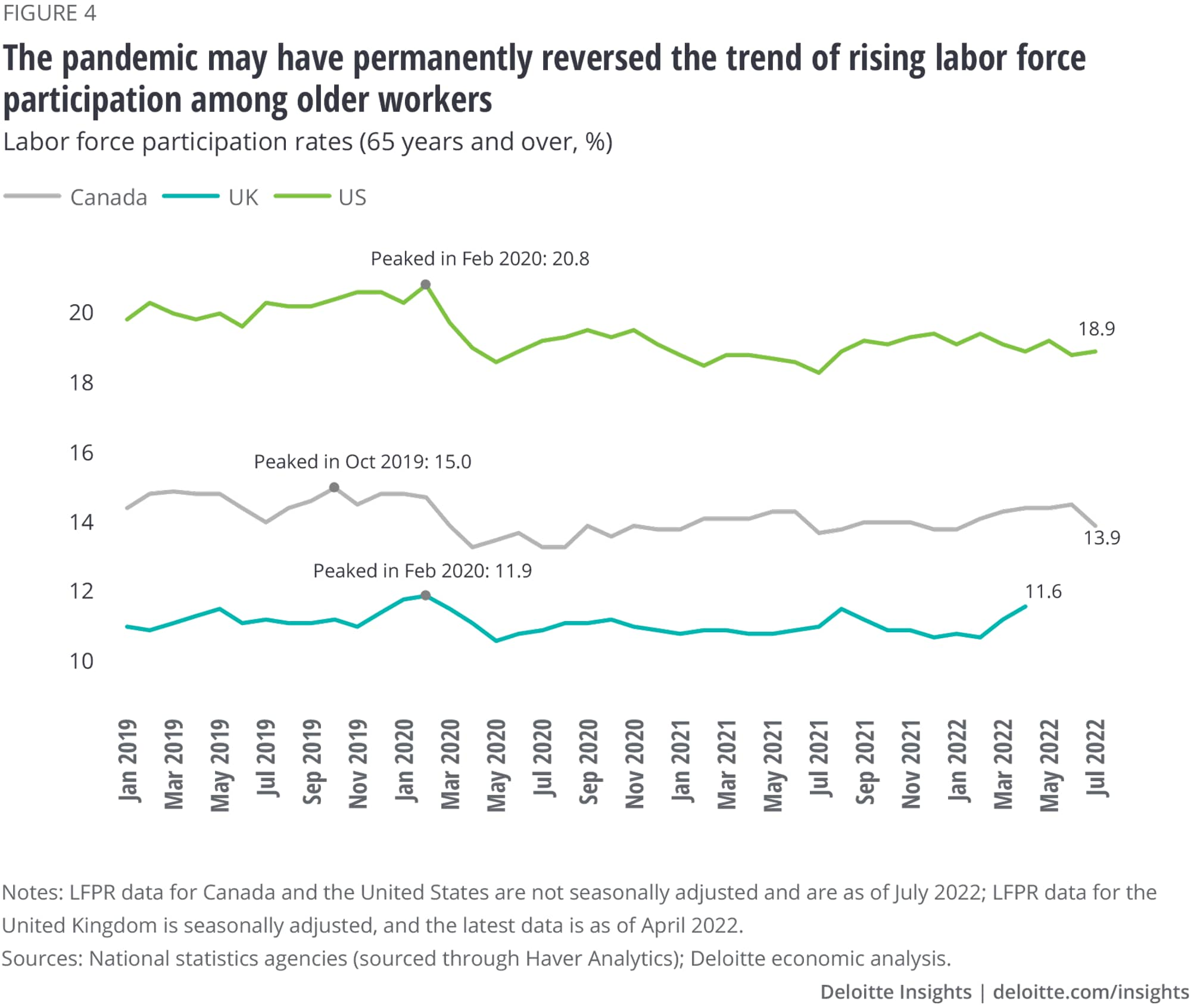

Even as the Canadian labor force growth gets a huge tailwind from immigration, it will continue to face similar constraints to labor force growth as the United Kingdom and the United States from its rapidly aging population. In addition to the strong growth in the number of people aged 65 and older, Statistics Canada notes that the number of people nearing retirement has never been so high—more than one in five (21.8%) working-age persons are aged 55 to 64.6 As figure 4 shows, the LFPR of those aged 65 and above is much lower than that of younger cohorts.

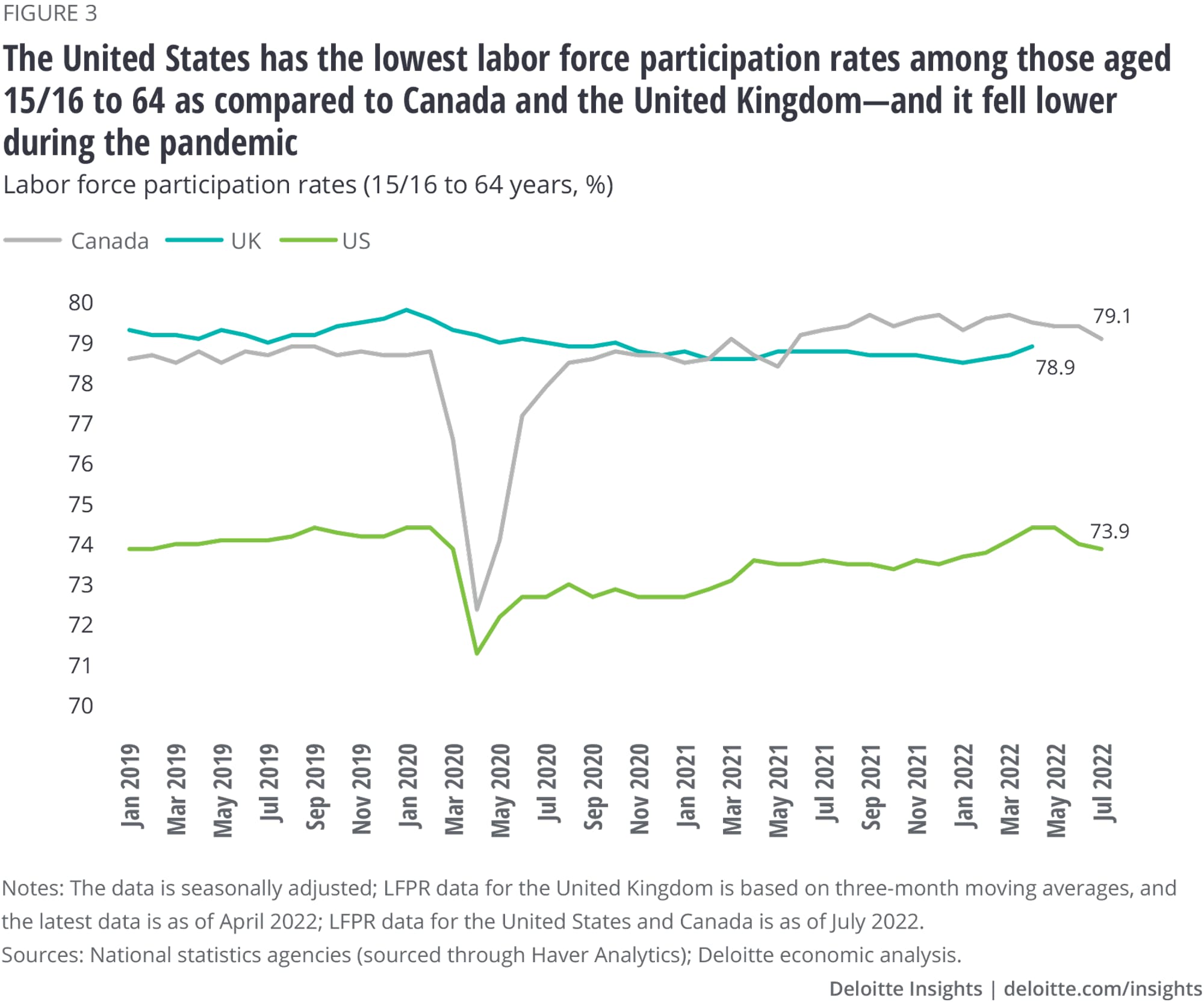

Aging of populations in these three countries impacts overall LFPR and looking at the trends in the 15/16 to 64 age group separately from the 65+ age group offers useful perspective. Figures 3 and 4 offer some interesting contrast—in particular, the United States has a lower LFPR as compared to Canada and the United Kingdom for the 16 to 64 age group (figure 3), but a higher LFPR among those aged 65 and older (figure 4). In the under 65 age group, the United Kingdom is below its prepandemic level, the United States is about the same as its prepandemic level, and Canada shows a higher level of participation (figure 3). The last few months have shown declines in the LFPR for this group in Canada and the United States; however, it is too soon to say if this is a developing trend.

Over the pandemic, the US labor market witnessed a surge in retirement, and this is evident in the decline in the labor force participation among those aged 65 and older (figure 4). And even if the pre- and postpandemic LFPRs of the 65+ age group are not much different for Canada and the United Kingdom, the aging of the populations will constrain labor force growth in the future.

The forces that resulted in slow growth in the UK and the US labor markets are unlikely to change—adjustments to the retirement patterns that emerged during the pandemic are likely to be long-lasting and immigration policy is a highly charged topic that will take years to resolve. The highly immovable trend of aging populations will likely lead even Canada into slower, if not negative, labor force changes in the relatively near future. Even if other factors such as “long Covid” and those who cited the need to drop out of the labor force to care for children7 are transitory, there are no easy fixes to increase the supply of labor.

It is highly likely that labor market pressures will ease in the near term as the impact of monetary tightening slows the pace of economic growth. Indeed, this easing may already be happening—the number of job openings and the job openings rate in the United States have dropped over the past three months.8 However, businesses would be prudent to keep in place the employee retention and attraction policies they have developed over this period of labor market tightness—in this situation, past is likely prologue.

{kind=link}

{kind=link}

{kind=link}

{kind=link}