The labor market is recovering but unevenly so has been saved

Cover image by: Jaime Austin

Amid all the conversations about inflation and its impact on economic growth, it’s easy to miss out on the bright spot that is the labor market. Since the trough of April 2020, the economy has added 21.5 million jobs, unemployment has fallen to 3.6%, and the employment-to-population ratio is edging back to what it was before COVID-19 hit American shores.1 The strength of the labor market, in fact, is a key factor aiding consumer sentiment at a time when worries about inflation and monetary tightening by the United States Federal Reserve (Fed) are rising.

The labor market recovery, however, hasn’t been even. Sectors like accommodation and food services, which suffered strong declines in demand from consumers and businesses in the initial months of the pandemic, are yet to return to prepandemic levels of employment. Others like professional and technical services, and retail trade have fared much better. That the recovery is uneven is also evident from analysis of data on employment by occupations—employment in high-wage occupations, for example, has fared better than medium- and low-wage occupations.2

While a steady shift in consumer spending from goods to services since mid-2021 will help in smoothening some of the unevenness in the labor market, inflation poses a major risk. A prolonged period of high inflation or a subsequent recession may not only dent overall employment but will also leave some sectors and occupations more vulnerable than others.

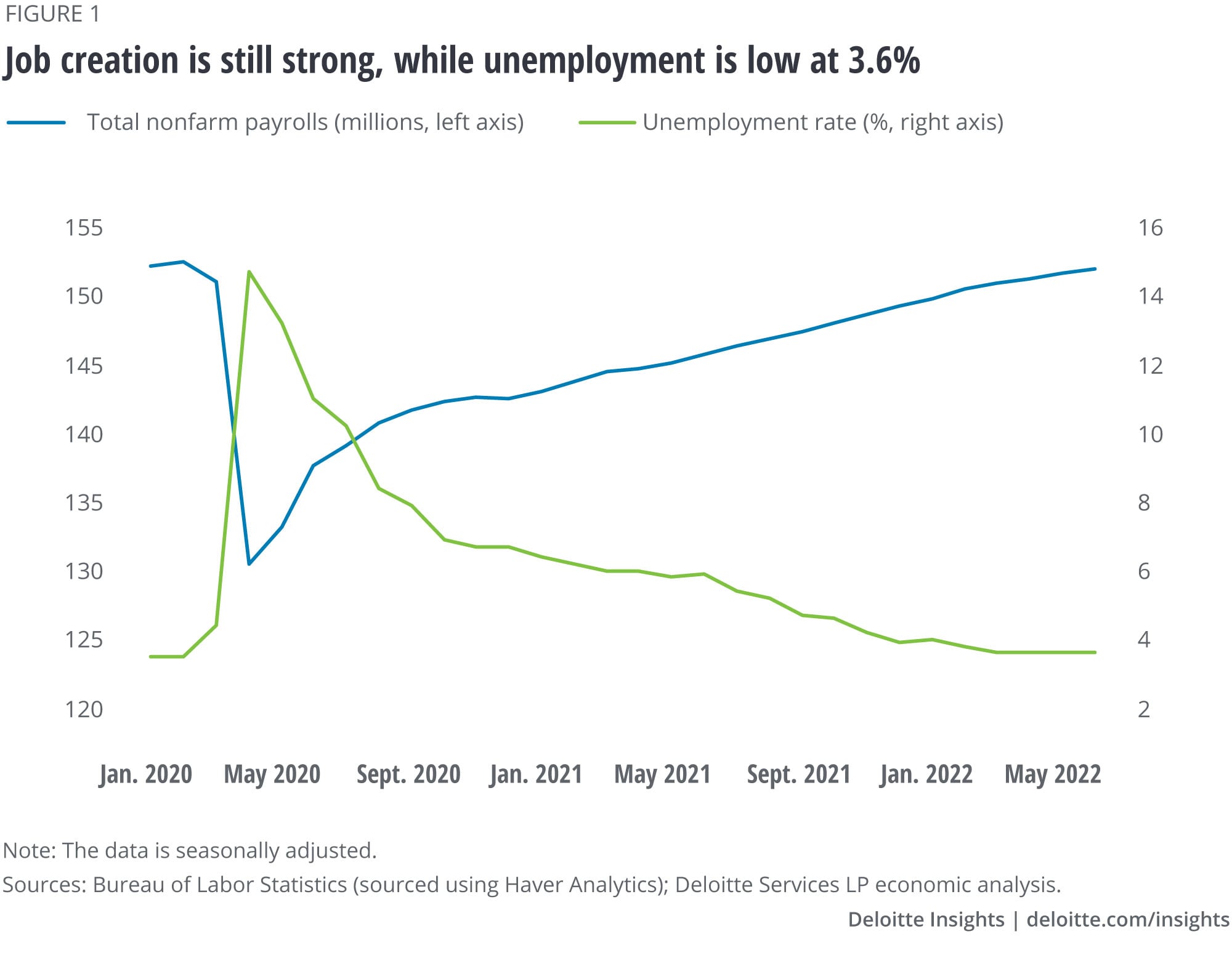

Between February and April 2020, as lockdowns, social distancing measures, and fears of COVID-19 spread, economic activity and employment fell sharply. Total nonfarm payrolls3 declined by 14.4% or close to 22 million during this period, the sharpest two-month decline ever recorded in the history of the series. Of the total decline in payrolls, 96% were in the private sector and the remaining were in government, mainly state and local. This isn’t surprising, given the overwhelming share of the private sector in the economy. However, as the initial shock of the pandemic faded and the economy reopened, the labor market bounced back. Payrolls have been steadily going up—16.4% between April 2020 and June 2022—with the pace of job creation still going strong (figure 1).

With payrolls going up, unemployment has fallen from its peak of 14.7% in April 2020 to 3.6% in June 2022. Encouragingly, people who had dropped out of the labor force in the early part of the pandemic have started coming back. The employment-to-population ratio at 59.9% is now just a little more than a percentage point below the prepandemic level. The surge in the labor market, along with shortages brought about by the pandemic, has led to strong growth in nominal weekly earnings (by 12.7% since February 2020), although rising inflation over the past year has reversed these gains in people’s purchasing power. Nevertheless, the labor market has been a key contributor to consumer confidence over the past year and continues to buoy sentiment despite high inflation, as is evident from Conference Board’s Consumer Confidence Index (figure 2).4

There’s still some way to go for the labor market to recoup all the losses of the pandemic. Given that some sectors are still below prepandemic levels of economic activity, they are yet to make up for the loss in jobs. Consequently, total payrolls in June were still 524,000 short of levels in February 2020.

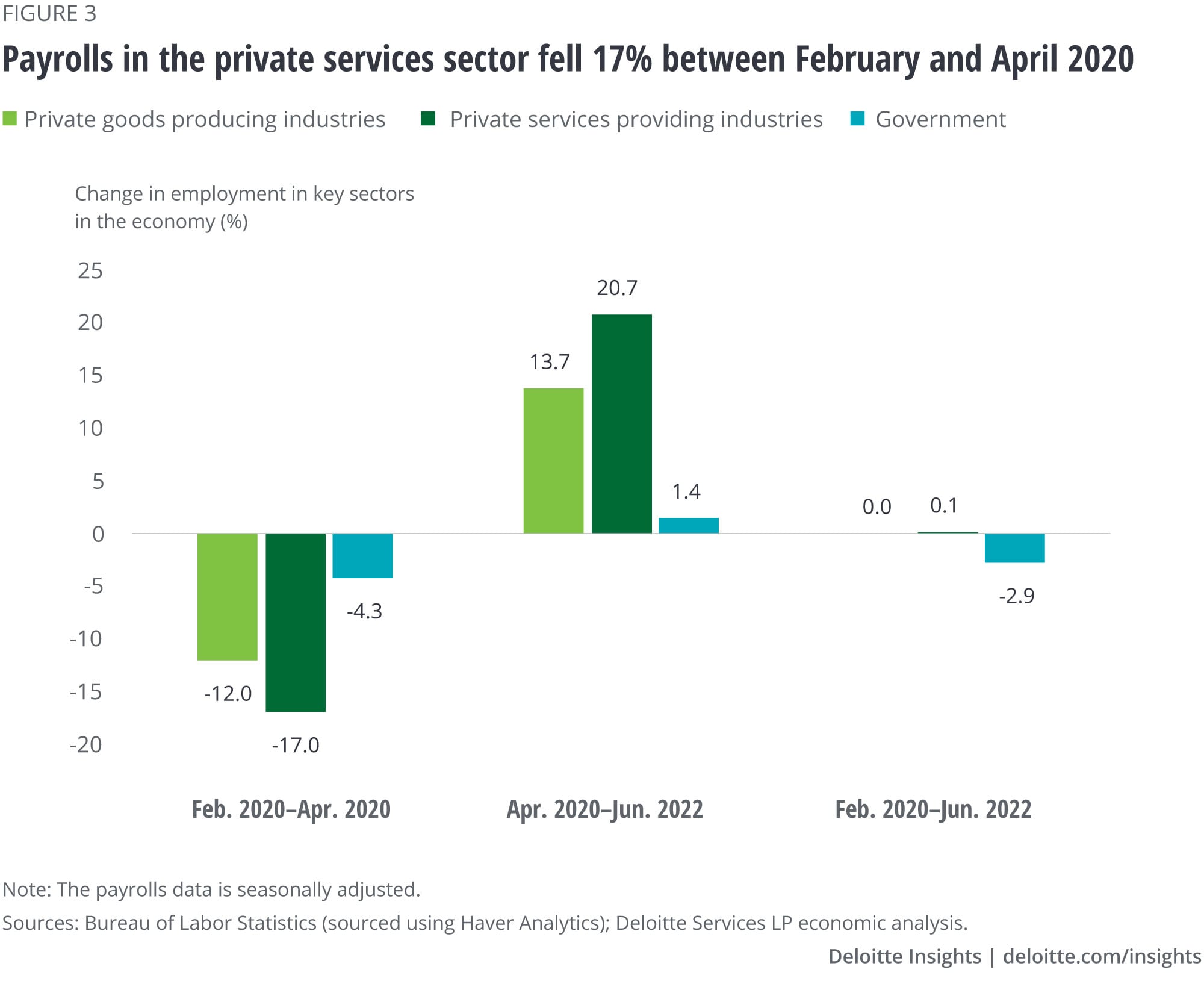

Neither the drop in employment in the initial phase of the pandemic nor the recovery after that has been uniform across industries. In the private sector, services were hit the hardest, with payrolls dropping by 17% between February and April 2020, higher than the corresponding 12% decline in goods producing industries (figure 3). Within services, the biggest setbacks in employment were in arts, entertainment, and recreation (51.7%) and accommodation and food services (47.7%), as social distancing measures and fear of COVID-19 kept consumers away. The dent to these sectors is also evident from national accounts data,5 with gross value added in arts, entertainment, and recreation dropping 58.7% between Q4 2019 and Q2 2020, while accommodation and food services fell 48% in this period. In fact, the US$6.9 million worth of job losses in accommodation and food services between February and April 2020 was the highest across all major sectors in the economy and amounted to more than 30% of total job losses during this period. Within goods producing industries, job losses were the most in construction (1.1 million) and durable goods manufacturing (0.9 million).

The decline in employment during this time would likely have been higher had it not been for strong fiscal support. Since the start of the pandemic, the federal government has disbursed US$6 trillion on a wide variety of support programs.6 These include various loan and grant programs (totaling US$1.4 trillion) to support businesses, such as Paycheck Protection Program, Grants for Restaurant, and Airline Industry support.7 Interestingly, among the major sectors and sub-sectors in the private sector, couriers and messengers were the only ones that saw a rise in employment between February and April 2020 (figure 4). This is likely due to the rise in demand for online purchases during that time, as many offices shifted to remote work and consumers stayed indoors due to health-related fears.

Figure 4 shows employment trends in key sectors within goods and services producing industries since February 2020, including the ongoing recovery. There are two interesting trends worth noting about the recovery. First, given the depth of the trough between February and April 2020 and the strong shift in consumer spending toward goods from services during 2020–2021, the level of economic activity and, hence, employment in certain sectors are still markedly lower than prepandemic levels. For example, employment in accommodation and food services is still 7.7% lower than levels in February 2020 (figure 4) with gross value added in the sector about 15.8% less in Q1 2022 compared to Q4 2019. Consequently, payrolls in accommodation and food services are still trailing its prepandemic level by more than a million; the sector, along with health care and social assistance, and other services, accounts for a deficit of nearly 1.4 million jobs compared to February 2020.

Second, some sectors have gained more than others during the pandemic, with payrolls now higher than prepandemic levels. Payrolls in professional and technical services, for example, are now 7.8% higher than February 2020, which is not surprising given that gross value added in the sector was up by 11% in Q1 2022 compared to Q4 2019. Figure 4 also shows the strong surge in employment in transportation and warehousing and its key sub-sectors. This is likely due to rising e-commerce purchases as remote work and fears of COVID-19 meant that people turned more toward online purchases than they used to before the pandemic. Ecommerce sales excluding food services grew 3.3% (quarter-on-quarter) on average between Q2 2020 and Q1 2022 compared to 0.4% growth in the preceding eight quarters.8

Among the 23 major occupations, only one—computer and mathematical occupations—saw a rise in employment between February and April 2020. The sharpest declines were in low-wage occupations such as food preparation and serving (-48.8%) and personal care and service (-44.2%). This is likely because these occupations couldn’t easily shift to remote work and hence, were affected more than those like computer and mathematical occupations. Overall, low- and medium-wage occupations fared much worse than their high-wage counterparts during this period (figure 5).

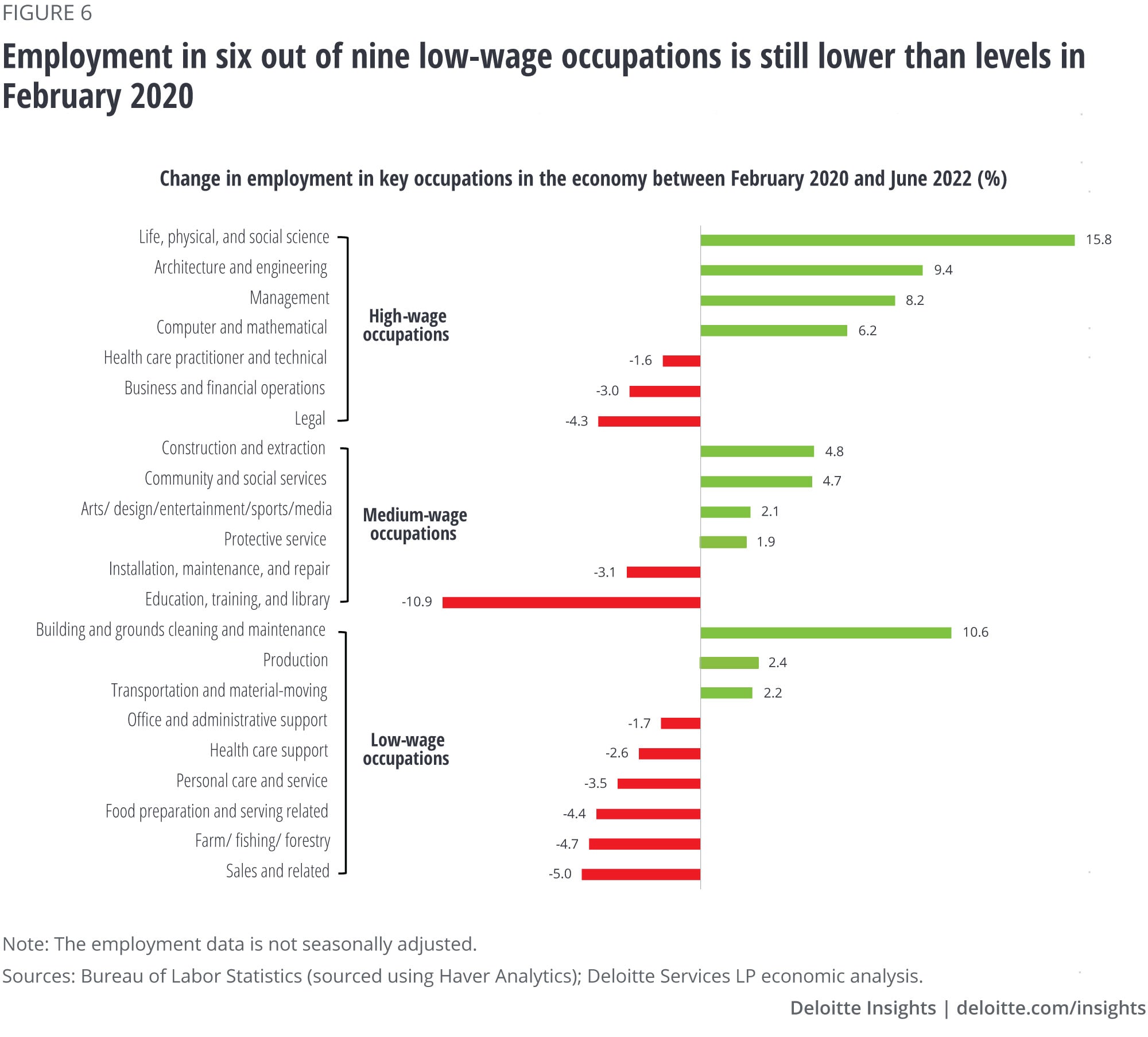

Employment in all occupations has, however, been recovering steadily since those initial months of sharp setbacks. The pace of recovery has been highest for low-wage occupations, given the deep trough between February and April 2020 and the revival in certain services like food services, travel, personal care, and health care support as the pandemic eases in severity. However, even then, employment in low-wage occupations in June 2022 was still 0.9% lower than levels compared to a 3.8% increase in high-wage occupations (figure 5). Figure 6 shows that six of the nine low-wage occupations are still witnessing levels of employment below what it was in February 2020. Contrast that to high-wage occupations where three out of seven occupations have employment below prepandemic levels as of June 2022.

The strong pace of jobs growth isn’t likely to continue even if economic growth remains healthy because unemployment is currently low, and the participation rate is edging close to levels before COVID-19. For example, in Deloitte’s baseline forecasts (55% probability), even with a forecasted growth of 2.2% in 2023, average monthly payrolls growth is expected to decline to 95,000 from about 423,000 this year as the economy moves closer to full employment levels.9 The risk to this scenario, however, is from inflation. Rising prices have offset strong growth in nominal income since last year, thereby denting consumers’ purchasing power. Since December 2020, nominal weekly earnings have gone up by 6.6%, yet real earnings—nominal earnings adjusted by inflation—have fallen by 5.6%.

If high inflation persists, the reduction in purchasing power may force consumers to cut down on a swathe of discretionary spending.10 This, along with monetary tightening, has the potential to slow economic activity and hence, employment growth. And a period of high inflation or a recession may make it even worse. It will likely also thwart gains made so far in sectors and occupations that are yet to reach prepandemic levels of employment. That will be worrying for those in low-paying jobs compared to others. Inflation is already hitting those at the lower end of the income ladder the hardest; the last thing they would want is a faltering labor market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}