The (true) cost of a low-carbon future has been saved

Cover image by: Jaime Austin

Success in limiting greenhouse gas emissions is necessary for the future of our planet and humanity. But success in limiting greenhouse gases is likely to be accompanied by weak measures of economic growth and productivity. As the world moves toward sustainability, measured living standards in the United States and other countries are expected to fall or grow more slowly than in the past. But don’t be fooled. While the move to clean energy will not be free, much of the supposed “cost” is an artifact of how our economic data is constructed. The real story will be coming to terms with the fact that, today, we are living beyond our means. And in the future, we intend to live within them.

The “Inflation Reduction Act” puts the US government in the position of spending heavily to convert the US economy to a low-carbon future. In that, it joins Europe—and, likely, a growing group of countries around the world. Many people are going to be watching to see how policies that limit carbon emissions affect the economy. How do electric vehicles, renewable power, and perhaps less travel and overall energy use affect people? Is all this effort worth it? Current economic data may not really provide an accurate description of how this shift impacts the standard of living over time.

The National Income and Product Accounts are designed to be comprehensive measures of economic activity. However, by convention, some things are excluded from the calculations. Nonmarket production—for example, the production that takes place within households—is not counted. So, your dinner preparations, child care, and housecleaning aren’t part of GDP. And nonmarket costs that might subtract from the value of production are not included. Pollution is a classic example of a nonmarket cost. Greenhouse gases are, of course, a form of pollution.

This is not a conspiracy and doesn’t happen because economists are blind or biased (well, mostly not). The problems are well known, and they are addressed in any introductory macroeconomics textbook.1 Why not revise the comprehensive production measures we use to solve these problems? The answer is two-fold: Refining economic measurement to correctly include nonmarket production and costs may not be necessary for many of the purposes of this data—for example, for measuring business cycles. And our measurement system uses market valuations to compare and add different activities. It’s hard to set a price on nonmarket activities.

Greenhouse gas emissions impose costs that aren’t paid for through the market, most of which will be felt in the future. Just how much do greenhouse gases cost? In other words: How much is GDP overstated because it fails to include the cost of greenhouse gas emissions?

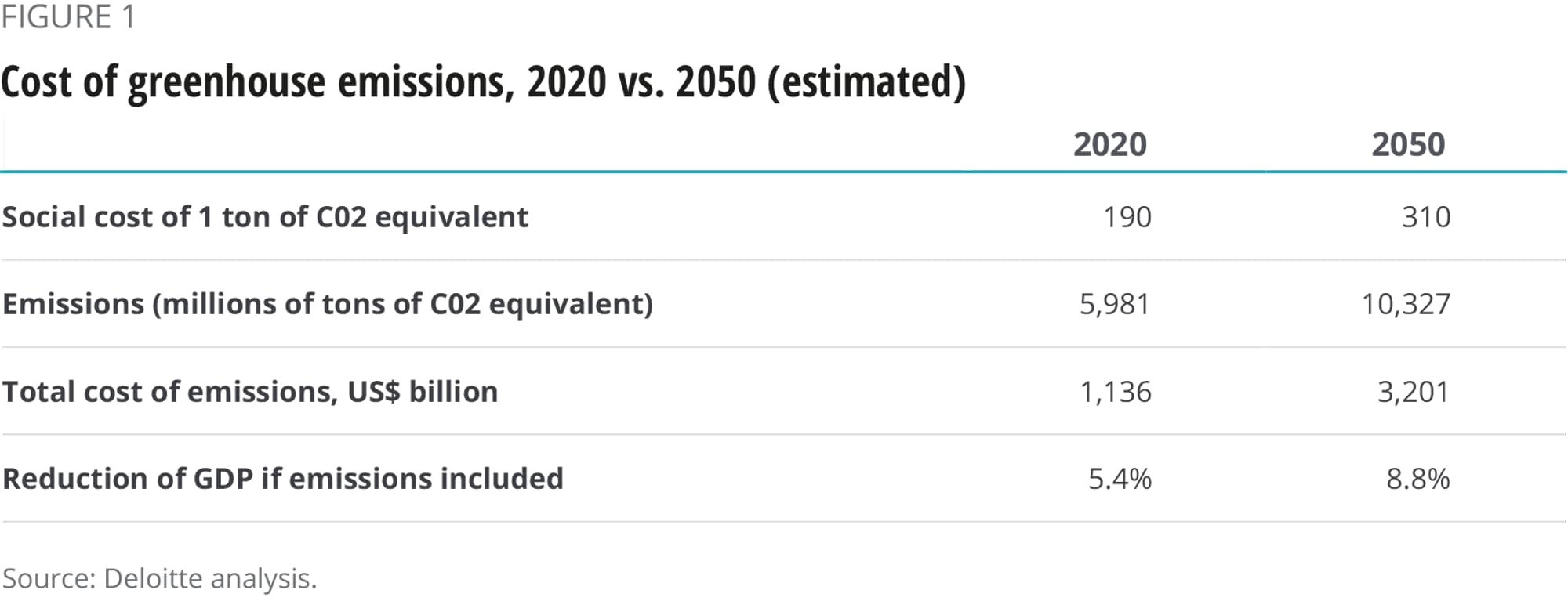

Figure 1 shows an accounting for the value of greenhouse gas emissions in 2020 and a projection of the cost in 2050.2

Figure 1 shows that our measures of GDP may be significantly higher today than they would be if we incorporated the cost of carbon correctly (that is, subtracted the social value of carbon emissions from GDP). And over time, the cost rises, suggesting that—absent any policy change—a measure of GDP growth that includes the cost of greenhouse gas emissions would be lower than GDP growth estimated using current methods, which take no account of those emissions.3 So official GDP is overly optimistic about our current level of production, and likely to be overly optimistic about how fast the economy grows in the future.

The overestimation of GDP and national income leads to two further problems:

Lower-measured GDP growth as the economy adjusts to a low-carbon-output world will therefore show up in the form of lower labor productivity growth, a decline in the return to capital, and a fall in corporate productivity. To be clear, correctly measured, these metrics may not necessarily slow (and may even accelerate). But official data, if it continues to reflect current methods, will show a slowdown in labor productivity growth. This will create an impression that the economy is performing poorly. Analysts—and, more importantly, citizens—will have to be aware of this problem to avoid being misled about the impact of climate change remediation.

The problem goes beyond official data. Businesses will experience declining profitability even as they make large investments in plant and equipment to reduce greenhouse gas emissions. But at least some of the decline in profitability will actually reflect the correct internalization of the costs of greenhouse gases. The real problem is that, in the past, profitability—ignoring the costs of greenhouse gas emissions—appeared higher than the true level. The earlier high profitability, however, while coming in the form of actual cash, was really something of a mirage since businesses did not pay the full social costs of production.

Another related problem involves valuing the capital stock. Much of the world’s existing capital—buildings, machines, and even knowledge—was created based on ignorance of the true costs of climate change. As those costs become internalized, existing capital will prove to be less valuable than users had believed. In essence, capital depreciation is likely to be very fast over the period of adjustment to a world of reduced greenhouse gas emissions. The depreciation will be an artifact of the speed and types of policies taken and represents movement from a false overvaluation of capital to the true, lower valuation that takes into account the cost of climate change.

One example—albeit slightly extreme—is the much-debated possibility of a reversal of the Gulf Stream. By one estimate, this could lower the average temperature in the United Kingdom by 3.4 degrees (Celsius).4 That would require retrofitting much of the stock of buildings in the country to continue to be useful in the colder climate, essentially reducing the value or depreciating the unretrofitted capital stock and requiring a huge investment simply to keep the capital producing at the current level.

Something similar happened on a smaller scale when oil prices tripled in the early 1970s. The global capital stock, which had been built under the assumption of cheap oil, essentially depreciated suddenly because it was no longer as profitable as it had been. Over the next decades, older capital (for example, “gas guzzling” automobiles) was replaced with newer, more energy-efficient capital, and very likely at a faster rate than had the oil shock not occurred.

The world’s adjustment to reduced greenhouse gas emissions is likely to be messy and controversial. Misleading data could make the debate even more difficult. Policymakers and citizens will need to interpret economic data carefully over the coming years.

Expect the following:

Unfortunately, the debate over climate change and the need to reduce greenhouse gas emissions has incentivized a small number of analysts to provide intellectual support to those who do not wish to accept the lower profits and economic change required. Those analysts are likely, over the next decade, to point to lower GDP growth, low productivity growth, and low profitability, as reasons why the United States should reverse the measures to fight climate change, like those in the Inflation Reduction Act. Astute observers should realize the weaknesses of the data underlying these arguments and recognize that the methods we’ve used in the past to measure the economy haven’t taken the cost of climate change into account.

{kind=link}