At the most recent Central Economic Work Conference, policymakers identified three chief economic difficulties: weakening demand, supply chain shocks, and subdued expectations.33 If weakening demand is to be reversed, private investment must be jumpstarted while revenge consumption is needed. Supply chain stabilization is about improving the business environment against a geopolitical backdrop fraught with areas of contention. In concrete terms, this is about outcompeting other investment-led markets such as the ASEAN region and India, which may benefit from investment moving away from China. The good news is that financial investors’ expectations have significantly improved since the second week of November,34 thanks to the relaxation of COVID-19 restrictions and stepped-up policy support to the ailing property sector. Relaxing COVID-19 management controls is not only about demonstrating policymakers’ capacity to weigh the acute trade-off between economic growth and public health, but it is also a powerful move to dispel investor doubts about the priority of economic development as part of China’s overall policy agenda.

The main risk faced by consumers remains the uncertainties stemming from the property market, not because the sector presents a systemic risk (the Chinese government has the means to prevent such risk), but because consumers might increase their savings if they do not see much upside to holding real estate as a financial asset. Encouraging a rise in homeownership without stoking a housing bubble becomes the key challenge.

The long-term solution is for local governments to move away from relying on land sales as their main source of revenue, but such a shift could only be made gradually under the precondition of developing a viable municipal bond market. In the short run, a stable housing market will be necessary. In practice, this means support to complete unfinished projects, incentives for healthy developers to increase investment, and industry consolidation. This is a tall order, but liquidity has returned to offshore US dollar bond markets within a short period of time on the back of a slew of policy support from liquidity injections, debt issuance, and revived equity listing options.35

Assuming the property market stabilizes, stronger property developers will emerge on the back of further policy support and the People’s Bank of China's accommodative monetary stance. With the Fed heading to the final innings of its tightening campaign, China's monetary easing certainly faces fewer constraints. This is particularly true as the USD/CNY hovers around 7.0, compared to 7.3 two months ago.

We think a focused approach of promoting consumption and continued accommodative monetary stance are likely while a major fiscal stimulus would be ruled out in 2023. However, the biggest hurdle remains reviving private investment beyond the property sector. That is why the Central Economic Work Conference prominently emphasized the role of the private sector.36 Platforms were singled out for their key roles in helping Chinese companies develop and internationalize their operations. We anticipate that concrete measures will be unveiled following such signals, such as the tutoring sector being rehabilitated. The underlying point is that policymakers appear to have a sense of urgency to boost consumption and private investment as external demand could face a more challenging environment in 2023. All in all, we see 2023 GDP growth narrowly exceeding our original forecast of 4.5%.

India

Rumki Majumdar

We step into 2023 with continued uncertainties in global geopolitics and the world economic outlook turning less favorable. Amid chaos and anxiety, India’s economic outlook remains optimistic for this year and the next. Of course, growth may not be touching the numbers we had expected this time last year, but who knew then that the world would witness a series of shocks one after the other.

India’s economy has outperformed numerous economies over the past year. India’s equity market performance, the strength of its currency, and the foreign reserve cushion have done fairly well, compared to its emerging-market peers.37 In the growth-inflation dynamics, India is way ahead in growth among its peers, but inflation is a concern.

Economic indicators point to resilience of the domestic economy, even as the rest of the world sees an economic slowdown. Private sector balance sheets have improved over the past couple of years. This implies that the private sector can boost capex as and when the investment cycle picks up. Corporate deleveraging has also improved banks’ balance sheets, aiding the banking system to come out of the asset quality cycle.

High tax collections give the government ammunition to spend and cushion the impact of the impending global slowdown. Consumer demand remains strong, especially among the affluent, as is evident from the retail industry and the better profit performance of consumer discretionary goods companies in recent quarters.38 A strong rise in labor force participation and jobs points to a resilient labor market.39

What is interesting is that some global headwinds have played to India’s advantage. For instance, geopolitical developments are influencing trade relationships and disrupting supply chains. Nations and multinationals are emphasizing resilience, diversification, and self-sufficiency.40 India has huge potential as an export hub and investment destination in light of the China Plus One strategy, especially in the manufacturing and services sectors, where it has competencies and comparative advantage.

India’s recent trade agreements have aimed at integrating the manufacturing sector with the global supply chain while attracting investments in sectors that are expected to drive long-term growth.41 Consequently, there has been a healthy rise in FDI equity flows from Japan, Singapore, the United Kingdom, and the United Arab Emirates in H1 FY2022–23, even as FDI from the United States has fallen. If the trend continues, investment from these destinations will exceed numbers from last year, which was among the strongest on record. The destination sectors have also diversified, with infrastructure, non-IT services, and chemicals witnessing ample inflows. This shows that globally, there is rising confidence about investing in India.42

Low asset values have also allowed healthy companies to consolidate positions and enter new segments. A record number of M&A deals were registered in 2022 with the biggest transactions seen in the banking, infrastructure and materials, and aviation industries. Many conglomerates entered new businesses, while brick-and-mortar companies partnered with technology firms.43

Despite the relatively good economic news, the path ahead will still come with challenges. First, although we believe that inflation has peaked, it is expected to persist for longer, due to relatively high oil prices, a stronger US dollar, and supply chain interruptions in certain industries. Further, a relatively stronger economic recovery may add to the inflationary pressure.

Second, aggressive tightening of monetary policies across the central banks of advanced economies is resulting in a slowdown across major economies this year. This could impact domestic investment and consumer demand as the proclivity to save increases. Tighter liquidity conditions may also result in capital outflows and a rising imbalance in the balance of payments.

Third, job creation has improved lately but not to the extent that wage growth is running ahead of inflation. Opportunities and wage growth remain low, impacting the low- and middle-income populations. The government’s focus has rightly been on sectors that create jobs for workers across all skills, such as infrastructure, construction, and manufacturing. However, the services sector has huge potential as it contributes to 55% of GDP. India also has the competency and a comparative advantage in a few services such as IT and IT-enabled services. Yet, the service sector generates slightly more than a third of total employment.44

We believe the path to recovery will be resilient even if it is longer than previously anticipated. Investments will likely be a key driver of growth, primarily thanks to the government sector’s capital spending. However, the private sector may take some time to join the investment bandwagon. Given that the economy turned out to be weaker in H1 FY2022–23 than we had anticipated, we have revised our outlook. India is likely to grow in the range of 6.5–6.9% in FY 2022–23 and 5.8–6.3% in FY 2023–24.45 Inflation will come down but remain above the Reserve Bank of India’s comfort level.

What will be critical is to stay prepared for the time when the global economy recovers. India must do what it takes to keep the economic fundamentals strong; it will not only help the country stay ahead of its peers in the investment race but, will also aid in a quick economic rebound when uncertainties subside.

Australia

Stephen Smith and Lester Gunnion

Like central banks in other advanced economies, the Reserve Bank of Australia (RBA) raised interest rates sharply through 2022 to quell an acceleration in inflation. However, with the high likelihood that inflation has already peaked, Deloitte Access Economics’ view is that any further increases in the cash rate are likely to unnecessarily tip Australia into recession in 2023. That forecast is dominated by the outlook for two important components of the economy—household consumption and dwelling investment. Both remained remarkably resilient throughout 2022 but are likely to weaken dramatically in 2023.

Real consumer spending has outpaced the wider economy. Recent gains have been fuelled by pent-up demand for travel. But this isn’t expected to last. The outlook for consumer spending has softened as high inflation and rising interest rates combine to add to cost-of-living pressures. Further, the full impact of the RBA’s current interest rate hike cycle is yet to be felt in the form of larger monthly mortgage repayments by households. Falling dwelling values are also weighing on household wealth.

Meanwhile, measures of consumer confidence have fallen to the lows experienced during lockdowns in 2020.46 The tight labor market is likely to continue to support nominal wage gains, but real wages are likely to remain under pressure. Growth in consumer spending through 2023 is highly likely to be much slower than in 2022.

Australia is also experiencing the fastest housing market correction since monthly records began in 1980. Sharp rises in borrowing costs from mid-2022 have reduced the amount homebuyers are willing and able to spend on new dwellings, with the value of new lending falling to its lowest level since late 2020. Weaker prices have hurt investment as developers typically respond by building fewer dwellings. The number of dwelling units approved—a key forward-looking measure of building activity—fell at double-digit rates over the past year, and building approvals remain around one-third below the peak seen in early 2021.47

The softer outlook is yet to materially ease the pressure on the residential construction industry caused by bottlenecks in the supply of labor and materials. Steel and timber shortages are persisting and upward pressure on wages is adding to labor costs, while wet weather and COVID-19–related absences are disrupting activity and prolonging construction timeframes. This has contributed to a 20% increase in the cost of building a new house over the past year, while the cost of building other residential dwellings has increased by almost 10%.

Housing also remains the largest source of inflation, contributing around one-third of price growth on average over the last four quarters. More recently, as inflation in residential building costs has decelerated, higher household gas and electricity bills have contributed more strongly to growth in the consumer price index (CPI) for housing. Outside of housing, inflation continues to be predominantly driven by goods rather than services, with prices of the former growing at more than twice the rate (9.6%) of the latter (4.1%) over the year to September 2022.48 Indeed, Australia’s inflation continues to be largely imported, with import prices growing 18.7% over the year to September 2022. However, business inventories have normalized from pandemic-era disruptions and indexes of shipping costs are consistently falling. Softening global demand will also provide space for supply to catch up. Inflation likely peaked over the year to the December quarter of 2022 at around 7.8% and will likely slow—although gradually—through 2023.

There are also some clear positives for the Australian economy. For one, the labor market is in extraordinarily good health. There are more than 200,000 fewer Australians unemployed now than before the onset of COVID-19 in February 2020 and the unemployment rate sits at just 3.4%.49 The underutilization rate, which captures both those wanting work (the unemployed) and those wanting more hours of work (the underemployed), has fallen to its lowest point since the early 1980s. However, the rapid, postlockdown growth in the labor market seen over the past year is nearing its end, with evidence of a turning point showing up across several indicators. The pace of employment increases has slowed and indicators of labor demand, job vacancies, and advertisements have started to decline. Going forward, employment is expected to grow through 2023, although at a declining rate. However, the unemployment rate is expected to rise slightly in 2023 as the labor force grows faster than total employment.

Second, commodity prices have remained higher for longer than expected, providing a welcome boost to Australian exports, business profits, and government budgets. The value of Australia’s goods exports rose in the latter half of 2022, despite the slowdown in the global economy and weather-related disruptions at ports in eastern Australia. That’s because the war in Ukraine continued to affect global supply chains and place upward pressure on prices for Australian food and energy exports. However, these windfall gains were always expected to be temporary. The correction in energy markets may be relatively slow, but lower prices are already flowing through to nonenergy commodity exports such as iron ore, coking coal, and other metals.

A combination of strong demand and higher prices has also added to the nominal value of goods imports. But the outlook for those imports has softened. The easing of price pressures is set to weigh on import values, while the forecasted slowdown in Australian consumer spending is expected to weigh on import volumes.

Japan

Shiro Katsufuji

We expect Japan’s economy to be on its way to a sustainable recovery through 2023. The recovery is partly aided by the complete lifting of COVID-19–related social restrictions last year, which lagged one year behind those of America and Europe, and partly because of the continuing accommodative monetary policy by the Bank of Japan (BoJ), while the other central banks in developed economies are taking tighter monetary policies to fight against inflation. As a result, we expect Japan’s real GDP to grow 1.7% in 2023, accelerating from an expected growth of 1.3% in 2022. Domestic personal consumption and business investment will lead the economic expansion as social mobility comes back, and government stimulus spending continues. In addition, corporate profits were at a record high in 2022. Semiconductor supply constraints are easing, which is good news for Japanese manufacturers. We also expect that the BoJ will maintain its Qualitative and Quantitative Easing (QQE) program through at least the end of 2023, given that the underlying consumer inflation rate is below the bank’s target of 2%.

Nevertheless, a few factors complicate the relatively optimistic outlook, and risks are weighted to the downside. To begin with, the robustness of Japan’s economic recovery is relative. The rebound from COVID-19–related social restrictions has been strong, but real GDP remains below its prepandemic peak. The momentum of this rebound will ultimately subside, bringing the growth rate back toward its potential, which is below 1%.50

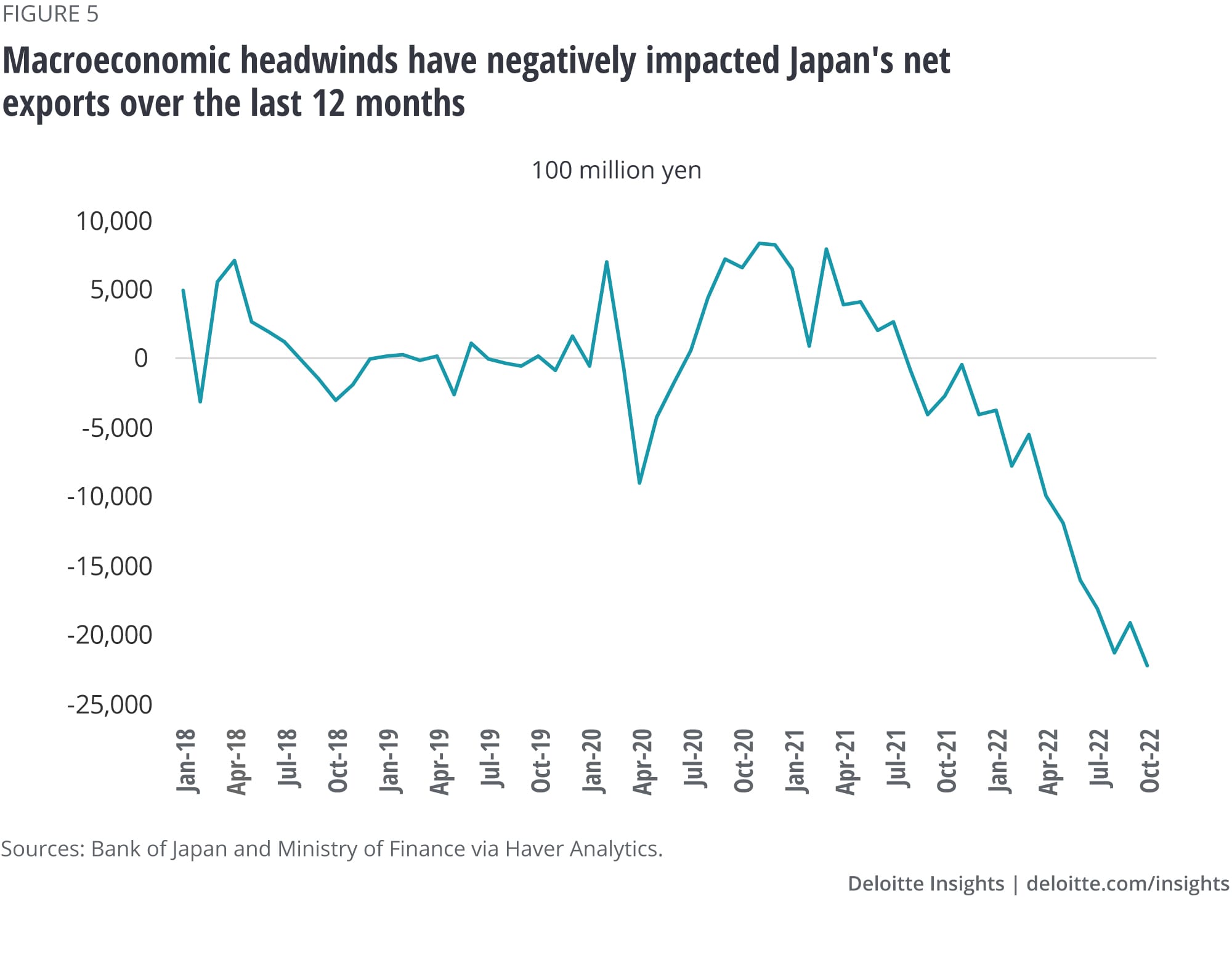

In addition, Japan’s economy is generally vulnerable to the rest of the world. The moderation of China’s economic growth and supply chain constraints have already affected Japan’s trade balance, which recorded negative net exports for more than 12 consecutive months (figure 5).51 If China’s economy deteriorates further, or if the United States or European economies go into recession, that may create more significant downward pressures.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}