The labor market braces for headwinds has been saved

The author would like to thank Patricia Buckley and Danny Bachman, US Economics, for their reviews and suggestions.

Cover image by: Sofia Grace Sergi

The labor market has been a bright spot in an economy jolted by high inflation and rising interest rates. Unemployment is low, and payroll growth is healthy, despite strong monetary tightening by the Federal Reserve (Fed).1 In fact, strength in the labor market is a key factor buoying consumer sentiment amid rising cost of living. The Conference Board’s consumer confidence index, which puts greater focus on the labor market than inflation,2 is still elevated relative to the historical average. Job gains have also translated to a strong increase in earnings since 2021. For low-wage occupations, a rise in wages goes a long way to bridge the wage gap with their medium-wage and high-wage counterparts.

However, the labor market is likely to grapple with three key concerns as the economy heads into 2023. First, employment in key medium- and low-wage occupations is yet to reach prepandemic levels. Any economic slowdown or, worse, a recession may create roadblocks to employment growth. Second, while average wages in the economy have gone up, not all occupations have enjoyed such an increase. Finally, even in occupations where nominal wages have gone up, real gains in wages have weakened or reversed due to high inflation.

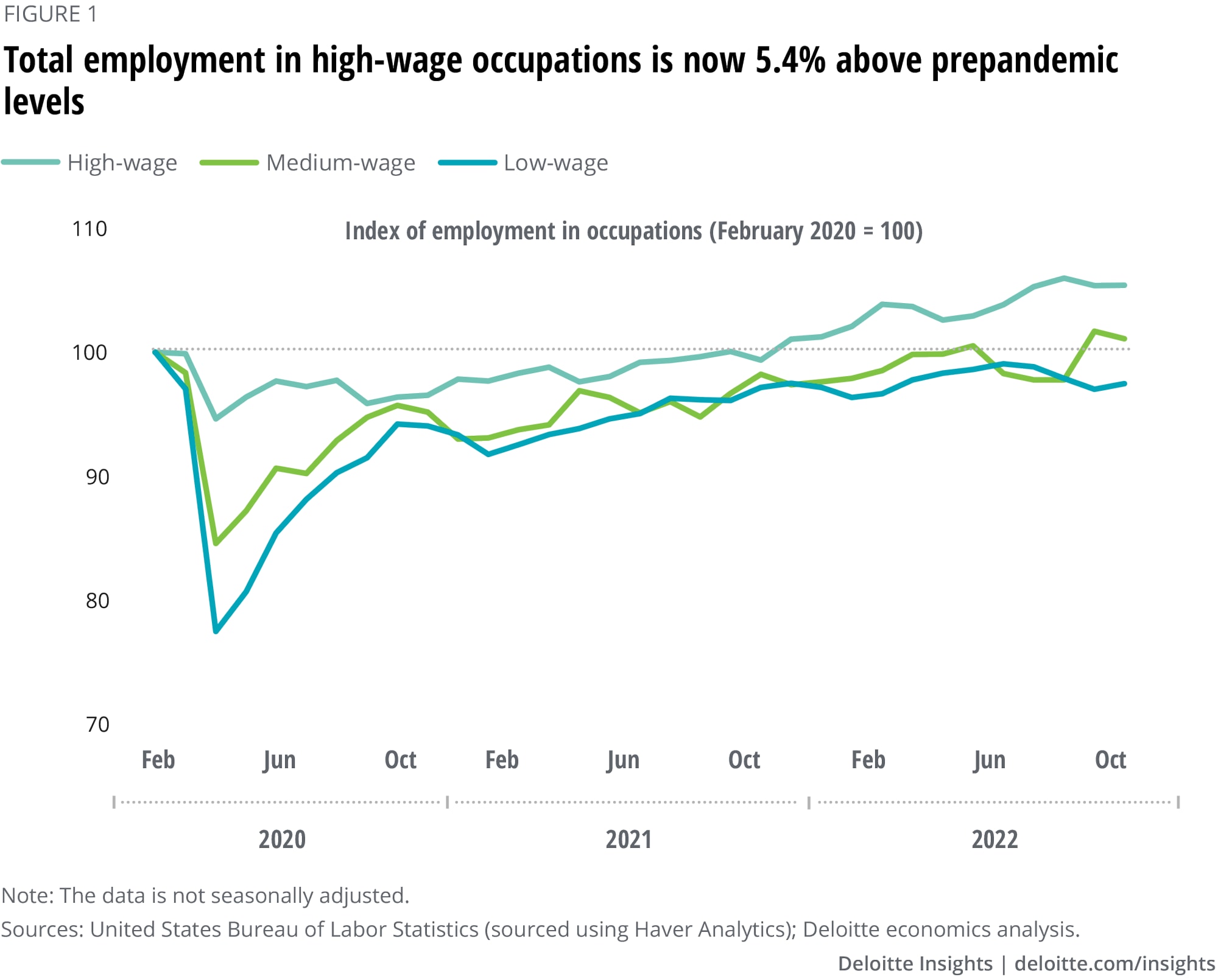

Employment, which fell by a staggering 16.1% between February and April 2020, has recovered steadily over the past two years. In September this year, total employment in the economy crossed its prepandemic peak before declining marginally in October. Yet, this recovery hasn’t been uniform.

Employment in low-wage occupations,3 taken together, has gone up at a faster pace than others since April 2020. This is not surprising given the steep decline in these occupations in early 2020 due to lockdowns and social distancing measures. Occupations like food preparation and serving, and personal care suffered the most during the initial months of the pandemic as businesses employing those workers could not shift them to remote work. In contrast, it was easier for high-wage occupations like computer and mathematical science to make the quick transition to remote work. As social distancing measures eased and vaccinations picked up pace in 2021, low-wage occupations recovered faster than others, reflecting the large initial decline.

Despite this sharp recovery, low-wage occupations have been lagging behind high- and medium-wage occupations. Figure 1 shows the trajectory of employment in high-wage, medium-wage, and low-wage occupations since February 2020. High-wage occupations crossed their previous peak 17 months after the trough of April 2020; total employment in high-wage occupations is 5.4% above prepandemic levels as of October 2022. In contrast, low-wage occupations are yet to return to their prepandemic levels.

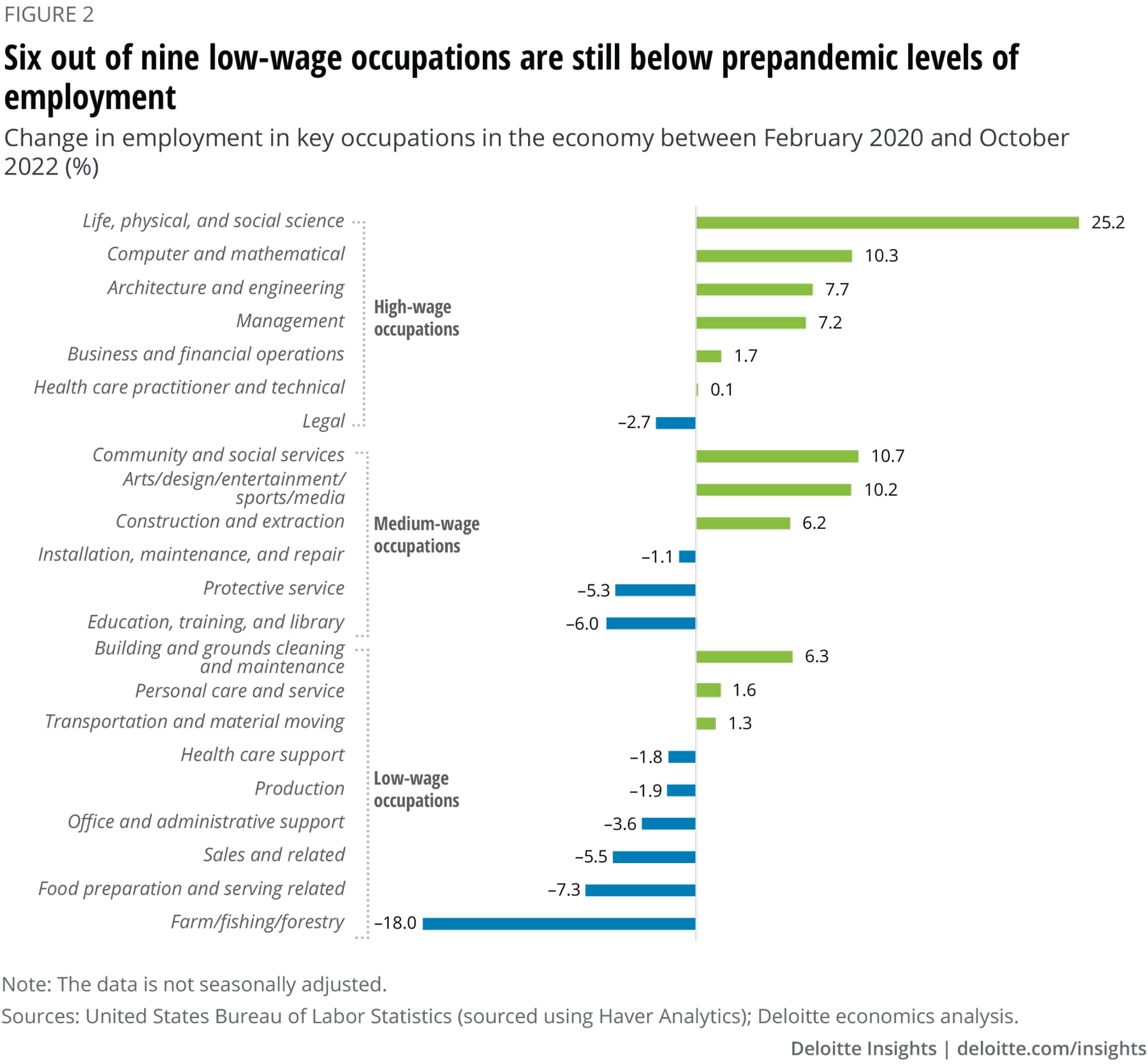

Within high-wage occupations, only employment in legal occupations is still lower than what it was before the pandemic. In contrast, employment in six of the nine low-wage occupations and three of the six medium-wage occupations is still lower than in February 2020. Figure 2 shows that some of the biggest gains in employment have happened in high-wage occupations. While life, physical, and social science occupations stand out in the sheer degree of employment gains (25.2% since February 2020), computer and mathematical occupations continue their trajectory of steady growth over the years. In fact, this was the only occupation that experienced growth in employment between February and April 2020.

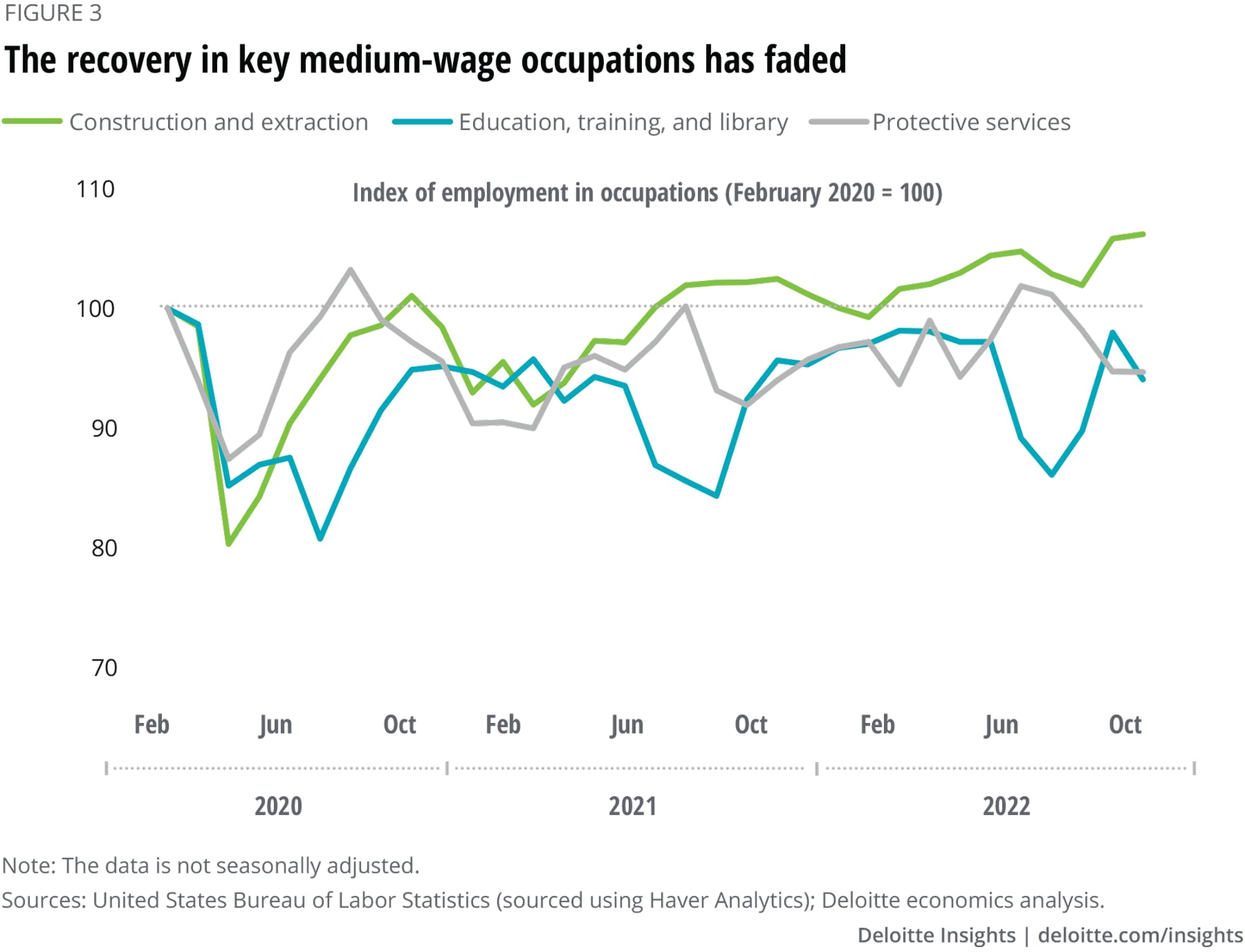

Within medium-wage occupations, education, training, and library occupations are down 6%, while protective services are 5.3% lower than prepandemic levels. The pace of recovery in these occupations has slowed this year, as figure 3 shows. In contrast, the recovery in construction and extraction occupations is still steady, with employment up by 6.2% since February 2020.

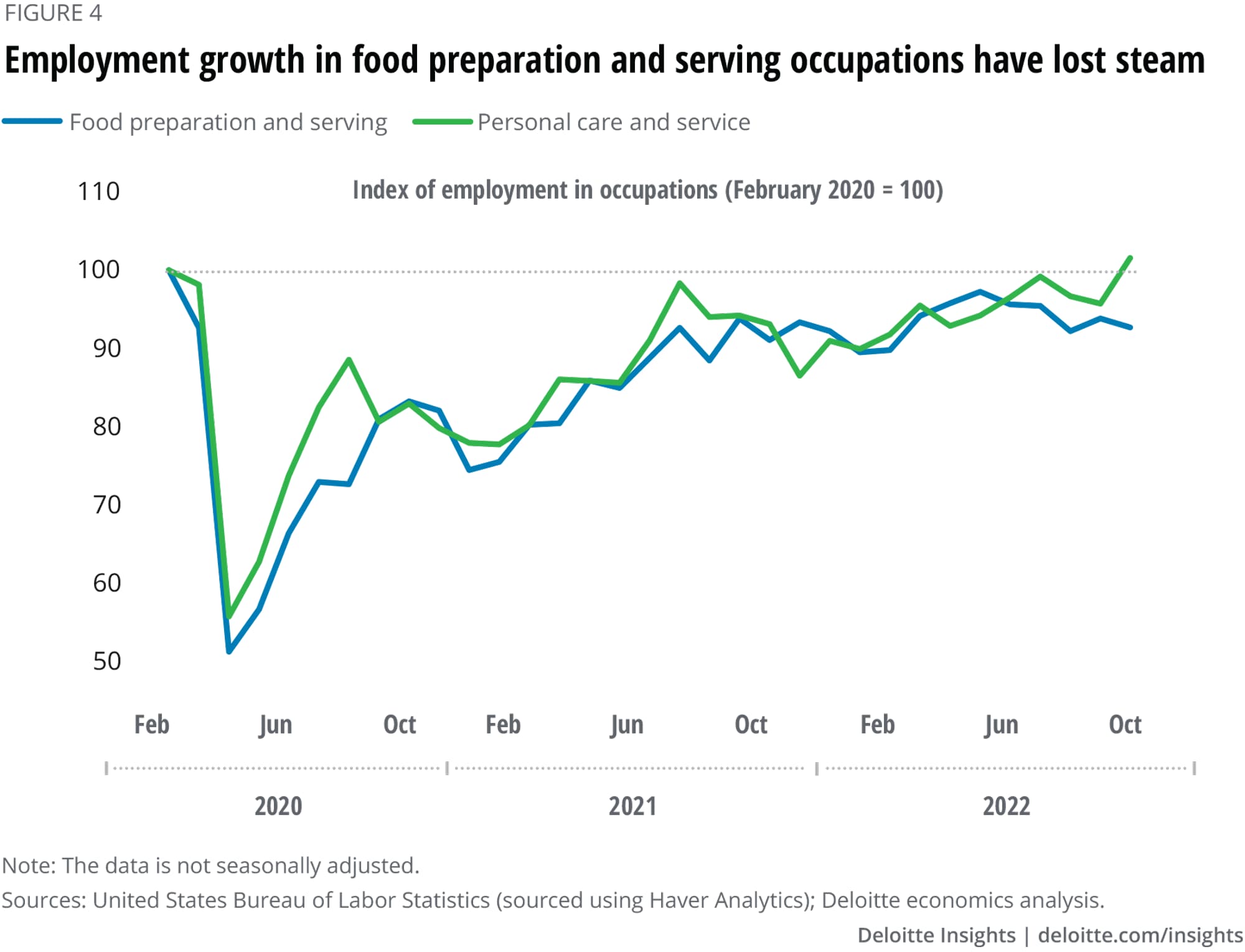

Among low-wage occupations, the recovery in employment in food preparation and serving seems to have fizzled out since May this year, despite a steady increase in consumer spending on food services and drinking places. Contrast that to personal care and service—an occupation that suffered as badly as food preparation and serving—where the recovery is gaining ground and employment is now 1.6% above prepandemic levels (figures 2 and 4).

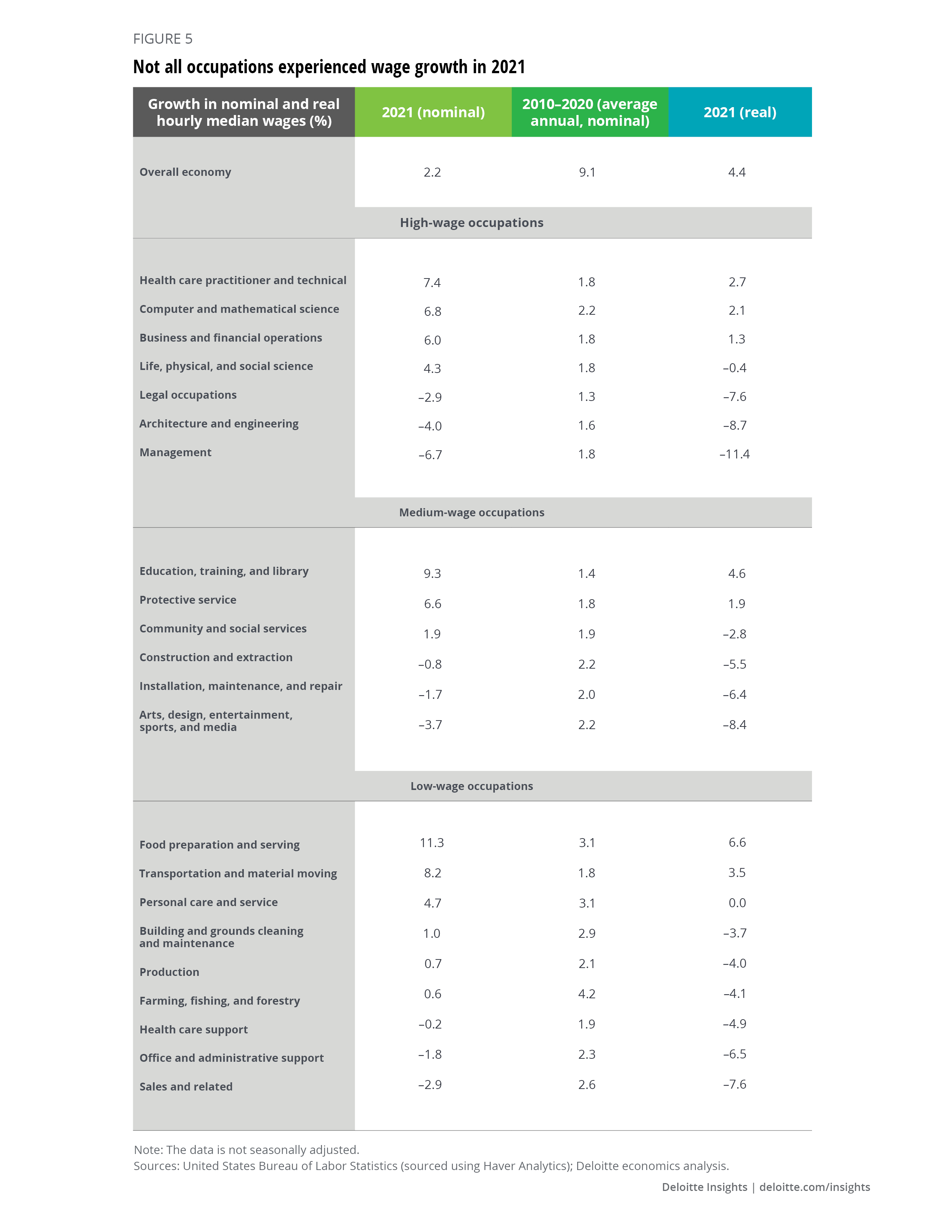

A strong labor market has led to robust growth in wages. Nominal average hourly earnings have gone up by 8.9% since the end of 2020. While monthly data on wages for occupations is unavailable, annual data from the Occupational Employment and Wages Statistics database shows a sharp surge in the economy’s median wage last year.4 Nominal median hourly wages for the economy went up by 9.1% in 2021, more than four times the average annual growth during 2010–2020. Interestingly, the sharpest rise in wages last year were in some low- and medium-wage occupations. As figure 5 shows, in food preparation and serving-related occupations, median hourly wages went up by 11.3% last year, followed by education, training, and library occupations (9.3%), and transportation and material moving occupations (8.2%).

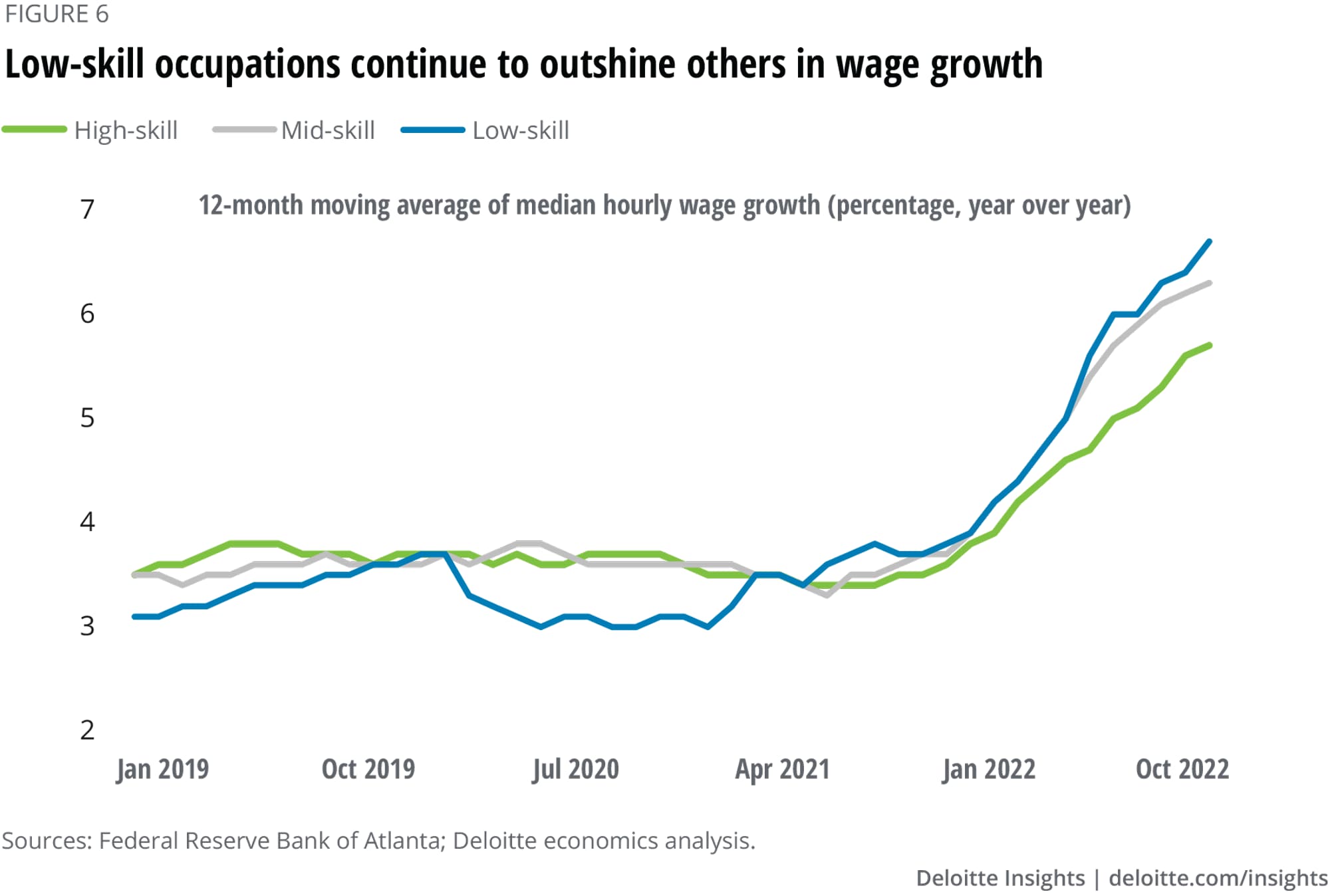

Data from the Federal Reserve Bank of Atlanta’s wage tracker suggests that the surge in wages for low-wage occupations has mostly continued in 2023.5 According to the tracker, median hourly wage growth in low-skill occupations6 continues to outpace wage growth in mid-skill and high-skill occupations (figure 6). Figure 6 also shows that across skill levels, wage growth since the middle of 2021 has been far higher than in the past few years.

However, two worrying trends have emerged. First, as figure 5 shows, median hourly wages declined for nine occupations in 2021, three of which were in medium-wage occupations and three in low-wage occupations. While the sharpest decline was in two high-wage occupations—management (-6.7%) and architecture and engineering (-4.0%), the decline in wages for other occupations works against bridging the income inequality gap. Second, high inflation has offset nominal gains in wages. Real median hourly wages,7 for example, declined for 14 occupations in 2021—four in high-wage occupations, four in medium-wage occupations, and another six in low-wage ones. That trend is likely to have continued into this year as inflation has remained relatively high. Real average hourly earnings, for example, have gone down by 2.4% so far this year, despite a 3.8% rise in nominal earnings.

While high inflation has dented real wages, the biggest threat to the labor market is from a slowing economy—more so for certain low-wage occupations that are yet to reach prepandemic levels of employment. For example, if consumers cut back on discretionary spending due to souring economic prospects, that may thwart the recovery in occupations like food preparation and serving, and sales. In certain sections of the economy, these risks are already taking shape. Housing is one example where housing starts and home prices have been falling as surging mortgage rates hit demand. Deloitte economists expect real investment in private housing to contract by 9.3% this year and by 8.8% in 2023, according to their baseline forecast.8 This will likely weigh on employment in construction occupations.

A recession, however, will make it much worse for the labor market. In Deloitte’s recession scenario—probability of 35%—average monthly employment for the economy is forecasted to contract in 2023 and unemployment to rise to 5% from 3.6% this year.9 For now, slower employment growth next year is the best one can hope for given current economic trends—a scenario that’s already playing on consumer sentiment. Consumers’ expectations of the future have fallen, even while their confidence about the present situation remains relatively elevated.10 Signals such as those are probably enough to keep economists awake at night.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}