Housing takes a hit, but fears of a repeat of 2006–09 are unfounded has been saved

Cover image by: Govindh Raj

As inflation reared its ugly head in the United States last year at a scale unseen since the 1980s, the monetary policy response was swift and strong.1 Between March 2022 and February 2023, the United States Federal Reserve (Fed) raised the federal funds rate by 450 basis points (bps), including four hikes worth 75 bps each. The speed and scale of the Fed’s response was unlike its previous bout of tightening between December 2015 and December 2018, which was more gradual. While strong tightening has brought down price pressures slightly—inflation fell to 6.5% in December from a peak of 9.1% in June—the move to thwart aggregate demand growth has arguably had its first casualty: housing.

Housing had been a bright star for the economy since the pandemic’s initial impact. After a sharp dent due to lockdowns and social distancing measures in March and April of 2020, housing starts picked up and grew 92.4% to their peak in April of last year.2 Existing home sales, too, grew sharply during this period.3 With demand rising, home prices also went up. However, policy tightening by the Fed last year to counter inflation led to a rise in long-term borrowing rates—mortgage rates doubled last year. Demand for housing, therefore, got hit. Starts are down by 23.4% from April 2022, while prices have eased. Does this mean that housing is set for a repeat of the crisis in 2006–2009? We don’t think so. While housing will feel the pressure of high mortgage rates this year, it will start recovering from 2024. And unlike the subprime crisis, which was primarily due to lax rules in the mortgage market, the current downturn is more a cyclical one.

Housing outshone most other parts of the economy after the initial impact of the pandemic. Between Q2 2020 and Q4 2021, real residential investment went up by 20.8%, far higher than the 13% rise in business investment during this period.4 In fact, within business investment, only investment in equipment grew more than residential investment during this period. This is also evident from housing starts, building permits, and home sales. After a hiccup in early 2020, housing starts went up to a seasonally adjusted annual rate of over 1.8 million units by April 2022. It’s not just new housing that benefited after the initial wave of COVID-19. Sales of existing homes grew 59.5% between May 2020 and the recent peak of January 2022.5

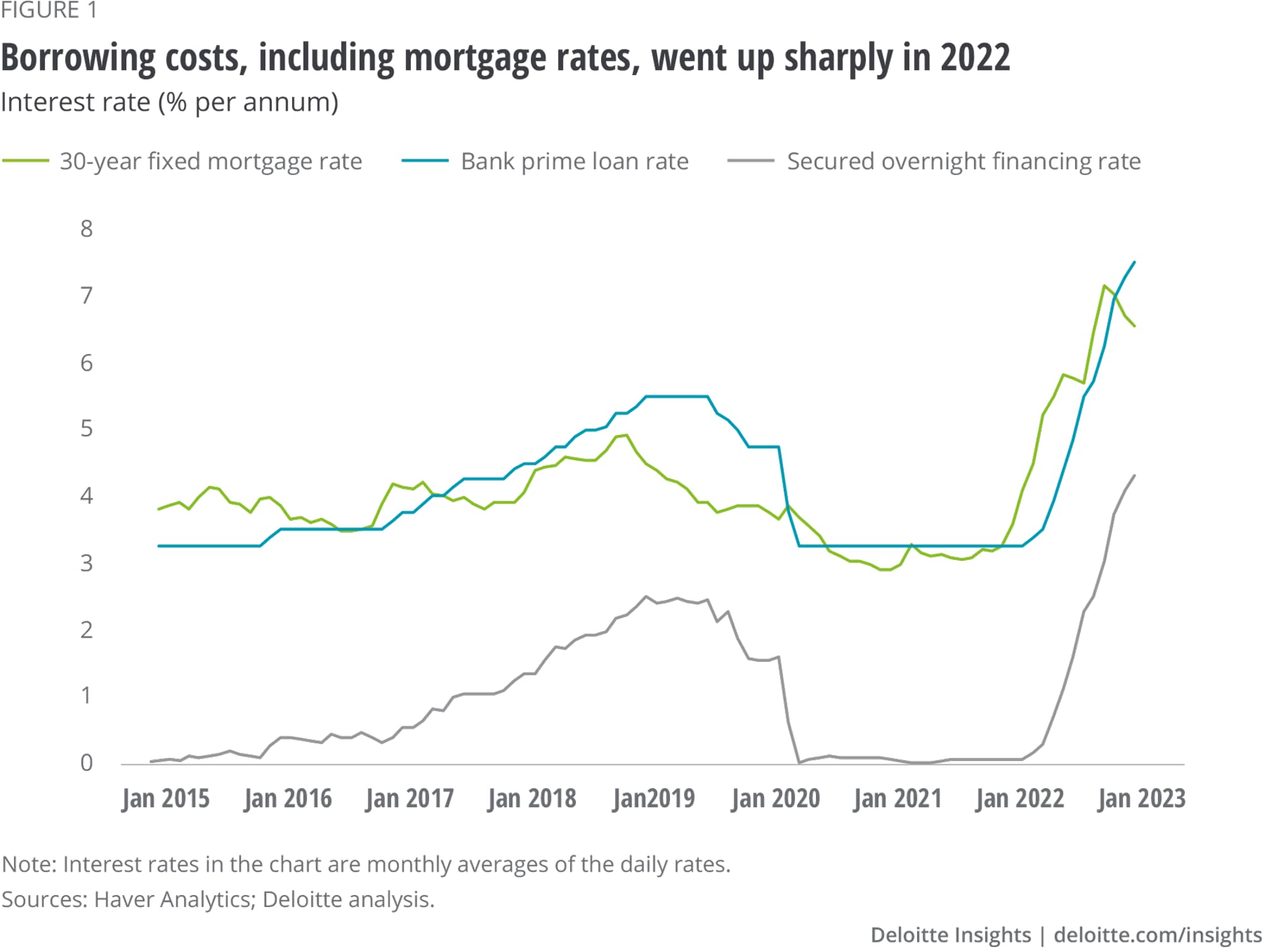

The home run in housing, however, hit two major roadblocks last year. First, the cost of mortgages shot up, as figure 1 shows. The 30-year fixed rate mortgage ended January 2023 at 6.4%, more than three percentage points above the rate at the beginning of 2022. And this too after rates had been edging down since October. Rising borrowing costs also come at a time of high inflation, which has dented consumers’ purchasing power. Real average weekly wages, for example, are still down 4.5% compared to December 2020 despite an 8.8% gain in nominal wages during this period.

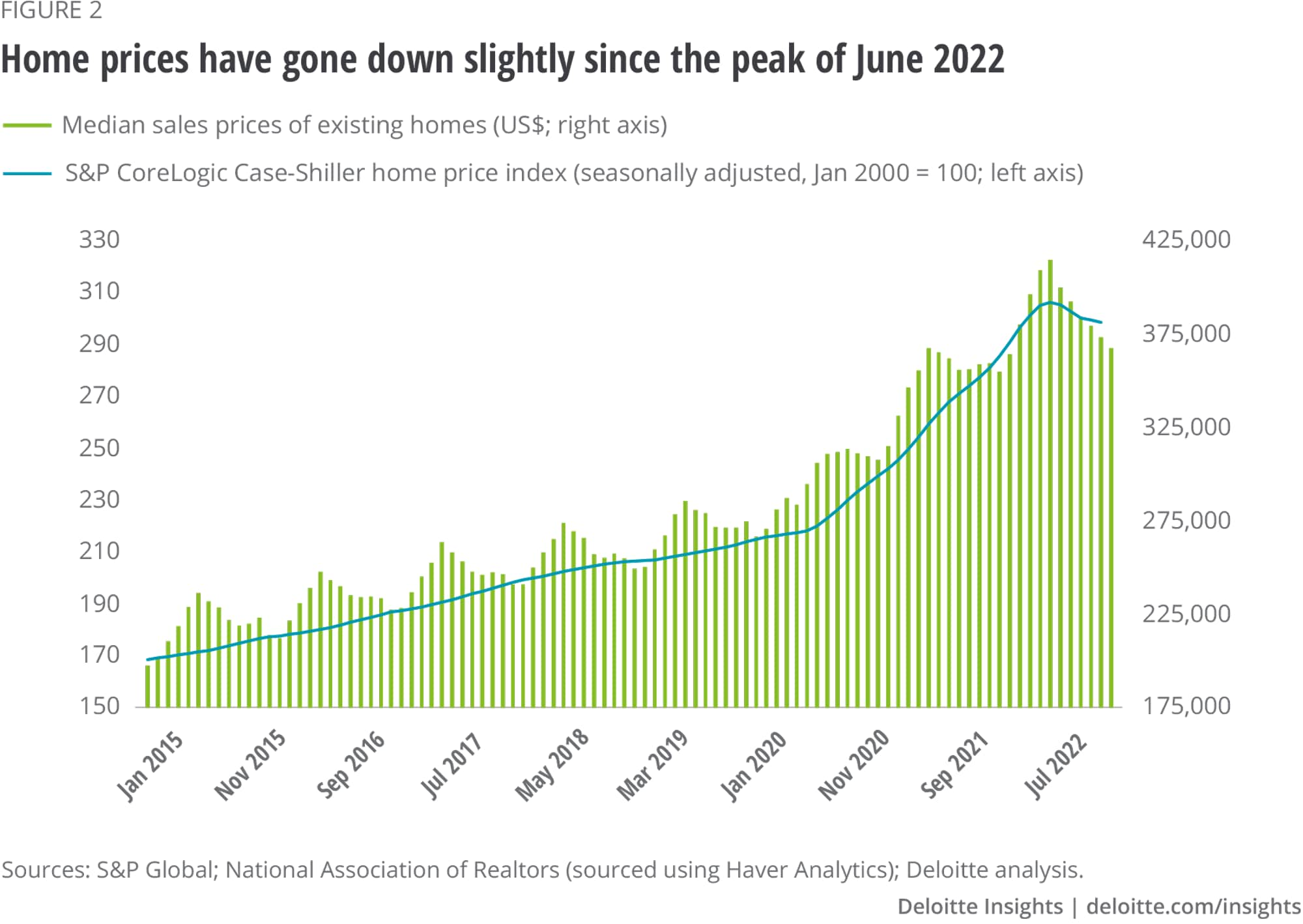

Second, housing demand also came under pressure from home prices last year. Home prices hardly suffered during the initial days of the pandemic—a sharp contrast to some asset categories, such as equities, that were hit hard in the first half of 2020. According to the S&P CoreLogic Case-Shiller home price index, the national average of home prices went up by as much as 43.1% between December 2019 and the peak of June 2022 (figure 2).6 Figure 2 also shows that much of this increase was in 2021 when prices went up by 18.9%. Similarly, data from the National Association of Realtors (NAR) shows that median sales prices of existing homes went up by 50.7% during this period.7

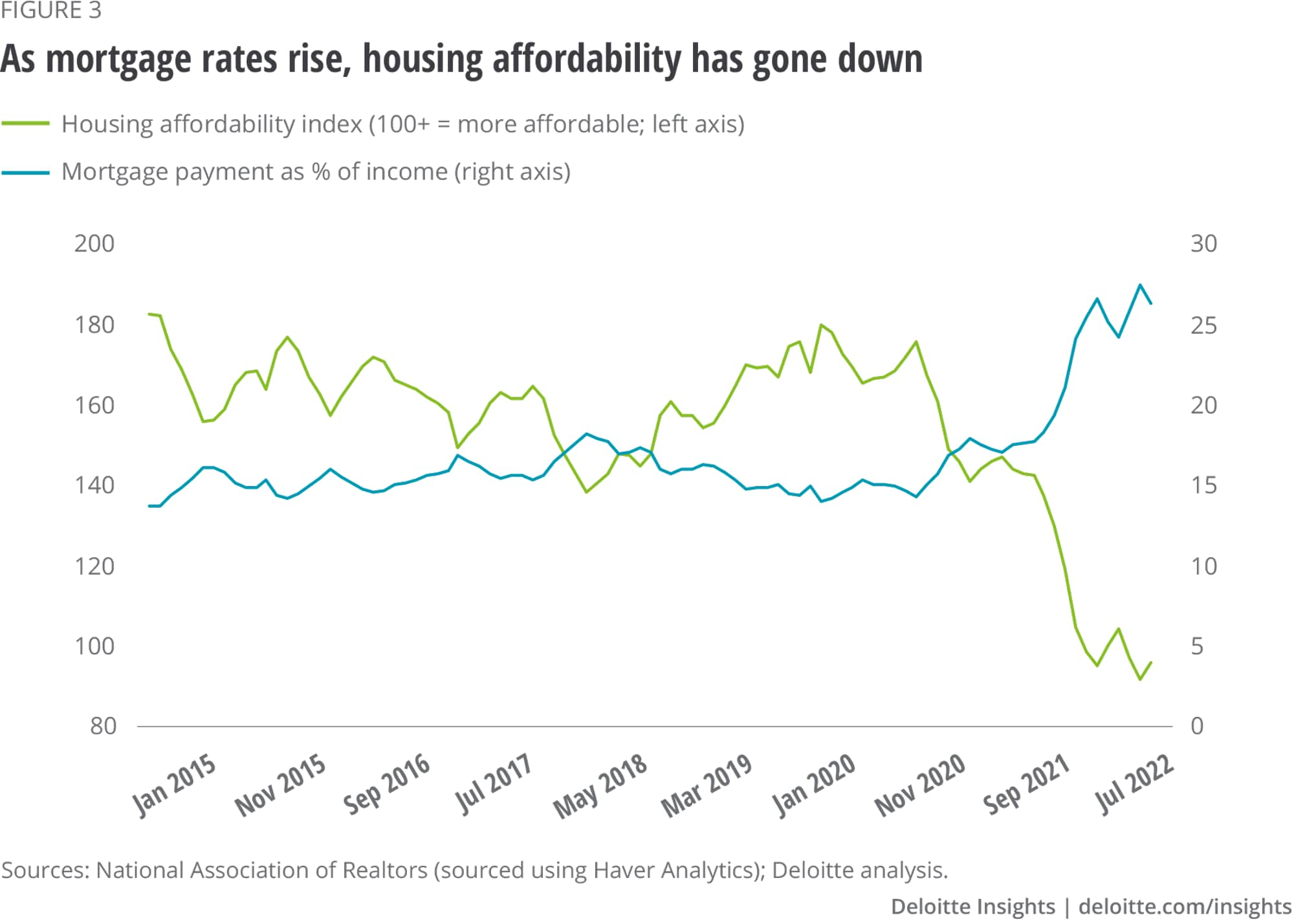

The rise in the cost of borrowing last year worsened housing affordability, which had already been under pressure in 2021 due to rising home prices (figure 3). Principal and interest payments as a share of income was 26.2% in November 2022, close to nine percentage points higher than a year before.

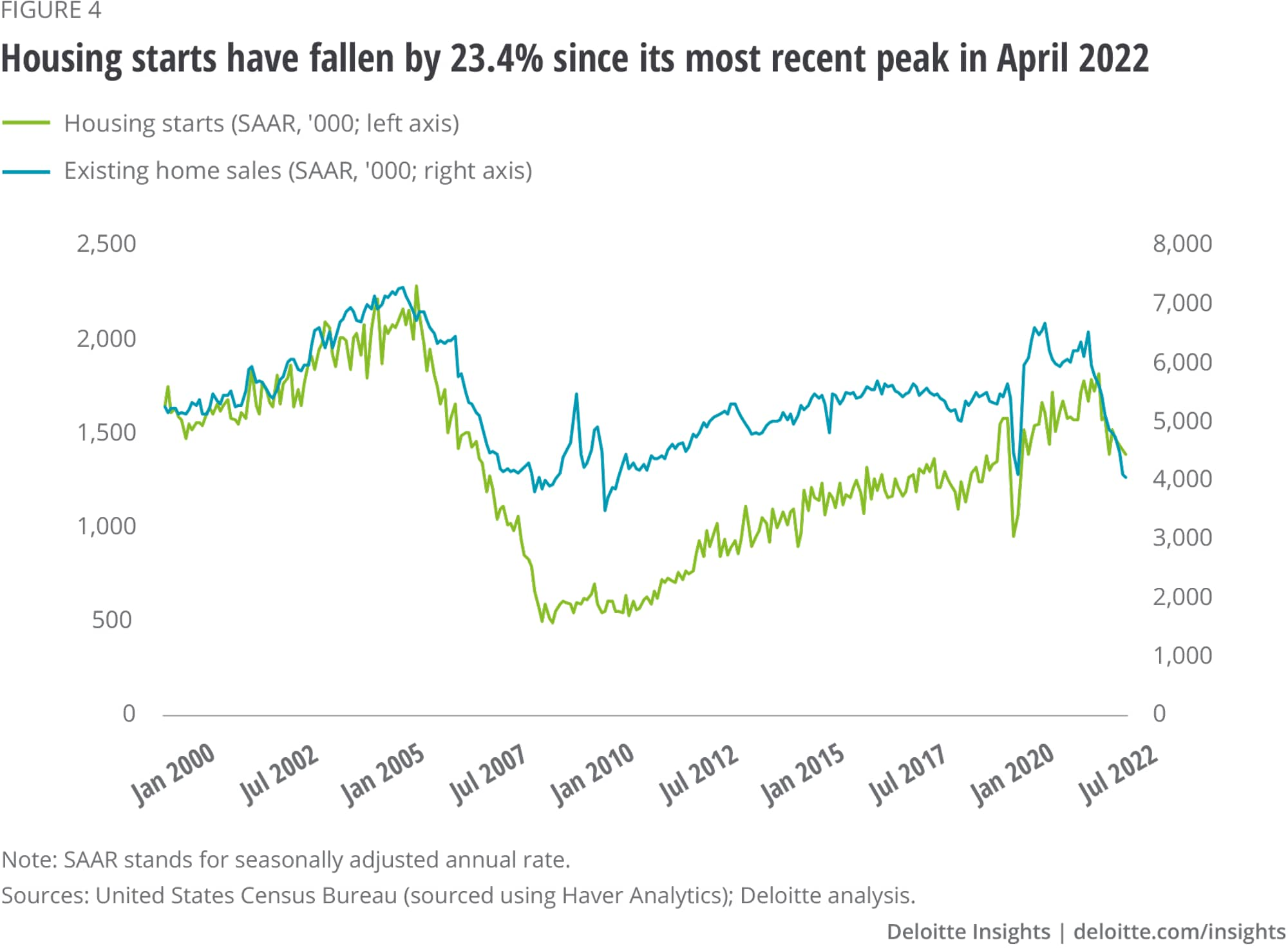

As affordability took a hit, the housing sector suffered. Real investment in residential investment, for example, was 19.2% lower in Q4 2022 compared to the year prior. In contrast, business investment was 3.7% higher during this period. And, by December 2022, housing starts had fallen below a seasonally adjusted average annual rate of 1.4 million, more than 400,000 lower than the peak in April (figure 4). Permits have also gone down—by 29.5% compared to the recent peak in December 2021. It’s not just new residential construction that has borne the brunt of decreasing housing affordability. Sales of existing homes also peaked in January last year at 6.5 million (seasonally adjusted annual rate); since then, sales have dropped by 38.1%, as figure 4 shows.

There is, however, a fair amount of diversity in the way housing trends have played out. Data on starts shows that single-family homes fared much worse than multifamily for most of last year. Until November 2022, starts for single-family homes were down 29.5% since the peak of April, much worse than the 5.2% decline for multifamily starts. That changed suddenly in December with starts picking up for single-family homes while declining 19% for multifamily homes.

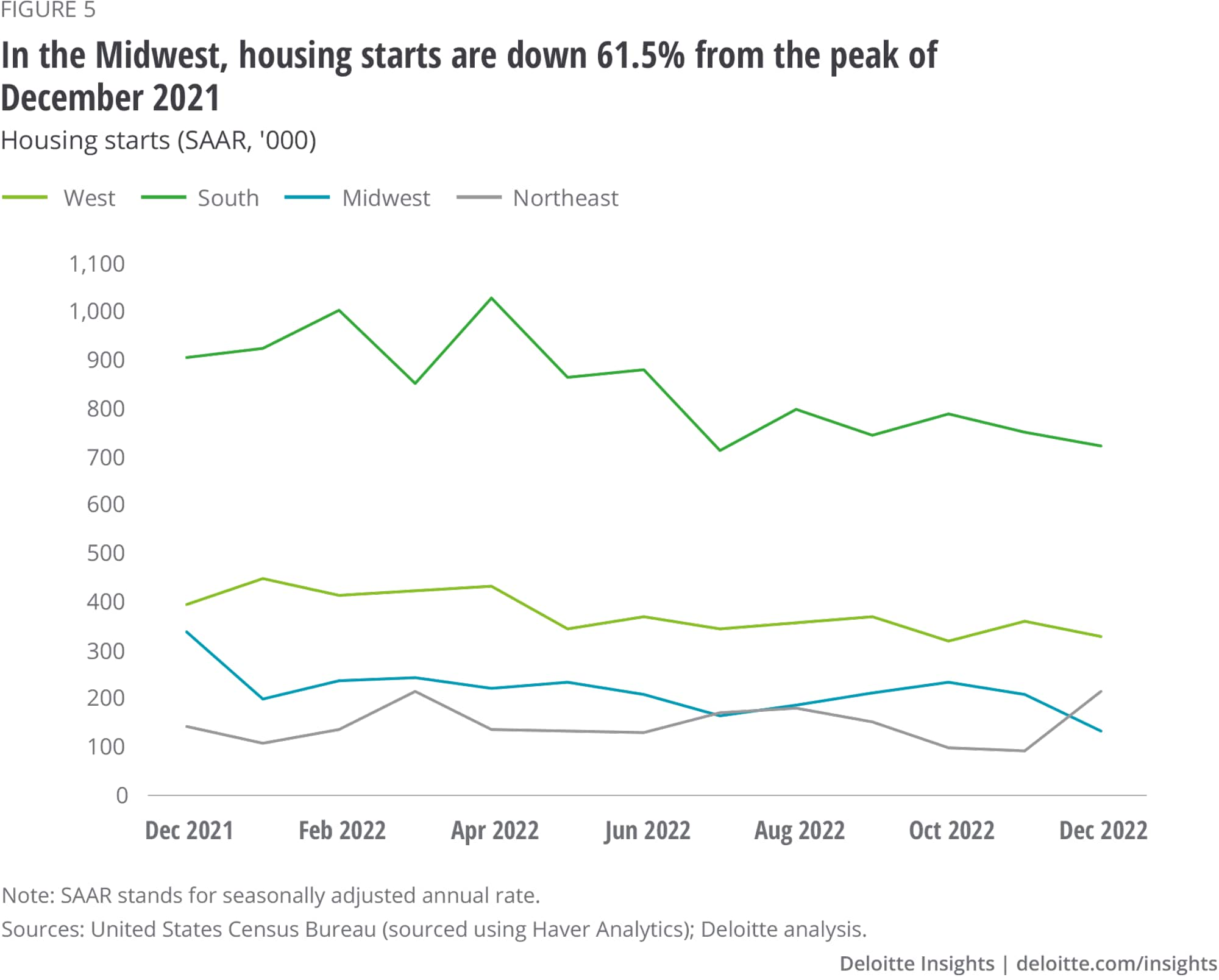

A look at housing starts by region reveals that peaks and the degree of contraction after respective peaks differs across regions. In the Midwest, starts have fallen by 61.5% from their peak in December 2021, while in the South, starts peaked in April 2022 and are down by 30% (figure 5). In the Northeast, starts have been volatile. Starts fell for three months after August, but then shot up in December by 135.6%. The data also shows that there seems to be some form of stabilization in starts since August in the West and to a degree in the South. Some stabilization in the two regions augurs well for the national figure given that these regions accounted for a little over 77% of total starts in the United States, on average, last year. Differences also crop up in the sales of existing homes relative to postpandemic peaks for different regions. Sales, for example, are down 49.3% from their peak in the West compared to a 34.4% decline in the Midwest.

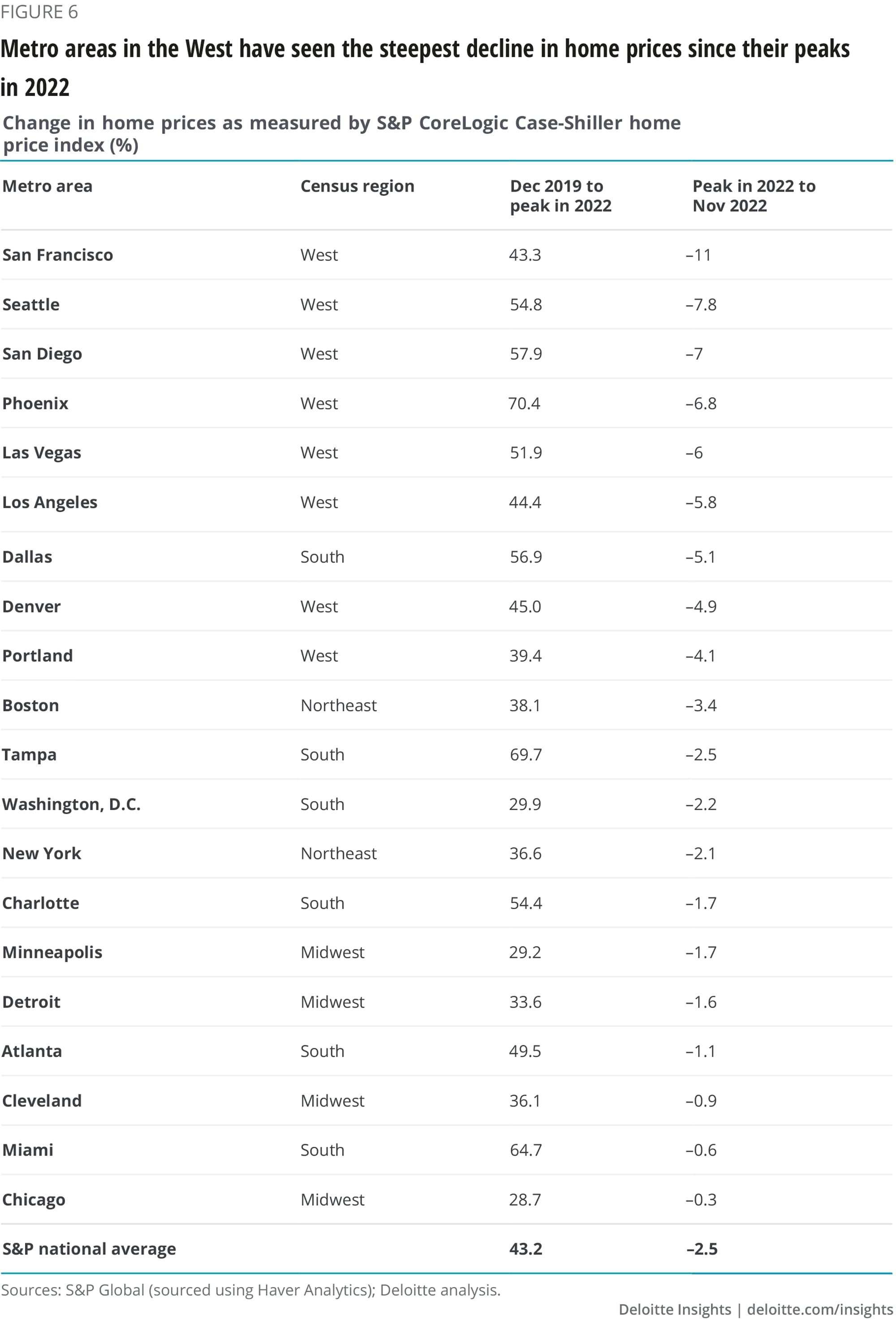

Unlike starts and sales, prices have not gone down by as much, although there is quite a bit of difference in the degree of declines among metro areas. Figure 6 shows trends in home prices in 20 major metro areas as revealed by the S&P CoreLogic Case-Shiller index. The biggest decline from their respective price peaks has been in metro areas in the West region, in cities such as San Francisco (-11%), Seattle (-7.8%), and San Diego (-7%). In the South, Dallas witnessed a 5.1% decline in prices followed by Tampa and Washington DC. Cleveland and Chicago, in the Midwest, experienced the lowest declines. Figure 6 also shows that some of the metro areas that experienced a sharp rise in prices since December 2019—for example, San Diego, Phoenix, and Dallas—have also seen strong price drops.

The current slowdown in housing has led many observers to wonder if this will be a repeat of the housing downturn of 2006–2009 and the global financial crisis during that time. That seems highly unlikely. Although the roots of the global financial crisis can be traced back to the bursting of the housing bubble starting in 2006, it was the problematic mortgage lending practices that created the bubble. It was also a general lack of understanding of how these questionable mortgages were packaged and dispersed across financial systems that touched off the recession of 2007–2009.

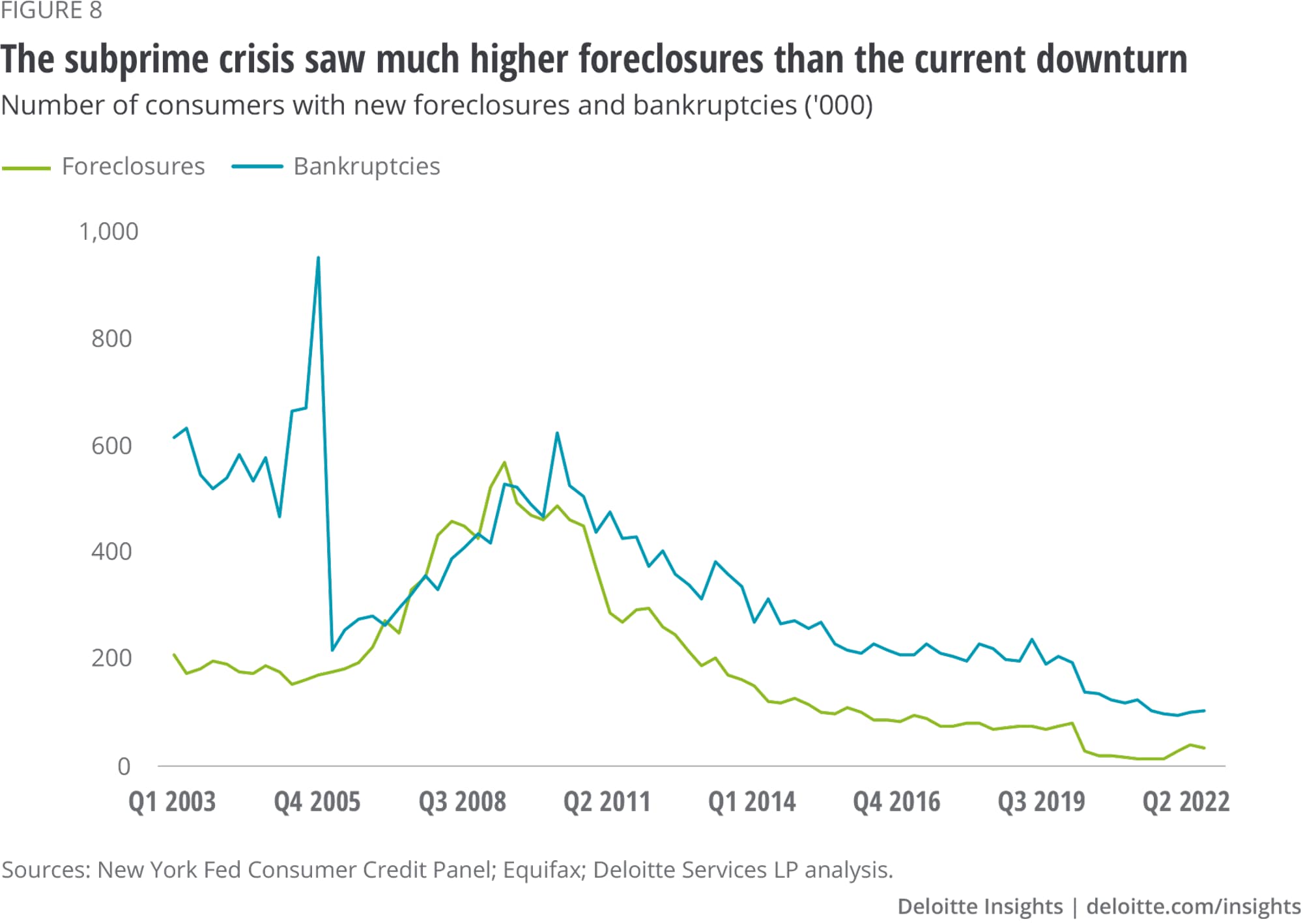

In the years leading up to the financial crisis, originations of subprime mortgages (mortgages originations to borrowers with a credit score below 620) and low prime borrowers (credit score between 620 and 659) were high. Many of them were receiving “Alt-A” loans—loans where employment, income, and net worth are not verified and/or their debt-to-income ratio is higher than acceptable for a conforming loan. These loans are inherently more risky than conventional loans. The combination of a high number of credit-shaky borrowers (figure 7) mixed with some amount of housing speculation led to a jump in foreclosures between 2006 and 2009 (figure 8). This led to panic in financial markets given the extensive use of mortgage-backed securities at that time. Fortunately, there hasn’t been a sharp uptick in risky borrowers or a substantial rise in foreclosures in recent quarters. Although foreclosures may rise if the economy slips into recession in 2023, it won’t be as severe as it was in 2006–2009 thanks to regulations on banks about lending, capital adequacy rules, and oversight on asset-backed securities enforced after the previous crisis remain in place.

Furthermore, the role of housing in the economy is smaller than what it was in 2006, and the slowdown in the sector to date is much smaller than in the period right before and during the global financial crisis. Housing starts fell by a staggering 79% between the peak of January 2006 and the through of April 2009. That figure is much higher than the dip in starts so far from their most recent peak.

The housing sector is an interest-sensitive one—business cycles and changes in monetary policy impact housing more than other sectors, such as manufacturing. With mortgage rates more than doubling last year, affordability will continue to weigh on the housing market in the near term. Rates are unlikely to go down by much this year as the Fed keeps its focus on inflation, which may have eased a bit from the highs of June 2022, but nevertheless, is elevated compared to the Fed’s target of 2%. And although home prices have declined, quantum of decline is hardly enough to offset high borrowing costs.

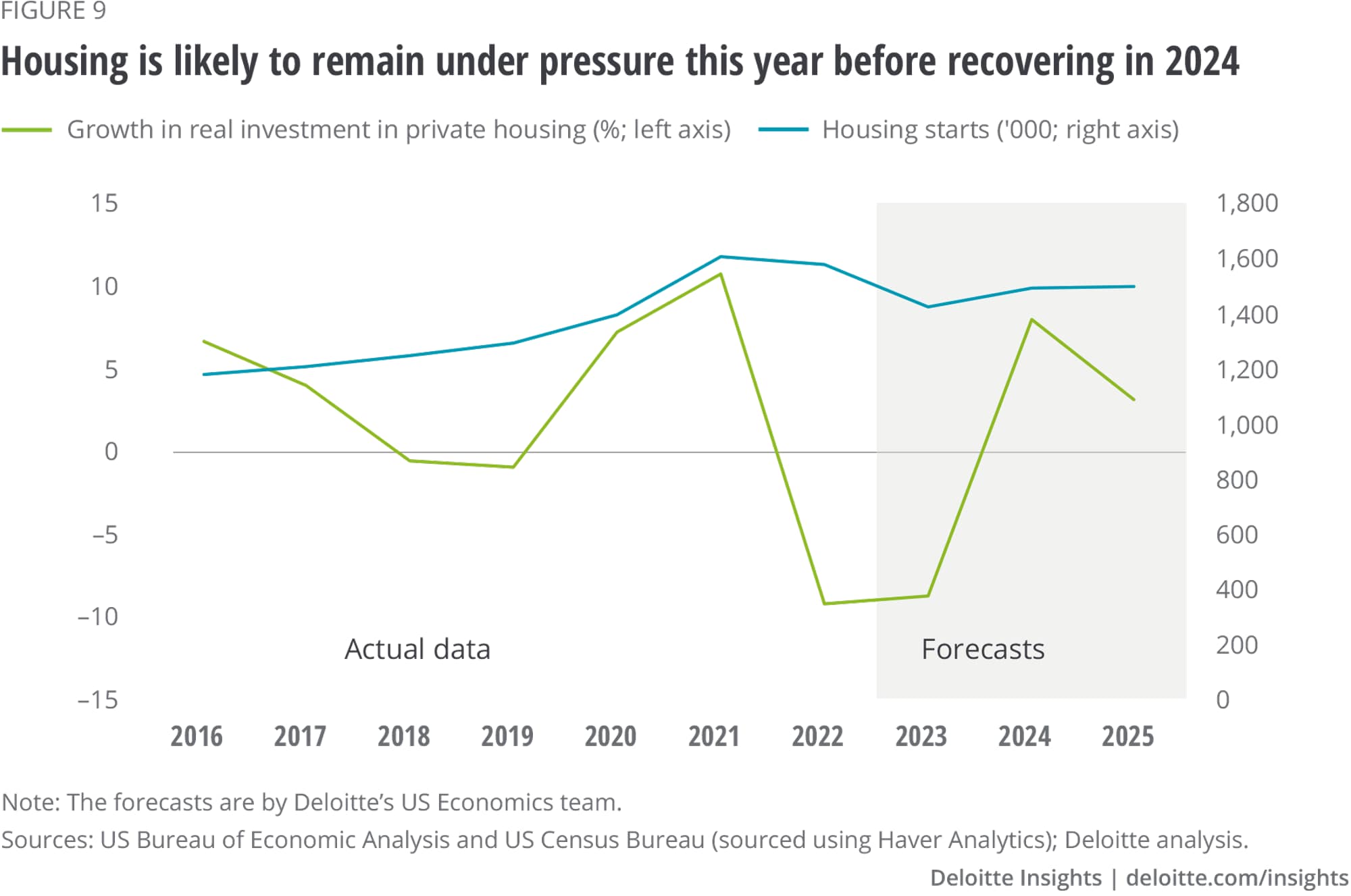

Yet, the current downturn in housing is more of a cyclical one than being driven by structural deficiencies as happened during 2006–2009. According to Deloitte’s baseline forecast, real investment in private housing is expected to decline by 8.8% in 2023, following a slightly larger contraction in 2022. Residential investment is, however, expected to recover next year if the economy stabilizes, inflation goes down, and the Fed gradually moves away from its tightening stance. Housing starts, too, are expected to contract this year before recovering next year (figure 9). A recession, however, will have a bigger impact, with investment in private housing and housing starts likely to contract by more than in the baseline scenario; in such an economic downturn, any recovery is expected to start only in the second half of 2024.

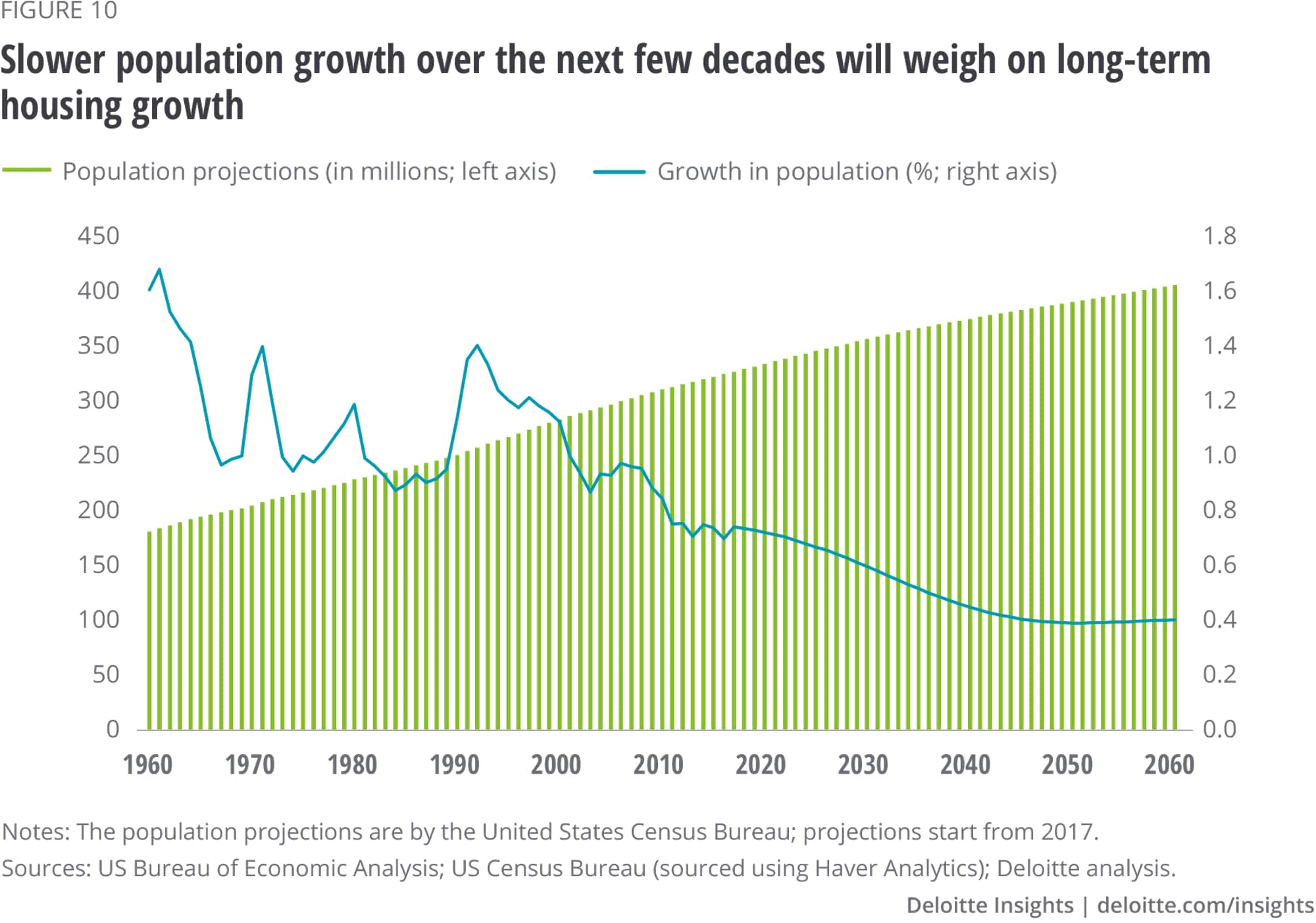

Growth in housing, however, will face challenges over the long term from demographics. Population growth—a key driver of housing over the long-term in developed economies—has been slowing steadily in the United States and is likely to slip below an average of 0.5% by the end of the 2030s, according to projections by the Census Bureau (figure 10).8 With homeownership relatively elevated at 66%—lower than the peak of 69.2% in Q1 2004 but higher than levels in the early 1990s—it is unlikely that slower population growth over the next decade will be able to support housing growth as strong as what has been seen in the post-war era.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}