{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Is deglobalization in the cards? has been saved

Cover image by: Pooja Lnu

Dating back to the global financial crisis, many economic observers have worried that a trend of deglobalization has been underway, threatening to reverse decades of gains from trade. However, similar to a recently published Deloitte study that looked at trade flows, we find no evidence of deglobalization when considering trends in cross-border investment.

In “Globalization is here to stay,1” Deloitte economists Ira Kalish and Michael Wolf analyze one of the major indicators of globalization: trade in goods. For the purpose of this report, we also assessed cross-border investment flows to evaluate changes, if any, in patterns of financial integration between economies. Specifically, we: i) noted the decline in global investment flows but also the increase in foreign direct investment (FDI) stock; ii) acknowledged the vulnerability of foreign investment to economic shocks and policy shifts; iii) noted the evidence on resilience of investment flows; iv) distinguished between conduit and productive investment; v) examined alternative measures of investment to overcome inadequacies in FDI data; and vi) noted future challenges for cross-border investment flows. We concluded that though cross-border investments are vulnerable to shocks in economies and policy shifts, there is evidence of resilience in the levels of foreign investment.

We take a deeper dive into each of these aspects:

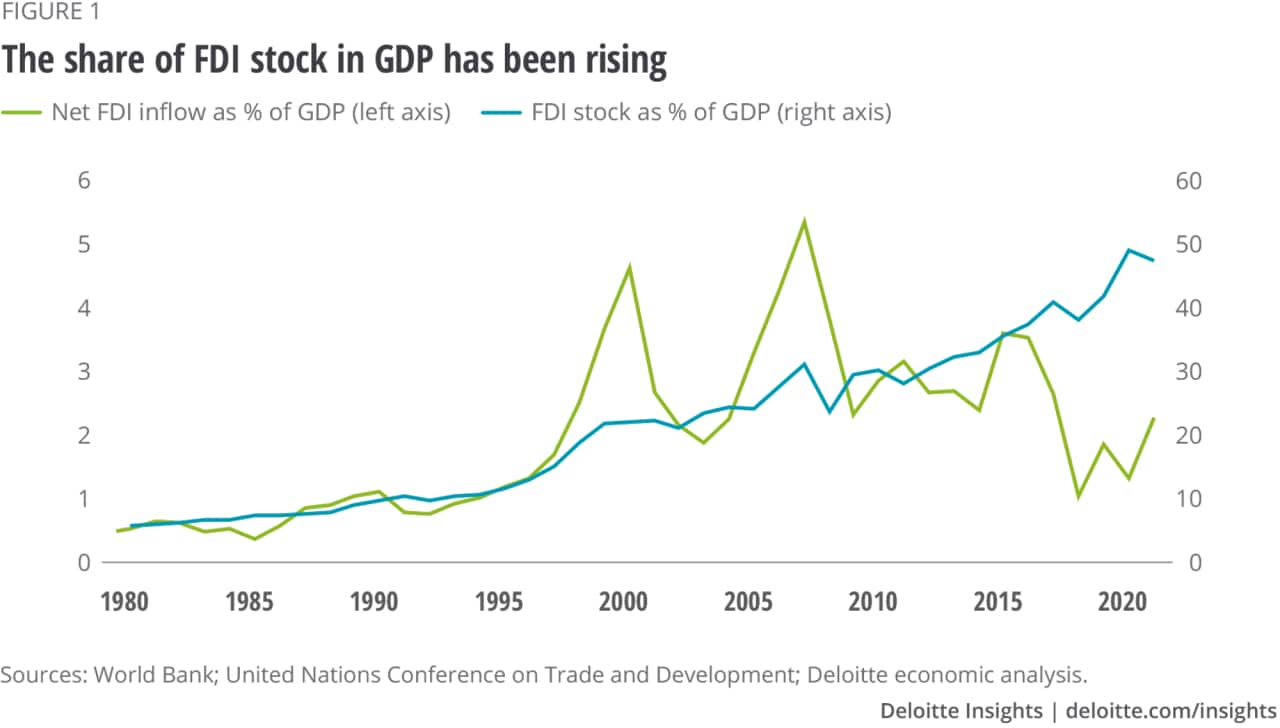

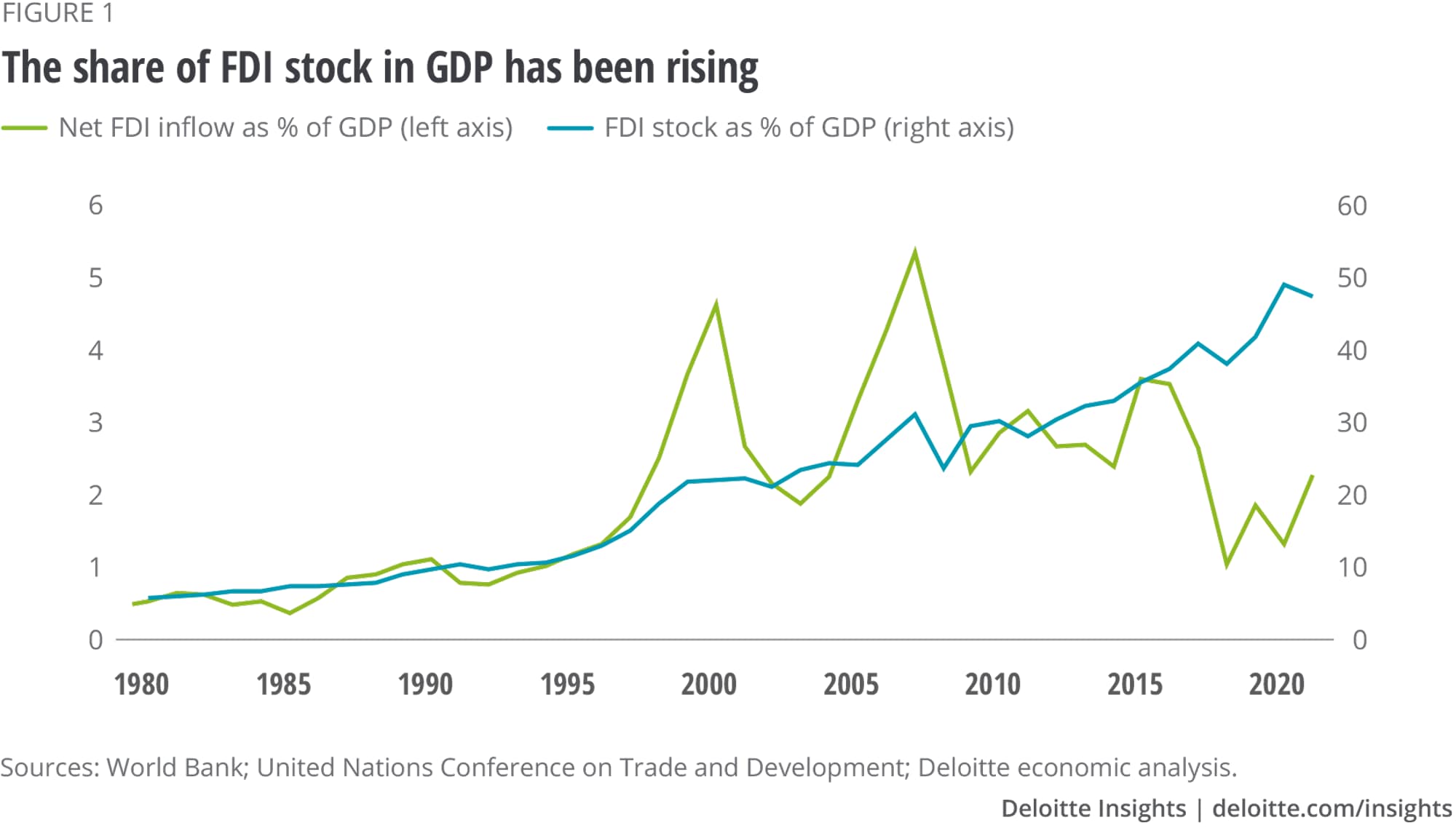

FDI flows versus stock: Post the global financial crisis, net global FDI inflows have not been growing as fast as global gross domestic product (GDP), mainly due to declining rates of return and a less favorable policy climate.2 However, the growth in FDI flows has been sufficient enough to increase FDI stock as a percent of GDP. Barring the initial setbacks during shocks to the economy, such as during the global financial crisis and the initial emergences of the COVID-19 pandemic, the share of FDI stock in GDP has been rising.

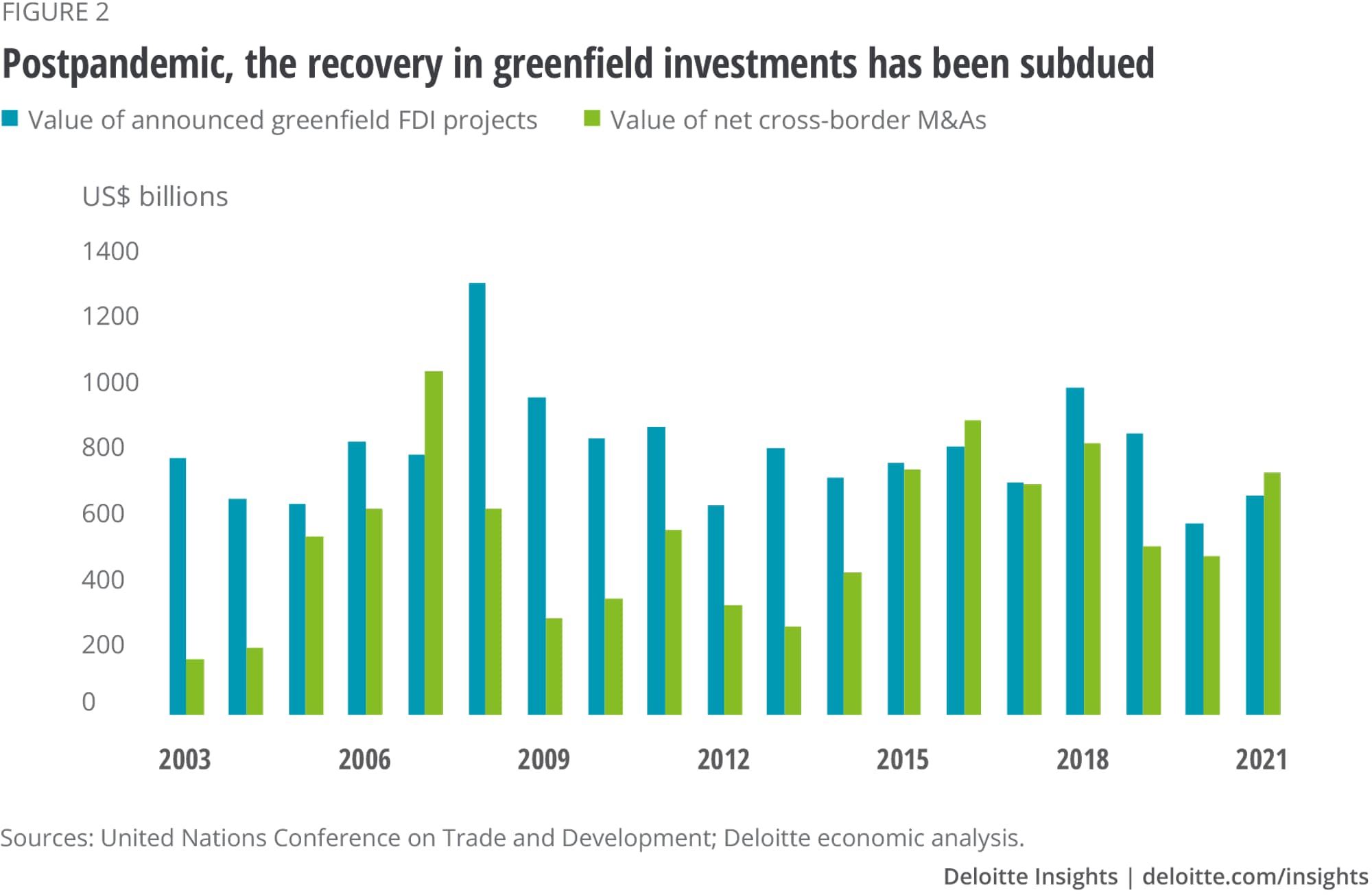

Vulnerability of foreign investment to economic shocks and policy shifts: Foreign investment is channeled into the creation of productive assets via greenfield investments, or through the purchase of existing assets via mergers and acquisitions (M&A). The United Nations (UN) also reports data on international project finance, a mechanism to channel investment in infrastructure and other sectors relevant for sustainable development.3 These components of FDI respond differently to uncertainties in the economy and the policy environment.

While greenfield investments appear to be more vulnerable to economic shocks, M&A and international project finance are closely linked to financial markets and are more responsive to policy initiatives and changes. In 2021, FDI flows rebounded from the low levels reached during the pandemic in 2020.4 This recovery was driven by a rebound in M&A markets and international project finance due to a return to accommodative monetary policies and an increase in infrastructure stimulus packages across economies. However, the recovery in greenfield investments remained subdued.

Resilience of investment flows: Although foreign investment is sensitive to changes in policies, there is evidence of resilience after the initial impact wears off. For instance, in 2018, the United States enacted the Foreign Investment Risk Review Modernization Act (FIRRMA), which strengthened the ability of the Committee on Foreign Investment in the US (CFIUS) to review foreign investment for national security consideration, even if it did not result in the control of a US business.5 While not explicitly aimed at China, the number of CFIUS cases involving Chinese investors fell between 2017 and 2020 before rebounding in 2021,6 as Chinese investors appear to have adjusted to the new rules. The data on M&A also suggests that the CFIUS turned cautious post-FIRRMA but is now stabilizing in its reviews.

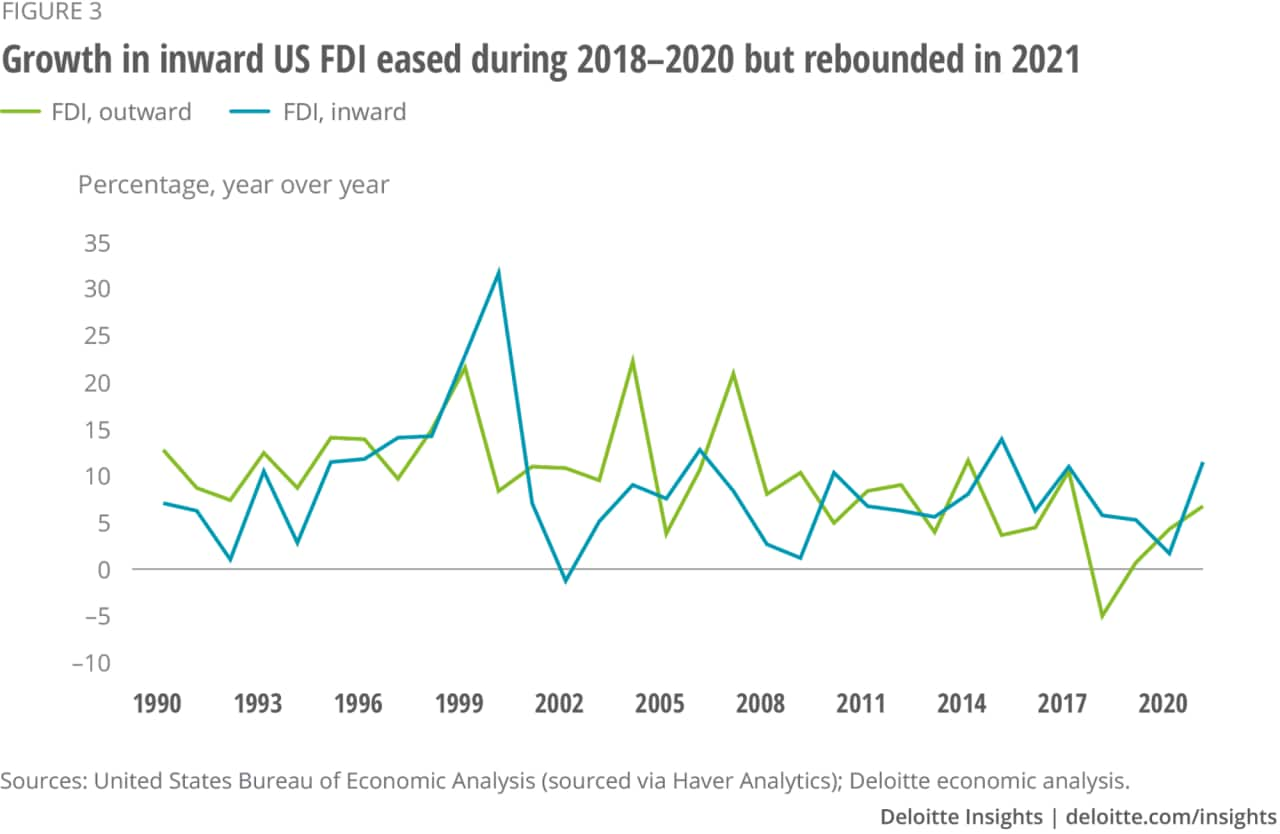

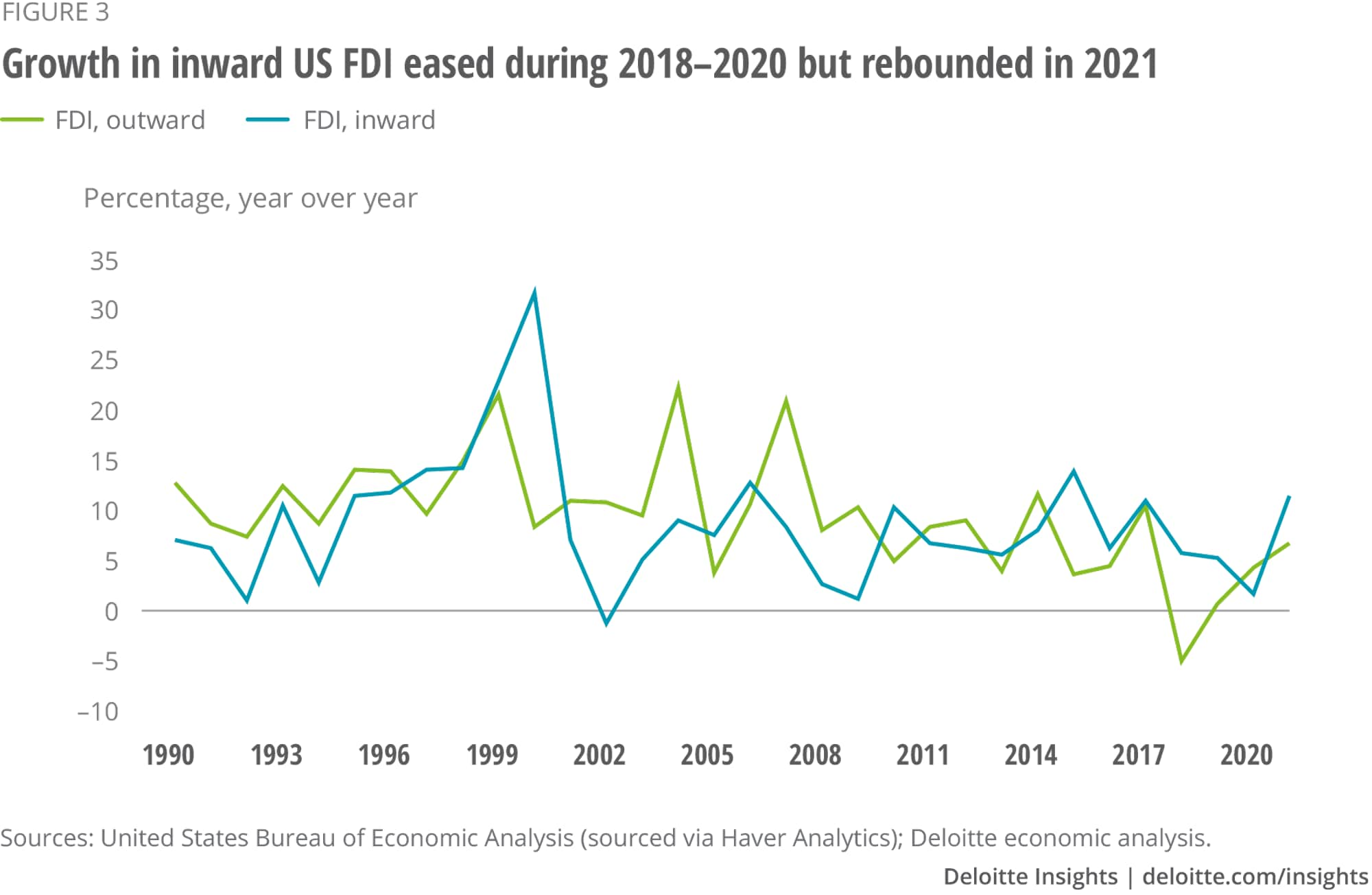

The growth in inward investment in the United States declined during 2018–2020 but rebounded in 2021. In fact, the International Monetary Fund (IMF) reported that in 2021, the United States was the world’s top destination for FDI, while China also moved up a notch to the third position.7

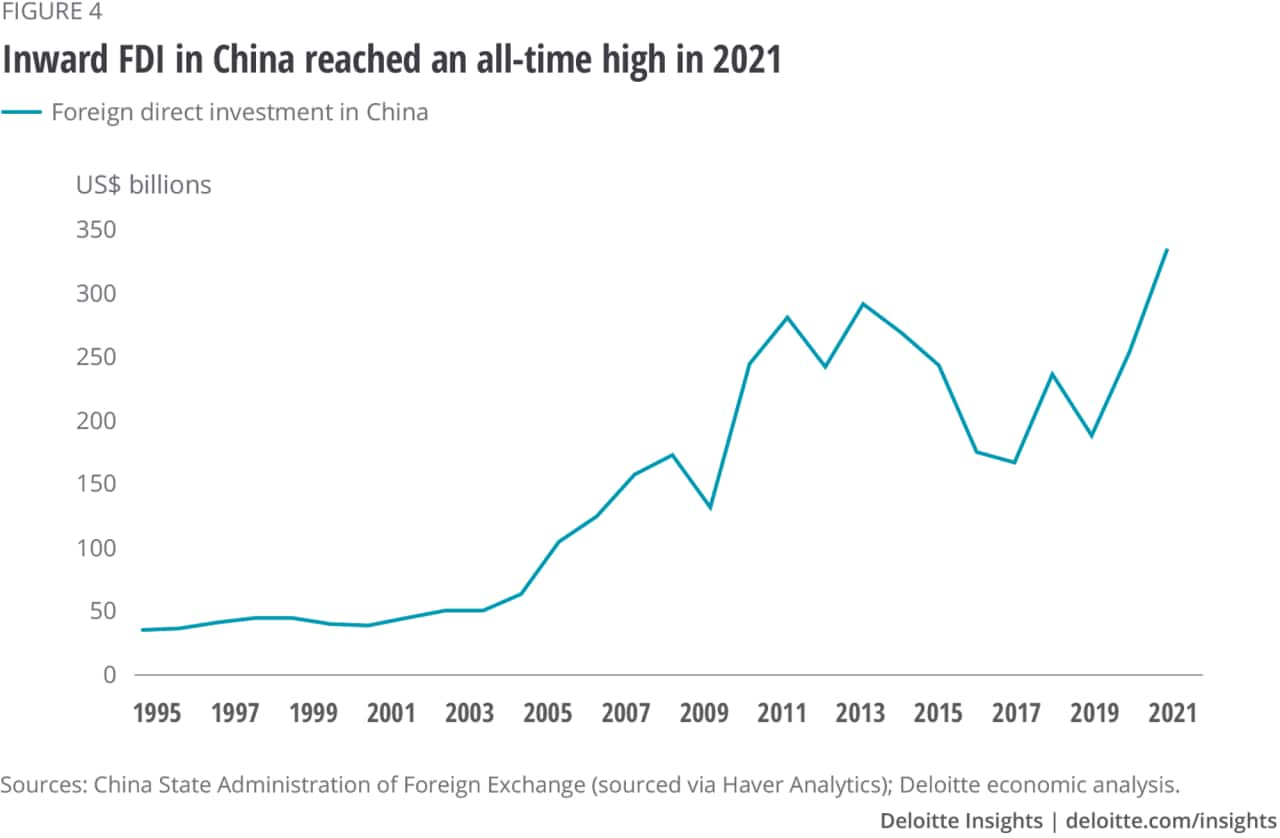

Despite a rise in protectionist sentiment and talk of nearshoring amid global supply chain pressures during the pandemic, the Peterson Institute for International Economics notes that inward FDI in China rose by a third, to reach a new all-time high, allaying concerns around deglobalization.8 Further, the Peterson report notes that a majority of the firms in the United States and Europe with investments in China do not plan to pull out of the economy amid an increasingly favorable policy climate.

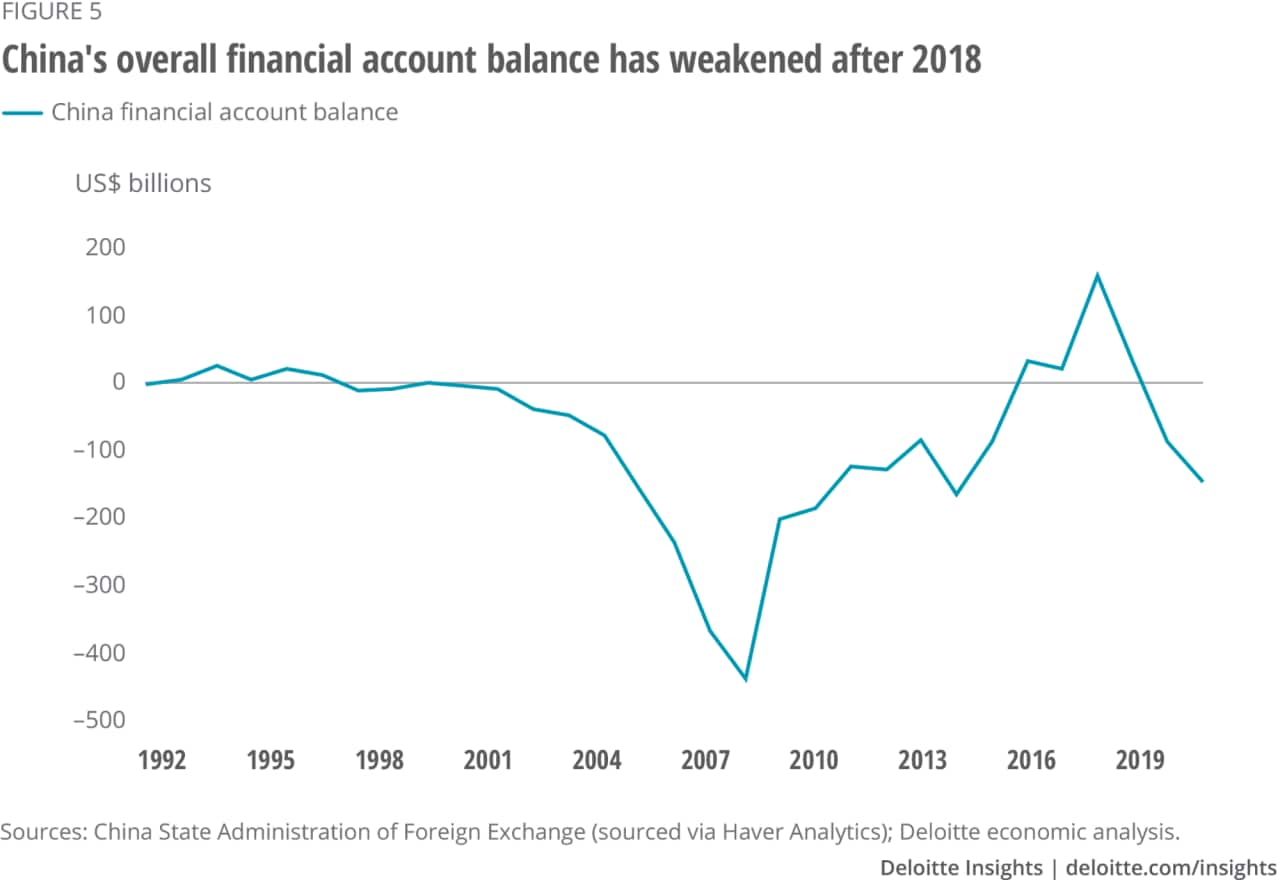

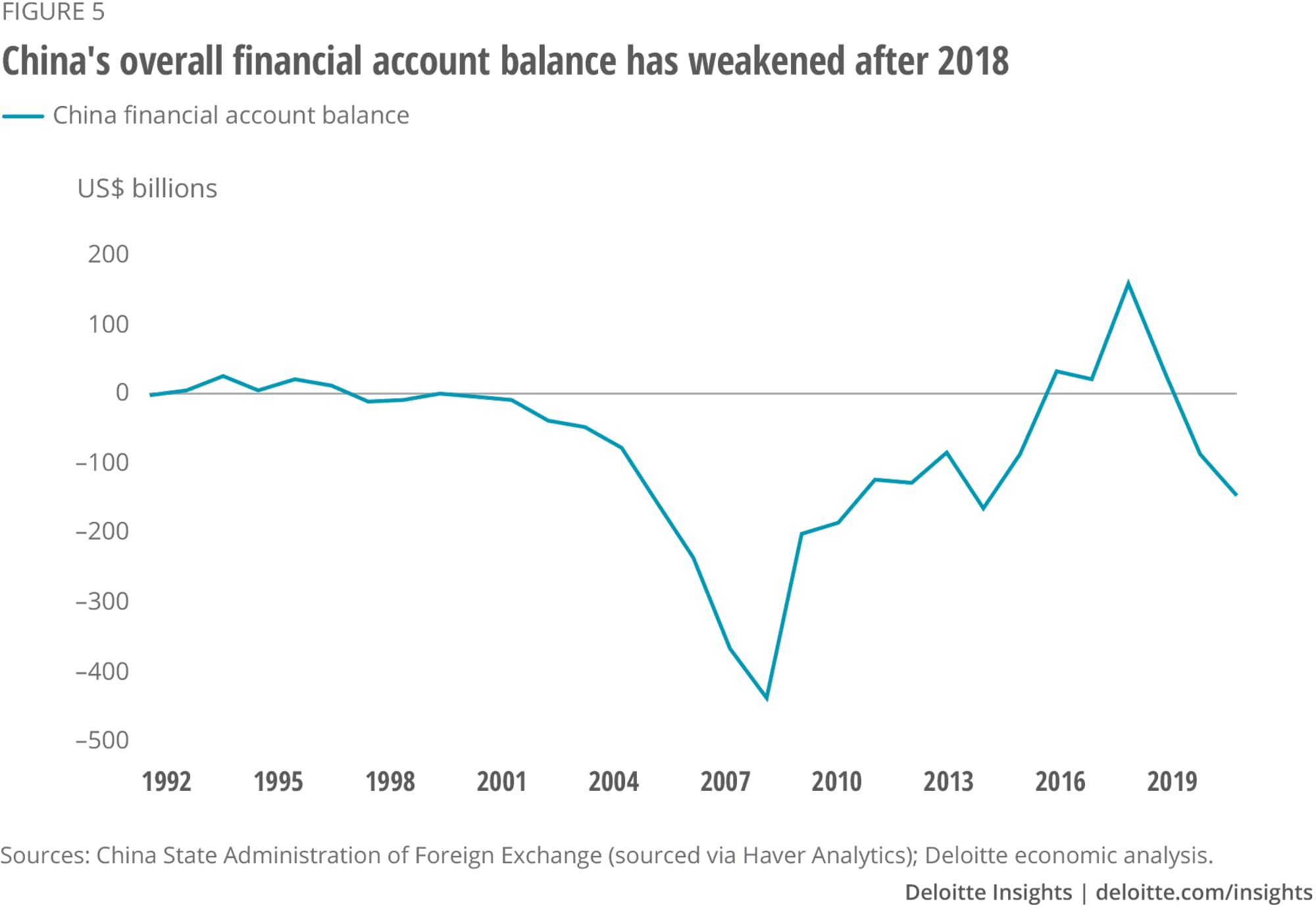

Deglobalization versus shifts in globalization: Despite the evidence of resilience in investment, patterns of investment have changed due to economic shocks or policy shifts, as noted in the case of M&A and greenfield investments. Even in the case of China, the strength in FDI inflows masks the weakness in overall financial account balance or implied international capital flows, as measured by the difference in nongold international reserves and the merchandise trade balance.

Business confidence in China, as noted by the PIIE report, bodes well for investment in the economy, but there is also anecdotal evidence9 and research10 in favor of policy shifts to build resilient supply chains that could change prospects for the economy. These measures do not particularly point toward deglobalization but indicate changes in patterns of globalization, as noted by our global economists.

Disconnect between investment flows and the real economy: The IMF note on FDI ranking highlights that some of the smaller economies such as the Netherlands, Luxembourg, and Hong Kong, with relatively low GDP, were among the top 10 global investment destinations in 2021.11 The likely reason for this disconnect is that these investments are likely “conduit FDI,” which arises when a multinational enterprise (MNE) investing from a home country in a host country establishes an intermediate step (often, a special purpose entity, or an SPE) in an offshore financial center with the aim of availing low taxes or favorable fiscal incentives (for more details, read the sidebar, “Data inadequacies and alternative measures of investment”). Studies estimate that such conduit FDI accounts for 30–50% of global investment.12

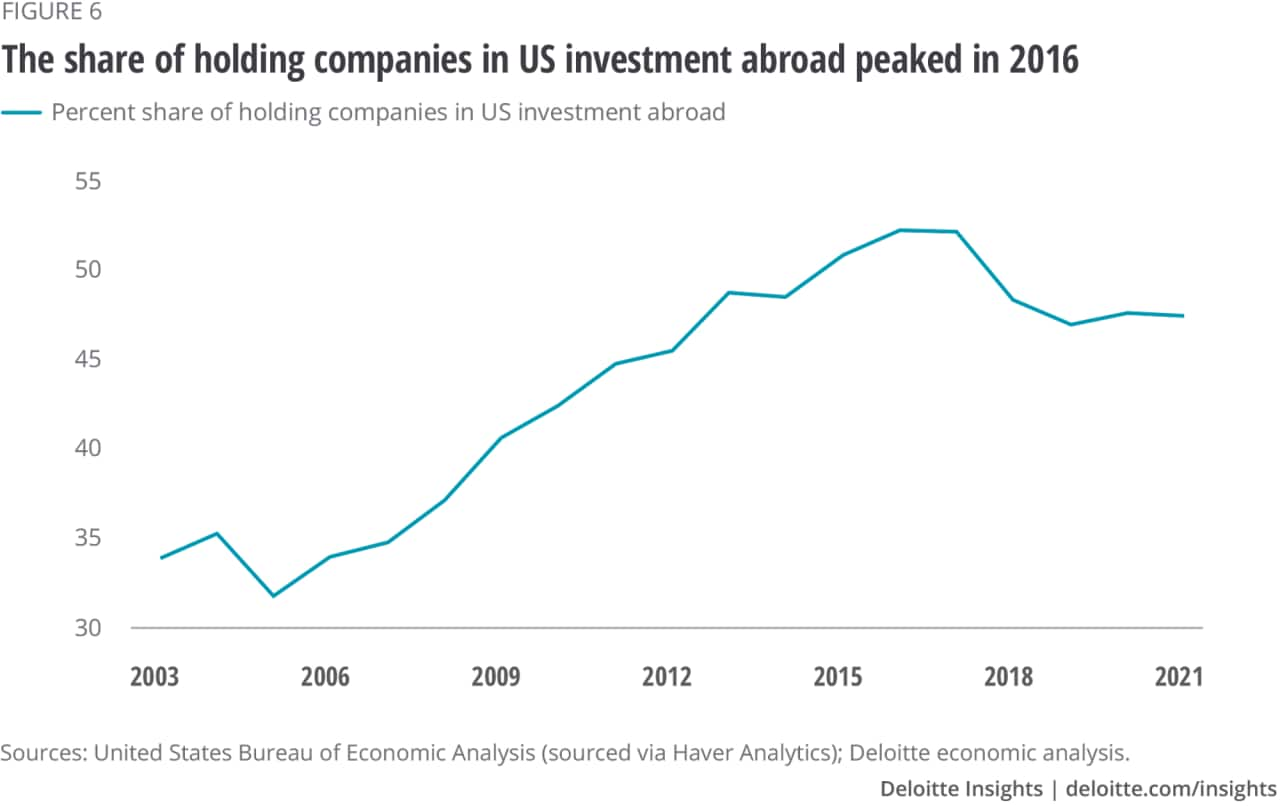

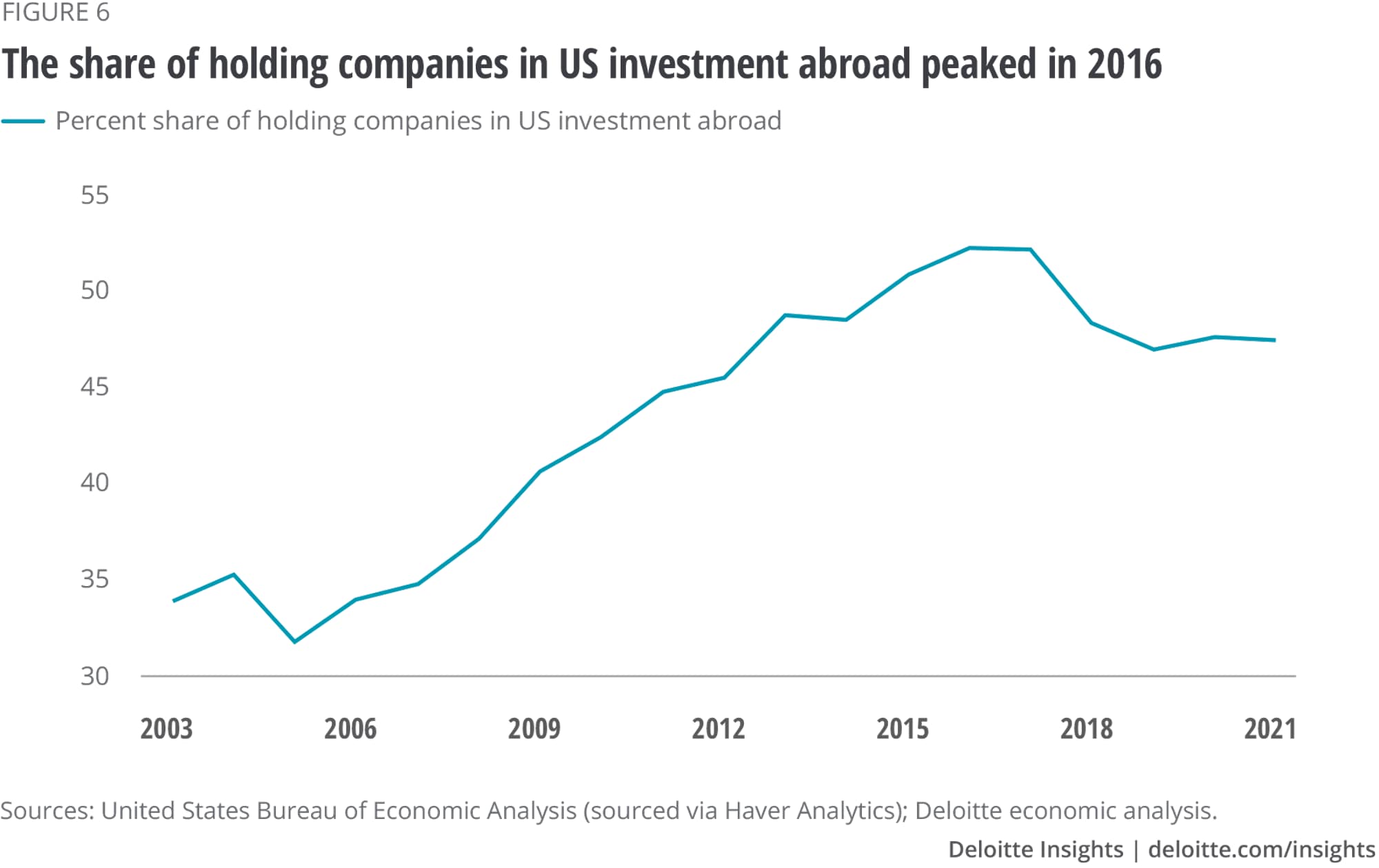

This form of investment is evident in data on US investment abroad. In 2021, nearly half of US investment abroad was in holding companies.13 The Bureau of Economic Analysis defines holding companies as “businesses engaged in holding the securities or financial assets of companies and enterprises for the purpose of owning a controlling interest in them or influencing their management decisions.” In effect, these entities channel investment to other countries and aggregate income from them.

The UN, in its 2016 report on world investment,14 noted that a growing share of FDI income to an economy’s GDP could indicate an increase in the share of holding companies that aggregate MNEs’ foreign profits. In the United States, before the global financial crisis, most FDI income was generated by entities other than holding companies. However, by 2015, around half of the FDI income from abroad was from holding companies.

In fact, the share of holding companies in US investment abroad peaked at around 52% during 2016-17 before starting to decline from 2018. The fall in share can be attributed to the US Tax Cuts and Jobs Act introduced in 2017, which reduced incentives for US MNEs to keep profits in low-tax jurisdictions and led to large scale repatriation of accumulated foreign earnings.15 This legislation not only dragged down US investment abroad in 2018 but it also had an impact on global investment flows. Global FDI flows, however, have recovered since 2019, as the impact of the US tax reform waned.16 Due to this policy change, the share of holding companies in US investment abroad declined during 2018-19, though it remained above the pre-GFC average. The IMF also notes the impact of this legislation on the decline in shares of offshore financial centers in global FDI since 2017.17

Conduit FDI makes it difficult to measure international production or investment in the “real” part of the economy using standard bilateral FDI statistics. There are two main challenges related to conduit FDI:

The standard bilateral FDI statistics help to understand financial flows, including claims and liabilities across economies. However, to measure international production, alternative measures of data provide better insights. For instance, for inward FDI, bilateral FDI statistics show FDI positions by direct investors. If economy A is investing in another economy B via offshore financial center C, C becomes the direct investor in B, while A is the ultimate investor. The data classified by the ultimate investing country (UIC) helps to understand which economies invest, take investment decisions, and bear the risks and reap the benefits of investment.18

For instance, in 2018, European investment hubs Luxembourg and the Netherlands together accounted for 41% of foreign investment in Germany, while the United States accounted for only 8%. However, from the ultimate investor lens, the share of the United States increased to 21%, while that of Luxembourg and the Netherlands combined fell to 14% of German inward stock. Similarly, in 2016, bilateral FDI statistics show that the United States accounted for 3% of total Chinese FDI stock, but data by ultimate investors suggests that the country was the biggest foreign investor in China, accounting for 12% of total inward Chinese stock.19

Currently, not all economies report FDI data by ultimate investors. The inadequacies in bilateral FDI statistics have been noted in literature and attempts to distinguish between conduit and productive FDI have motivated organizations. such as the IMF, to launch SPE statistics, among other measures.20

Future challenges for cross-border investment: Governments are generally interested in attracting and retaining foreign investment, and tax regimes are one of the most widely used policy tools. In the international context, the Base Erosion and Profit Shifting (BEPS) project was a major initiative launched by the OECD and G20 in 2013 to curb tax avoidance by MNEs and to make the global tax system fairer. The BEPS project spawned future work that now proposes a global minimum tax on the profits of MNEs to counter shifting of profits to low-tax economies.21

The expected reduction in profit shifting could lower indirect or conduit FDI, but a global minimum tax could raise costs, and possibly result in a decline in productive investment. The minimum tax is also likely to shift patterns of financial integration across economies, as higher tax countries could become increasingly competitive and attractive FDI recipients, due to the narrowing of tax differentials with low-tax economies.

In terms of national investment policies, the global financial crisis triggered a surge of measures, particularly within developed economies that were protectionist or less favorable to investment due to national security concerns and economic nationalism.22 The pandemic accentuated this trend, which is now gradually spreading to developing economies that were traditionally focused on attracting investment. Such policy shifts could be a barrier to future investment flows.

In addition to these policy shifts, some of the megatrends shaping the future of industrial production in the decade to 2030, and therefore, investment flows, include: i) technological changes and advancement, including digitalization in the supply chain; and ii) sustainability concerns around the economics of international production that are driven by environment, social and governance (ESG) standards. While the changes in policies could pose challenges, it could be premature to assess the final impact of these megatrends on the financial integration between economies.

Ira Kalish and Michael Wolf, Globalization is here to stay, Deloitte Insights, December 14, 2022.

View in ArticleUnited Nations Conference on Trade and Development (UNCTAD), World Investment Report, 2019.

View in ArticleUNCTAD, International project finance: Boosting investment in infrastructure and the SDGs, October 20, 2021.

View in ArticleUNCTAD, World Investment Report, 2022, accessed on February 13, 2023.

View in ArticlePeterson Institute for International Economics (PIIE), Worst case averted on foreign investment reviews, August 20, 2018.

View in ArticlePIIE, US security scrutiny of foreign investment rises, but so does foreign investment, September 1, 2022.

View in ArticleInternational Monetary Fund (IMF), United States is world's top destination for foreign direct investment, December 7, 2022.

View in ArticlePIIE, Foreign corporates investing in China surged in 2021, March 29, 2022.

View in ArticleOlaf Scholz, “We don’t want to decouple from China, but can’t be overreliant,” Politico, November 3, 2022.

View in ArticleIMF, Global trade and value chains during the pandemic, World Economic Outlook, April 2022.

View in ArticleInternational Monetary Fund (IMF), United States is world's top destination for foreign direct investment, December 7, 2022.

View in ArticleUNCTAD, Looking through conduit FDI in search of ultimate investors—a probabilistic approach, July 15, 2019; IMF, What is real and what is not in the global FDI network?, December 11, 2019.

View in ArticleBureau of Economic Analysis, Direct investment by country and industry, 2021, July 21, 2022.

View in ArticleUNCTAD, World Investment Report, 2016.

View in ArticleIMF, United States is world's top destination for foreign direct investment, December 7, 2022.

View in ArticleUNCTAD, World Investment Report, 2020.

View in ArticleIMF, United States is world's top destination for foreign direct investment.

View in ArticleUNCTAD, Looking through conduit FDI in search of ultimate investors—a probabilistic approach, July 15, 2019.

View in ArticleIMF, United States is world's top destination for foreign direct investment.

View in ArticleUNCTAD, World Investment Report, 2022.

View in ArticleUNCTAD, World Investment Report, 2020.

View in ArticleCover image by: Pooja Lnu