What’s up with the dollar? Or why is the dollar up? has been saved

Cover image by: Jaime Austin

What goes down, comes back up. That’s the story of the dollar’s foreign exchange rate—not just this year, but in all the decades since the United States untied the dollar from gold in 1971. The dollar’s international value tends to be relegated to the business page. Makes sense, since the United States devotes a relatively small share of its economy to foreign trade. But the dollar’s value does have an impact on Americans and US businesses and consumers through the price paid for imports and the competitiveness of US exports. Just as important, the factors behind the dollar’s current rise can have a large impact on foreign countries—especially emerging economies that depend on dollar finance.1

The dollar is one of about 180 currencies (according to the United Nations2) existing today. Each of the approximately 179 nondollar currencies has its own exchange rate with the US dollar. That means we have to define what we mean by a rise in “the exchange rate,”3 as the dollar may be appreciating against one currency but depreciating against another. We have to take into account the importance of each of those 179 currencies to US and global trade, and to the international financial system.

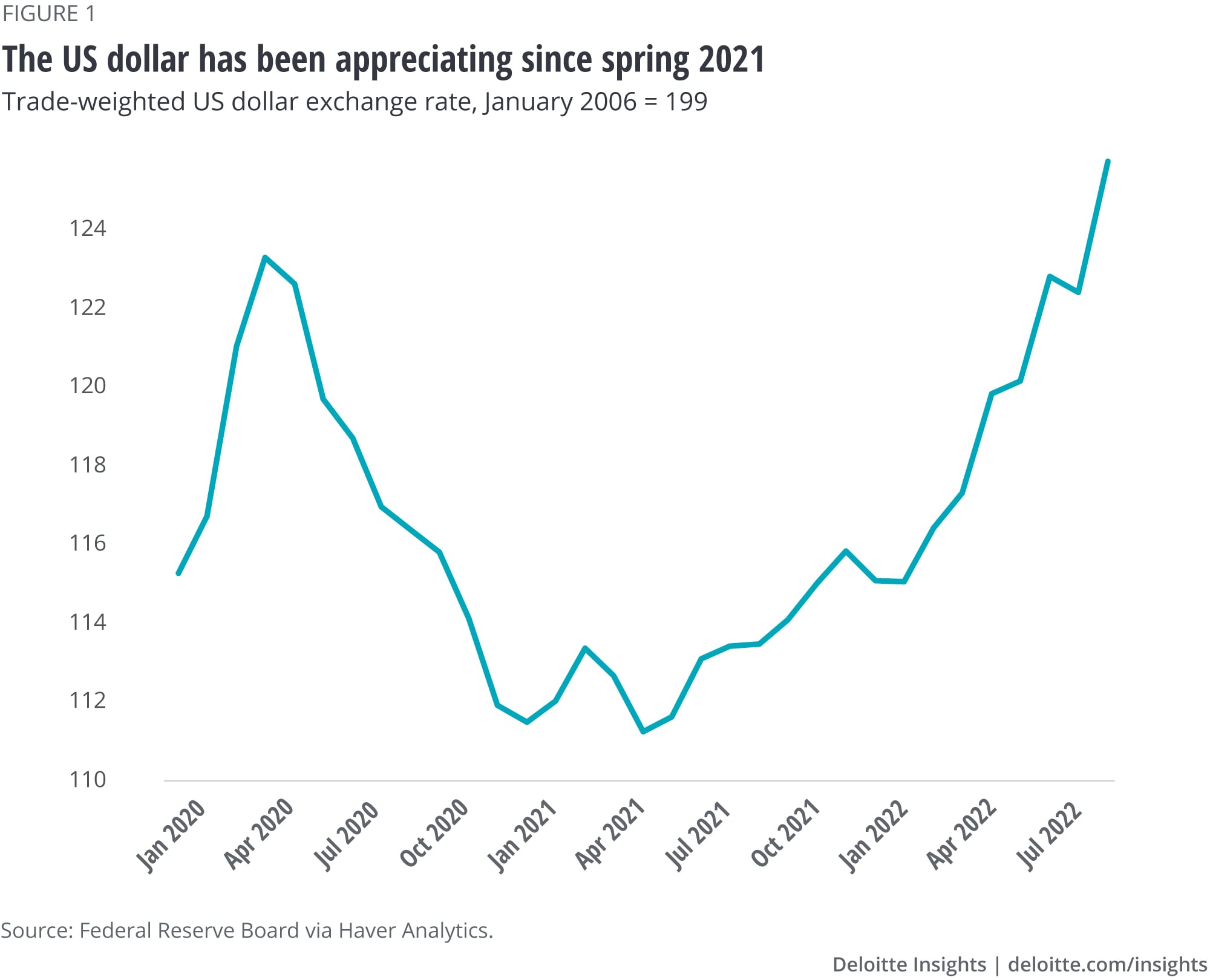

Figure 1 shows one attempt to summarize the dollar’s international value. It shows the average exchange rate of the dollar in about 30 currencies, where each currency’s value is weighted by the importance of the currency’s country in US trade. According to this measure, the dollar started appreciating in July 2021—and has continued to do so. In fact, it’s now above the peak value observed during the first pandemic period in April 2020.

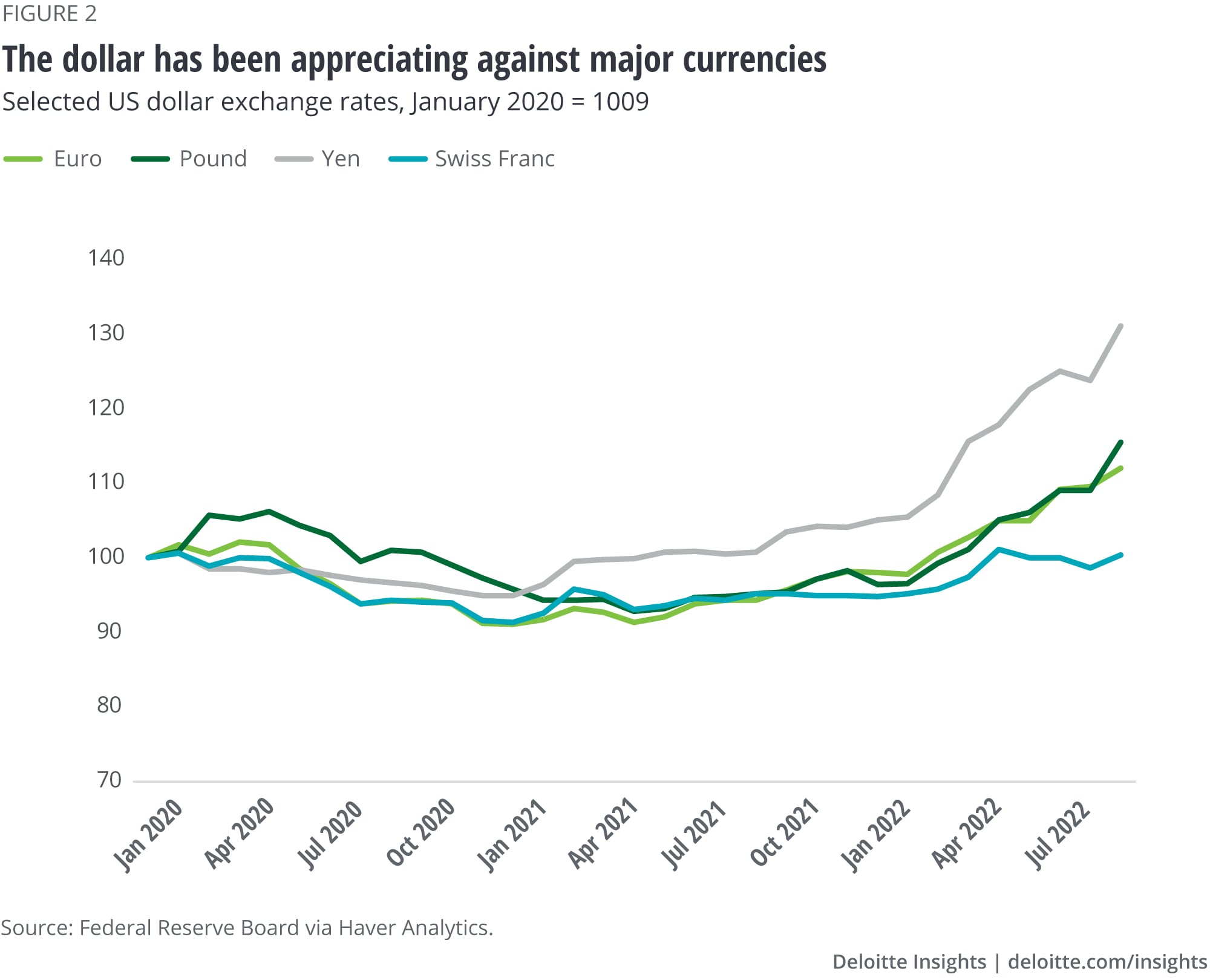

Trade weights are not always the best measures of the importance of different currencies. Three of the currencies with the largest trade weights are the Mexican peso, the Canadian dollar, and the Chinese yuan. These currencies are less important for international investors than others, such as the Swiss franc and the UK pound. Figure 2 shows the exchange rates of the nondollar currencies that play the largest role in the international financial system. The Swiss franc, although not important in US trade, does play a role in international finance. On the other hand, the Canadian dollar, which is a key currency for US trade, is not as important for global finance.

Three of these currencies account for much of the dollar’s recent appreciation—the euro, pound, and yen. The euro made headlines earlier in 2022 by breaking the dollar/euro equity level. This is not meaningful by itself, but carries some psychological weight. The yen’s level is higher than it has been for more than 10 years. And while the pound remains above dollar/pound unity, it is approaching that level—another psychological shock.

Foreign exchange rates exude mystery. But the explanations for exchange rate movements tend to be relatively prosaic. The problem is that the exchange rate is a key price in two international markets—the market for goods and services, and the market for global investments. Economists have long understood that exchange rates behave very oddly sometimes for that reason.4

On the one hand, the price of the dollar reflects the relative desirability of holding dollar assets (which is to say, investing in the United States). Any investment, whether a share of stock or a Treasury bond, has a price based on two things: the expected return of the asset and the riskiness of the asset. These are always measured relative to an alternative. Investors usually compare owning a share of stock to holding cash (or some other short-term asset). In the case of the dollar, an investor would compare the return on a dollar asset to the return on similar foreign assets. Figure 3 shows the return on a three-month US Treasury bill minus the return on three-month government securities in the Eurozone. That’s a pretty hefty increase in the premium for holding short-term dollar assets. Unless an investor is convinced that the dollar is going to depreciate substantially against the euro, shifting a portfolio toward dollars looks like a no-brainer.

On top of that incentive, the US dollar is still considered the safest currency in the world. Investors have always responded to geopolitical conflict by buying dollar assets. The Russia-Ukraine conflict, for instance, threatens the Eurozone directly, and major European countries like Germany and France are considered to be the most plausible alternatives to dollar assets. It’s not surprising, then, to see international investors shifting portfolios toward the dollar, which raises demand and the price of dollars.

But where can international investors obtain those dollars? That brings us to the other market for dollars: dollar demand and supply generated by US exports and imports.

If US goods and services are relatively expensive, foreign sellers will accumulate dollars, since people aren’t buying US goods. That’s useful, because if foreign investors want more US dollars, they can obtain those dollars by selling goods and services to the United States. The two markets—the market for financial assets and the market for goods and services—are closely connected. The market for goods and services determines the amount of dollar assets available to global investors. And the market for assets sets the price of US exports and US imports to make the right amount of dollar assets available.

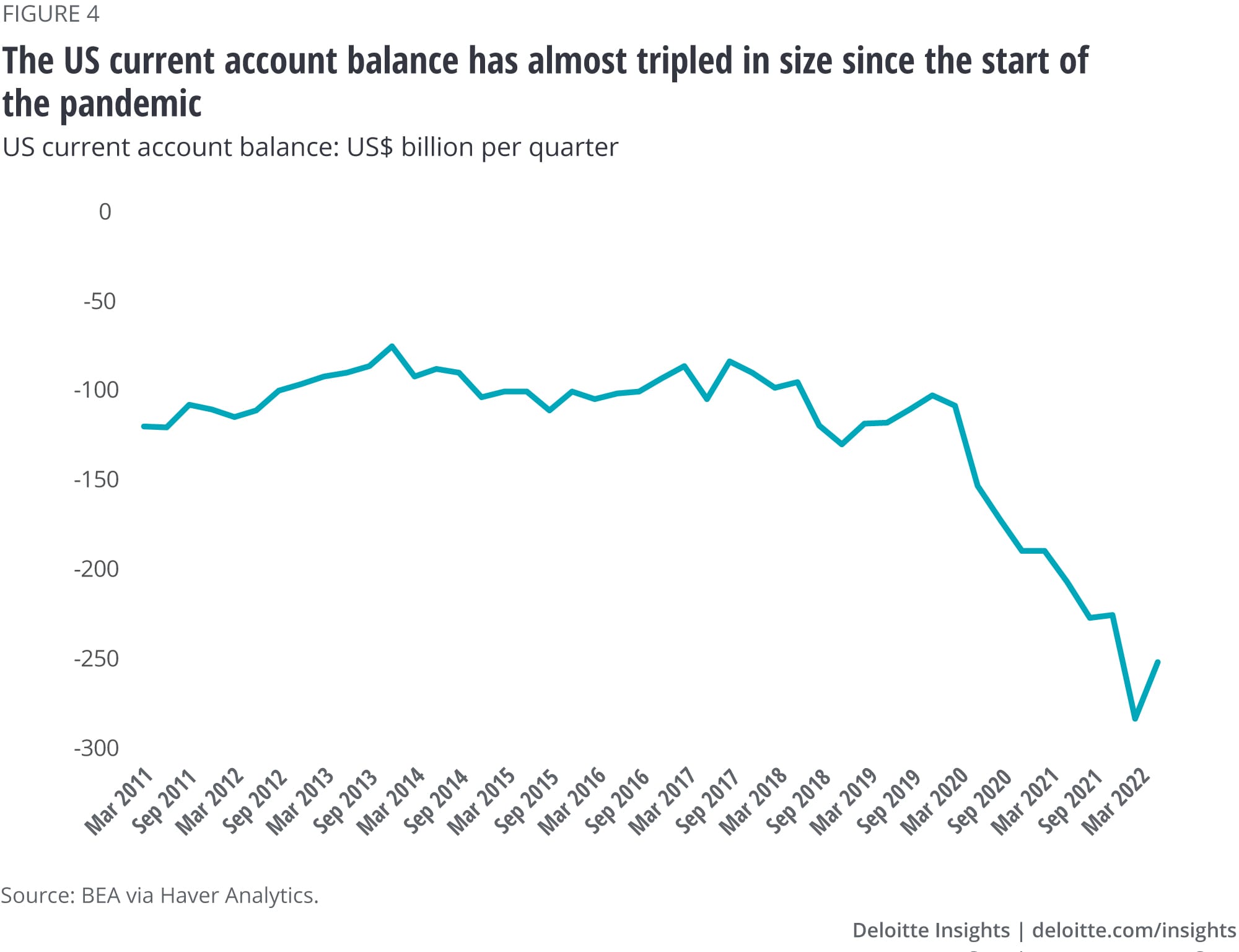

This means that a global demand for dollars will make US businesses less able to compete with their foreign counterparts. And, in fact, that is precisely what has been happening. Figure 4 shows the US current account, the key measure of foreign acquisition of US dollars. The current account is mainly the value of US exports minus the value of US imports, and—since the United States imports more than it exports—is generally negative. But the size of the imbalance has exploded since the start of the pandemic. It reached almost US$300 billion in the first quarter of 2022, about three times the size before the pandemic. The dollar’s strength in the face of this large increase is an indication that foreign investors want even more dollars than they can get their hands on.

Of course, the dollar’s rise is brutal for US exporters and US companies that compete with imports. And it is a fact that real US imports are now about 15% above the prepandemic level, while exports are almost 4% lower than before the pandemic, despite some improvement in the last few months. But there is some hope.

Economic research suggests that, while financial prices and investment behavior drive exchange rates in the short run, exchange rates tend to revert to levels that allow exports and imports to grow at sustainable long-run levels. The exchange rate at which a basket of traded goods costs the same in both currencies is called the “purchasing power parity” (PPP) exchange rate. And economists have found that, over long periods of time, exchange rates tend to move toward this level.5 The Organization for Economic Cooperation and Development estimates the current euro/dollar PPP exchange rate to be about 0.75 euros per dollar, considerably lower than the current level of unity.

There is good reason to expect that absent additional geopolitical risk or a recession in Europe, the euro is likely to appreciate over the next five years—likely, but not a certainty. The same is true for the Japanese yen, and quite possibly many other currencies. When that happens, commentators will no doubt express concern over the “weak” US dollar. But improving investment opportunities abroad, and improved competitiveness for US businesses, will only be good for the US—and global—economy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}