United States Economic Forecast

The Q3 2023 forecast is optimistic, reflecting increasing signs of a “soft landing” for the US economy. But risks are still anticipated to be relatively high; the full impact of the Fed’s tightening may not have been felt, leaving us to put the chances of recession at around 20%.

A case of optimism?

Starting in early 2022, talk of recession was in the air.1 That summer, internet searches for “recession” peaked at a level that was more than 20% above the level of searches when the pandemic started in March 2020.2 Some well-known economists had argued that inflation would only drop if the unemployment rate rose substantially.3 But inflation has moderated, yet no recession has occurred. The labor market continues to grow, and the unemployment rate remains at extremely low rates.

Now, recession fears are falling. The August National Association for Business Economics Policy Survey found that two-thirds of the panelists are confident of a “soft landing.”4 The Wall Street Journal’s survey of economic forecasters found a drop in forecasters’ probability of a recession.5 It certainly looks like an outbreak of surprising optimism from dismal scientists.

A cynic might assume that optimistic economists are a sure signal of a downturn, but the optimism reflects reality. Even if monetary lags are “long and variable,” most economists would have expected a 5-percentage-point rise in the funds rate over such a short time period to have slowed the economy more than what we have seen so far. And inflation readings during the summer were low enough to suggest that despite continued issues in some sectors, overall price inflation was under control.

The economy is indeed slowing. But GDP still appears to be growing faster than its long-run potential—the growth rate that can be sustained in the long run. And job growth has slowed, but the economy continues to add jobs at rates that are much greater than the underlying growth of the labor force. GDP and employment growth will have to slow even more sooner or later to reflect longer-term trends. In our forecast, we estimate that labor force growth will fall to around 500,000 per year in the coming years. The level of job growth consistent with full employment would then be just 41,000 per month. Increased immigration and unusually high growth in labor force participation could allow faster job growth, but it would be hard to bet on either of these scenarios.

On the face of it, this would seem to call for even more Federal Reserve (Fed) tightening, as slow labor force growth keeps the job market tight. But two problems arise. First, those “long and variable lags” of monetary policy tightening suggest the possibility that a slowdown is already embedded in economic decision-making. Of course, many economists have been saying this for about a year, and they have been wrong. That’s why we are seeing the current bout of optimism. But what if the economy finally comes to the point when the impact of past monetary policy starts to show up? After all, it’s been less than two years since the Fed started raising interest rates. Second, Fed tightening has already created fragility in financial markets. The Fed doesn’t intend to create a recession by sparking a financial crisis. The higher it raises interest rates, however, the more likely such a crisis becomes.

Despite all those possible reasons for gloom, the US economy is coming into fall with continued growth, lower inflation, and the possibility that all that talk about recession was, in the end, just that—talk.

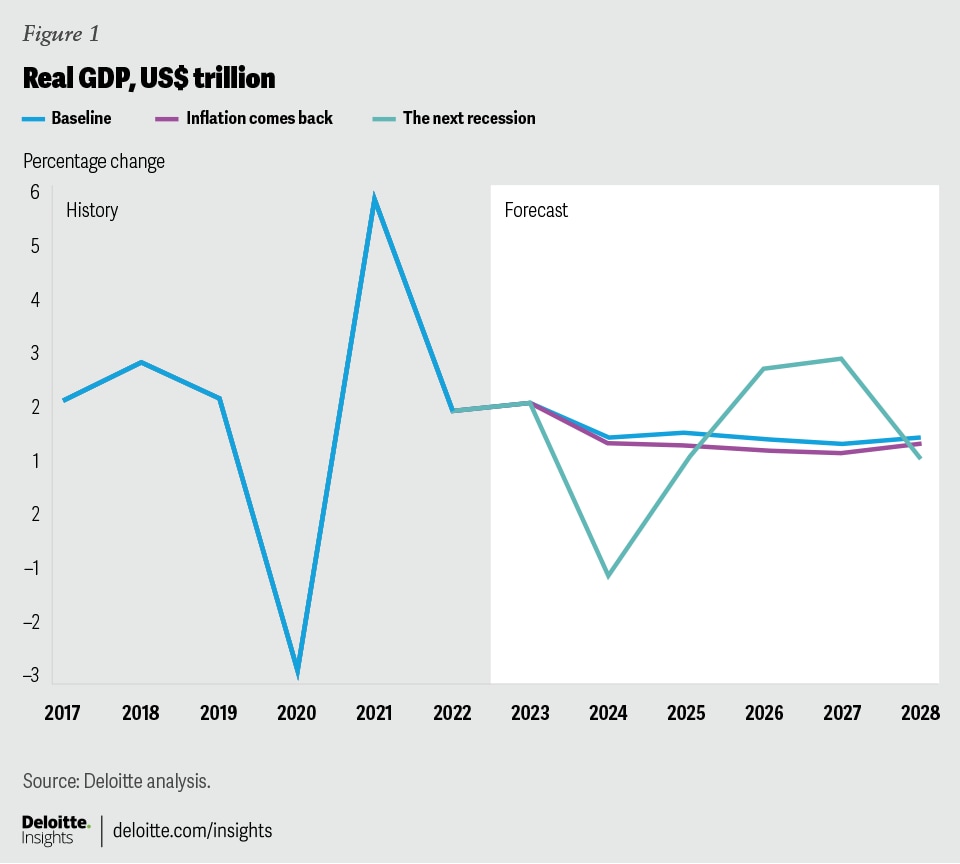

Scenarios

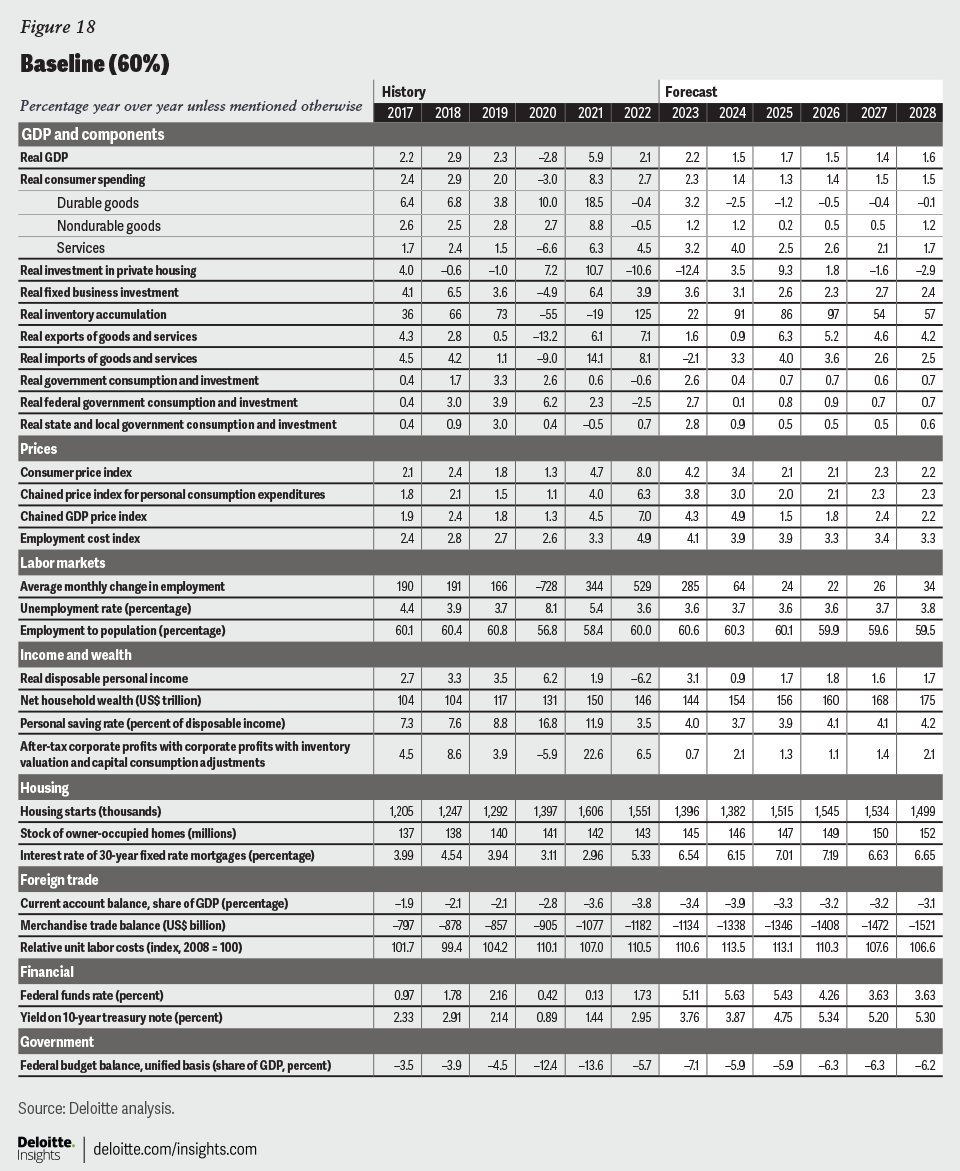

Baseline (60%): Economic growth slows to the potential rate of around 1.5% to 1.6%, while inflation moderates to below 3% by 2025. This long-desired “soft landing” is accompanied by a stable labor market, despite slowing job growth. Slow growth in Europe and China, higher energy prices, and an expensive dollar have not proven to be strong enough headwinds to push the US economy into recession, or even to slow it below potential. Some sectors, however, do experience weakness. High interest rates and market saturation reduce demand for consumer durables and housing. Investment in nonresidential structures remains weak, as the oversupply of office buildings and retail space weighs on the market. Construction of manufacturing structures—encouraged by efforts to build chip plants in the United States as well as alternative energy production—offsets this weakness.

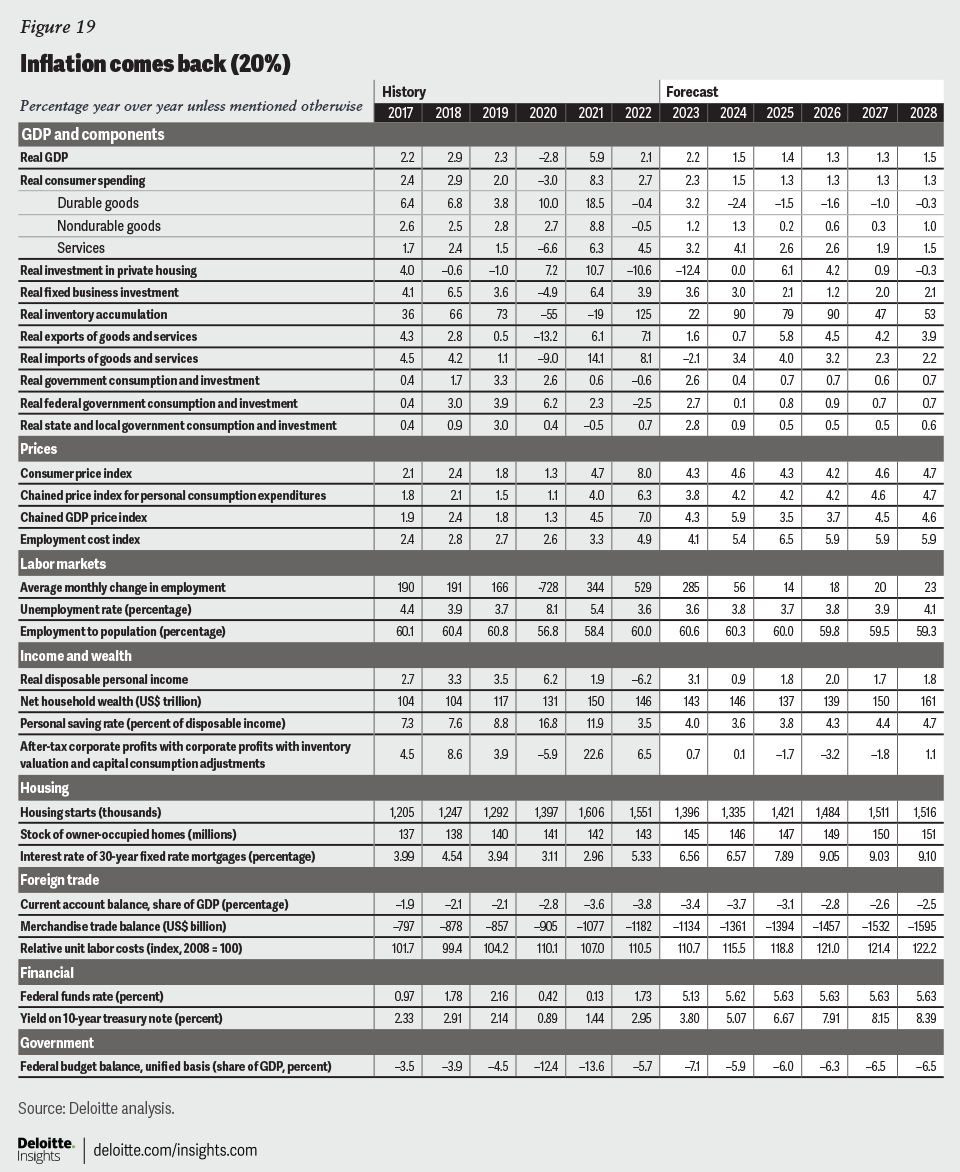

Inflation comes back (20%): The decline in inflation due to decreasing supply chain pressures proves to be temporary. Continued strength in the labor market pushes wages up, leading to higher costs and prices. The Fed, having attempted to slow inflation through shock therapy in 2022 and 2023, proves reluctant or unable to continue the effort, which presents significant dangers to the financial system. Inflation settles in at about 4.5%. Although short-term interest rates remain moderate because of the Fed’s reluctance to create more risk, long-term rates continue to rise as inflation expectations move up. By 2026, mortgage rates are over 9.0%, with the expected impact on housing. The combination of high interest rates and uncertainty slows growth, and the unemployment rate gradually rises over the forecast horizon.

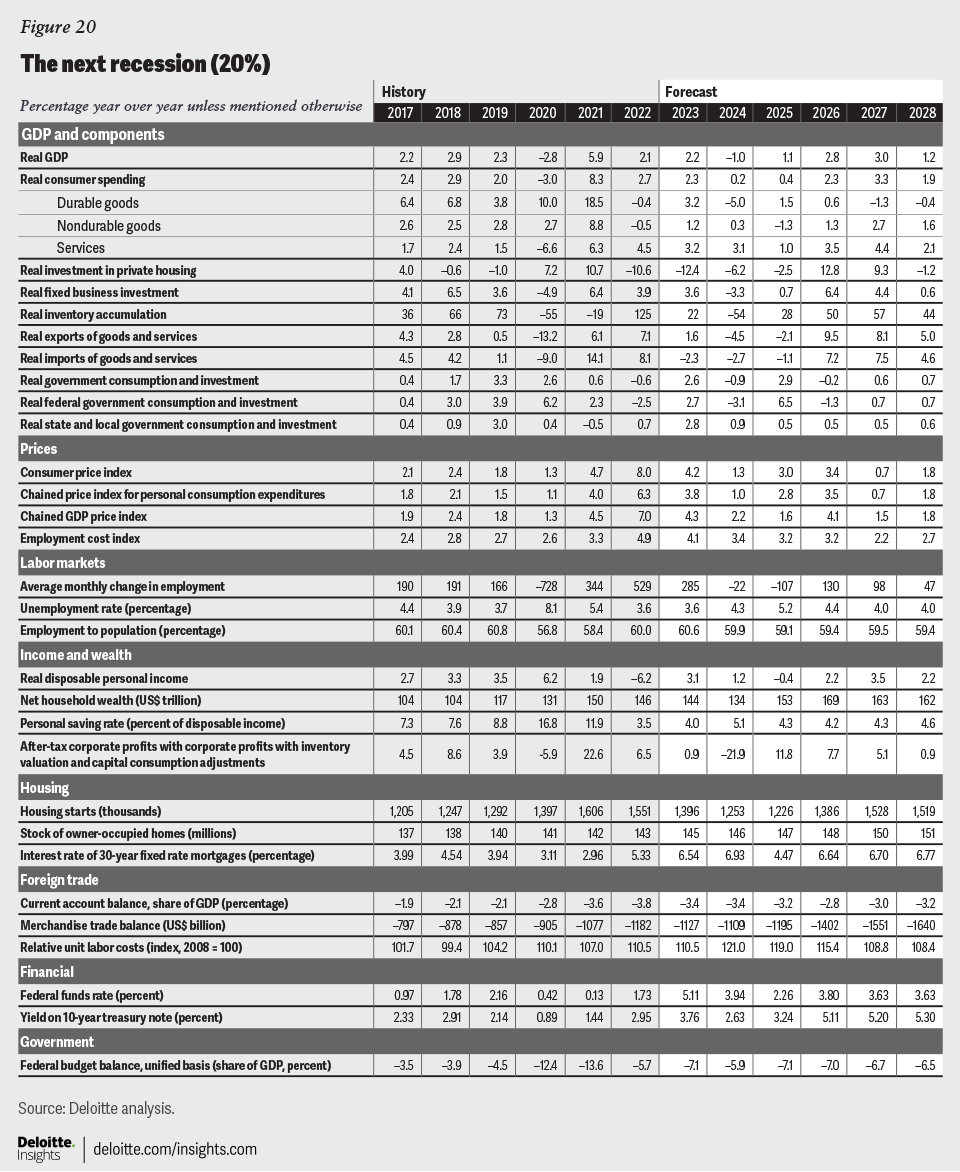

The next recession (20%): The Fed’s focus on inflation leads it to minimize risks to the economy until it is too late. Although the financial shock is smaller than in 2008, the already weak economy contracts a substantial 1.9% by the end of 2024. The unemployment rate rises to 5.2% in 2025, which alleviates some—but not all—of the pressure on the job market. The Fed eases monetary policy and the economy starts growing in 2026.

{kind=link}

Sectors

Consumer spending

The near-term outlook for consumer spending turns on two big questions:

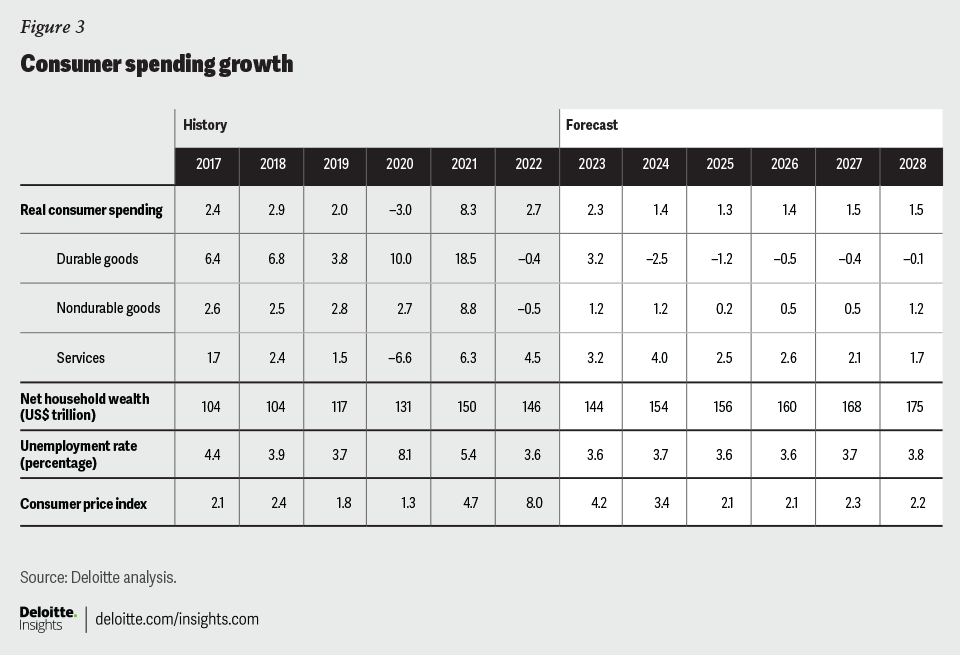

1. What will happen when consumers finish running down their pandemic savings?

In 2020, during the height of the pandemic, we estimated that households saved about US$1.6 trillion more than we forecasted before the pandemic. Most of that money has been spent, as the savings rate has dropped from an average of around 9% before the pandemic to around 4.5% in the second quarter of 2023. Many households still have more cash on hand now than they normally would want, but how much of that will they spend as the economy slows? One possibility is that many consumers will remain cautious and hold on to those savings even as they are able to go out and spend. However, the households without savings have been running up their credit card debt—and those card balances have become a lot more expensive, with most cards charging over 20% on unpaid balances. An additional headwind to spending is the fact that households with student loan debt will need to divert funds to serve that debt—money that now will not be supporting additional consumption.

The baseline Deloitte forecast assumes that consumer spending will continue to grow, but slow to about 1.5% per year.

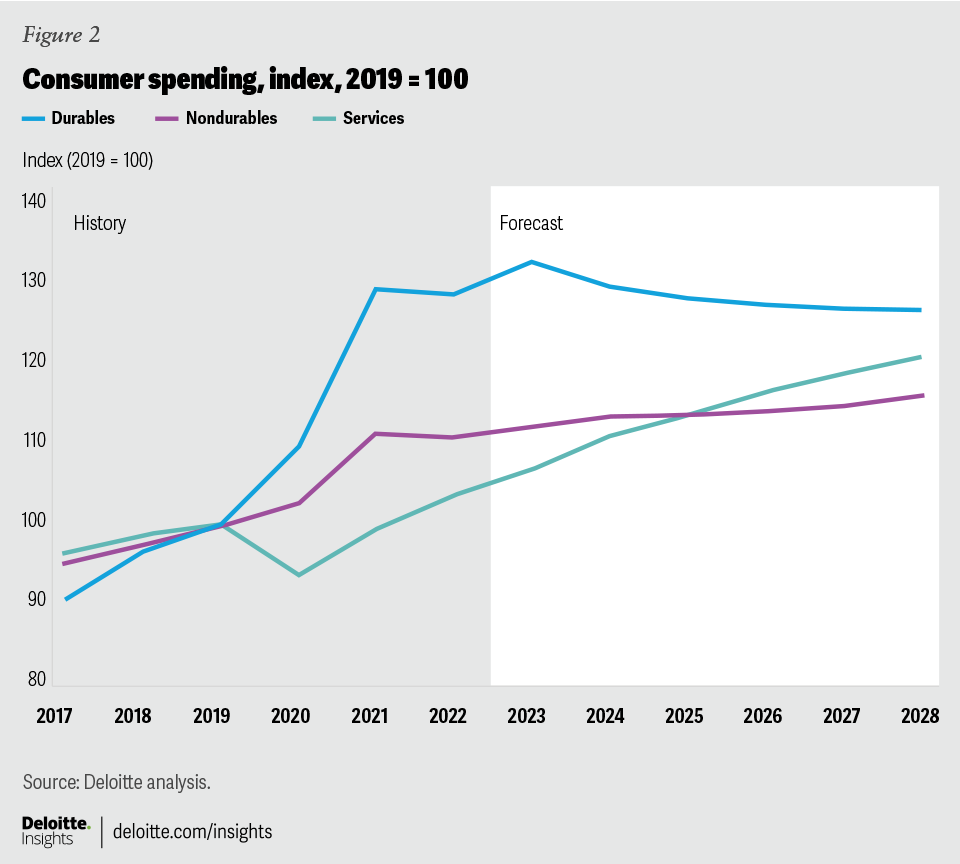

2. As consumer services recover, what happens to durable goods?

The pandemic sparked a remarkable change in consumer spending patterns. Spending on durable consumer goods jumped US$136 billion in 2020, while spending on services fell US$473 billion over the same period. Households substituted bicycles, gym equipment, and electronics for restaurants, entertainment, and travel. This trend started reversing after mid-2021, and by the end of 2022, real durable goods purchases were down over 4%. However, consumer purchases of durable goods have started growing again. With the exception of motor vehicles, this trend seems unlikely to continue. If consumers just return to their prepandemic spending patterns, durable consumer goods sellers will be looking at a 20% fall in spending. And consumers could conceivably spend even less, since the durable goods they previously bought aren’t going to wear out that quickly.

Deloitte’s forecast assumes that durable goods spending starts to fall over the next few years as consumer spending “renormalizes” and consumers resume spending on services. While services spending grows more quickly, total consumer spending slows to a level slightly below the rate of household income growth, as the excess savings households accumulated during the pandemic period are exhausted.

There is a silver lining for some households in the tight labor-market/high-inflation environment of the past couple of years. Low-wage workers have seen real wages go up, while high-income workers have experienced the greatest erosion in the value of their pay.6 It remains to be seen whether this reduction in inequality will continue, but it’s certainly welcome news to lower-wage workers.

Retirement remains a significant concern for many workers: Even before the crisis, fewer than four in 10 nonretired adults described their retirement as on track, with a quarter of nonretired adults saying they had no retirement savings.7 As the population ages, many people are likely to find it difficult to afford the retirement they expect.

{kind=link}

{kind=link}

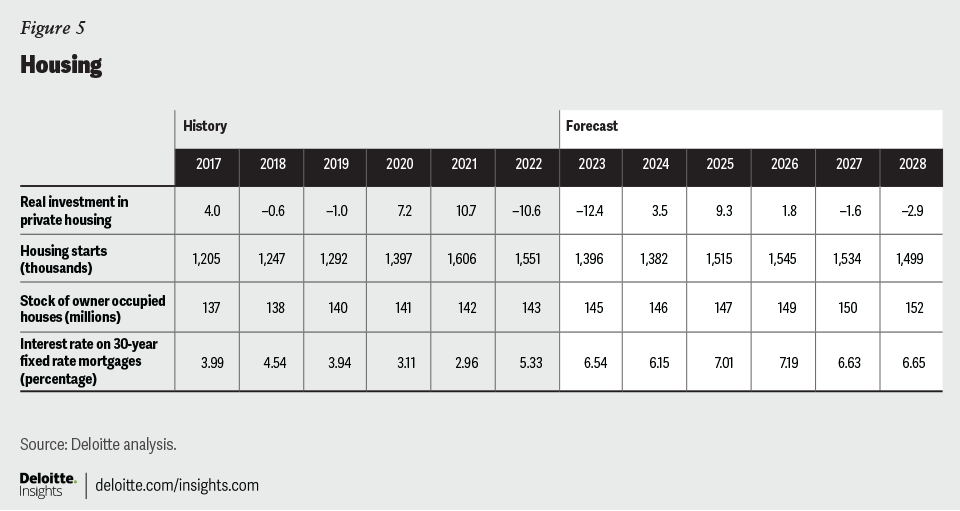

Housing

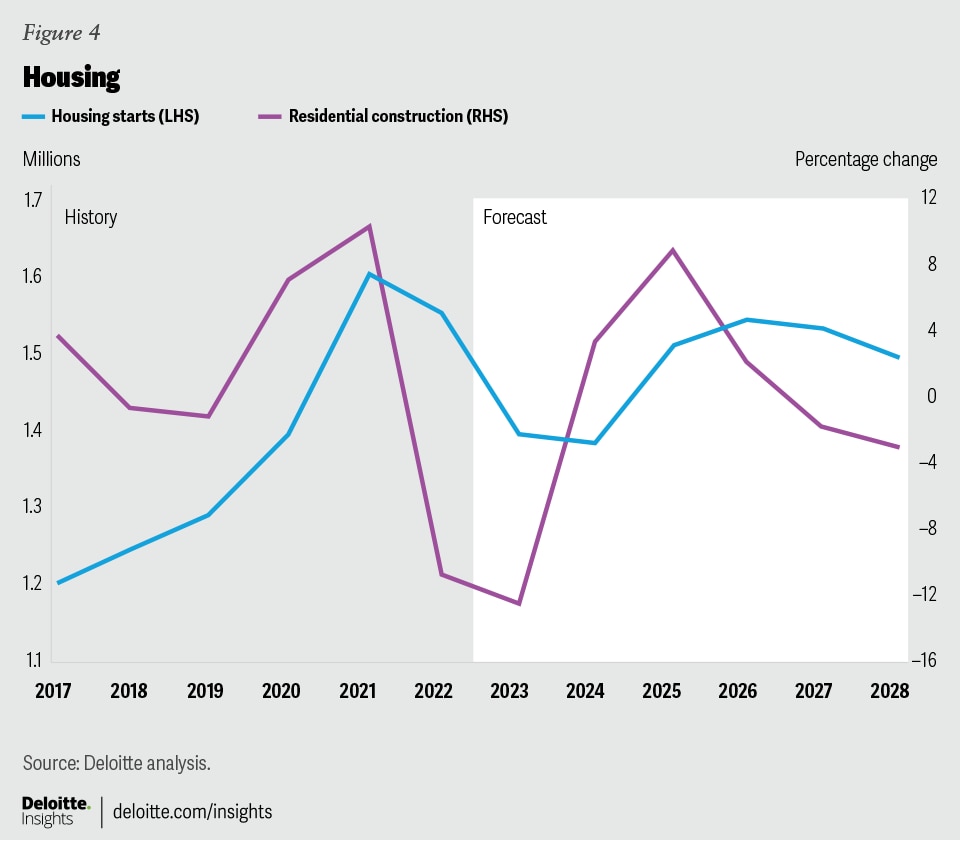

The housing sector outperformed the broader economy in the wake of the pandemic, as buyers and sellers found ways to navigate the pandemic’s restrictions. Then the tables turned. As the Fed raised interest rates and inflation appeared, long-term interest rates moved up dramatically. The result was a decline in housing starts from 1.7 million (at an annual rate) in Q1 2022 to less than 1.4 million Q1 2023. And house prices, which rose sharply starting in the middle of 2021, appear to have stabilized, at least for the time being.

The runup in house prices created a huge housing affordability problem. Unfortunately, the moderation in house prices over the past year won’t solve the affordability problem because mortgage rates have moved up substantially. Don’t be too worried, however; some research suggests that homeownership patterns for younger families aren’t that different from those of previous generations.8

Our forecast shows the fall in residential construction continuing through the end of this year. Housing construction is then forecast to bounce back, but only modestly; by 2025, housing starts reach our estimated equilibrium of about 1.5 million units per year.

Demographics suggest that housing is not likely to become a key driver of economic growth in the foreseeable future. Population growth has slowed to less than 0.5% per year (compared to over 1% during the housing boom in the 2000s). The baseline forecast assumes that, after the recovery from the current housing downturn, housing starts will begin to fall. Faster medium-term growth in housing would require faster population growth, most likely from immigration. Otherwise, the heightened demand for housing during the pandemic is likely to be a short-term phenomenon.9

{kind=link}

{kind=link}

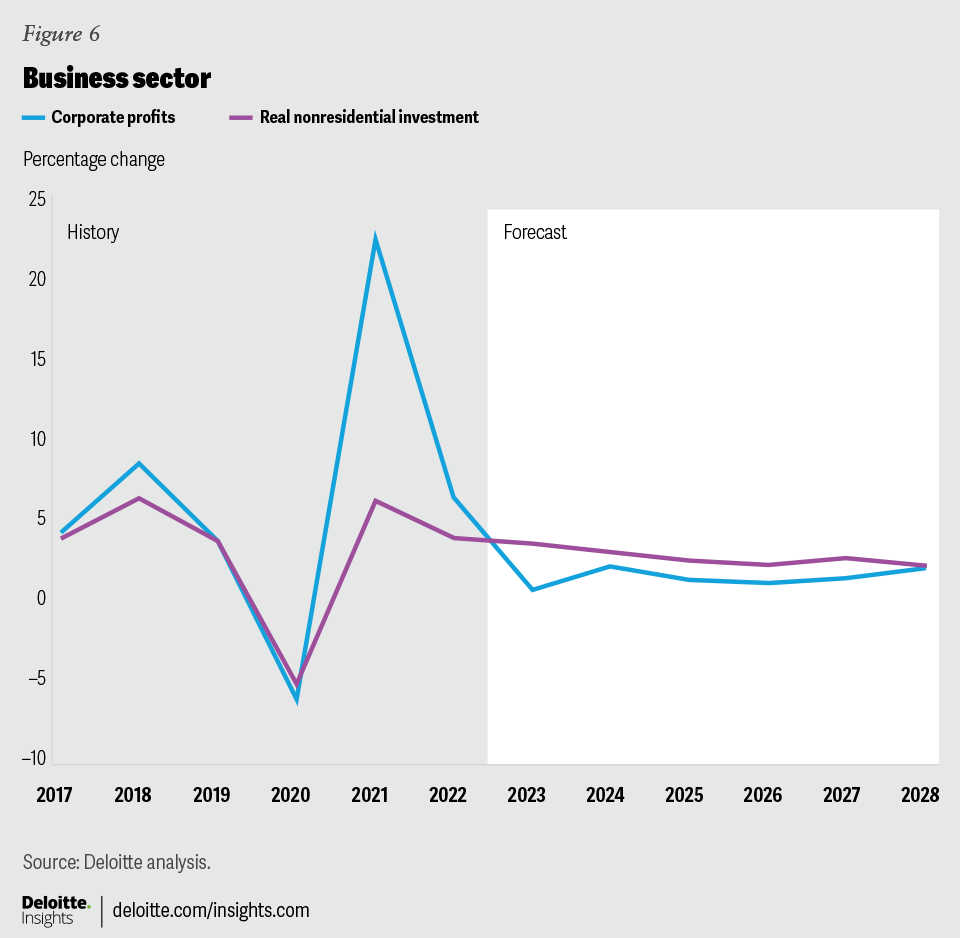

Business investment

Businesses have ramped up investment since the initial impact of the pandemic, but they have been selective about what they are investing in.

Investment in nonresidental structures fell more than 20% between the pandemic and the third quarter of 2022. Prospects in many nonresidential building sectors remain grim. The business case for office buildings and retail space has diminished, with online shopping and the shift toward working at home. Current talk of converting office buildings to residential spaces suggests that real estate experts don’t see a lot of room for growth in office demand.

However, the past few quarters have seen some growth in nonresidential construction. Mining structures investment has picked up in response to higher oil prices. The surprise here is that mining didn’t grow earlier and faster. But the more surprising contributor to growth is manufacturing structures. Recent legislation—the CHIPS and Science Act and the Inflation Reduction Act—provide significant incentives for increasing manufacturing capacity in the United States. And those incentives do seem to be creating demand for investment in manufacturing.

Investment in equipment has been slowing. After rising over 10% in 2021 and 4.3% in 2022, equipment investment has been flat during the first half of 2023. Since the pandemic, equipment investment has been dominated by transportation equipment and information technology (IT) equipment. Remote work makes IT equipment (and software) a substitute for buildings, and so the counterpart to weak investment in commercial structures is a lot of investment in IT. That need was particularly strong as companies moved to more virtual work over the past few years. But now that the initial investments have been made, we are seeing a slowdown in investment in information processing equipment. Some of this weakness has been offset by continued fast growth in investment in transportation equipment.

Investment in intellectual property (which consists primarily of software and R&D) remained strong during and after the pandemic. That’s mostly because of investment in software, and it likely reflects in the investments needed for teleworking. We expect this category to remain strong over the next few years as businesses continue to require software to accompany their investments in information processing equipment.

Future investment is likely to gradually switch in response to incentives to invest in climate change remediation. Such investment may not appear as profitable as past investment. Current methods of measuring the economy, and corporate profits, don’t correctly measure the cost of climate change, or the benefits from reducing greenhouse gas emissions.10 US government policy is now pointing companies toward more investment in climate remediation, and an increasing share of business investment spending is likely to be dedicated to this goal.

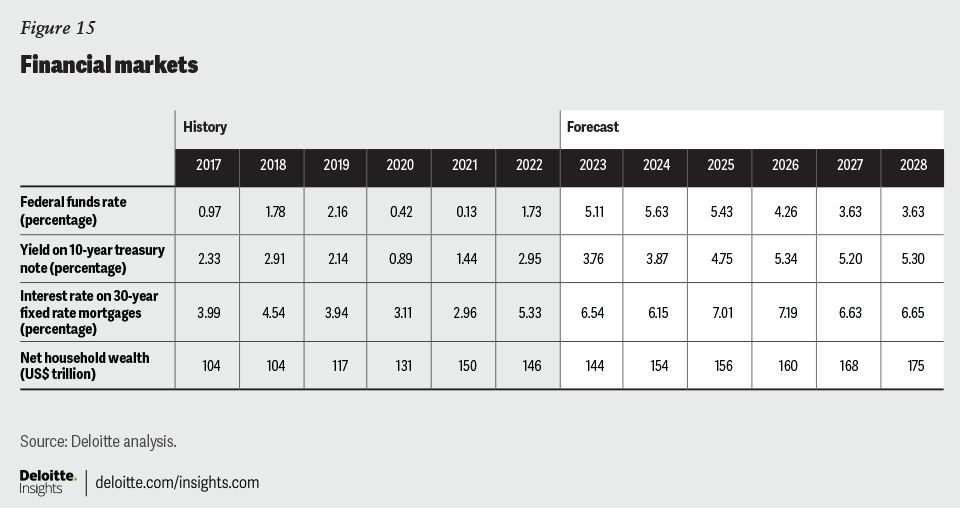

Financing investment is becoming a bit pricier as long-term interest rates rise. However, many nonfinancial businesses are sitting on a pile of cash. In our baseline forecast, the AAA corporate bond rate rises to just under 6% and stays there through the end of the forecast horizon. Although that may appear high, historically it is not that high. And continuing innovation in areas like artificial intelligence will help to raise the demand for capital. On top of that, the need for investments in climate remediation may be quite costly. The International Monetary Fund mentions estimates of US$3-US$6 trillion of spending per year required through 2050.11 US business are likely to find plenty of uses for capital, even at interest rates that remain elevated above the prepandemic level. Our forecast has nonresidential investment spending growing faster than GDP through the forecast horizon.

{kind=link}

{kind=link}

Foreign trade

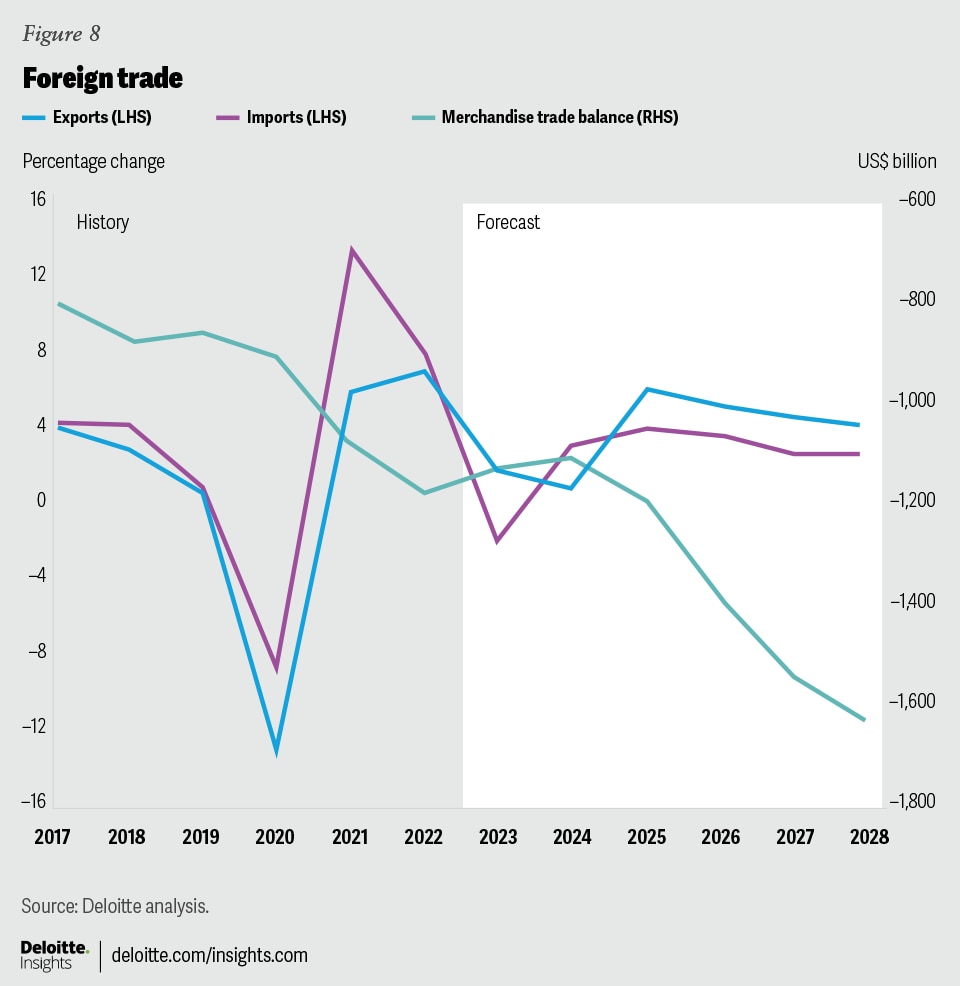

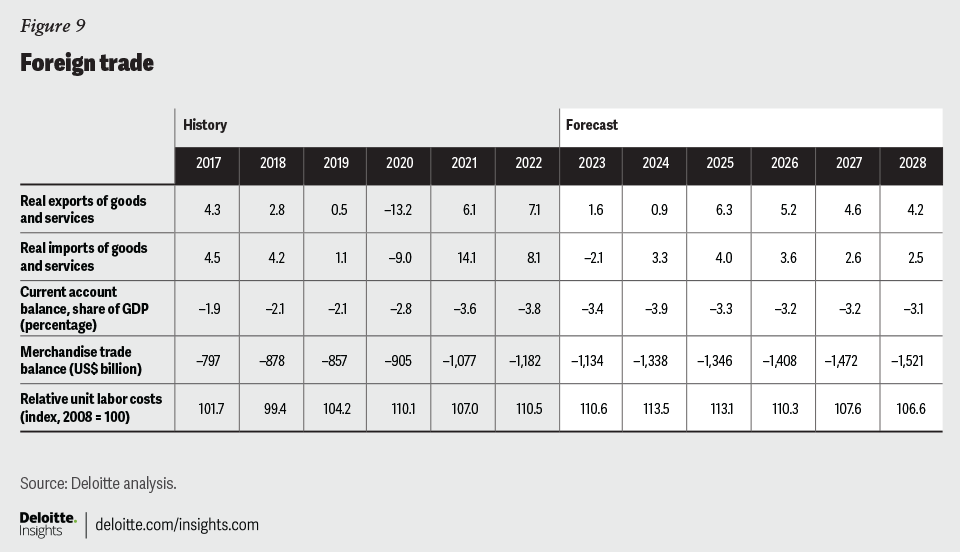

Recent US trade data has been surprisingly strong considering that both China and Europe—two major drivers of the global economy—are experiencing slower than expected growth. After contributing to growth for the last four quarters, net exports were slightly negative in Q2 2023. And that’s despite a relatively strong dollar coupled with high inflation. Petroleum products are part of the story. But exports of automobiles and related products, consumer goods, and capital goods have all grown surprisingly fast over the past year.

Our forecast shows US exports growing at a good pace over the five-year horizon as the dollar falls (due to a reduction in global risk) and growth picks up abroad. Imports, however, will be restrained by the fall in demand for consumer durables.

There is a lot of talk about “deglobalization,” meaning a reversal of the dramatic increase in international trade that occurred in the past few decades. Global exports grew from 13% of global GDP in 1970 to 34% in 2012 and have stabilized at that level. More recently, the pattern of trade has changed. US imports from China have fallen, and US imports from other Asian countries are growing. This suggests that, while trade patterns may be changing, the United States remains as fully connected to the rest of the world as it has been in the past.12 In 2022, exports accounted for 8.6% of GDP, above the 8.2% average in the five years before the pandemic.

{kind=link}

{kind=link}

Government policy

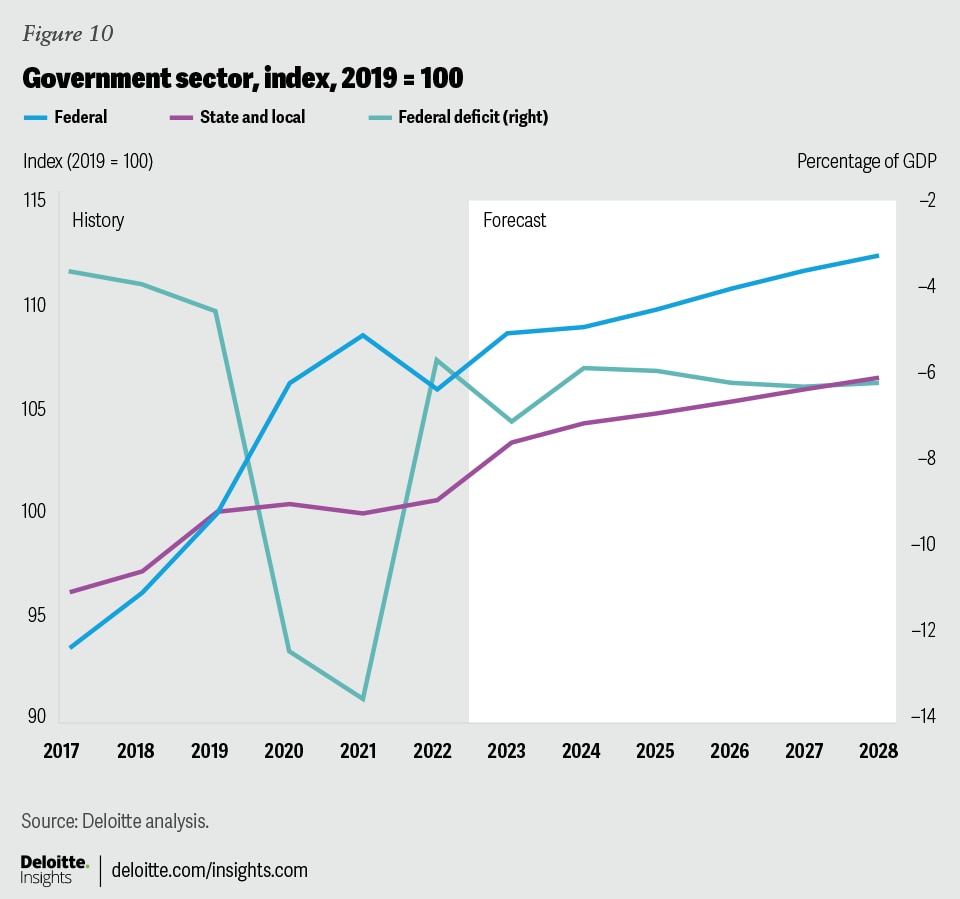

Funding the federal government remains a source of significant risk for the economy. Although the budget deal provided an agreed-upon blueprint for House and Senate spending bills, it is becoming less likely that both houses can agree on the details for the 12 appropriations bills by October 1. There is a risk—accounted for in our recession scenario—that the US government could experience a shutdown. To have a significant economic impact, the shutdown would have to last for longer than any past shutdown, a possibility that is also included in our recession scenario.

Looking beyond the immediate problems of finance, the earlier Infrastructure and Jobs Act and Inflation Reduction Act will boost government spending over the next 10 years. This spending will increase the capacity of the economy, although it might not show up as faster productivity growth.13 However, much of this additional spending comes toward the end of our forecast horizon, and consequently, the short-term impact on the forecast is minor. Also, the amount of spending is relatively modest compared to the economy as a whole. According to the Congressional Budget Office (CBO), in 2026, the peak year of spending, the Infrastructure and Jobs Act will add about US$61 billion to the federal deficit.14 That amounts to about 0.2% of projected GDP. These initiatives are likely to have a positive and significant impact on public capital in the United States, but they are not a large fiscal stimulus by any means.

Our baseline forecast assumes deficits will rise to over US$2 trillion by FY28. That’s a hefty amount, one that inevitably raises the question of whether the US government can continue to borrow at such a pace. The answer is that it can—at least until investors lose confidence. At this point, most investors show no sign of concern about the ability of the United States Treasury to repay US debt.

Eventually, however, the US government will face a crisis if it does not eventually find ways to reduce the deficit and consequent borrowing. The crisis may be many years away, and current conditions may argue for waiting. It would, however, be a bad idea to wait too long once those conditions lift.

{kind=link}

{kind=link}

Labor markets

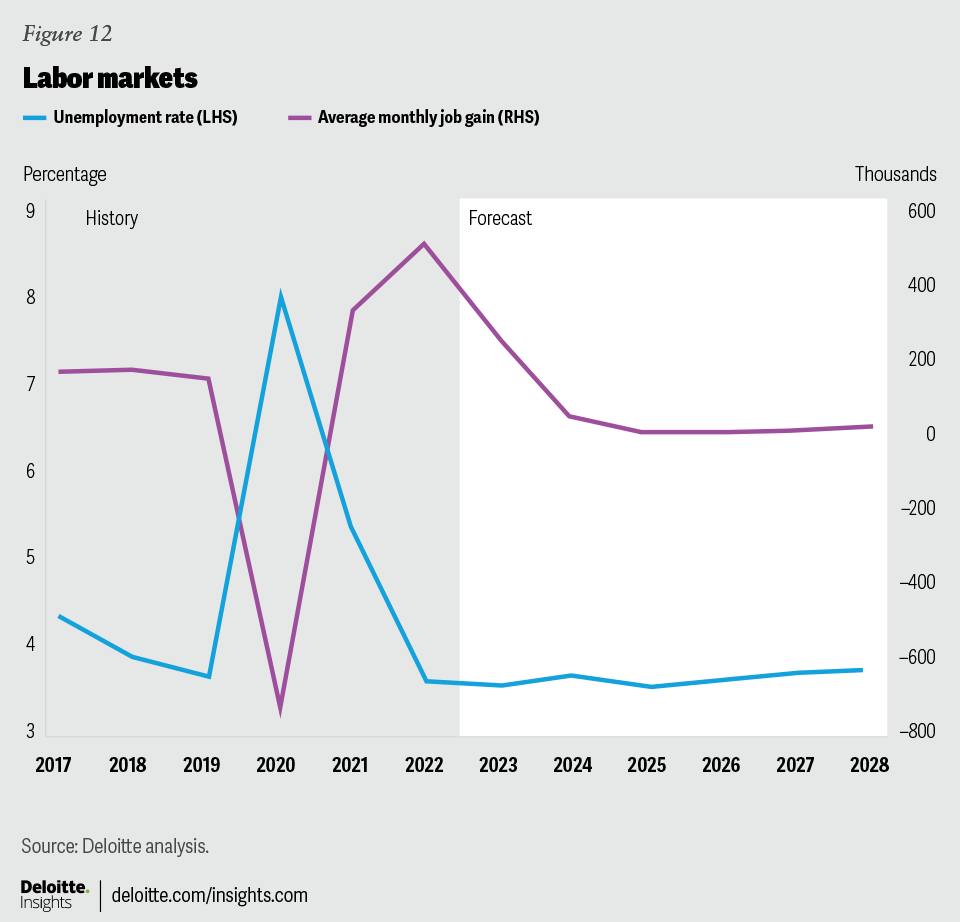

The labor market is slowing—but is still hot. The unemployment rate remains low, and the three-month average rate of job growth was 218,000 in July, substantially above the 50,000 jobs that we estimate would meet the long-run growth of the labor force. The slowing is likely to continue, but the baseline scenario assumes that labor markets remain tight over the forecast horizon.

While employment has fully recovered from the pandemic, total labor force participation has not. However, the labor force participation rate for people under the age of 65 hit the prepandemic level in April. Most of the workers who left the labor force are older Americans. Many of these people have probably retired, in the sense of expecting to remain permanently out of the labor force, but some can likely be enticed back with the right compensation packages and flexible working hours and conditions.

As is the case in many areas, the pandemic accelerated trends that were evident even before it started. Slow labor force growth and continued high demand had already created conditions that required companies to offer higher wages to lower-skilled workers and to be more imaginative about hiring. In the post–COVID-19 world, companies that make extra effort to find the workers they need and provide conditions to attract those workers will have an important competitive advantage.

Deloitte’s baseline forecast assumes that job growth slows to sustainable levels in the next few years. It’s important to remember that job growth is likely to slow simply because there aren’t enough workers. That means slowing employment growth—if the unemployment rate remains low—is not necessarily a signal of an economic downturn. Over the longer horizon, labor force growth slows to just 0.2% per year, presenting continuing challenges for employers. It’s a demographic fact that employers will have to learn to live with.

{kind=link}

{kind=link}

Financial markets

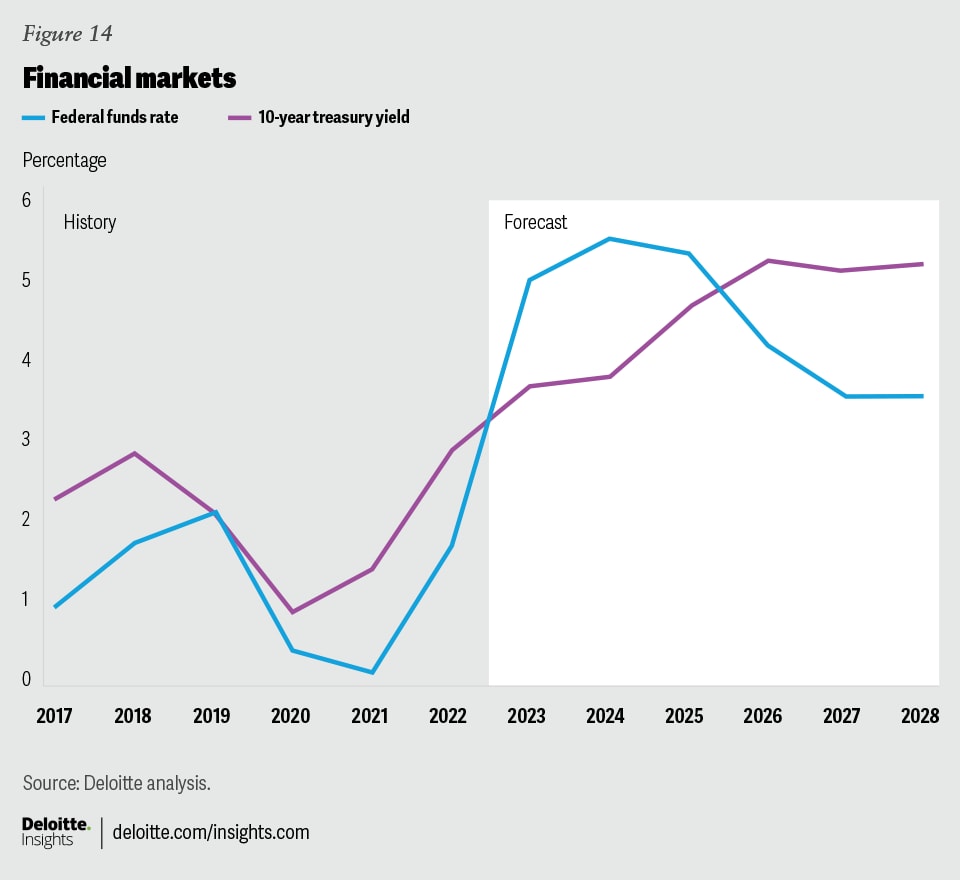

The key question for financial markets over the next few years is whether long-term interest rates will once again settle in at a relatively low level, or whether they will return to levels consistent with the experience before the global financial crisis. Those arguing that interest rates will return to low levels point to fundamentals such as demographics (the aging global population) and slowing innovation growth.15 Those arguing that interest rates will return to previous behavior point to the slowing of savings growth from China and the need for large investments (whether public or private) to reduce the impact of climate change.16 The Deloitte forecast assumes that long-term interest rates remain relatively high as demand for capital remains strong, while global savings grow more slowly over the coming years.

Short-term rates play a smaller role in the long-term outlook, but a larger role in the minds of people following financial markets. Our baseline forecast assumes one more Fed hike this year. Then, with inflation slowing and the possibility of higher interest rates weakening the financial system, the Fed stops raising rates. Given our relatively optimistic forecast for GDP and employment in the baseline, the Fed does not start lowering the funds rate until late 2025, and then gradually eases until it reaches 3.6%, which is our estimate of the long-term neutral rate. Demand for capital for investment (including significant government and private outlays on climate change) keeps the 10-year rate from falling, and it reaches its long-run value of around 5% by 2025. This outcome is consistent with the historical relationship of these rates under moderate inflation: Should inflation continue to be high, the spread between the 10-year note and the Fed funds rate could continue to rise (as investors account for expected inflation in the later years of the note’s period). Investors should watch out for the possibility of higher interest rates—although by the standards of the 1970s and 1980s, these rates are still quite low.

{kind=link}

{kind=link}

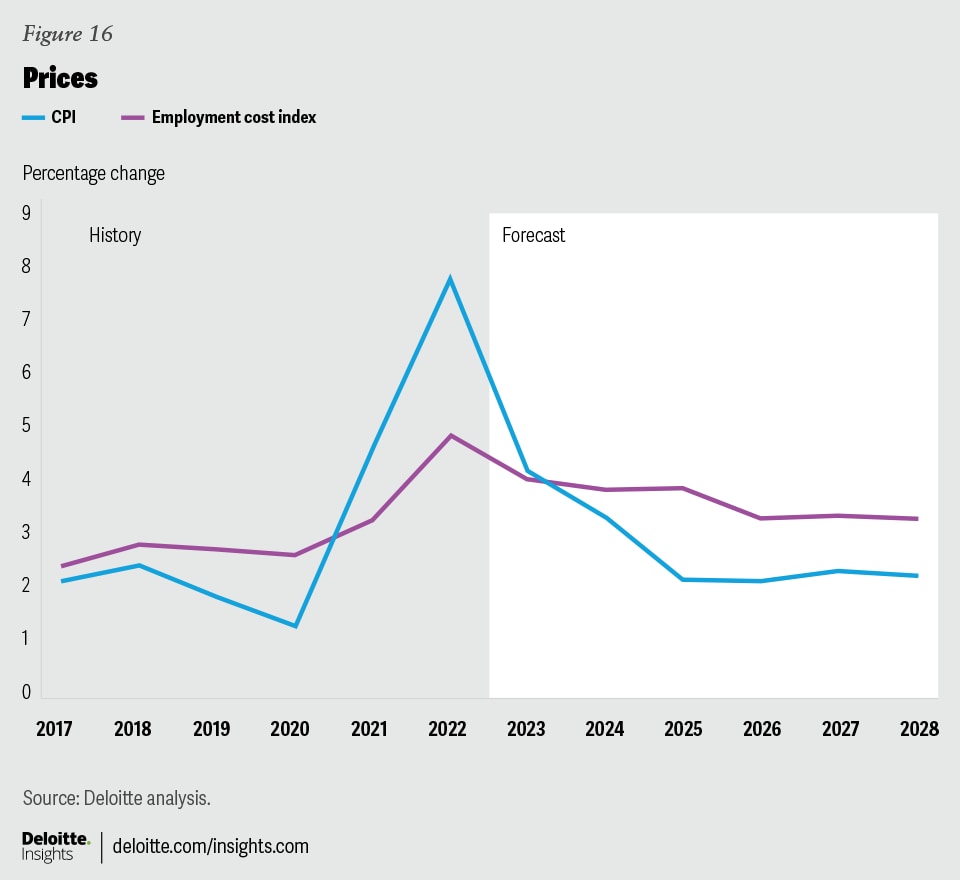

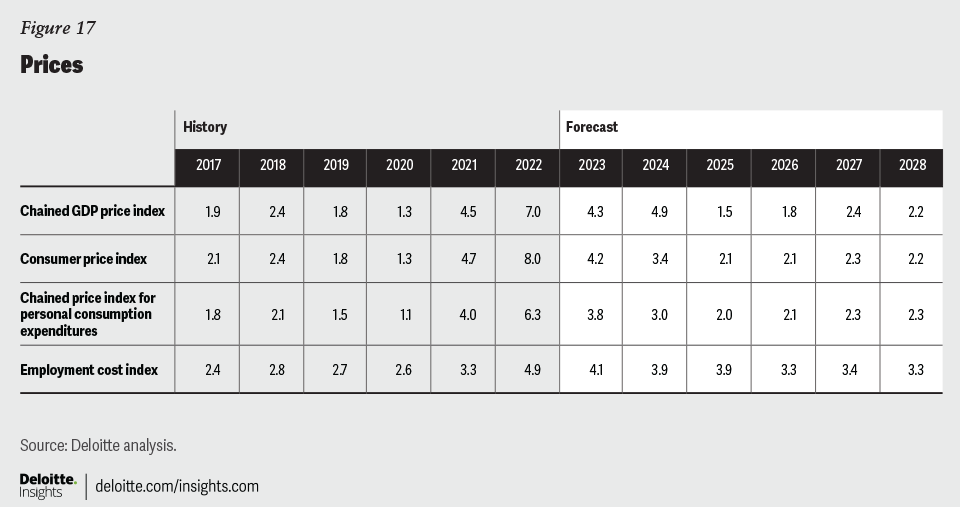

Prices

Inflation is closer to the Fed’s target than you might realize. The low inflation reported in June and July reflects a decline in the underlying trend, with some estimates of trend inflation now below 3%.17 The year-over-year inflation rates often cited in the press are higher, but the period they cover includes a lot of “old news.” It’s certainly too early to completely declare victory. But—absent another shock like the Russian invasion of Ukraine—inflation appears to be at manageable levels.

The Deloitte forecast continues to assume that the current inflation is “transitory” in the sense that it will dissipate over time. Our baseline forecast shows CPI inflation falling to below 3% by late 2024. We remain optimistic that today’s households and businesses will likely avoid the unpleasant experiences of long inflation and painful disinflation that their predecessors experienced during 1970–1985.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}