United States Economic Forecast

The US economy remains strong with robust consumer spending and high business investment, but its future trajectory largely hinges on the policies of the incoming administration

The US economy has had the strongest recovery from the COVID-19 pandemic of any major developed economy. Annual inflation is approaching the Federal Reserve’s target without a recession, non-managerial real wages have exceeded pre-pandemic trends, consumer spending is continuing to exceed expectations, investment in factories is at record levels, and the United States is a net exporter of petroleum products.1

Against this backdrop, in January a new administration will take charge of government. Initial market response to the news was favorable,2 with the expectation that the new administration will be able to build on the economy’s strong foundations and unlock further growth. At the same time, there remains uncertainty around the potential implications of economic policies of the incoming administration.

During the campaign, the president-elect proposed a range of economic policy changes.3 Our baseline scenario anticipates that many of these policies will not be implemented in their most maximalist forms. For instance, while we expect the introduction of some new tariffs, we do not foresee the implementation of the across-the-board tariffs that were occasionally floated during the campaign. Similarly, while we expect there may be an increase in deportations of undocumented immigrants, legal immigration levels could remain relatively unaffected.

However, this forecast is among the most uncertain in recent times, so we include two alternate scenarios to capture a full range of possible outcomes for the coming years. Our upside scenario reflects markets’ positive reactions to the election, and includes tax cuts, increased investment and productivity, and a minimum of harmful tariffs. Our downside scenario, on the other hand, includes a wide range of tariffs, significant deportations, and sweeping cuts to government spending.

Scenarios

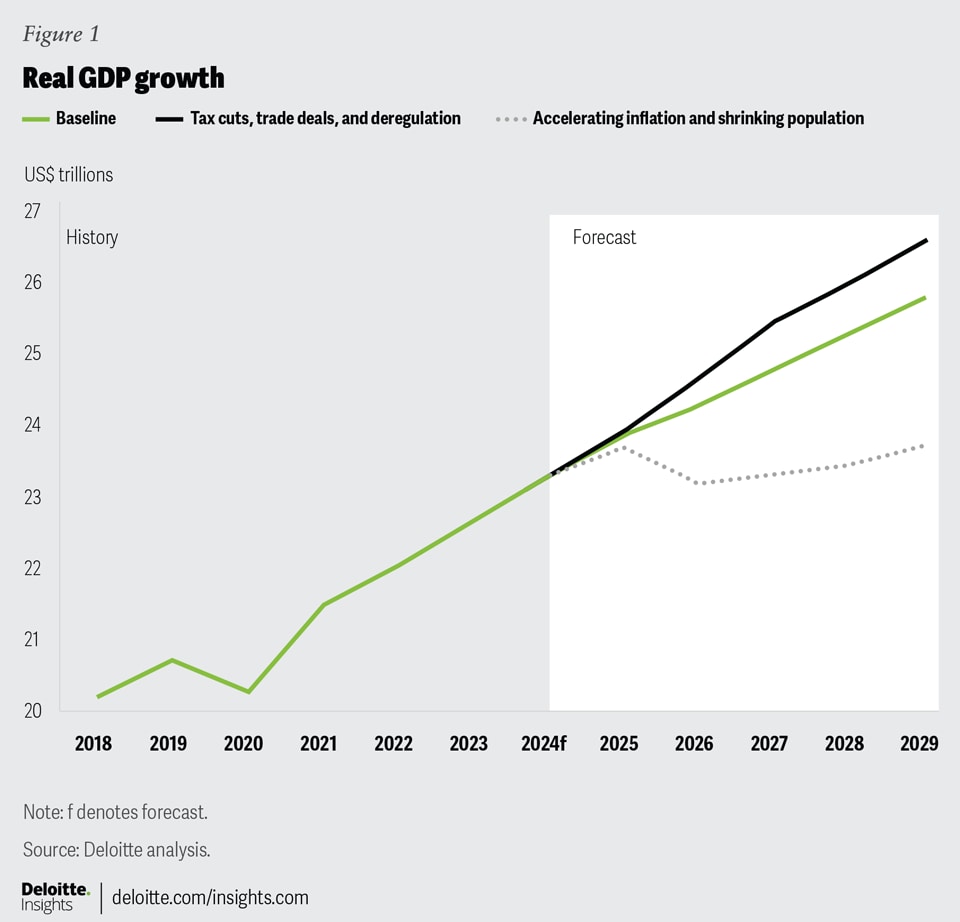

Baseline (50%): In our baseline scenario, we expect the new administration to be judicious in how they implement their campaign promises. We foresee new tariffs on China and some targeted tariffs on other trading partners, but none on Canada or Mexico, and many categories of goods—such as food and energy products—will be spared. Similarly, while we expect deportations to run above their current levels, this scenario does not foresee millions of deportations as this would cause food prices to rise given that nearly half of the agricultural workforce is made up of undocumented immigrants;4 voter anger with high food prices was a significant factor in the election outcome, and the new administration is expected to be sensitive to that. Significant government spending cuts are enacted, but these are not enough to change the overall economic picture. There are also some easy wins: Tax cuts under the Tax Cuts and Jobs Act (TCJA) are extended, and the Fed remains independent.

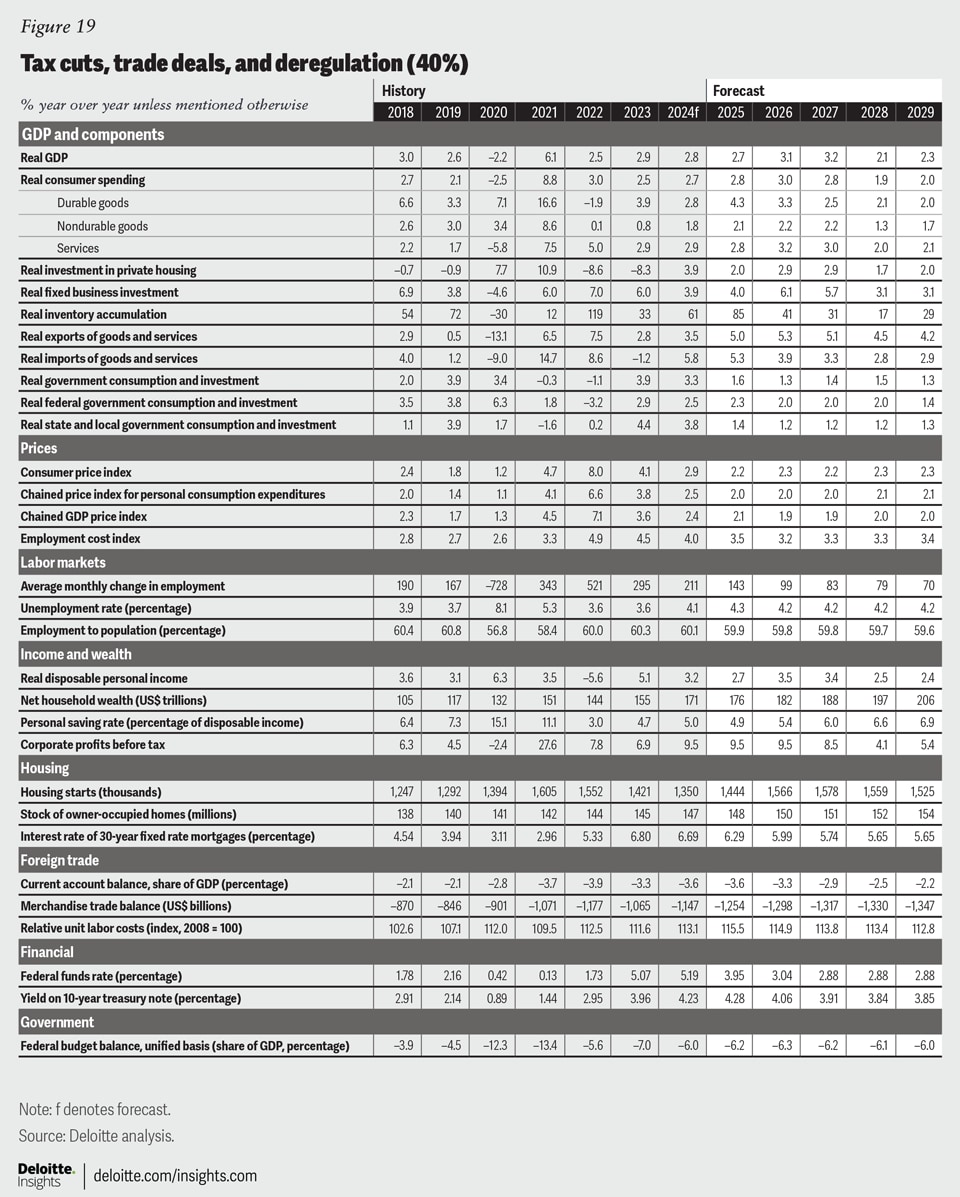

In this scenario, individuals and businesses front-load some trade activity in 2025 to avoid tariffs, with exports growing by 3.2% and imports growing by 4.4%. Once tariffs take full effect in 2026, both exports and imports grow by just 0.7%. The inflationary effects of tariffs mean inflation rises again, and the Fed is forced to pause rate cuts until mid-2027. Consumer spending grows by 3.1% in 2025 and 2.3% in 2026; overall consumer spending growth remains low throughout the remainder of the forecast horizon, averaging 1.8% per year as deportations hold back population growth. Government spending cuts are fully implemented in the 2026 fiscal year and further subtract from growth. Overall, our modeling shows real GDP growth of 2.4% in 2025 before slowing to 1.7% in 2026. GDP growth then ranges from 1.9% to 2.1% between 2027 and 2029.

Tax cuts, trade deals and deregulation (30%): Markets reacted positively to the election results. Investors clearly believe the new administration can unlock a new level of growth through tax cuts and deregulation. In this scenario, we examine what might happen if these hopes come true. The TCJA tax cuts are extended, and the corporate tax rate is lowered to 15% for domestic producers as per a campaign promise,5 prompting a boost in investment. That additional investment, as well as the successful introduction of novel technologies like AI to workplaces, results in a productivity boom. We see this scenario as about equally as likely as the baseline.

We include minimal new tariffs in this scenario, working on the theory that the president-elect will use the threat of tariffs to successfully strike new trade deals on favorable terms. In addition, businesses convince the administration to limit deportations in the name of keeping prices low.

In this scenario, GDP will rise more rapidly than the baseline forecast through to 2029. Between 2025 and 2029, this scenario expects GDP to rise at an average annual rate of 2.7%, which is 0.7 percentage points above the average in the baseline forecast. With fewer tariffs in place, this scenario also predicts lower inflation compared to the baseline, stronger consumer spending starting in 2026, and a lower merchandise trade deficit. However, due to the inflationary impact of the tax cuts, inflation does settle around 2.3% per year by the outer years of the forecast, higher than in the status quo ante. Finally, with fewer deportations, labor markets will not be as greatly impacted as in the baseline. The labor supply will rise above the levels in the baseline scenario, and consequently, so will employment, limiting the gains in the unemployment rate.

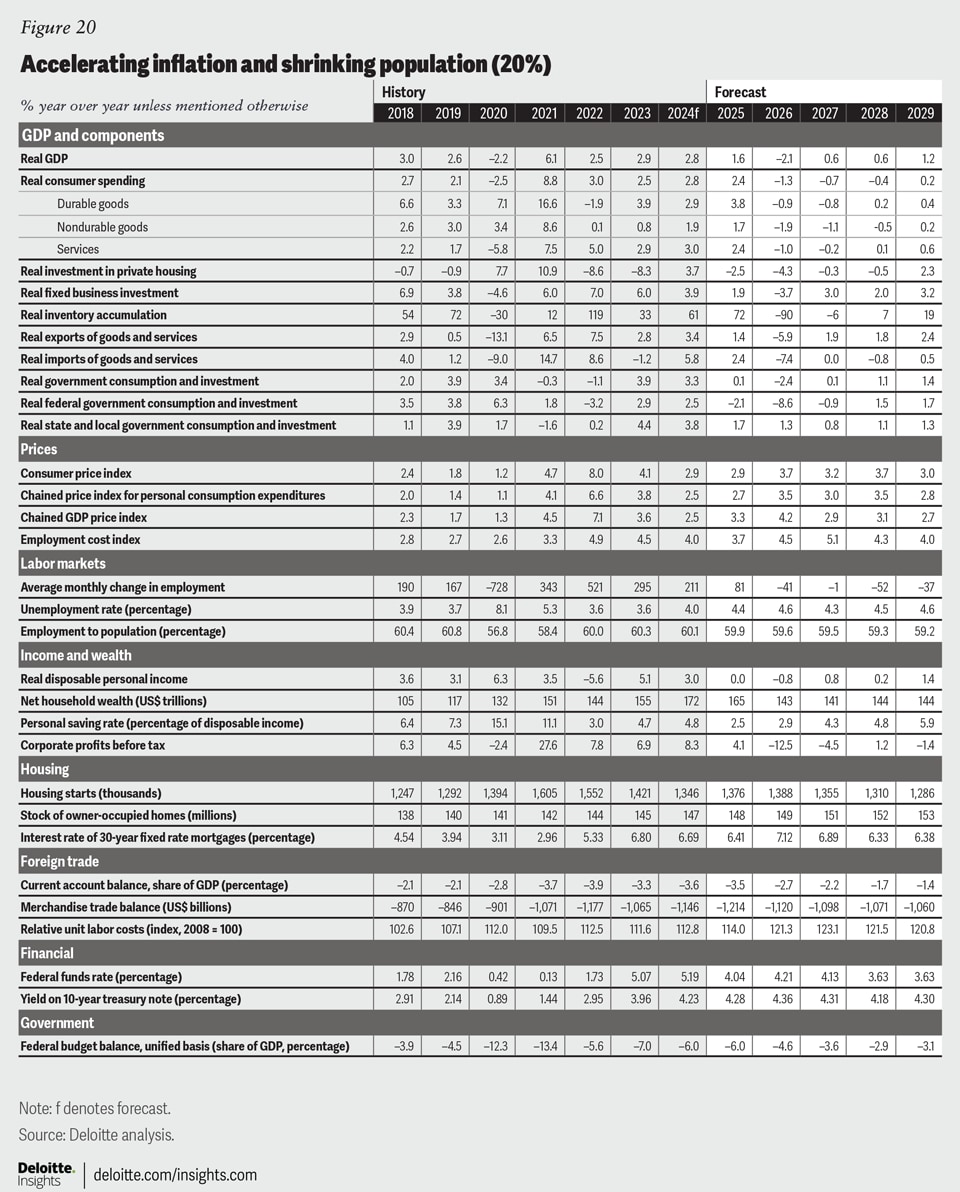

Accelerating inflation and shrinking population (20%): While our baseline expects some policy changes from the incoming administration, it reflects a relatively minimalist version of what was promised on the campaign trail. There is a possibility that some of the more impactful policy proposals could be implemented in full, and we therefore model an alternate scenario where many promises are implemented more fully.

The full range of promised tariffs (60% on all goods from China, 20% on goods from all other trading partners6) are introduced, resulting in a major reduction in both exports and imports and a broader economic slowdown. Deportations reach 1 million people per year and legal immigration levels are cut in half, with the result that the US population is lower in 2029 than it is today. A total of US$1.35 trillion is cut from federal government spending, achieved through deep cuts to Medicaid transfers, social security payments, and income security programs, representing a big decrease in the living standards of millions of Americans.

Overall, economic growth slows considerably to 1.6% in 2025 before the economy suffers an outright contraction of 2.1% in 2026, a recession of similar magnitude to those we experienced in 2020 and 2009. The economy is expected to run weaker for longer as rising trade tensions and the sustained enforcement of the new immigration policy keep consumption growth in the red for most of the forecast. Inflation also trends higher for longer, peaking at 3.7% in 2026 before easing gradually to 3% by the end of the forecast. With these inflationary pressures, we expect the Fed to enter a new rate hiking cycle in 2026 before again beginning to ease monetary policy in 2027.

To some extent, the weaker economy in this scenario is not surprising: The stated purpose of tariffs is to re-shore manufacturing to the United States, but that process will take time, so any benefits of such a policy will not be felt during the next four years. The policy of mass deportations would likely have a profound effect on industries like agriculture and hospitality, where undocumented workers make up a significant share of the total workforce. Likewise, making deep cuts to government spending and transfers will always be a net negative to the macroeconomy in the short term.

{kind=link}

Sectors

Consumer spending

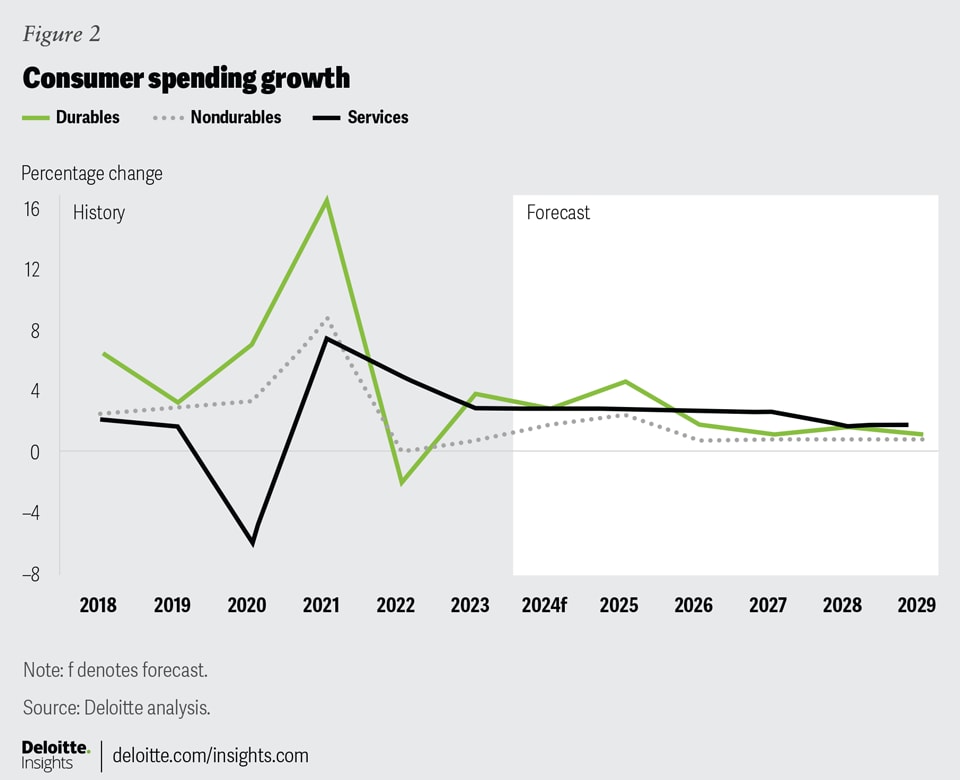

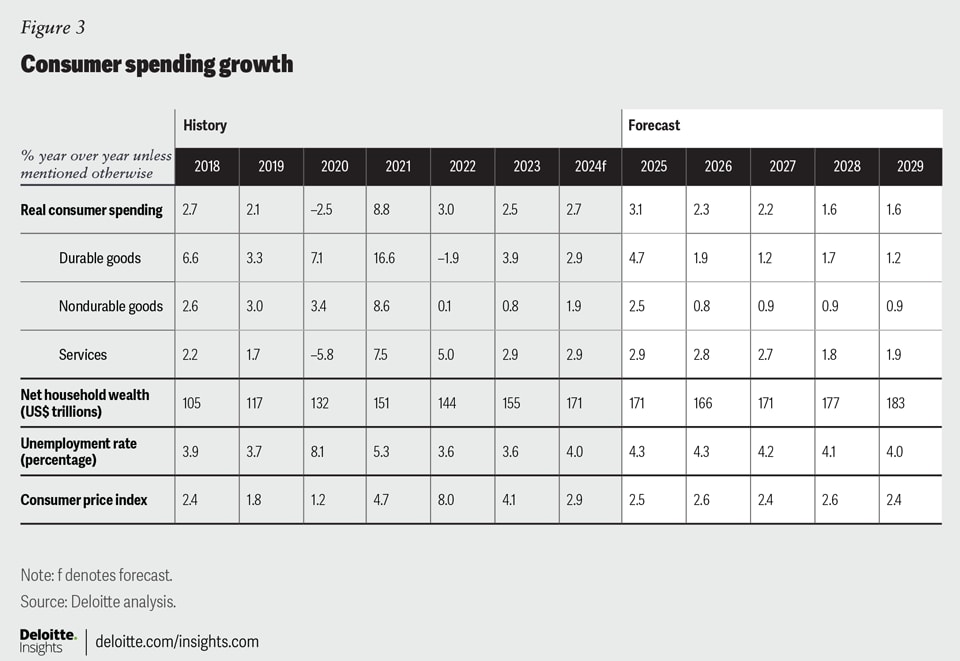

Real consumer spending remains strong. In September, real personal consumption expenditures (PCE) increased 0.4% after a 0.2% rise in August. For the third quarter of 2024, overall real PCE rose 3.7% (at annual rates), stronger than the 2.8% growth recorded in the second quarter, with spending on goods, specifically durable goods, remaining elevated. Real consumer spending on durable goods grew 8.1% in the third quarter after rising more than 5% in the second quarter of this year. Generally, increased spending on durables is seen as a signal of rising consumer confidence.

Households depleted their pandemic-era excess savings in March of this year,7 and thus gains in consumer spending in the short term are expected to be driven by growing income and the ability of households to add new debt. Household debt continued to rise, increasing by US$147 billion in the third quarter of 2024, which increased consumer’s spending capacity.8

In the coming quarters, the Fed’s expected rate cuts will make borrowing cheaper, enabling households to take on more debt, and therefore providing breathing room for households to continue spending until 2025. We also expect consumers will be doing some front-loading in late 2024 and 2025 to try to get ahead of tariffs, which we see coming into full force in 2026. Starting that year, the tariffs will impact households’ real purchasing power. Consumer spending will also be negatively affected by the broader economic slowdown caused by the tariffs and government spending cuts. Additionally, our forecasts are for aggregate consumer spending, and as deportations continue, the number of people spending money in the economy will be lower than in the status quo. Nonetheless, the underlying strength of the consumer means we do not see any outright declines in spending.

Overall, we forecast consumer spending will rise 2.8% this year and another 2.4% in 2025 before growing at a slower 1.7% pace in 2026. Lower interest rates should help boost demand for durable goods, boosting spending on that category by 4.7% in 2025 before tariffs bring growth to just 1.9% in 2026. Spending on non-durables is expected to rise by 2.5% in 2025 and 0.8% in 2026. Finally, spending on services is expected to increase by 2.9% in 2025 and by a similar amount in 2026, given that services will not be impacted by tariffs.

{kind=link}

{kind=link}

Housing

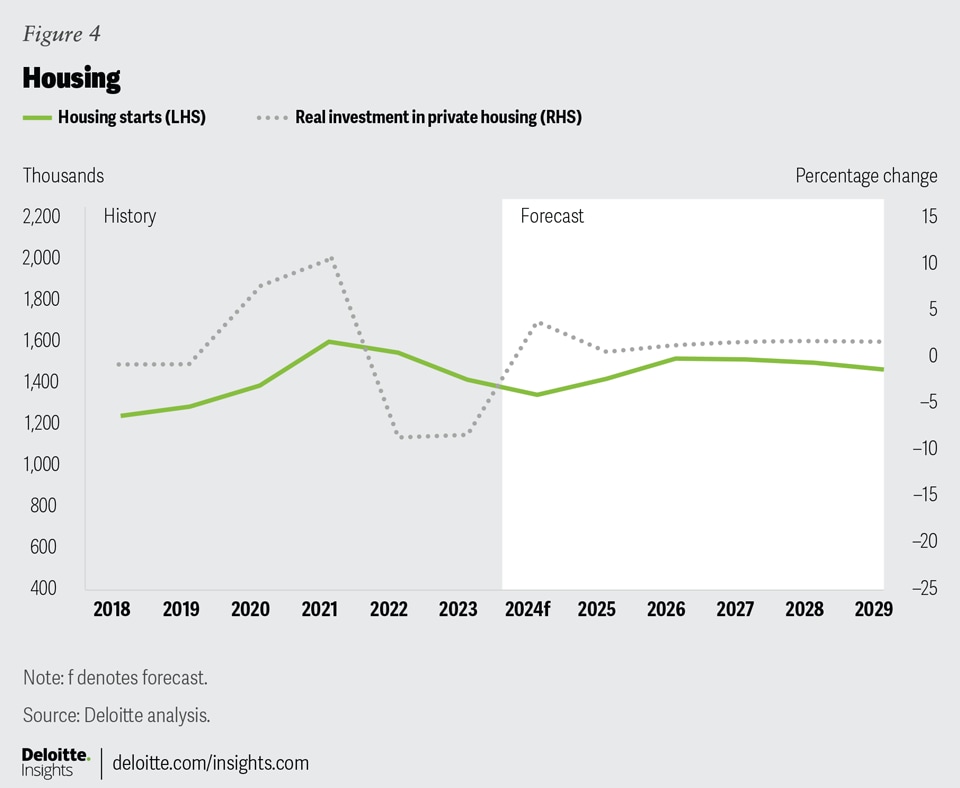

Home building has been more heavily impacted by high interest rates than other categories of investment. In October, both housing starts and building permits fell for the second month in a row, as elevated rates continue to weigh on affordability for buyers and on the ability of builders to borrow. During the 2010s, housing starts did not return to their peak levels from before the global financial crisis of 2008–2009. The long-term failure to build enough homes has contributed to the housing crisis we see today in some parts of the country, and we may have to wait for rates to drop to see a significant uptick in housing construction. One opportunity for the new administration could be to pursue something like the Creating Helpful Incentives to Produce Semiconductors (CHIPS) Act, but for building housing.

We expect housing starts to continue falling in the last quarter of this year before rising again in 2025 to 1.4 million as interest rates fall, encouraging more construction. We also anticipate housing starts to increase above 1.5 million in 2026 and remain around 1.5 million for the rest of the forecast. In 2025 and 2026, the housing stock is expected to rise more rapidly than total population, helped in part by the slower population growth.

Despite a strong level of construction in the medium term, for there to be a real impact on affordability, more of this new construction will need to be “starter homes” and will need to be built in parts of the country experiencing the largest increases in population. We expect this to continue to be a challenge. Consequently, the house price index is forecasted to rise by 4.8% in 2024, with growth expected to slow to 2.9% in 2025. In the outer year of the forecast, the house price index is expected to rise more rapidly once again.

{kind=link}

{kind=link}

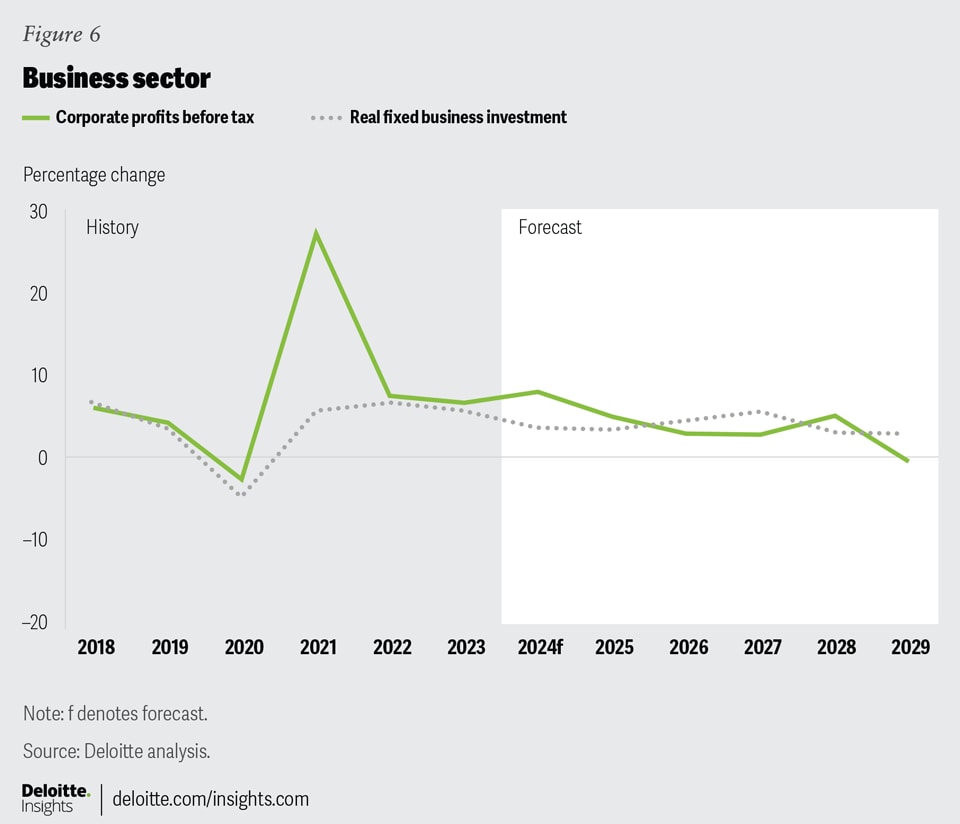

Business investment

Investment is spending that helps grow the long-term productive capacity of the economy, and as such, is the most important sector for understanding an economy’s potential. Investment in structures, which includes both buildings and engineering structures such as power plants and oil platforms, has typically followed a cyclical pattern, and is often driven by commodity price booms and economic cycles. However, the main factor driving growth in this investment class since the pandemic, especially in manufacturing construction investment, has been the passage of the Inflation Reduction Act and the CHIPS and Science Act. These pieces of legislation aimed to increase US production of strategic technologies like electric vehicles, batteries, renewable energy, and semiconductors.9 Since the passage of these pieces of legislation in August of 2022, spending on manufacturing construction has risen to historic highs, with investment in structures increasing 10.8% in 2023. Although House Speaker Mike Johnson has floated the possibility of repealing these pieces of legislation,10 we do not expect that to happen. Both pieces of legislation are popular, and their benefits are skewed toward Republican districts, making it unlikely they will be able to get enough votes for a repeal with their slim majority in the House.

As factory construction increases, so do machinery and equipment (M&E) investment and intellectual property (IP) investment, which capture everything from plant machinery and computers to software. M&E and IP investments increased significantly since the start of 2024. We predict the rise in manufacturing construction activity to continue to increase investments in M&E and IP. Overall, our forecast shows M&E investments rising 5.1% in 2025 and 5.4% in 2026. This type of spending has seen a strong upward trend over time, and we expect that strong trend growth to remain throughout the rest of the forecast period. Business investments in IP, which include not only software purchases but also research and development spending, increased significantly during the pandemic as firms adapted to new work-from-home realities. Growth in IP investment is expected to slow compared to the gains observed in 2021 and 2022 but will remain high over the course of the forecast period as many sectors incorporate artificial intelligence and other technologies.

While higher interest rates are used to combat inflation by reducing demand, they can paradoxically cause inflationary pressures to persist for longer by making it more expensive for firms to invest in the capacity to produce more and relieve supply pressures. The average corporate borrowing rate increased to nearly 7% by the end of 2023 and remained elevated through the first three quarters of 2024, presenting a barrier to firms who need to borrow to invest. However, many firms still have more cash on hand than they did before the pandemic11 and can consequently avoid borrowing at these rates. As a result, business investment has been coming in relatively strong since the start of the year. Further rate cuts from the Fed should help contribute to a positive environment for business investment. This should be felt in particularly rate-sensitive categories of investment like housing and commercial real estate, both of which have been weak during the current high-interest rate environment.

Looking ahead, markets seem to expect the incoming administration will further boost the attractiveness of business investment. All our scenarios foresee the extension of the tax cuts put in place through the TCJA, which were set to expire in 2025, as well as the lowering of the corporate tax rate and cuts to some regulations. As a result of all these factors, non-residential business investment is projected to increase 3.9% this year, 3.7% in 2025, and another 4.7% in 2026. Growth in business investment is expected to rise even further in 2027 and remain elevated in the outer years of the forecast.

{kind=link}

{kind=link}

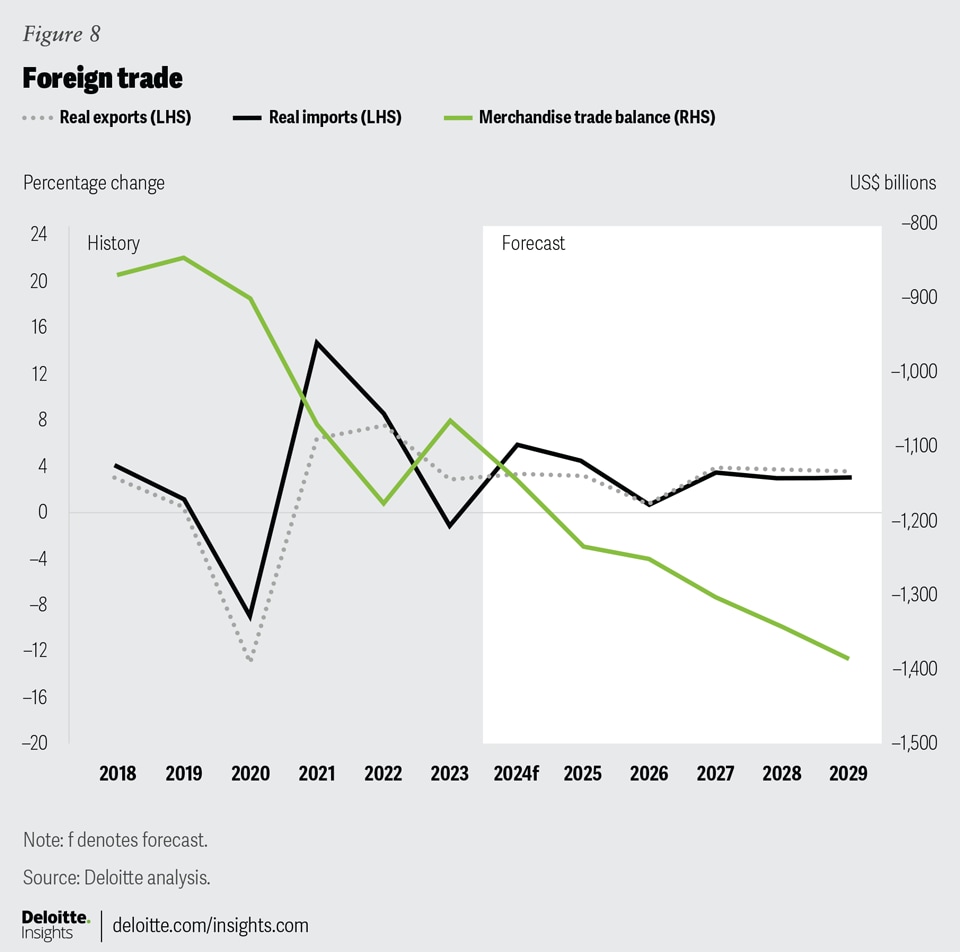

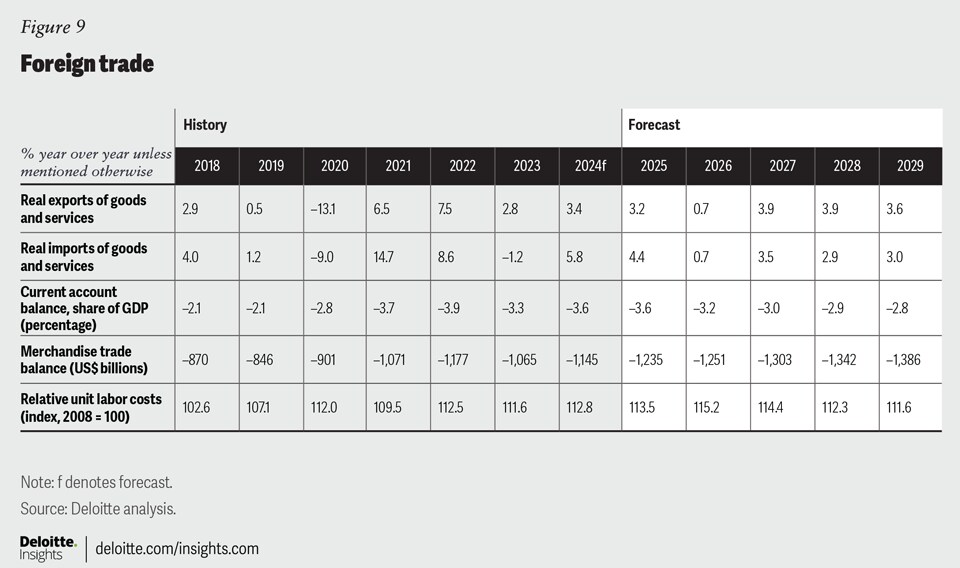

Foreign trade

Foreign trade is the sector with the biggest question mark surrounding it. The president-elect has promised to introduce 60% tariffs on goods imported from China and a 10% to 20% tariff on goods imported from all other trading partners. At present, 14% of goods imports come from China and a total of 38% of all goods imports come from countries without a trade agreement. If the proposed tariffs are only imposed on this group of trading partners, the average tariff rate on imported goods would reach 11.8%. There is some debate about whether the White House can impose these tariffs unilaterally, but at the very least they will not immediately be able to do so on goods imported from countries with which the Unites States has a free trade agreement. We expect this will provide an opportunity for countries to negotiate deals to avoid tariffs.

Additionally, there are good political reasons to expect broad categories of critical goods, such as food or energy, to be exempted from tariffs altogether. With this in mind, our baseline scenario models the impact of an average tariff of 30% on Chinese goods and an average tariff of 5% on goods imported from countries that are not part of the United States-Mexico-Canada Agreement.

Although the tariffs in our baseline scenario are less ambitious than the numbers floated on the campaign trail, their total effect is expected to be much greater than what we saw during the president-elect’s first term. The imposition of these tariffs is likely to turn into a complicated process involving individuals and businesses trying to make substitution decisions based on new relative prices. Until the tariffs take effect, we should continue to see growth in both imports and exports. We expect this will translate in a 3.1% increase in exports and a 4.4% increase in imports in 2025. Once the tariffs are officially put in place, we forecast both exports and imports to grow much more slowly: 0.7% each in 2026.

It may be a bit surprising to see that exports suffer as much as imports by the imposition of tariffs. There are a few reasons why this is the case in the short term, and why these tariffs may not have their desired impact in the long run. First, about half of imports are currently used as intermediate inputs by US businesses. It is likely to take some time for US producers to find local alternatives to the goods they are currently importing, and in the meantime, their cost of doing business will rise. This dynamic will reduce the money available to firms to invest and may drive some US producers out of business; it will also make their exports costlier and less competitive. Second, when the United States imposes tariffs on other countries’ goods, it has the side effect of causing the US dollar to appreciate, leading exports from the United States to become relatively more expensive in other markets. Tariffs will shield US producers from the import competition required to make globally competitive products. So, while they may dominate the US economy, they are likely to lose export sales, leading to limited net gain for American manufacturing.

Many of the theoretical benefits of tariffs would take much longer than four years to be realized, and so do not occur within our forecast horizon. There is not a large pool of American manufacturing production currently staffed up but sitting idle. Factories will need to be built and workers hired, both of which will take years to achieve. During this transition period when there are no US alternative goods, the cost of tariffs is likely to be borne by American households and businesses. In many cases, the reason for offshoring has as much to do with the availability of certain skills as it does cost, and reshoring all this production will require a major skills training program to ensure an adequate supply of workers.

{kind=link}

{kind=link}

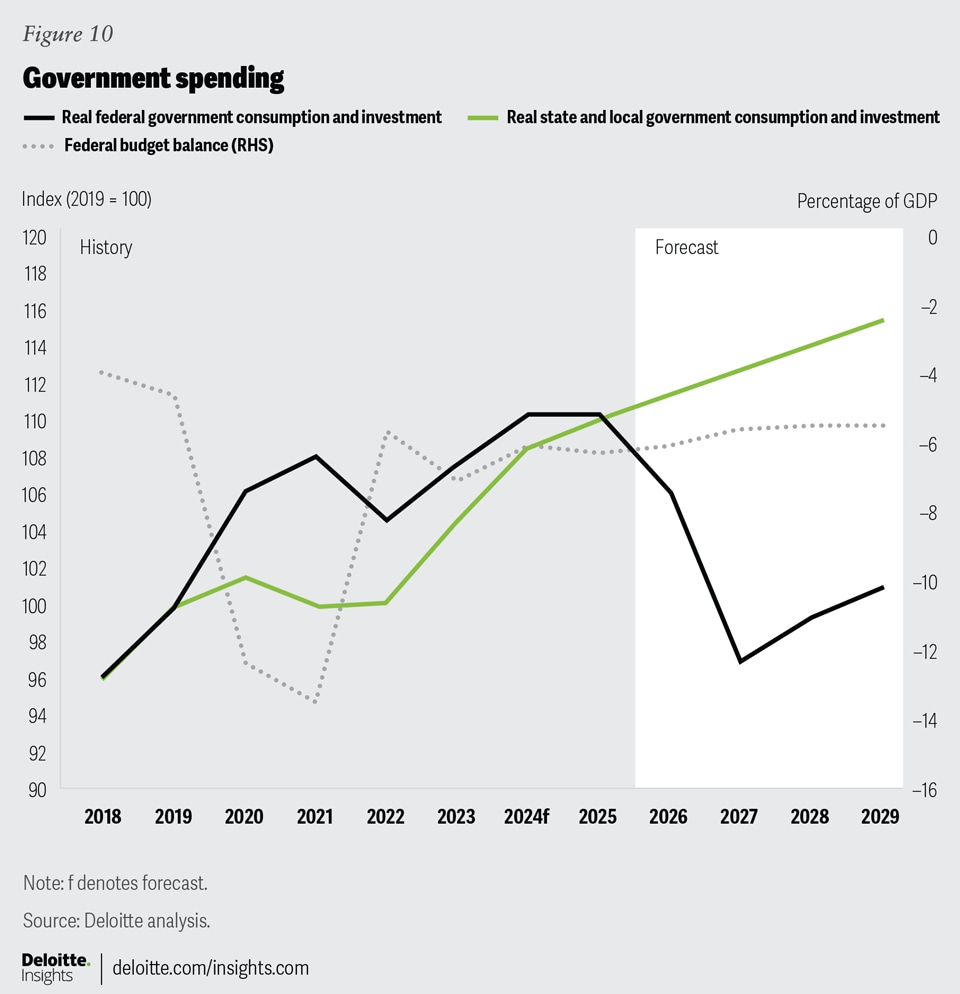

Government policy

During the campaign, the president-elect promised to make major cuts to government spending. While we can expect some spending cuts, it is very difficult to determine where and to what extent they will occur. One of the future co-heads of the proposed new Department of Government Efficiency (DOGE) promised to cut US$2 trillion in spending,12 and DOGE’s other future co-head called for the elimination of certain departments.13 The official Republican platform has explicitly promised to close the Department of Education.14

However, reaching some of the dollar amounts floated would be very difficult. Given the hawkish makeup of the president-elect’s cabinet appointees so far, it is difficult to see cuts to defense, which is the largest category of discretionary spending. The federal government spends less than US$1 trillion each year on nondefense, nondiscretionary items like education, training, housing, law enforcement, transportation, veterans affairs, embassies, the environment, and space exploration. In our baseline scenario, we assume the following cuts:

- Subsidies and transfers related to the Affordable Care Act (saving US$120 billion)

- The Department of Education (saving US$255 billion)

- Net savings of US$24 billion from cuts to other discretionary spending

Altogether, the above would save approximately US$400 billion per year, which we expect would be implemented over the course of fiscal 2026 and 2027. While other smaller cuts could occur, realistically, some of the president-elect’s promises would also lead to increased government outlays. Tariffs will bring in some additional revenue, but retaliatory action by trading partners could result in additional spending by the federal government, a dynamic we saw play out in the president-elect’s first term.15

Thus, in our baseline scenario, we forecast the federal budget deficit as a share of GDP to rise slightly from the 6% expected in 2024 to 6.2% in 2025 before falling in the outer years of the forecast as economic growth outpaces spending growth. With the deficit as a share of GDP falling in the longer term, we predict the 10-year federal bond rate will decrease to 3.9% in 2029 after rising in the short-term.

{kind=link}

{kind=link}

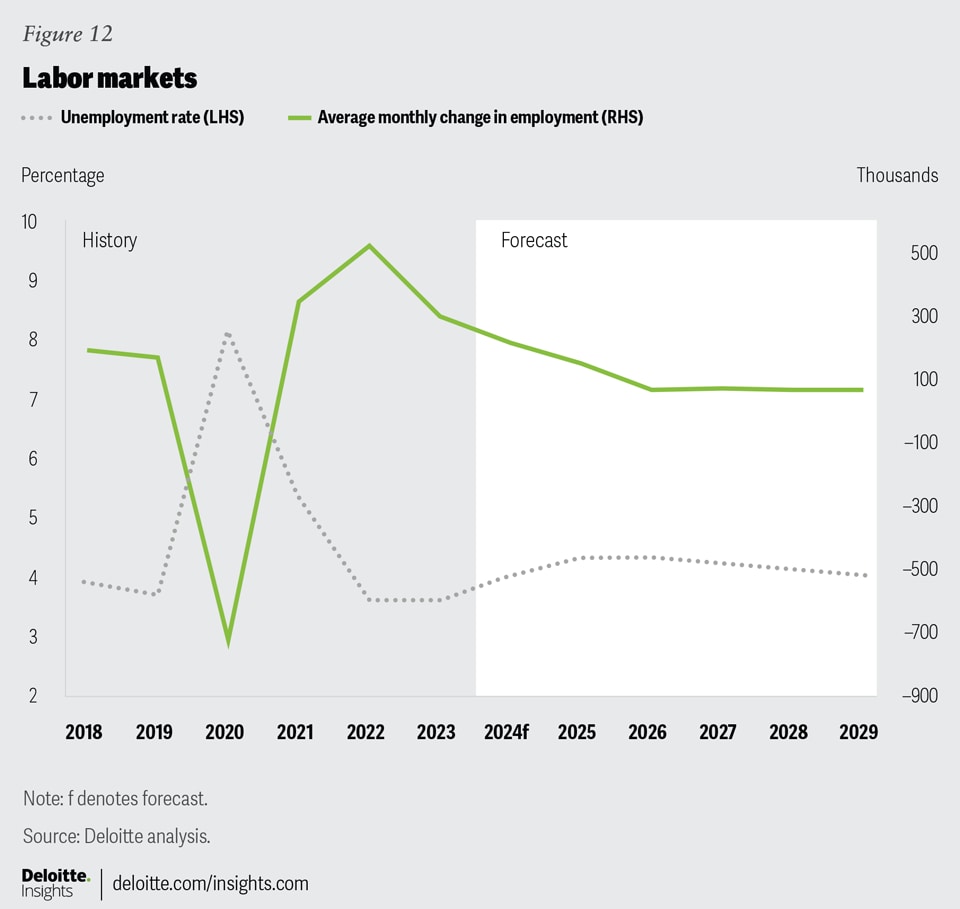

Labor markets

US unemployment rate came down to 4.1% in September and remained unchanged in October. While nonfarm payrolls increased by only 12,000 in October, significantly below the 12-month average monthly gains of 194,000, employment numbers were likely distorted by the effects of the hurricanes and dockworkers strikes. We expect employment to continue rising over the coming quarters, although at a slightly slower pace than at the start of 2024. The unemployment rate is expected to fall slightly in the last quarter of 2024 before rising again throughout 2025.

In the longer term, demographics are expected to be the most important determinant for labor markets. Our demographic forecast has changed from our previous estimates in response to likely policy changes that would affect population growth and consequently the size of the labor force. During the president-elect’s first term, there was no major change in legal immigration levels.16 We therefore do not have any changes to legal immigration levels in our baseline scenario.

However, questions remain around deportations. The president-elect has promised a major program of deportations, suggesting the possibility of declaring a national emergency and using the military to detain people who are in the country illegally.17 In fiscal year 2022, the most recent year for which data is available, the Department of Homeland Security recorded close to 109,000 compulsory deportations.18 Our baseline scenario expects an additional 300,000 annual deportations above and beyond current levels. This number is not based on a specific promise, but rather represents a slightly higher rate of deportations than we saw during the president-elect’s first term in office.

This higher rate of deportations would result in a reduction in population growth. Compared with our last forecast, published in September, our new baseline scenario has the total population 1.16 million lower by the end of 2028. The Pew Research Center estimates that there were approximately 11 million undocumented immigrants in the country in 2022, of which about 8.3 million, or 75%, were in the labor force.19 Consequently, this higher rate of deportations is also predicted to impact the size of the labor force. In our baseline scenario, we forecast the labor force will be 1.14 million smaller by the fourth quarter of 2028, compared with our September forecast.

However, these undocumented workers are not evenly distributed throughout the workforce: Some industries, such as agriculture and hospitality, rely much more on undocumented workers. According to the Department of Agriculture, 41% of agricultural workers are undocumented.20 Thus, the impact of deportations on labor supply (and therefore on wages and prices) will differ significantly across sectors of the economy. Overall, fewer people in the labor force would translate in a slower pace of job growth, as employers struggle to fill some positions. For readers interested in the implications of a much more aggressive immigration policy, our downside scenario (see beginning of the article) assumes a bigger divergence from the status quo, where deportations reach one million per year and legal immigration levels are halved.

Another factor that would affect employment are the expected government layoffs. The recently created DOGE has suggested reducing the over 2 million federal labor force by approximately 75%,21 which would result in more than 1.5 million unemployed workers. We do not expect this to happen even in our downside scenario.

All factors combined, we expect employment growth to slow significantly in 2026 before rising slightly in the outer years of the forecast. That would cause the unemployment rate to remain at or above 4.3% that year before falling to 4% by the end of the forecast period.

{kind=link}

{kind=link}

Financial markets

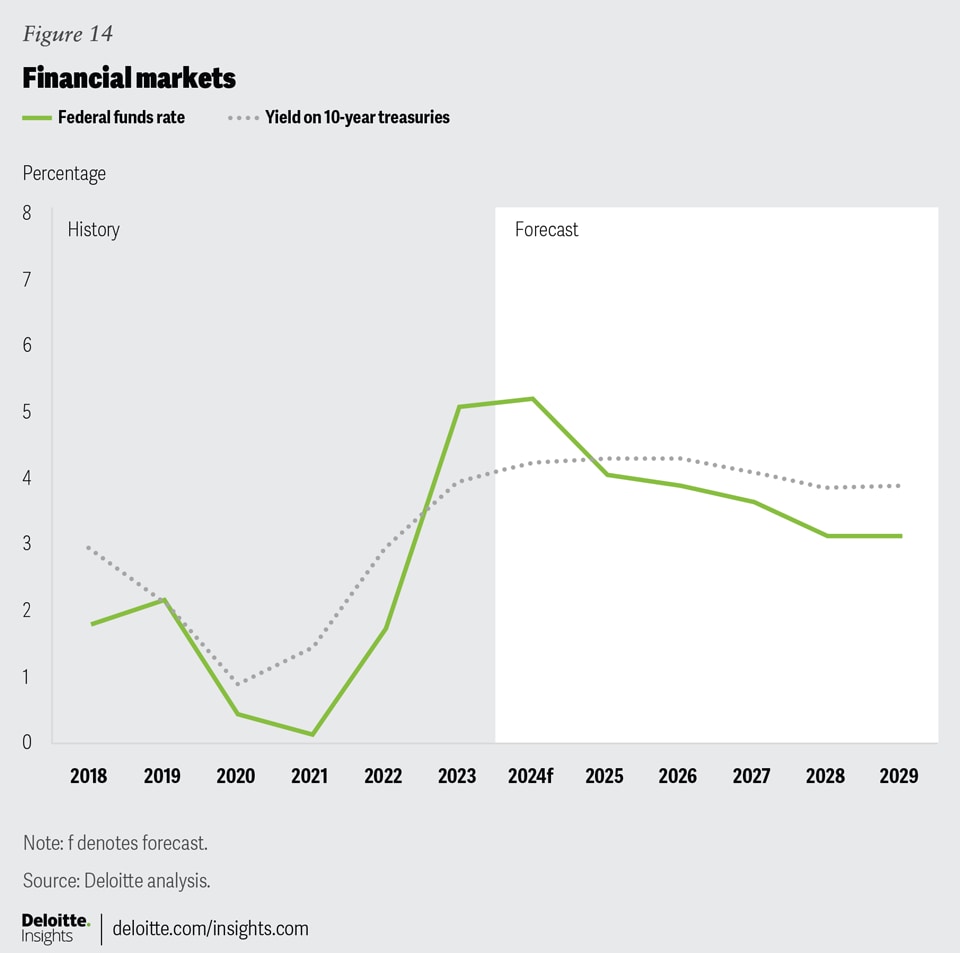

The day following the election results, both the Dow Jones Industrial Average and the S&P 500 posted their biggest single days of gains in two years, suggesting optimism from markets about some of the new administration’s policies.22 At the same time, both the US dollar and long-term treasury yields were up sharply, suggesting that markets expect a further run-up in deficits and rates.

The Federal Open Market Committee (FOMC) has already begun a rate cutting cycle, with 75 basis points of cuts through November. We expect that cycle will continue into 2025 in all scenarios, bringing the Fed’s target rate range to between 3.75% and 4% by the end of 2025.

Thereafter, the path of rates will depend on the evolution of price levels. In the baseline scenario, tariffs cause enough of an uptick in inflation to force the FOMC to pause its rate cuts until mid-2027, when the trajectory of cuts continues until reaching the neutral rate of between 3% and 3.25% by the first quarter of 2028. In all scenarios, however, we expect that FOMC will maintain its independence and with its mandate remaining unchanged.

{kind=link}

{kind=link}

Prices

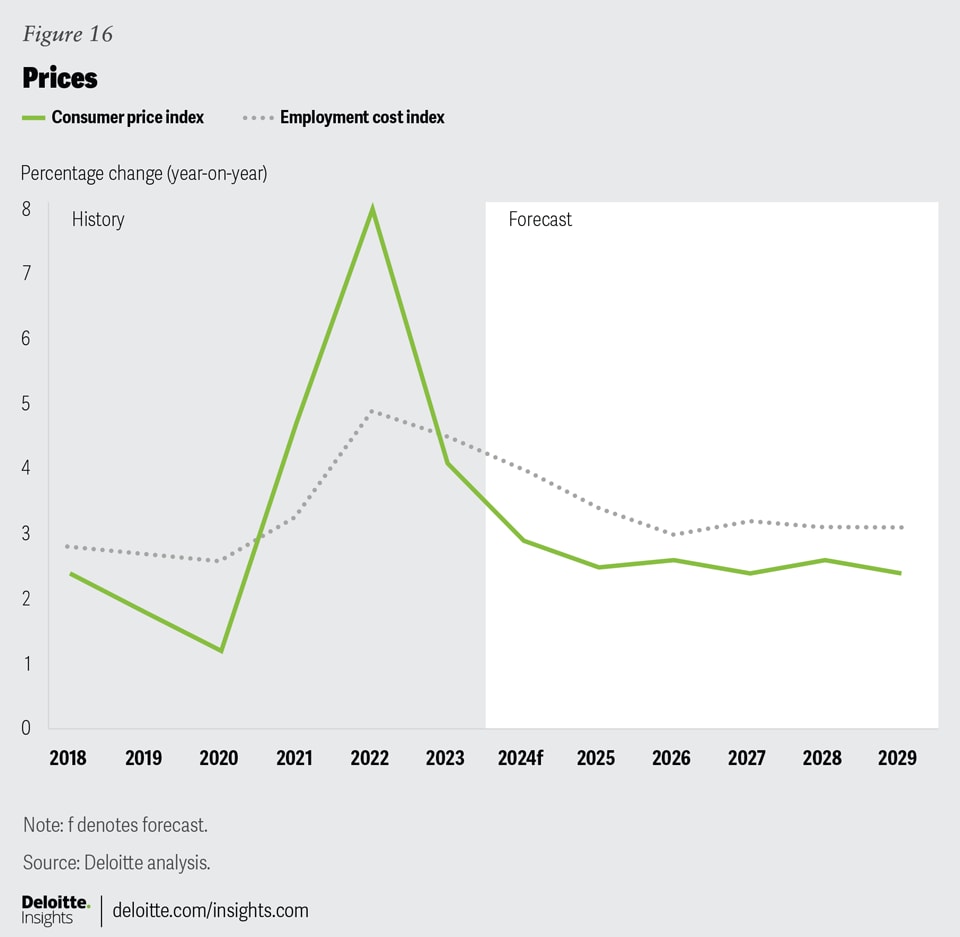

Consumer price index (CPI) inflation continues to decline and has finally gotten down to the target range. Year-on-year CPI inflation for all items fell to 2.6% in October, remaining below the 3% mark for the fourth consecutive month. Services CPI inflation has been the stickiest, in part due to strong wage growth. Ultimately, what has caused inflation to fall is soft prices for goods. In some cases, such as with energy products, we have seen outright declines in prices. In addition, the Federal Reserve’s preferred measure of inflation, the PCE deflator, came in at 2.1% year over year in September, almost hitting the Fed’s target.

We expect inflation to continue falling into 2025. The potential tariffs and deportations, however, represent the biggest changes to our status quo. While tariffs never make goods less expensive, evidence suggests that their impact on prices depends on a few factors, such as whether domestically produced substitutes exist for the goods in question. Therefore, the extent to which tariffs affect prices will depend on which goods receive tariffs and the size of those tariffs. Furthermore, most goods imports are used as inputs in domestically produced goods. Consequently, these proposed tariffs, along with driving up the price of internationally produced goods, would increase the price of American goods.

The impact of deportations would also be felt differently across sectors. For example, a major program of deportations could result in labor shortages and potentially an increase in food prices. In our baseline scenario, deportation levels are low enough that the impact on food prices is limited. Overall, we expect CPI inflation to rise once again in the second half of 2025 as tariffs start to take effect. Once the effects of the tariffs move out of the comparison period, inflation begins falling again in 2027. Over the forecast period, we expect CPI inflation to remain above 2%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}