Navigating coverage has been saved

Navigating coverage How behavioral factors affect decisions in health care plan selection

22 November 2014

- Larisa Layug, Ryan Carter

The shopper for health plans is increasingly becoming the individual consumer rather than organizations. How can health plans and exchanges help consumers effectively navigate the complex set of variables they need to weigh to make an informed choice?

In the news

Read the Modern Healthcare editorialExecutive Summary

Traditionally, the sale of commercial health insurance has focused on a business-to-business approach. Insurers distributed products through employers that chose one or two carriers to offer to employees, limiting the individual’s choice to a handful of options. However, the rollout of public health insurance exchanges under the Affordable Care Act (ACA), along with the growing use of private health insurance exchanges by employers, is increasingly placing the individual consumer in the deciding role when it comes to health plan selection. These consumers will likely have more choices and greater access to information than ever before.

The question remains whether the typical consumer—even if provided with all the information he or she needs—can effectively navigate the complex set of calculations and variables that must be considered to make a truly informed choice among a myriad of health plan options.

The question remains whether the typical consumer—even if provided with all the information he or she needs—can effectively navigate the complex set of calculations and variables that must be considered to make a truly informed choice among a myriad of health plan options.

Health insurance plans that hope to succeed in this emerging business-to-consumer (B2C) market should consider looking to what retailers and financial services firms have learned from behavioral economics, a discipline that has helped many of these firms more effectively market their products and services to individual consumers. Specifically, health plans can use insights from behavioral economics to develop a choice architecture that simplifies and better structures the health plan shopping experience so that consumers:

- Understand the products and services they are purchasing

- Can select a health plan that aligns with their level of medical need and cost requirements

Health plans that achieve these goals can increase consumer trust and confidence in these important choices, potentially growing their market share. Health insurance plans can use these insights directly in the way they structure offerings to consumers on their own websites or through private insurance exchanges (see sidebar, “Types of health insurance marketplaces”). With public exchange marketplaces, where health plans do not directly control the consumer interface’s design, health plans can still make recommendations to improve consumers’ shopping experience.

Types of health insurance marketplaces

Public insurance marketplaces

These are federal or state-run insurance marketplaces created under the mandate of the ACA and implemented in 2013. Uninsured individuals, individuals without employer-sponsored or other individual insurance coverage (e.g., purchased directly from a health plan), and small companies can purchase insurance through these marketplaces and their websites.

Private insurance exchanges

These are health insurance marketplaces run by private third-party entities, brokers, insurance companies, or employers. A private insurance exchange may include plan options from many different insurance companies or multiple options from a single insurance company. Employers may choose to offer a private insurance exchange to their employees, providing them with more health plan choices than they would traditionally receive through existing benefits offerings.

Other insurance market channels

Private health insurance companies can sell insurance products directly to individuals and employers, and often display products on their websites. They use a number of sales channels, including their own sales force and independent brokers.

“Behavioral economics is the combination of psychology and economics that investigates what happens in markets in which some of the agents display human limitations.1” —Sendhil Mullainathan and Richard H. Thaler

Introduction

John, a 40-year-old single man, is a freelance marketing consultant who purchased health insurance through a private health insurance company website last year.2 For John, the experience was not particularly satisfying. He felt overwhelmed by the “wall of text on the page” of his state’s health insurance exchange website, and frustrated by the site’s slow performance and substantial jargon. He also had trouble differentiating among the 25 plans he could choose from that were within his budget. He gave up and later decided to visit the website of one of the health insurance companies he remembered from his prior search. On that health plan’s website, John decided to select the option with the lowest deductible. He didn’t end up using much health care during the year, except for some preventive services (available without any cost sharing), and now wonders if he should have focused on premium costs instead. His current plan is up for auto-renewal, and he is considering looking for a cheaper health plan this year, if he can find one. John does not feel particularly loyal to his current plan. He has a nagging feeling that there may be better options out there and that he did not make the best decision last year.

Joanna is a Spanish-speaking, 30-year-old mother of three living just above the federal poverty level.3 Last year, Joanna received insurance for her three children through the Children’s Health Insurance Program. However, she and her husband remained without insurance coverage. This year, at a local church gathering, she learned from friends that she could attend an in-person meeting organized by a nonprofit group where she could learn about insurance coverage and receive help from an on-site “insurance helper.” Joanna attended the meeting and completed a paper form with step-by-step help from a facilitator, Paul, who sat with her while she filled it out. She is still unclear about the details of the health insurance plan she purchased. She calls Paul when she has questions about coverage.

A Deloitte series on behavioral economics and management

Behavioral economics is the examination of how psychological, social, and emotional factors often conflict with and override economic incentives when individuals or groups make decisions. The field has its roots in the work of Nobel Prize winner Herbert Simon, who as far back as 1959 questioned the classical economic theory that individuals rationally maximize the outcomes they seek (i.e., their “utility”) when making choices.4 Ever since, scholars have argued, and demonstrated, that in the face of uncertainty, humans employ all manner of simple, easy-to-use, but often inaccurate cognitive shortcuts. People are not maximizers, but rather muddlers, struggling to cope with a reality that is much less certain, much more complex, and much more variable than they admit. Worse, as has been shown repeatedly by another Nobel prize-winning behavioral economist, Daniel Kahneman, “We can be blind to the obvious, and we are also blind to our blindness.”5

The implications of cognitive limitation and bias in decision making are as varied as they are vast. Consequences stretch across industries and applications. Managers therefore need to understand something about those aspects of human perception and cognitive processes that can lead us astray. In short, they need to understand something about the psychology of choice.

This paper is one in a series offered by Deloitte6 that is intended to address this need of managers attempting to improve the performance, growth, and innovative capabilities of their organizations. Each paper in this series examines the influence and consequences of behavioral principles on the choices people make related to their work. The reader can expect to see some common themes emerge that are related to the framing of choice, the uncertainty of outcomes, the influence of time (and timing), and a general inability to effectively process information. Each paper will provide a set of practical guidelines for recognizing, managing, and/or mitigating the effects of these very natural human limitations and biases in an applied setting.

Collectively, these papers illustrate how an understanding of biases and cognitive limitations is the first step in developing countermeasures that limit their impact on the organization. Alternatively, they may help organizations and individuals identify strategies that ethically exploit these inescapable elements of our humanity to the benefit of a company’s performance, growth, and innovation.

For many consumers, as for John and Joanna, purchasing health insurance is a difficult process. The decision about which plan to buy is made infrequently, and it requires knowledge of a complex and unfamiliar subject. The consequences of getting it “wrong” can be significant for those who underinsure or choose an overly expensive plan. There are many available choices and channels, and selecting among them requires an understanding of potential costs and uncertain outcomes. The average consumer will likely rely on whatever tools are on hand to help narrow the options. For example, many consumers, like John, may opt to pick the “cheapest” product, zeroing in on a single variable—such as deductible or monthly premium—as the basis for their decision. The danger is that choices made in this way may not reflect a true understanding of the amount of coverage needed to be adequately insured, given the individual’s tolerance for risk and likely health care use. In other words, consumers may select a health plan based on a variable that they do not fully understand or that does not fully reflect their needs, therefore unduly narrowing their field of choice.

Over the next 10 years, a growing percentage of many health plans’ buyers will likely be individual consumers like John and Joanna who will be purchasing health plans on their own behalf. These shoppers may explore a number of different channels to make their purchases, such as health plan websites, in-person kiosks at big-box retailers, public marketplaces, and private insurance exchanges. The Congressional Budget Office predicts that, by 2018, up to 25 million individuals will enroll on public marketplaces alone.7

Health plans offer websites to help individuals and employers understand and choose among their offerings. They also participate in—and sometimes design—private health insurance exchanges for employers that offer multiple insurance choices. Other entities—state and federal government agencies, employers, and brokers—also offer websites that allow consumers to choose among health plans. Sometimes, these sites direct the consumer to follow links back to the health plan’s website for more information.

Even if they do not directly control other entities’ websites, health plans may be able to make recommendations for improving consumers’ health plan shopping experience—and potentially their own business results. Health plans that are able to effectively guide the Johns and Joannas of the world have the opportunity to establish market leadership in the emerging health plan consumer landscape. Many health plans are making large investments in analytics, marketing, product design, Web design, distribution, and consumer engagement tools to attract and retain consumers.8 To do this effectively, they should consider understanding and addressing John's and Joanna’s unique needs in order to build a satisfying shopping experience that enables and empowers them to choose plans that provide adequate coverage at the price that is right for them.

This may, however, be a difficult task. In the first ACA open enrollment period in 2014, during which over 8 million individuals9 signed up for coverage, shoppers like John and Joanna encountered a number of problems:

- According to a national consumer survey by Enroll America (figure 1), shoppers had low awareness of insurance terms and processes, and questioned health plans’ affordability.10

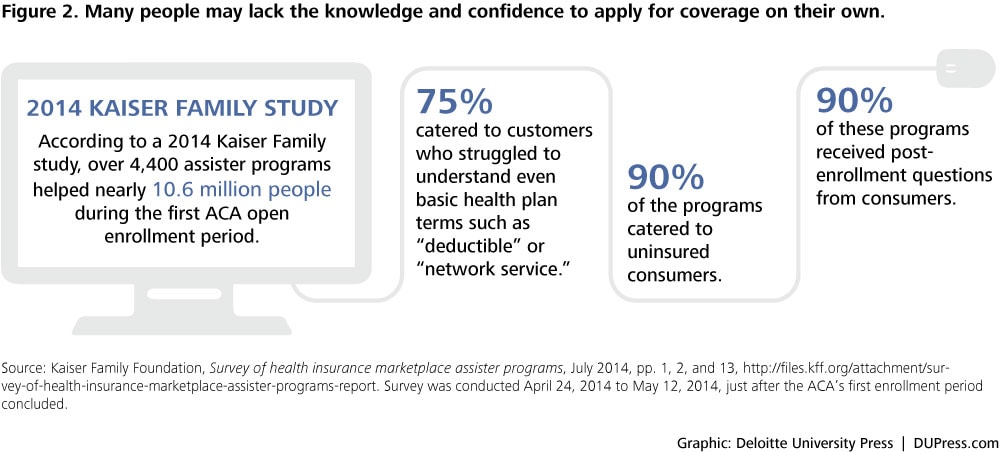

- Many consumers, according to a 2014 Kaiser Family study, lacked the knowledge and confidence to apply for coverage on their own (figure 2).11

- Consumers who shopped for health plans online had low satisfaction with the experience. A 2014 J. D. Power survey of new health insurance enrollees found that individuals who enrolled online (67 percent of all surveyed enrollees) had much lower levels of satisfaction than those who enrolled in person. The reasons included technical problems, the application process taking too long, and the lack of availability of information consumers were looking for. Almost half of all individuals surveyed did not choose a plan.12

The implication for both health plans and other insurance marketplace designers is that the current health plan shopping experience needs to improve. Many consumers, like John and Joanna, are not satisfied with their purchase decisions. Behavioral economics offers insights into how to both improve the shopping experience and reduce the uncertainty and regret felt by consumers who choose a plan but worry that there might have been a better option.

The value of behavioral economics

Behavioral economic insights can help health plans make it easier for consumers to select a health plan tailored to their needs. Behavioral economics is the combination of psychology and economics that investigates what happens in markets in which some of the agents display human limitations.13 The discipline of behavioral economics studies how psychology affects decision making. It suggests that human decisions are strongly influenced by context. Our behavior, and our choices, varying over time and space, are subject to social influences, emotions, and cognitive biases, and they can be influenced by the way in which choices are presented.14 By studying these phenomena, scholars have uncovered aspects of human behavior that run counter to economic theory and logic. For example, even if people are provided with the best information, if that information is organized poorly, individuals like John and Joanna are not likely to use it in ways that lead to the best outcome.

If applied thoughtfully, behavioral economic principles can help simplify decisions for health plan consumers. By doing this, health plans can build consumer confidence and trust, and potentially raise consumer satisfaction, loyalty, and overall profitability.

Designers of health plan shopping experiences should consider the following actions:

- Increase consumers’ understanding of options by reducing complexity

- Optimize coverage at the right price point for the consumer

By meeting these two goals, designers of health plan shopping experiences can help the consumer make a choice more quickly and feel more confident that he or she has made the right decision.

Goal 1: Reduce complexity

Challenge: People are overwhelmed by too much information

Today’s consumers, when exploring an exchange or other health plan shopping website, are often confronted with a large number of plans and variables from which to choose, and they may not understand what the terms they are presented with mean. Variables might include out-of-pocket costs, premiums, services covered, network design (what doctors and hospitals are available without extra cost), special pharmaceutical coverage rules, availability of wellness and care coordination programs, quality rating, and others.15 Many may find these insurance terms and variables confusing, and many might not understand how they relate to one another (for instance, how does a deductible relate to a copay?).

Too much information or too many choices can cripple individuals’ ability to choose—a phenomenon known as “choice overload.” For example, in one study, customers in a grocery store were more likely to purchase jam when presented with limited options (figure 3).16 The same can be true in health insurance selection: Too many options can lead to indecision. John, the freelancer, initially opted for “no choice” in his first health insurance shopping foray. The next time around, he homed in on one or two variables that he thought he understood (deductible and brand) and then made a “guess”—even after he had obtained additional data from doing research on the health plan website. Joanna did not even evaluate the aspects of the plans available to her. Instead, she believed that selecting among the products the assister shared with her would seem “OK for me.”

Recommendation: Consider narrowing down the options through an effective choice architecture

Behavioral economic research has established that the way a choice is presented—its “choice architecture”—has a direct impact on which option is selected.17 There are no neutral choice architectures, according to choice architecture theory.18 How options are presented always influences the decision. By presenting vegetables before desserts, for instance, a cafeteria can increase the amount of vegetables purchased. Similarly, by managing the way information is presented, health insurance companies can influence consumers’ decisions as they make their health plan selections.

Choices may be structured in a number of different ways. They can be sorted and ordered against specific criteria, bundled together, presented as a default, made additive or subtractive, compared with each other, or displayed with different information and visual guides. Each of these options has implications for how consumers make decisions.

To mitigate confusion about terms and reduce choice overload, health plans should consider opportunities to develop simplified plan designs customized to meet members’ specific needs. They can leverage analytics together with lessons from behavioral economics to create choice architectures that combat choice overload. Most useful are those that narrow down the range of options to a small number that are acceptable to the consumer. Strategies might include:

Elimination by aspects. One of the founders of behavioral economics, the cognitive psychologist Amos Tversky, describes a solution called “elimination by aspects” in which the choice architect presents the most critical aspect of a decision to an individual, and then eliminates all alternatives that do not meet this criterion.19 This process is repeated with the next most critical aspect of the decision, and then the next most critical, until a final choice emerges. In practical terms, consumers of health plans can be asked what factors are most important—for example, out-of-pocket monthly premium costs. Then all the options that do not include these most important aspects can be removed. From 30 options, the field can be narrowed to 10, then 5, then 3. Elimination by aspects can be very effective, as long as the criteria are well defined, accurate, and meaningful to the individual.

Analytics. Health plans can strategically deploy analytics solutions to effectively narrow down the choices available to customers based upon segment-specific responses to initial questions on the shopping interface. Many insurers are already investing or planning to invest in targeted marketing and sales analytics capabilities that can make this possible (figure 4). Some also aim to develop customized product solutions for specific consumer segments.20 Insurers that are able to deliver simplified, targeted products to specific segments in the most convenient marketing channel can differentiate themselves from the competition.

Social proof. Giving consumers access to “social proof” can also simplify the decision-making process.21 Individuals tend to feel more confident in their decisions if they think others similar to them are making similar choices.

Social proof can play out in several ways when consumers make health care choices. For instance, consumers may read online reviews about physicians from trusted sources (e.g., on a neighborhood blog) or hear opinions by word of mouth before they select a doctor. Their perceived similarity to the reviewers reassures them about the wisdom of their choice. Health insurers can leverage this by presenting information on how a particular product offers benefits to those with children (for instance), which may interest Joanna, or whether the product is popular among the self-employed, which may appeal to John.

Bundling. Another way to reduce choice overload is through “bundling.” In bundling, the choice architect may identify three or four key product attributes that are important to a consumer, describe them in language that consumers understand, and then “bundle” other attributes and options around each attribute. When purchasing a car, for example, a consumer may have an easier time choosing between base, premium, and luxury options than among the many different components that make up each option. Once a consumer chooses a “bundle” based on a few representative attributes, such as price, he or she can make further choices within that “bundle”—such as color—to customize his or her product.

To help consumers select a plan that provides adequate coverage and meets individual needs, health plans and other exchange and marketplace designers should consider presenting and bundling information about the available plans in such a way that it guides individuals toward an “optimal” decision. To do this, it is important to understand what attributes of health plans are important to most consumers’ decisions. What information would consumers find most helpful, and how should it be presented?

Based upon various surveys,22 we have identified several key factors that consumers consider when selecting a health plan decision:

- Affordability and cost. According to the Deloitte 2013 Consumer Survey, 59 percent of consumers indicate that lower payments and cost sharing are the most important factors in purchasing health insurance.23 To effectively choose a health plan, consumers may seek to understand which major plan design elements impact the price of the product. They also want to understand total “fixed” or monthly costs (such as the monthly premium) as well as the potential variable costs, which are influenced by medical utilization and cost-sharing plan design elements (such as copays and coinsurance).

- Network. Consumers may also want to understand the cost implications of belonging to a smaller versus a larger, more inclusive network of providers. They also need to know whether or not their preferred providers are in their network, and how much it will cost per visit for emergency or other care.

- Product. Consumers should seek to clearly understand what benefits and programs are “standard” versus “non-standard.” They also should clearly identify programs and services (e.g., chronic condition programs) that may impact the cost of different plans.

- Customer service. Consumers will be interested in a brand’s reputation for service. Do health plans help consumers receive care or hinder them? Do they deny services? “Yelp”-like brand and customer reviews are becoming increasingly influential.

Health plans and exchanges should consider presenting essential information on each of these components in a way that not only is simple to understand, but that also identifies key elements that differentiate the various plan options from each other. For example, lack of understanding of the terms around out-of-pocket spending alone can lead consumers to make inaccurate assumptions when choosing health insurance that can result in their having to spend more than planned.24

Oregon’s Health Co-op offers three additional “SiMPLE plans” along with its standard plans. These SiMPLE plans, which come with premiums, flat copays, and no coinsurance, are targeted to people who are especially concerned about out-of-pocket costs.25 As choice overload is triggered by the availability of too many choices and too many criteria by which to make choices, this approach appears to provide a simplified option to consumers, supported by a streamlined underlying plan design.

Goal 2: Optimize choice

Challenge: People are often unduly swayed by the first option they see

Consumers often base their understanding of a situation on the initial information presented to them, and they are quick to use this initially available data to support their subsequent assumptions and choices.26 Many consumers will likely take these initial defaults as the standard against which other choices are judged. Many will likely not look at or consider other options.27 In one study, more than 60 percent of users selecting health insurance on a private exchange made their decisions without leaving the initial screen.28

Recommendation: Consider providing “smart defaults” that are likely to align with the consumer’s needs

Recognizing that consumers frequently focus on the first information they are presented, smart defaults can be designed to provide consumers with a starting point—a default option—that is preselected by the choice architect. Health plans and exchanges using smart defaults should consider how they might guide consumers to a default plan or subset of plans by (for example) asking consumers certain qualifying questions. The aim is to set a default that more accurately reflects consumers’ requirements than what they would have chosen for themselves.

John chose to sort and select his health plan by deductible, and likely chose one of the first plans presented to him on the sorted list. This led to a choice that did not take into consideration copays and premiums. A system that deploys a “smart default” may ask John to enter key demographic information, ask several questions about his medical history, and then present the three major plans that are most likely to meet his needs.

Because how and what information is presented to John and people like him is so important, smart defaults are particularly effective when offered at the very beginning of the decision-making process, such as on the initial screen of a health exchange site. In fact, the initial screen is one of the most important element of any exchange site, as it is where consumers will find available plans and begin their decision-making process. Plans may actually wish to present a default “best choice” that can then be adjusted based on the information consumers enter and prioritize. They may also consider default selection criteria for various consumer segments. Exchanges may, for example, prepopulate the average number of specialist and primary care visits for a diabetic as a starting point for diabetic individuals. Additional guidance may be provided for different segments or conditions.

Finally, health plans should consider approaches used by retail e-commerce websites that sort initial search results by the best-selling or most popular products in a region. This links consumers’ decisions to what others—whom they believe are similar to themselves—have purchased. This may be an interesting strategy for private health insurance exchanges or other private insurance sales channels.

Challenge: People have trouble understanding the full cost of health care

Because health care costs loom so large in consumers’ choice of health plans, it is important to consider insights from behavioral economics about the irrational ways that people think about costs over time. “Present-biased preference” describes the tendency to weigh rewards in the present more heavily than rewards in the future.29 This bias can make it difficult for consumers selecting health insurance to compare one product with another, particularly when considering future costs, as they often are. They may fail to understand the “full cost” of health care, which includes monthly premiums, a potential deductible, and out-of-pocket costs associated with medical utilization (doctor visits, hospital visits, and pharmacy, for example), coinsurance, and copays.

For many members, the monthly premium is an immediate fixed cost that can be understood and planned for. Variable costs, however, are more difficult to estimate. Individuals may not adequately plan for or consider costs associated with care over time. They may have difficulty estimating the probability of possible future medical events, particularly if they think they are unlikely to occur.30 Many of these possible costs may not occur until far in the future, if at all. The fact that these costs are only a probability makes them difficult to integrate into a decision. This can bias shoppers toward choosing a plan with a low premium that does not offer enough coverage when they get sick.

Recommendation: Consider creating transparency into health care costs over time

By providing a more comprehensive picture of forward-looking “total costs” to consumers under a variety of major situations (e.g., if an individual is pregnant or diabetic), health plans may help customers overcome a naturally strong preference to avoid unnecessary costs in the present, and to consider their longer-term medical needs during the plan selection process. Clear information and calculators showing how costs add up over a year (or several years) under any particular health plan can help steer members to a more informed decision. Powered by an underlying analytics infrastructure, health plans could potentially share with consumers their projected costs under the most popular plans, or the costs of other consumers like them (e.g., pre-diabetics), from prior years’ experience.

To compare and contrast potential outcomes among consumers with and without such guidance, let’s return to Joanna, the mother of three. In one scenario, Joanna selects the lowest-premium plan with high deductible and coinsurance amounts, assuming that she will have no health care needs in the near future. Later that year Joanna gets the flu, makes one trip to the emergency room for a hurt shoulder, and has several office visits related to treating an emergent diabetes condition. In this scenario, she is underinsured and cannot cover her medical fees—exactly the situation a health plan wants to avoid. Everyone ends up dissatisfied.

In another scenario informed by behavioral economic theory, Joanna provides information about her age and medical status to her exchange provider and receives a table showing the average number of office and emergency room visits for someone with her profile, along with a projected total cost for the year classified by deductible and total out-of-pocket costs. When Joanna gets the flu later in the year and goes to the emergency room, or attends diabetes-related visits, she is prepared. She knows how much each visit will cost and has set aside funds for these visits based upon the information she received from her health plan.

Conclusion

John and Joanna have a significant need that is not often met in the marketplace today. They want a health plan that is appropriate given their budget, medical health risks, and network requirements. And they want reassurance that they made the right decision. Because of the confusing way health plan choices are often presented, Joanna and John are not confident in their decisions and are seeking out third parties for help.

Behavioral economics offers a number of lessons for health plans and designers of exchanges (figure 5). As health plan marketing leaders take advantage of new opportunities to directly engage with consumers, they should consider incorporating these powerful insights into their strategies.

In many ways, health plans and exchanges are the new choice architects for health plan consumers. The design and architecture of the tools they provide will likely influence individual consumers’ shopping experiences and plan selection. A key question for health plans, and other designers of health insurance marketplaces and exchanges, is whether they can create a simple, personalized, high-end customer experience for the individual member on a par with that offered by retailers. John and Joanna are likely loyal to certain retailers because these retailers offer them an enjoyable, targeted shopping experience. Can it be the same for a health plan or other entity selling health insurance?

About the Deloitte Center for Health Solutions

The Deloitte Center for Health Solutions (DCHS) is the research division of Deloitte LLP’s Life Sciences and Health Care practice. The goal of DCHS is to inform stakeholders across the health care system about emerging trends, challenges, and opportunities. Using primary research and rigorous analysis and providing unique perspectives, DCHS seeks to be a trusted source for relevant, timely, and reliable insights.

With more than 775 practitioners, Deloitte LLP’s Health Plans practice serves more than 80 parent companies and over 100 subsidiaries, including nearly 85 percent of the top 25 US health plans and nearly 60 percent of the nation's Blue Cross Blue Shield Plans. We offer services in the areas of analytics, government programs, growth and scale, retail consumerism, risk and compliance, technology, and value-based care. Read more about our Health Plans practice on www.deloitte.com/us/heathplans.