Upward climb with uphill struggles: 2024 Deloitte corporate travel study

Amid steady corporate travel growth, companies are challenged to balance a need for more face-to-face client interaction with steep pricing and persistent environmental impact

Eileen Crowley

Kate Ferrara

Matthew Usdin

Matt Soderberg

Bryan Terry

Maggie Rauch

Corporate travel outlook

While leisure travelers returned in a big way to airports, hotels, and vacation rentals beginning in the summer of 2021,1 corporate travel has been slower to return post–COVID-19 pandemic. Caution—initially about health, and then about financial costs and environmental impact—led most companies toward gradual returns to the road.2 New structural realities of working life have also curtailed the need to travel, with more home-centered days and virtual meetings, and fewer clients in office day to day to take sales meetings or collaborate on projects.

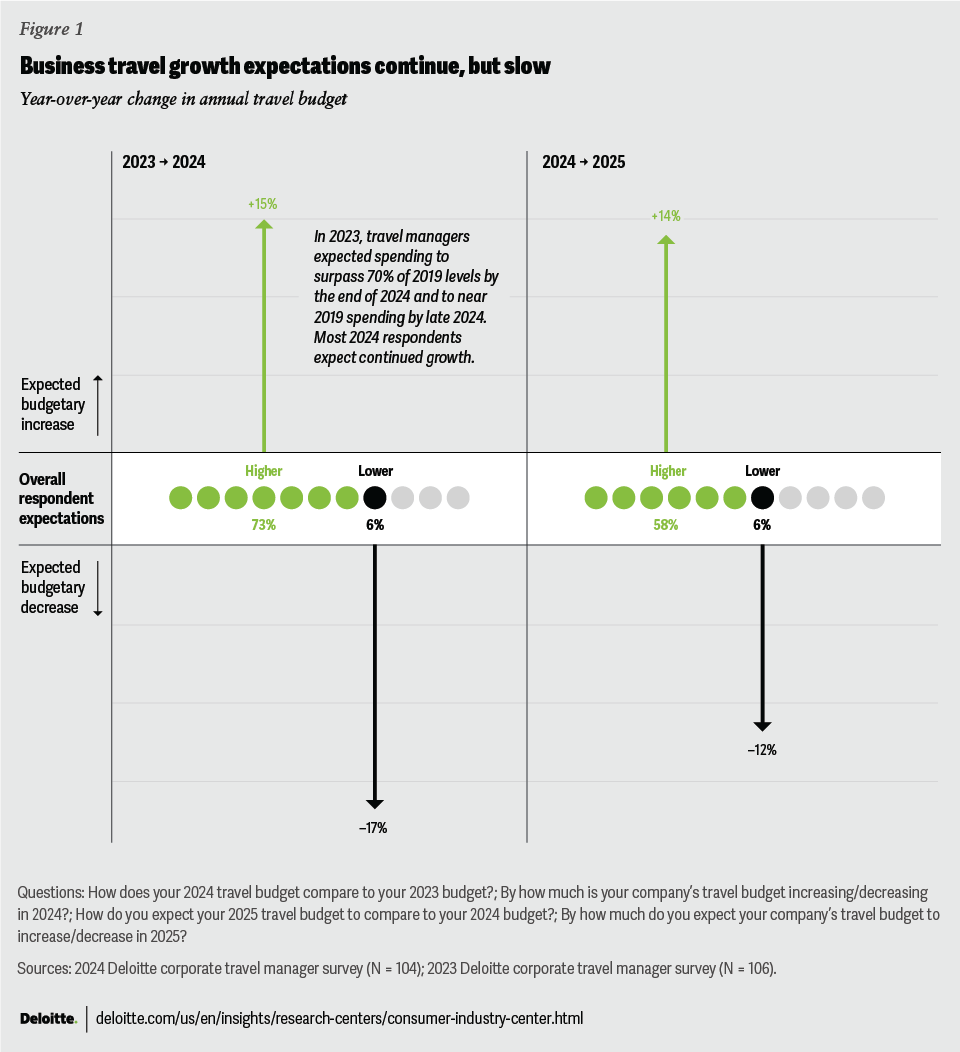

Still, corporate travel holds significant value across industries. By the end of 2024, US-based companies’ spend is expected to reach and perhaps surpass 2019 levels (figure 1). Findings from the fourth edition of Deloitte’s surveys of travel managers, travelers, and budget owners (fielded between May 8 and June 3, 2024) indicate that corporate travel spend could grow by 8% to 12% in 2024. That rate would put it well ahead of The Conference Board’s projected3 2.1% GDP gains, indicating a still-recovering industry. Frequency per traveler is up versus 2023 too—77% of business travelers say they took one to five trips in 2023, 15% took six to 10 trips, and 7% took more than 10. In 2024, 20% of travelers expect to take six to 10 trips, and 10% say they will take more than 10 trips. In 2025, travel managers expect growth to slow by a couple of percentage points, but gains appear likely to continue to pace at two to three times GDP growth.

If there is lingering discomfort with travel post-pandemic, those traveling report very little. Only 3% say they dislike business travel, while 83% call it overall “enjoyable.” And they see both professional and personal value in it—about half place networking opportunities (51%) and exploring different cities (47%) among the top three benefits of business travel. Some take the opportunity to enjoy the travel without the business—two-thirds of corporate travelers say they extended a business trip for leisure in 2023. Still, travelers do identify some drawbacks, with the most cited being general fatigue (55%), followed by time away from loved ones (41%) and the work that can pile up while they are away (39%). When it comes to specific in-trip pain points, travelers say they encounter the most friction, by far, when they need to cancel or reschedule flights or hotel bookings.

Key findings

- Most travel managers expect their companies’ spend to grow in both 2024 (73%) and 2025 (58%). For those projecting gains, expectations average out to 14% to 15% each year.

- Return to office is still cited as a driver of increased travel, as companies’ balance of remote, in-office, and hybrid work continues to stabilize post-pandemic.

- While fewer workers travel for sales and project work, those who do are on the road frequently. One in five frequent travelers say they travel for sales or project work more than once a month.

- Most say they enjoy business travel, and many take the opportunity to enjoy the travel without the business—two-thirds of corporate travelers say they extended a business trip for leisure in 2023. One in seven say they did so three or more times.

- About three in 10 travelers say they never book trips through corporate online booking tools or agents. Most travelers book at least some of their trips through unmanaged channels. Online travel agency (OTA) bookers are most attracted by better deals, while those who go directly to hotel and airline suppliers are seeking an easier process when their travel plans change. Better digital user experience and loyalty points also play significant roles in platform selection.

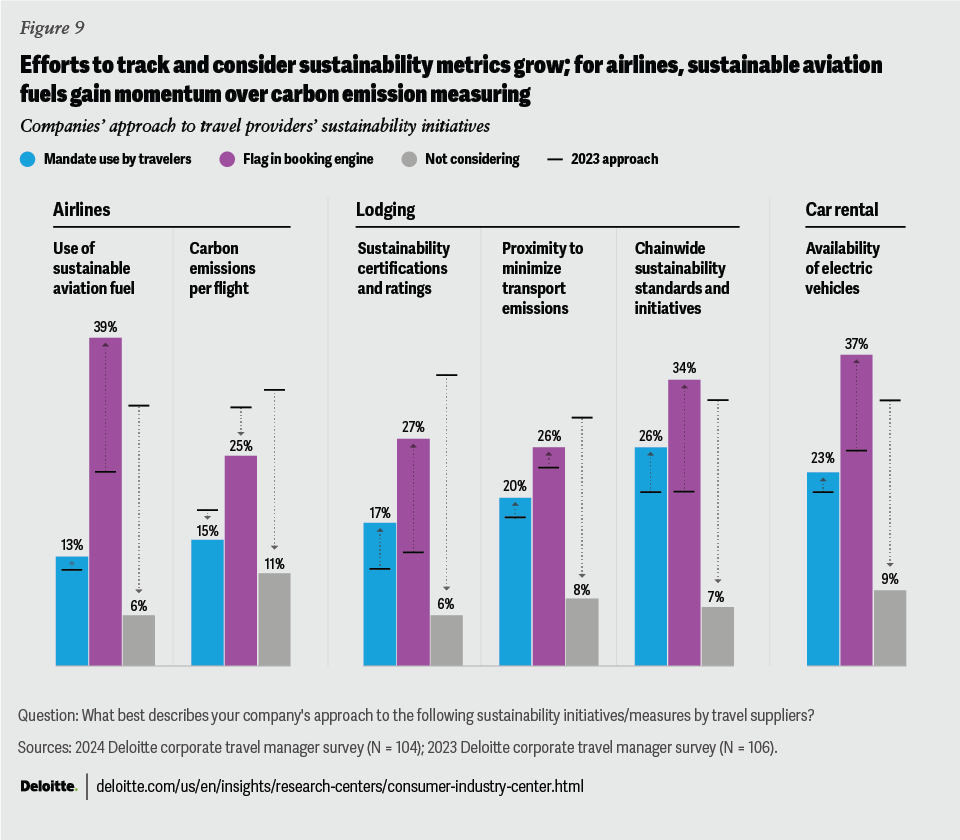

- Travel managers surveyed report significant progress over the past year on the sustainability front. On the airline side, there is a notable shift to support sustainable aviation fuel over flight-by-flight emissions comparisons. On the lodging side, certifications are increasingly appearing in the booking path, but chainwide initiatives are getting more attention.

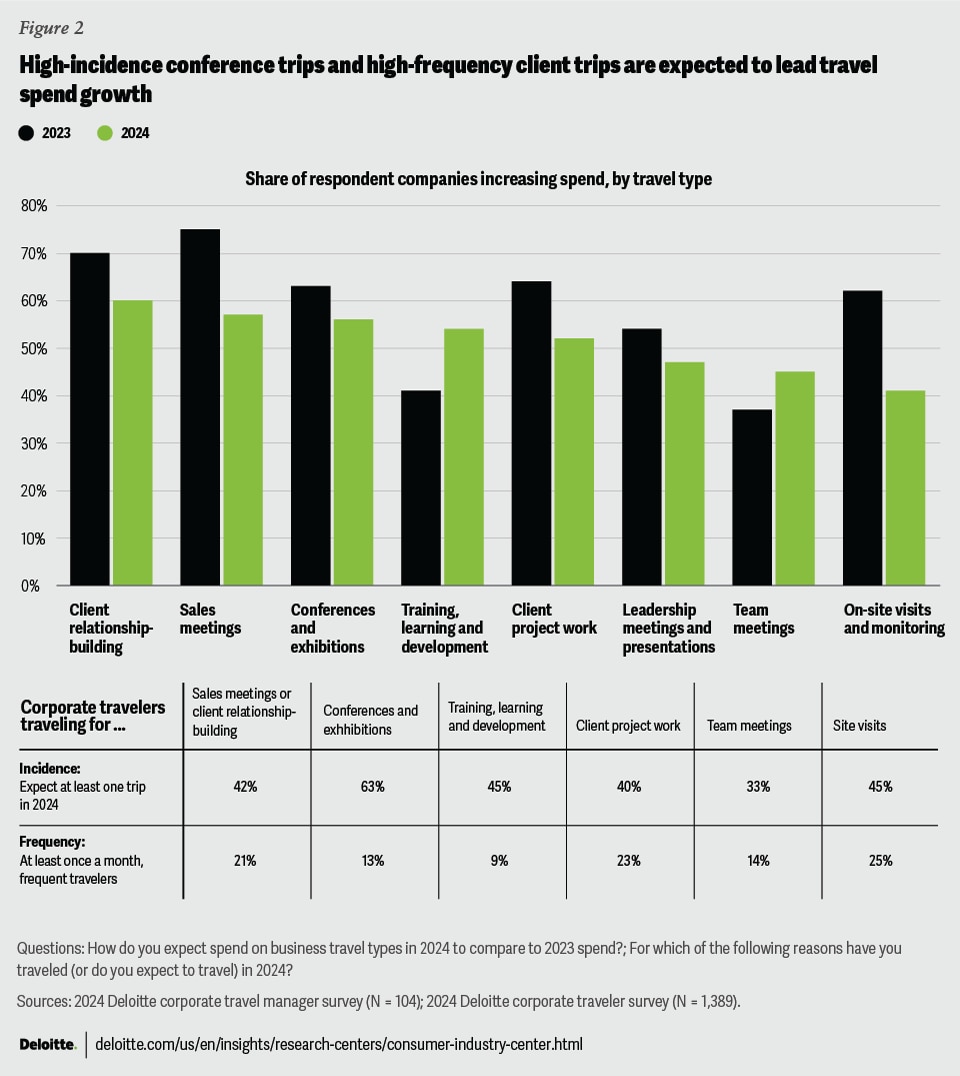

- Conferences, trade shows, and exhibitions are playing a big role in travel growth, and more than six in 10 business travelers expect to attend at least one in 2024. While fewer say they will take client-focused trips for sales and project work, these types of trips are responsible for considerably more frequency.

Growth drivers: Conferences boost the number of workers on the road, while road warriors chase client connections

As corporate travel steadily closes the gap with its pre-pandemic scale, travel manager respondents report some continued influence from the stabilization of pandemic-era changes—including the openness of international travel and workers returning to the office. But the role of those return-to-normal metrics is shrinking, as signs point toward growth led by conference attendance and client sales and project work.

Industry gatherings, which offer the opportunity to meet with many clients and prospects in a short time, hold an increasingly prominent place on respondents’ agendas. A quarter of travel managers say that conference attendance was the biggest driver of travel growth in 2023 and expect that to continue in 2024. Half rank conferences among the top two growth drivers. Six in 10 travelers say they expect to travel for a conference in 2024, significantly ahead of all other trip types, in terms of number of travelers (figure 2).

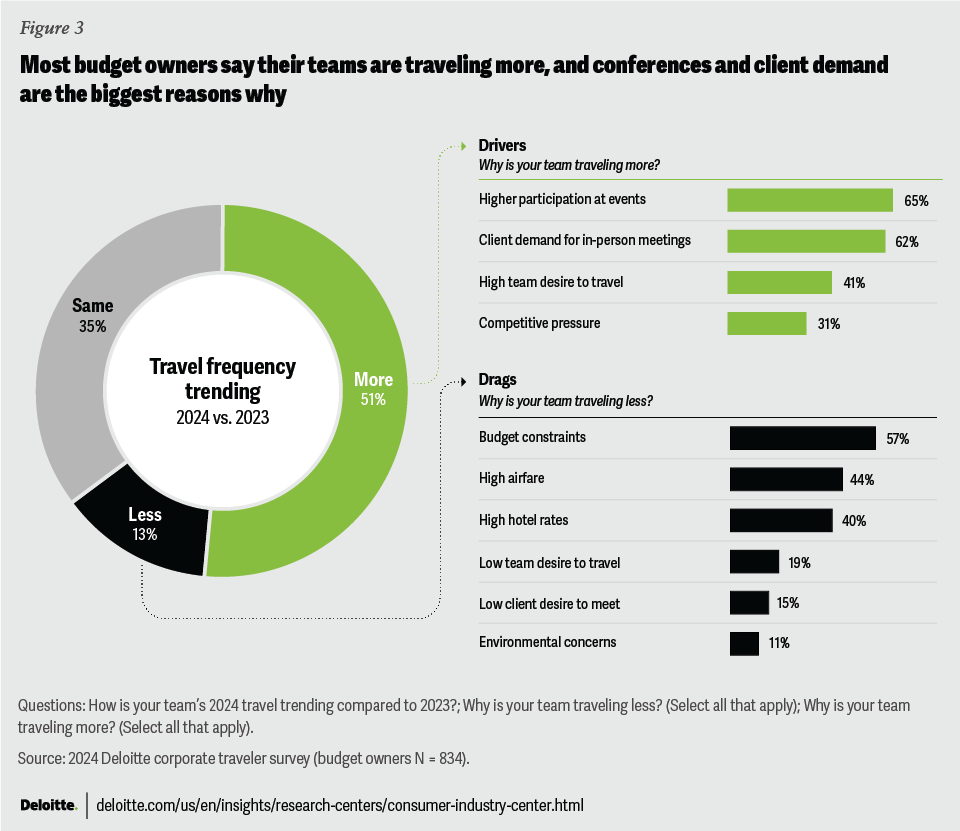

While conference travel is high incidence, sales and client project work are bigger drivers of frequency. Among frequent travelers, about one in five say that they traveled once per month or more in the first half of 2024 for client project work (23%) or sales and client relationship building (21%), compared to just 13% for conferences and exhibitions. Travel managers’ expectations for increased spend are led by high-frequency client travel, alongside high-incidence conference and exhibition travel (figure 2). Budget owners (those who play a role in travel decisions at the team level) rank live event attendance and client demand for meetings as the top drivers of increased travel (figure 3). Expectations for spend growth remain low in areas that are more easily replaced by virtual meetings, as described in Deloitte’s Why We Fly Matrix,4 affirming that technology is likely having some dampening effect on the growth of corporate travel.

Travel manager respondents expect international trips’ share of spend to increase slightly through 2025, and to increasingly go toward trips beyond North America. They cite easing of entry requirements as the third-biggest driver of 2024 trip growth, behind live event attendance and budget increases. Return-to-office still affects the return of corporate travel, but its influence is fading. About one in five travel manager respondents cite each of the following return-to-office patterns among their top two drivers of increased travel: significant return-to-office by client base (19%) and significant return-to-office by respondent’s company (18%).

Pricing’s looming presence: Corporate buyers report tough negotiations as they strive to balance cost with comfort and sustainability

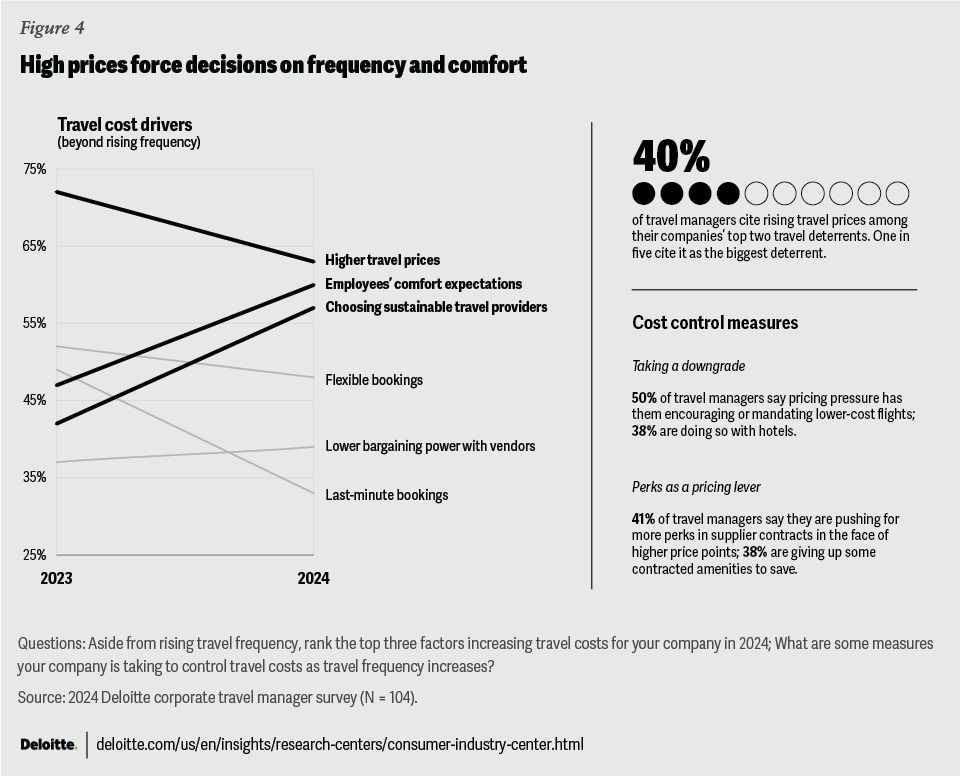

In a world where companies have decided that some trips can be replaced by virtual meetings, the cost of travel may be more scrutinized. The American Hotel & Lodging Association’s 2024 forecast5 projects 2024 average daily rate increases of 3% versus 2023 and 22% versus 2019. Average US domestic airfare in 2023 was up 8.5% versus 2019.6

High prices are a big driver of increased spend, but also lead companies to cut back on trip volume (figure 4). One in five travel managers (22%) say that high prices are the biggest drag on trip volume for their companies, and 40% put prices in the top two. According to travel managers, pricing’s impact on travel volume is 1.5 times as significant as that of budget cuts. Half of travel managers report that their companies are encouraging or mandating lower-cost flights. And many are putting amenity adjustments on the negotiating table—sometimes demanding more to justify strong rates, and sometimes sacrificing to save.

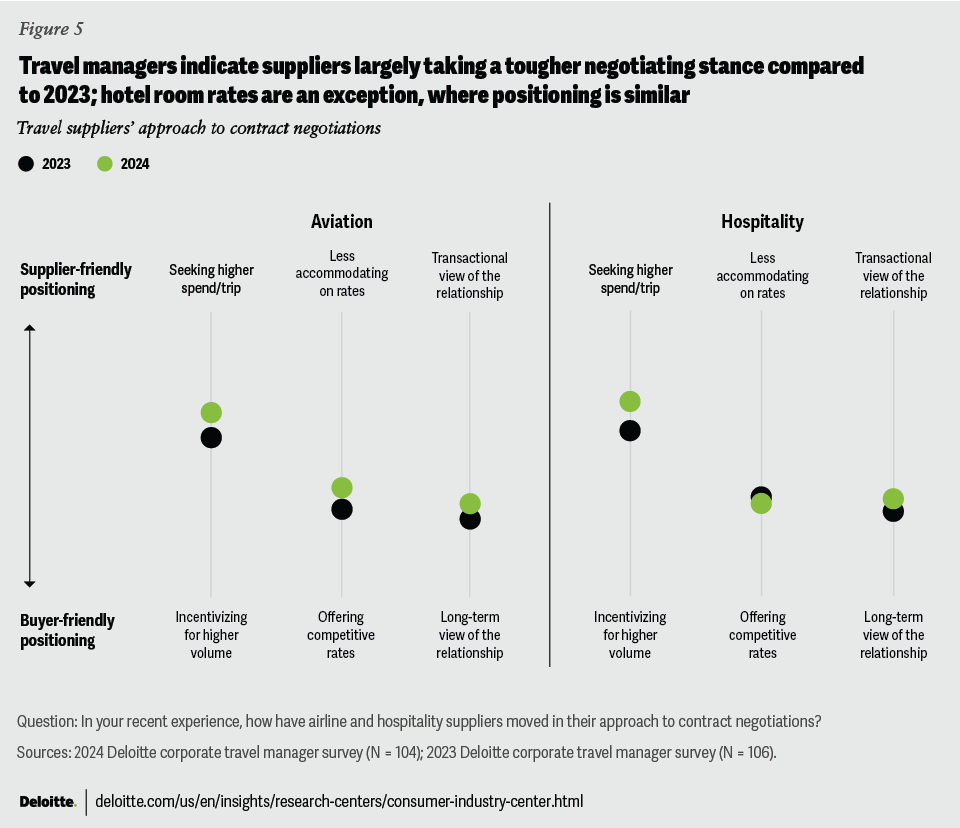

Airlines and hotels have not been particularly understanding, according to travel managers. Compared to 2023, they say suppliers have moved slightly toward tougher negotiating stances (figure 5). These cost challenges come amid growing pressures for travel managers to deliver more on some fronts that can drive up costs—more comfort for travelers, more sustainable trips, and more flexible bookings.

Booking compliance: It’s … complicated

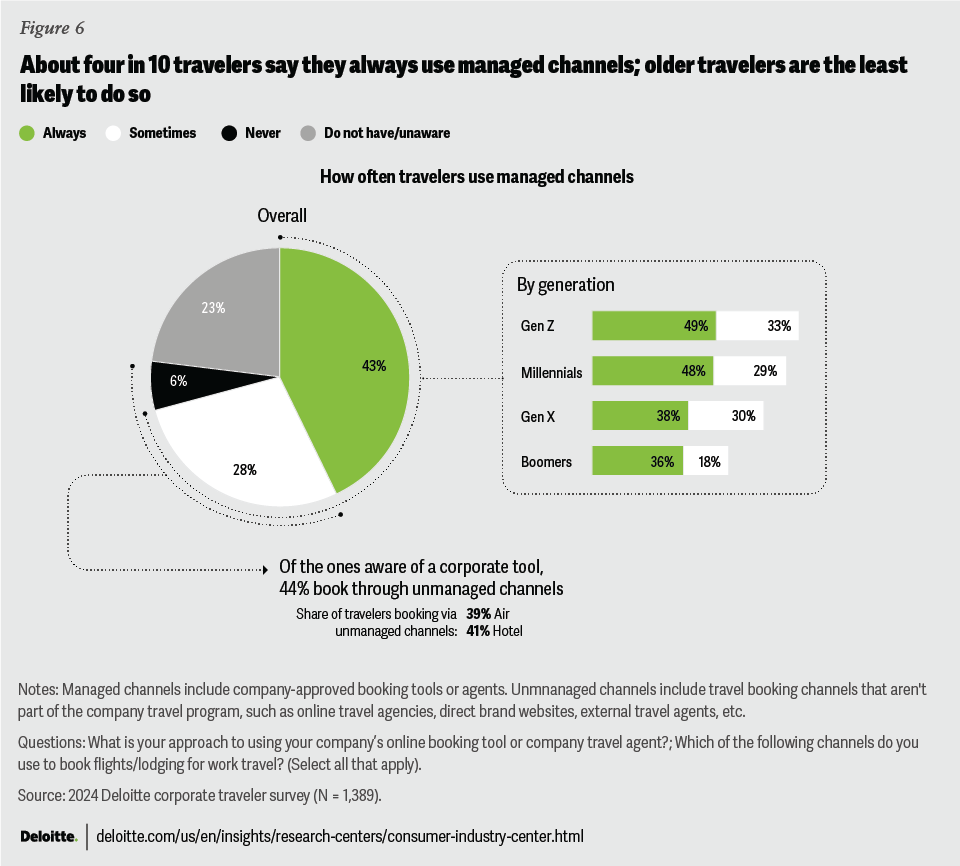

Maybe unsurprisingly, travel managers hope that booking compliance can help control costs—55% of those surveyed cite compliance as a top cost-control measure, ahead of all other options, including encouraging cheaper flight and hotel options. But just over half (56%) of travelers who are aware their company has a corporate booking tool or agency say they always book trips through these managed channels.

The rise of user-friendly online leisure travel platforms has challenged corporate travel booking compliance for several years.7 But contrary to what some might expect, “rogue” booking (outside of managed corporate channels) is not led by young employees turning to slicker consumer tech. Gen Xers and baby boomers8 are actually significantly less likely to say they always use managed channels (figure 6). Awareness is part of the picture, as Gen Xers and boomers are nearly twice as likely as Gen Zers and millennials to say, as far as they know, their company has no managed channel. But even accounting for awareness, older travelers are more likely to say they never use company channels. Age is a much stronger predicter of booking compliance than travel frequency.

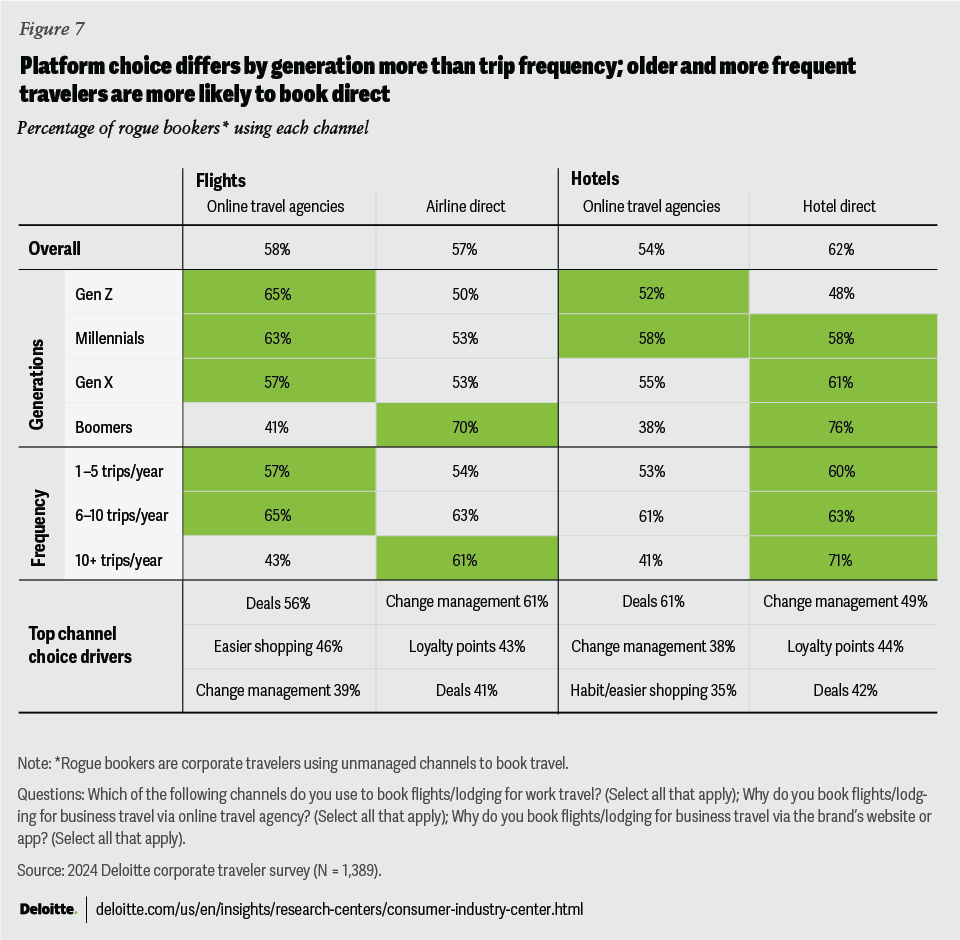

Travelers go “rogue” to book flights and hotels at a similar rate. A similar share of rogue air bookers go to OTAs and airlines’ direct channels, while on the hotel side, direct channels are more popular (figure 7). Younger and less frequent travelers favor OTAs, while older and more frequent travelers drive more of the direct booking (figure 7).

Overall, the biggest driver of booking directly with suppliers is easier management of trip changes, followed by earning loyalty points. On the OTA side, deals are the biggest driver by a big margin, followed by easier shopping and change management. Boomer travelers, nearly half of whom say they book flights and hotels direct, are most motivated by change management and loyalty.

Sustainability: Progress toward more visibility into impact, but most still expect emissions targets will curtail travel

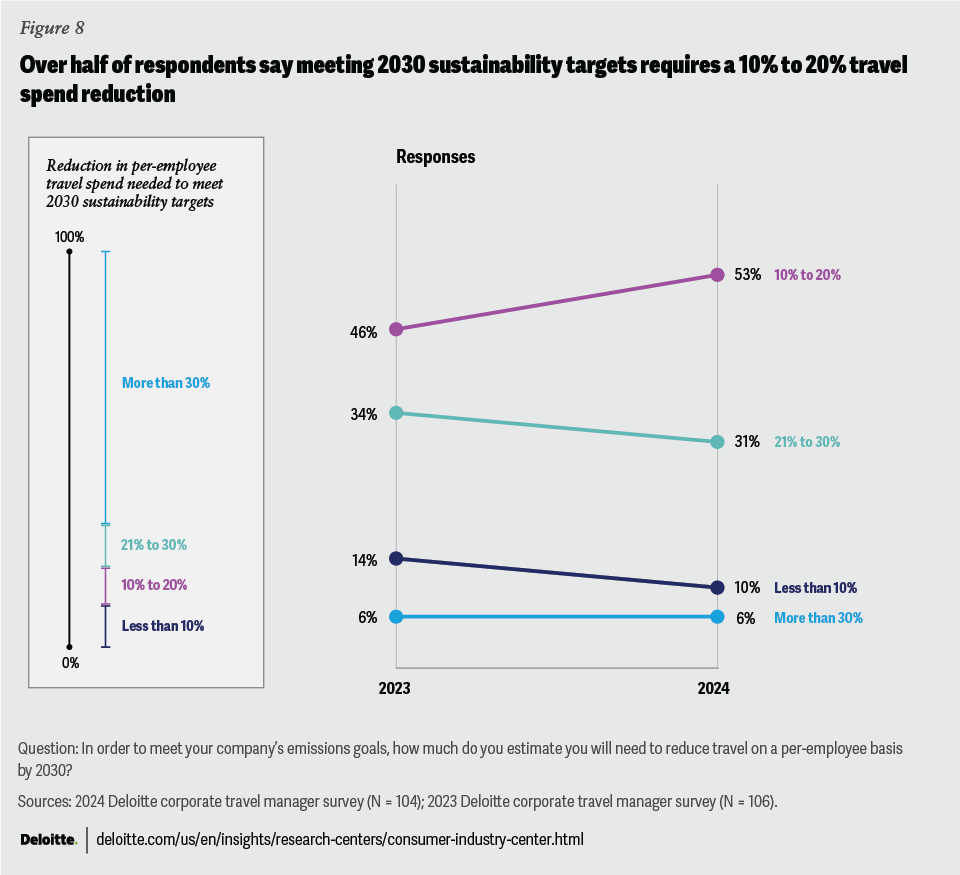

Most travel managers continue to say their companies need to reduce travel to meet sustainability goals. More than half surveyed say they need to cut trips by 10% to 20% (figure 8), as the percentage who predict either bigger or smaller cuts has shrunk. At the same time, more report that their companies have moved toward adopting travel-related sustainability measures, encouraging and enabling employees to make greener travel choices. A third of travelers corroborate that their companies are encouraging them to choose more sustainable providers when traveling for business.

Companies are more prepared and active in their approach this year (figure 8): Forty-six percent say they have a strategy in place to assign travel emission budgets to teams and individuals, up from 30% in 2023. And more companies have integrated into their booking engines information about sustainable aviation fuel and hotel sustainability certifications (figure 9). But many remain in the phase of collecting data and considering plans.

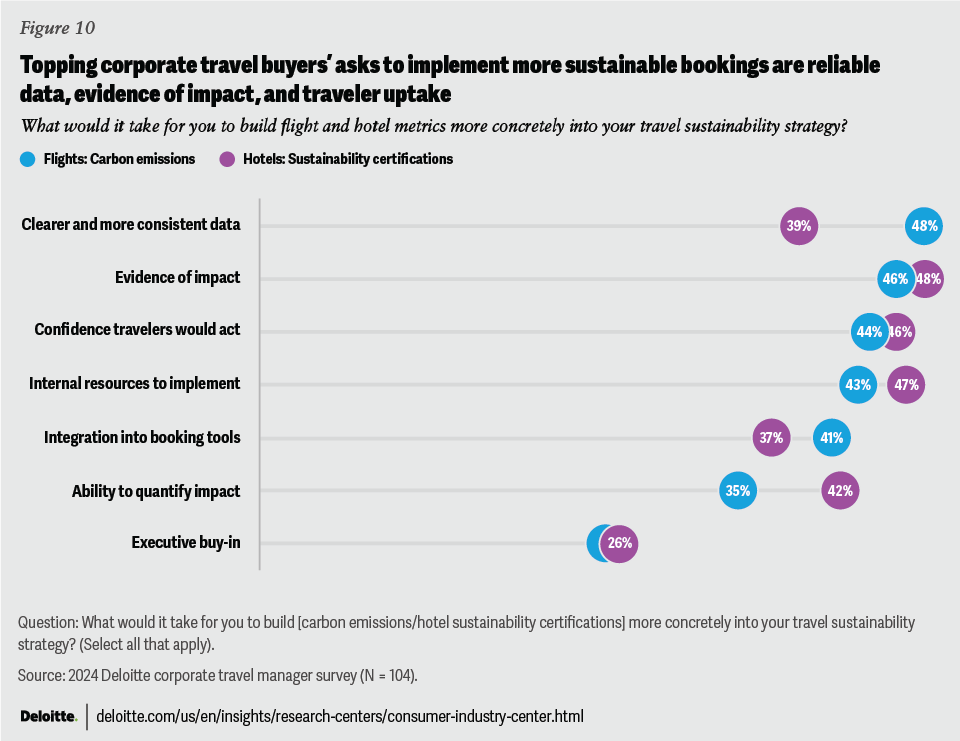

What will it take for companies to include some sustainable travel metrics into their program more meaningfully? A quarter of respondents say they still need more executive buy-in, but other challenges loom larger. Better data, evidence of environmental impact, and confidence that travelers would act on the information all were cited by more respondents (figure 10).

Travelers themselves have yet to widely adopt sustainable travel booking, which is not surprising as most travel managers surveyed note their online booking tools do not support it. One in 10 corporate travelers say they always factor carbon emissions into flight selection, while nearly half do it on occasion. Similarly, one in 10 say they always consider sustainability ratings when choosing hotels, while 53% do it on occasion. Travel managers indicate that the question of uptake is important: Nearly half say that before investing in more concrete integration of sustainability in their travel purchasing path, they want to be more convinced that travelers will take action.

A robust recovery on a rocky road

Corporate travel still lags pre-pandemic figures, but it is well along the road to recovery, growing at a rate significantly outpacing GDP growth. Conferences, sales visits, and client project work are all spurring gains, as companies and employees alike see the value of increasing in-person connections. But even on this upward climb, companies face significant challenges. In the face of high costs and tough supplier negotiations, corporate leaders are balancing travelers’ demand for certain creature comforts alongside the need for more sustainable travel options. As spend approaches pre-pandemic levels, gains are expected to slow down over the next year. This more stable annual growth rate is likely to present some challenges and opportunities as leaders adapt to new norms and priorities.

Methodology

This report draws on two Deloitte surveys. The first surveyed 104 US-based corporate travel managers, executives with various titles and travel budget oversight, and was fielded from May 16 to 28, 2024. The second survey reached 1,389 US-based corporate travelers and was fielded from May 28 to June 3, 2024. In the traveler survey, 834 respondents said they either oversee a travel budget or approve travel requests for their teams. Those respondents are referred to in this report as “budget owners.” Where traveler respondents are grouped by frequency, those groupings are determined by expected number of trips in 2024: Occasional business travelers expect to travel one to five times in 2024; regular business travelers expect to travel six to 10 times; frequent business travelers expect to travel more than 10 times.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}