1. Harnessing electric propulsion technology through alliances and partnerships: Since the future of eVTOL hinges on having a highly energy-efficient and high-performance propulsion system, the industry should focus on leveraging distributed electric propulsion (DEP) technology. eVTOLs need batteries that are light, powerful, long-lasting, cheap, and quick-charging. But achieving this would require the entire industry to work together since it involves developing advanced power sources, a combination of electrical power-producing devices such as electric generators and fuel cells, as well as energy storage devices such as batteries and capacitors. The industry should also invest in advanced technologies such as artificial intelligence, augmented reality/virtual reality (AR/VR), and high-performance computing.

2. Leveraging investments and progress made in ground autonomy: Industry players can benefit from strong tailwinds from the investments made in autonomous cars. On the computing side, semiconductor makers are fashioning powerful chips to allow manufacturers to perform advanced computations that weren’t even fathomable a few years ago. For instance, embracing micro- and millimeter-wave technology in radar sensors is designed to advance collision detection and avoidance capabilities and presents an opportunity to establish safer navigation capabilities.

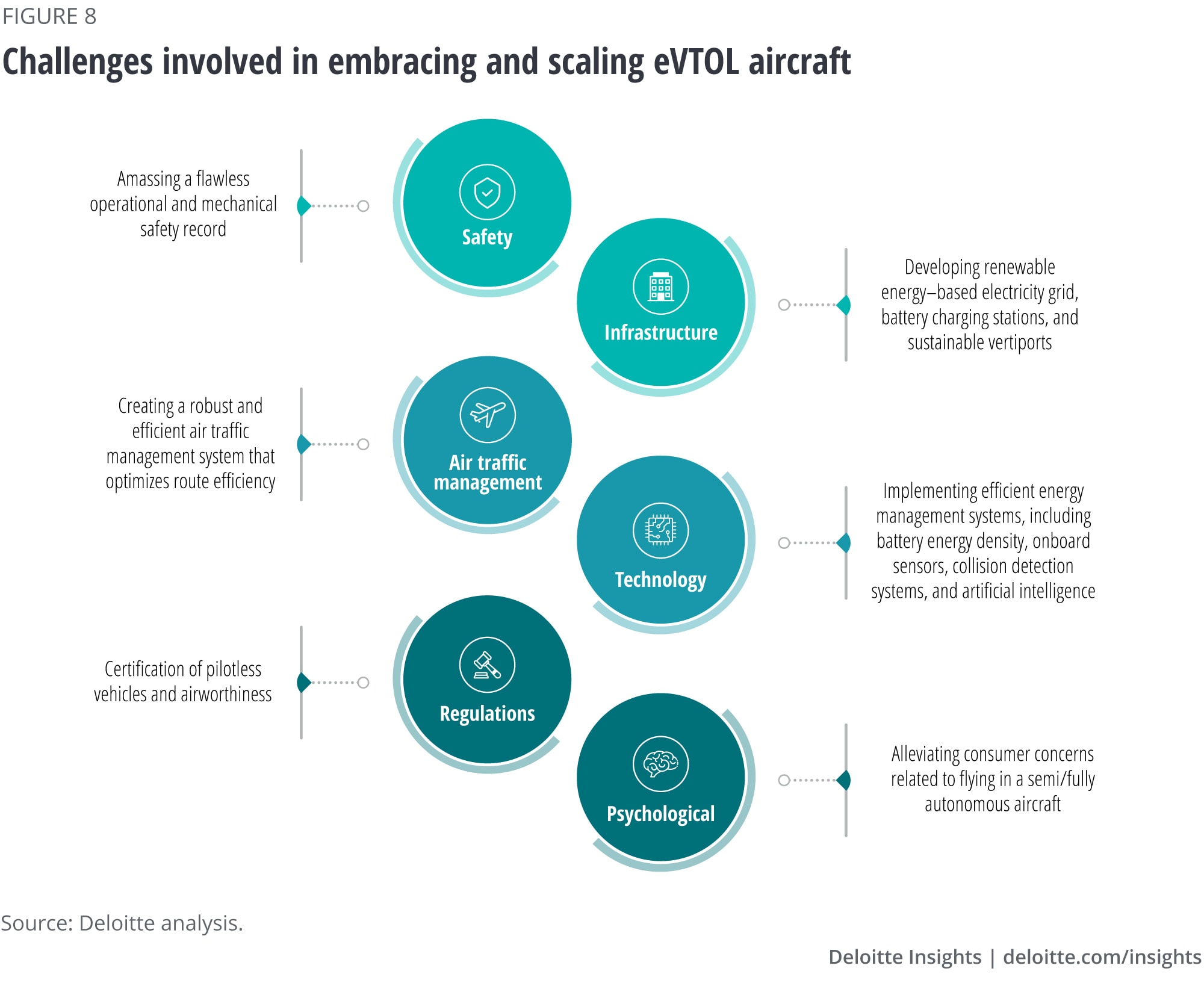

3. Stimulating investments to drive demand and build infrastructure: Aerospace companies should work with the entire aerospace ecosystem, including government agencies and regulators, to stimulate the market through fiscal arrangements, subsidies, and national procurement programs. By working closely with investors and governments, existing industry players and startups can secure investments to drive technology readiness levels to reach market readiness levels. Moreover, the industry should partner with governments by opening funding sources at the city, state, and national level to develop the physical infrastructure, including the electricity grid, electric recharging equipment, vertiports, aircraft hangars, and maintenance areas.

4. Developing the right talent needed in design and engineering: The shift from combustion to electric/hybrid-electric propulsion, piloted to autonomous, and centralized to distributed propulsion means the aerospace industry will likely need access to new skill sets. OEMs should partner with federal agencies, technical programs, and academia to attract, train, and hire skilled workers to meet current and future talent needs. They should also forge long-term partnerships with public and private educational institutions, industry associations, and agencies to develop programs that build a strong connection with companies, creating a skilled workforce for the future.

5. Scale production to manufacture eVTOL aircraft at near-automotive rates: To be commercially viable and economically feasible, the industry should scale its production capacities to levels not seen in the current aircraft manufacturing industry. As the materials used by the aircraft industry are generally more sustainable, advanced, and comparatively scarce, suppliers can demonstrate that the manufacturing processes developed for new materials can produce the needed quantities in a climate-friendly manner at aerospace grade. To truly eliminate emissions, the industry should enable a robust supply of materials with stable procurement costs and fabrication flexibilities, and scrap disposition and recycling capabilities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}