Riding the exponential growth in space has been saved

The authors would like to thank Lars Cromley, Adam Routh, Rudy Sleiman, David Jarvis, and Tarun Dronamraju for their contributions to shaping this study.

Cover image by: Sonya Vasilieff

United States

United States

United States

United States

The economics of space have never been more compelling. Over the past few years, challenges to manufacturing, launching, and operating satellites and other space-based assets have diminished significantly. Satellites have been “miniaturized,” costing less to produce and operate than ever before. And thanks to reusable rocketry, launch costs are much lower today.1 Accelerating these developments, digital and advanced technologies are helping new players to access satellite operators’ data and explore new business applications.

This growth in the global space sector is creating opportunities for new players and new offerings for incumbent ones. 2022 was a record year for the space sector, with 186 successful rocket launches (41 more than in 2021)—the most ever,2 signaling a rapid transformation of the space sector.

While there are several uncertainties and challenges ahead, a pragmatic and collaborative approach could enable steady growth toward a self-sustaining industrial base in the space ecosystem. With the right public and private investment, sector players can collectively build models to capitalize on both near-term and long-term revenue opportunities. Companies—both legacy and new players—should focus on innovation and enable a wide variety of new use cases across end-user industries.

In this report, we take a closer look at where future growth opportunities may exist and what it could take to capitalize on them in a more responsible, sustainable, and efficient manner (see the sidebar, “Study methodology”). Through this report, we hope to provide more clarity into this rapidly growing sector and explore the key areas that may be economically viable and help drive growth over the next few years.

In addition to in-depth interviews with subject matter specialists, Deloitte conducted a survey to understand how space companies are viewing and working toward the future of space development, specifically over the next three to five years. The survey was fielded in December 2022 to 60 senior space sector executives in the United States. The survey aimed to better understand the opportunities, challenges, and potential value of emerging space technologies and other critical trends across the space segments.

A few important factors have contributed to the recent growth in the sector, including advances in technology, increased private sector investment, and rising demand for space data and related products and services.

A major driver of growth in the space sector has been the development of new technologies, such as reusable launch vehicles, SmallSats (satellites of low mass and size, usually under 2,600 lbs.), and CubeSats (square shaped miniaturized satellites). Eighty-two percent of senior executives in Deloitte’s 2023 space survey said that innovation in the space market is a priority for their organization.3

Innovation has made it more cost effective to develop new space systems and launch payloads into space, which in turn has enabled a wider range of organizations to participate in the space sector. The development of SmallSats and CubeSats have particularly increased the interest of private companies and government agencies in investing in this field,4 as it allows for more affordable access to space and new business models, such as constellations (a group of satellites working together as a system with shared control).5 SmallSats accounted for about 95% of spacecraft launched in 2022.6

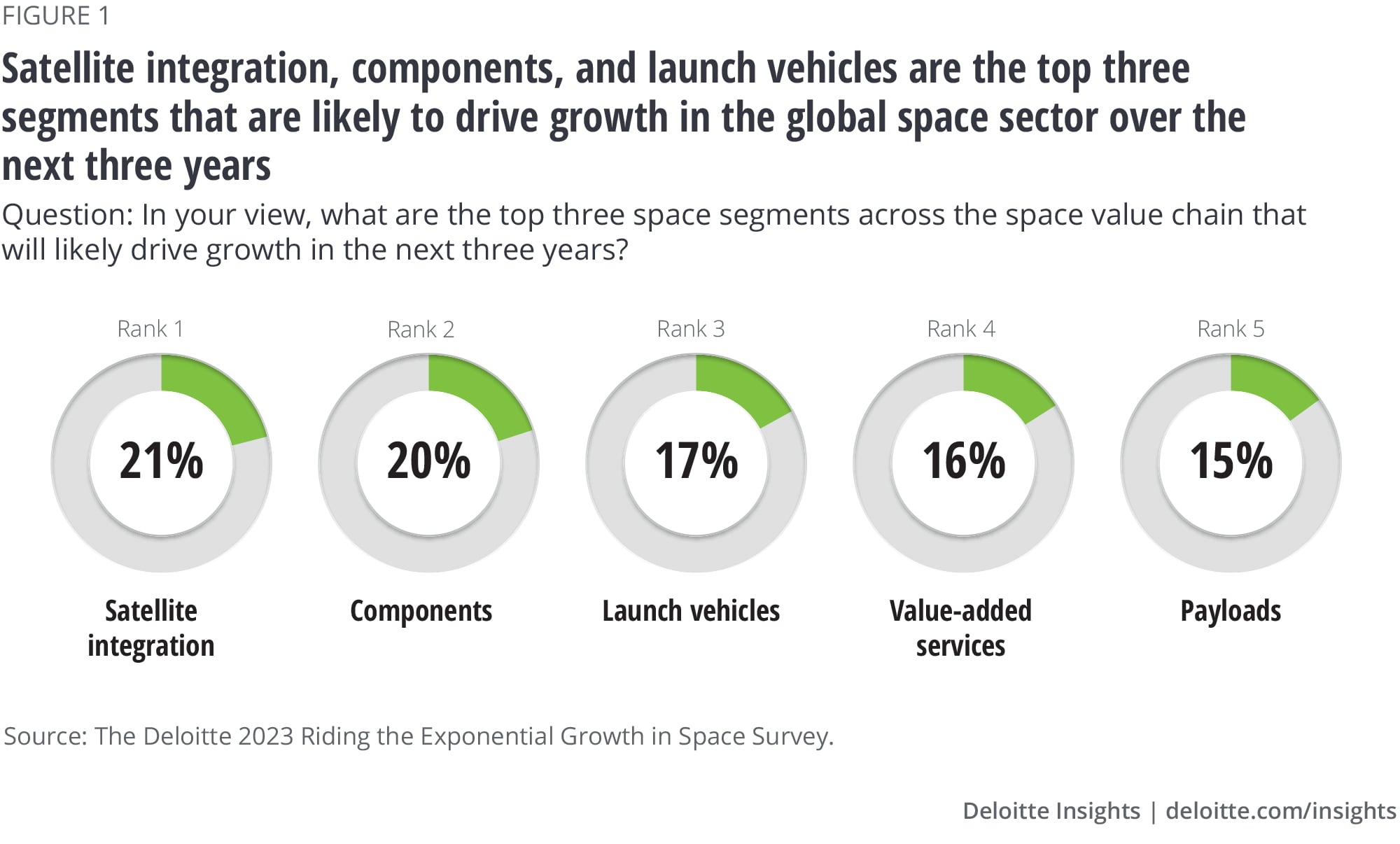

Satellite constellations are also likely to drive the space market in the coming years. As a result, there could be increased demand for satellite integration, components, and launch vehicles (figure 1). Unlike a single satellite, satellite constellations can provide global or near-global coverage, such that at least one satellite is available anytime, anywhere on Earth.7 However, addressing higher demand created by low costs would require launch service providers to increase both the production and launch rates.

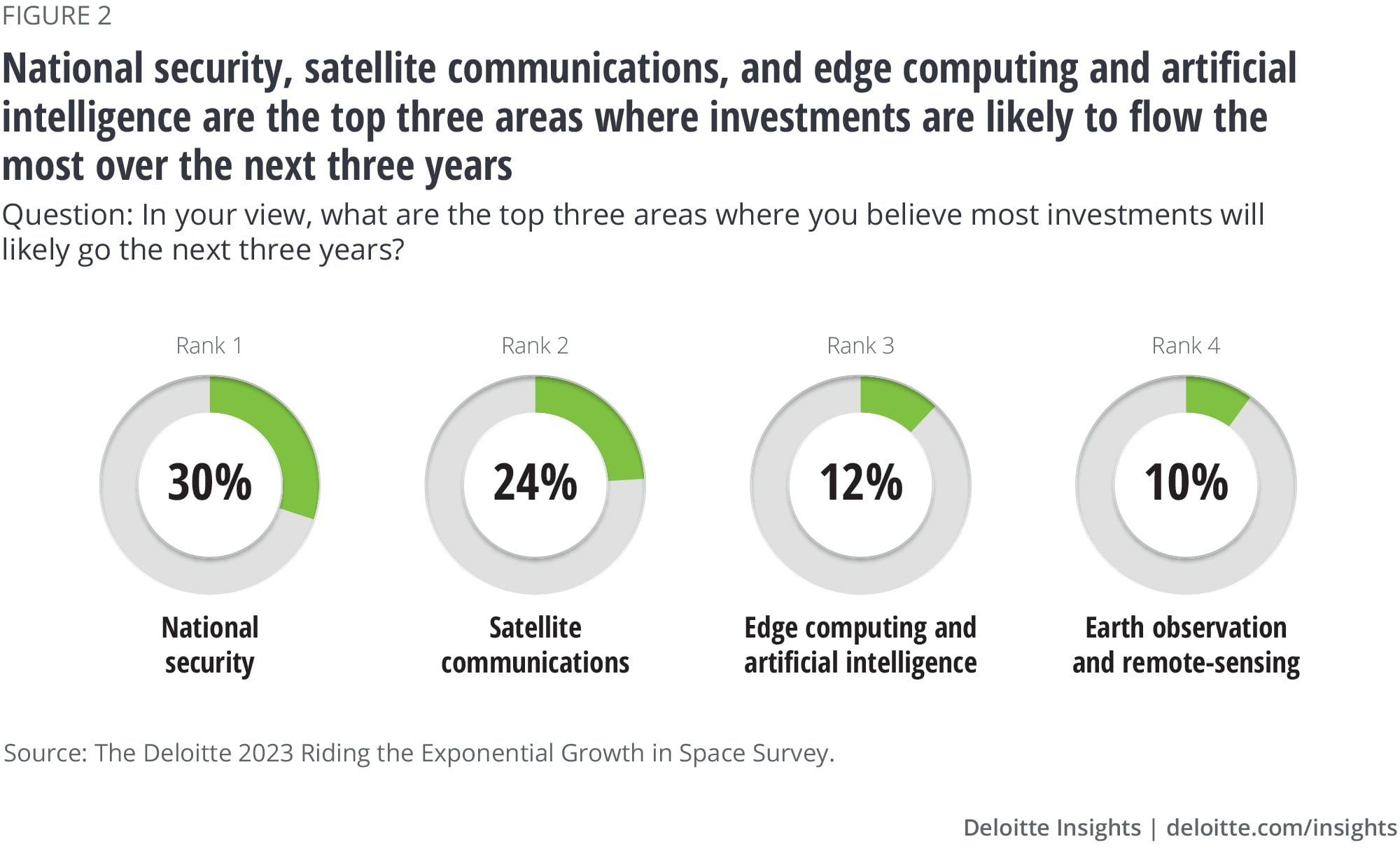

Another important driver of growth in the space sector has been increased private sector investment. A growing number of venture capital (VC) firms and private equity (PE) firms have been investing in the space sector, and more and more private companies are entering the market to provide space-related products and services.8 As of the end of 2022, the global space sector had attracted PE investments of about US$272 billion into 1,791 unique companies since 2013.9 At the same time, investments in the national security space are also rapidly increasing (figure 2). For instance, in the United States, the FY23 national security space budget allocated US$20.8 billion to National Security Space investment accounts, a 19.5% increase from FY22.10

The increase in investments has led to heightened competition and innovation and has enabled new business models such as mega constellations—systems utilizing hundreds or thousands of satellites in Low Earth Orbit (LEO) that deliver services such as low-latency broadband. Deloitte expects over 5,000 broadband satellites will likely be in LEO by the end of 2023 to provide high-speed internet to a million subscribers on all parts of the Earth.11 Moreover, 40,000-50,000 satellites could serve over 10 million end-users by 2030.12

Companies such as SpaceX,13 Blue Origin,14 and Relativity Space15 are investing in the development and commercialization of new technologies such as reusable launch vehicles.16 For instance, SpaceX raised about US$2 billion in 2022 with an ambitious plan for 2023 which includes 87 rocket launches, a sustained moon exploration project, and expansion of Starlink internet service.17 These private companies are also expanding to other segments, such as satellite-based services.

As the space market expands, the role of private companies in the space market will likely increase in the next decade. Ninety-eight percent of senior executives surveyed said that the role of private companies in the space market will likely expand due to emerging trends, such as space data services and in-space manufacturing.18 Going forward, more private companies are likely to bring capital, which can help the sector to grow and start to execute ambitious programs.

The fast-growing space data-as-a-service market, where specialized companies deliver high-quality data directly to their customers, is another key driver.

Government agencies, private companies, and research institutions are all increasingly using space-based data to support a wide range of applications, such as satellite broadband. Communication service providers and earth observation service providers are likely to benefit the most from data generated by satellites.

Specialized space companies can build, own, and operate satellites, delivering data and communications for customers, which would free end customers to focus on enhancing their core business. This solution enables customers to subscribe to space-based data services with custom data sets for tailored use cases.

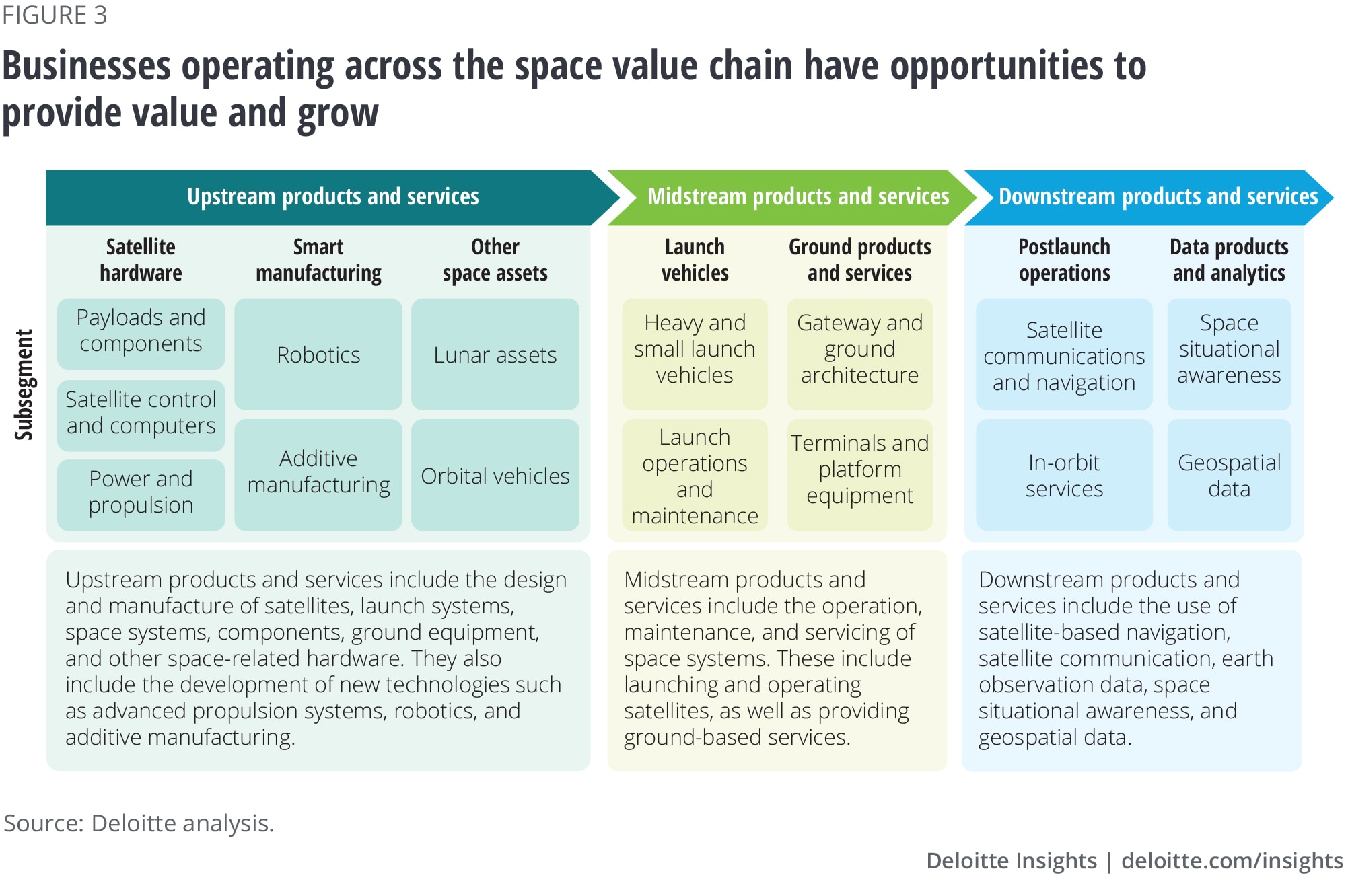

The space value chain refers to the various stages (upstream, midstream, and downstream) and activities involved in the design, development, production, and use of space-related products and services (figure 3). The space value chain is a complex and connected system involving many different actors, including government space agencies, commercial space companies, research institutions, and end-users. Each stage of the value chain is interdependent and requires the participation of multiple actors. The value chain also involves cross-border and cross-sector collaboration, as well as the coordination of various types of private and public investments.

Supply chain disruptions, developing space-grade products and components at competitive costs, and regulatory requirements/timelines for regulatory approval are the top three challenges in the commercial segment according to those surveyed. Other key challenges cited by respondents are shortage of skilled talent, reduced capital investment, mass production to meet demand, and miniaturization of electronic components.

In the space defense segment, respondents cited government acquisition timelines, funding, and shifting priorities in defense as the top challenges in the military segment.

Those surveyed said that regulating commercial space, integrating/ implementing global regulations, and building a transparent regulatory environment are the top three regulatory items.

Respondents noted that space debris, congestion, and security are the top three major environmental or sustainability-related concerns. Other major challenges cited by those surveyed include greenhouse gas (GHG) emissions and environmental impact at launch sites and radiofrequency (RF) congestion.

Source: The Deloitte 2023 Space Survey.

The space value chain is experiencing the emergence of many pure-play companies, which comprise a mix of traditional aerospace companies and space-focused startups. While many of these companies are primarily focused on the design, development, and manufacture of spacecraft, the majority are considering providing new and improved value-added services.19 And although many segments in the space sector are still evolving, the sector could experience faster adoption in less than a decade.

Companies across the broad space value chain that bring the essential capabilities could further collaborate, creating a network of investors, developers, integrators, suppliers, government agencies, academia, and research labs. This ecosystem could help provide a dynamic, adaptive, and holistic network through which companies in the space market can partner and form stronger relationships with stakeholders. Further, this ecosystem can promote collaboration with other end-markets, such as transportation, which are also advancing critical technologies, such as autonomous technology.

(i) Space companies whose primary business or a major segment of their business is Space. These companies build products such as launch vehicles and satellites and/or provide services to consumers from Space. Customers can include both government and nongovernment segments.

(ii) Government agencies, who build, launch, and manage space-based capabilities for national security and scientific research and development. This also includes policy and standards development.

(iii) Non-space companies that are impacted by space commercialization and services. They may be exploring an entry into the space market and could need assistance to get there.

(iv) Academia contributes to innovation through research and development of science and space technologies for the future space missions, and also plays crucial role in educating and supplying talent for the industry.

The space ecosystem can be recognized as a leader in delivering value to key industry sectors through space-enabled capabilities and business models. By leveraging the breadth and depth of expertise across domains, such as commercial, defense, and government, companies can work closely with multiple partners on a variety of exciting initiatives that could help develop new capabilities and build strategic space assets.

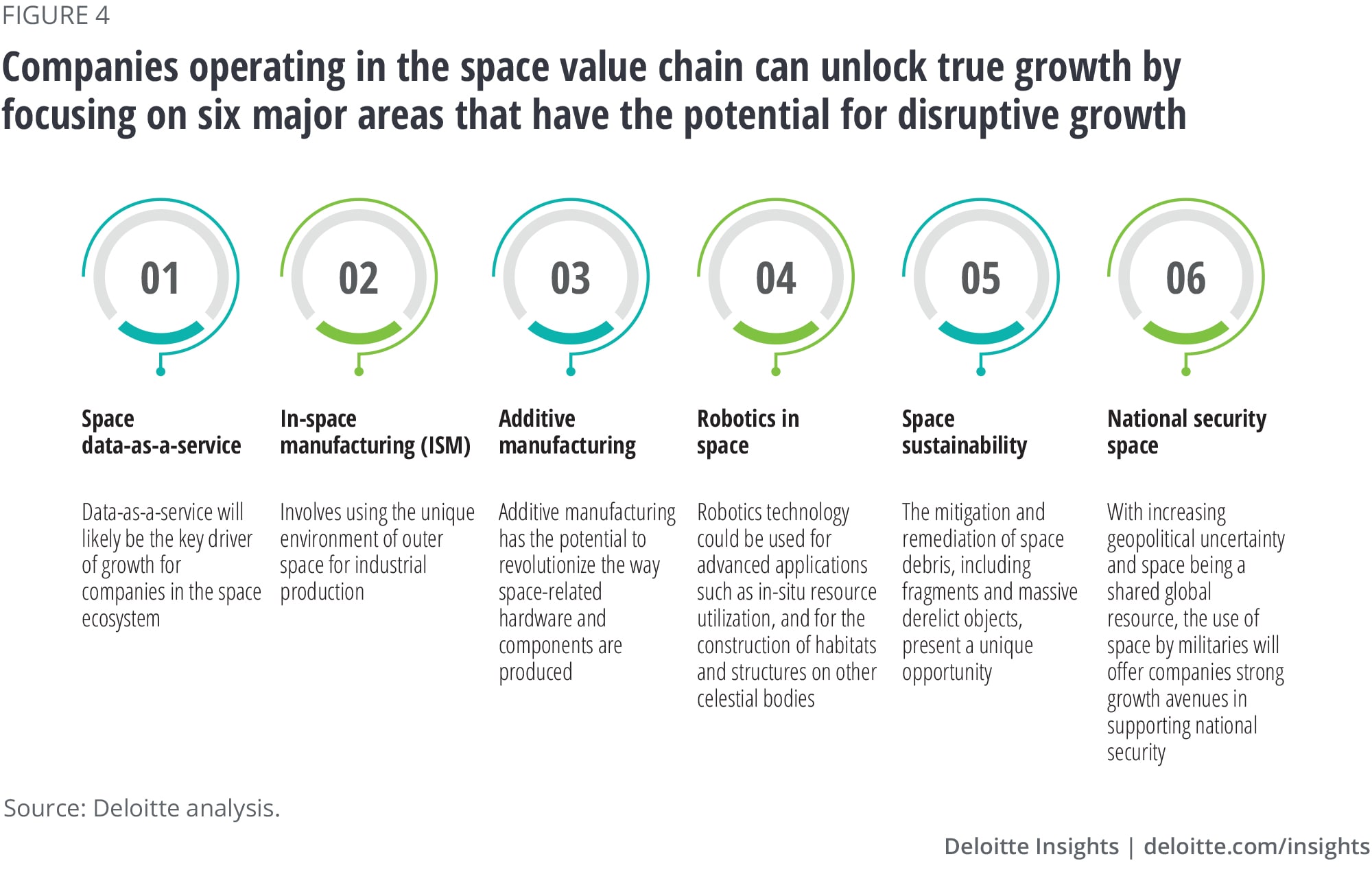

Companies operating in this space ecosystem could unlock growth by focusing on six major areas that have the potential for disruptive growth (figure 4): space data-as-a-service, in-space manufacturing, additive manufacturing, robotics in space, space sustainability, and national security space.

Data gathered from space, i.e., the vast amount of information collected by a wide variety of space-based instruments and platforms, can be increasingly used for a variety of purposes, including military communications, open ocean surveillance, environmental and climate change monitoring, and emergency response. Space data has the potential to support new technologies and industries, such as autonomous vehicles and the Internet of Things (IoT). As the cost of access to space is reduced and advances in technology continue, the amount and variety of data gathered from space will likely continue to grow and could provide valuable insights and benefits to several industries and end-users. For example, the amount of data being sent to and from space will likely grow to more than 500 exabytes of information from 2020 to 2030 (a 14x increase).20 Ninety-eight percent of senior executives surveyed said that demand for space data is increasing as it has broader use and significance across end-markets.21 One potential use case could include using space-based technologies, such as Earth observation and remote sensing, to monitor and manage natural resources, support agriculture, and assist with disaster response and management.

In addition, emerging breakthrough technologies such as edge computing and AI could transform space data services. Edge computing in space is an emerging technology that can open a new domain for software applications, probably similar in scale to mobile apps. As edge computing is all about processing data closer to where it's being generated and enabling processing at greater speeds and volumes leading to greater action-led results in real-time, edge devices on spacecraft could process sensor data (e.g., images) to produce actionable information on the spot.22

AI, too, could be increasingly used in processing space data in these ways:

Space data could enable digital reality technologies (e.g., augmented and virtual reality, and digital twins) for geospatial intelligence and space domain awareness. Potential use cases include:

However, as space companies prepare to offer “space data-as-a-service” solutions, such as imagery and sensor-equipped satellites and systems, for earth imagery and ISR (intelligence, surveillance, and reconnaissance), they should clearly understand who owns the data, who needs which type of data, and how much customers are willing to pay.

In-space manufacturing involves using the unique environment of outer space for industrial production, such as the use of vacuum and microgravity conditions, to produce materials and structures that would be difficult or impossible to produce on Earth. The microgravity environment eliminates forces of sedimentation, convection, and vibration and can be used to better isolate material from containers, which can enable us to study processes and make things that cannot be done on Earth. For example, in the microgravity environment of space, metals can be grown into large, single crystals that are stronger and more durable than those produced on Earth. Moreover, the vacuum of space can be used to produce materials, such as semiconductors and optical fibers, which require a high degree of purity that can be difficult to achieve on Earth. For instance, there is interest in manufacturing semiconductors in space to potentially improve the process and possibly reduce energy consumption by 60%.23

Space companies can make major advances in manufacturing through innovative technologies, including virtual testing, robotics, big data-driven methods, and quality control processes. Specifically, advanced manufacturing including surface engineering, composite manufacturing, virtual manufacturing, embedded sensors, process modeling, and simulation could open new industrial possibilities in terms of design freedom, streamlined production stages, reduced costs, and increased performance.

Advanced technologies, such as additive manufacturing (also known as 3D Printing), in space could also enable on demand manufacturing components and spare parts, reducing the need to launch these items from Earth. For instance, Mitsubishi Electric Corporation has developed an in-orbit additive manufacturing technology for 3D printing satellite antennas in outer space, which could further reduce costs and create more space on the rocket.24

Industry could also realize the additional capability generated by manufacturing parts in simulated microgravity on Earth. For instance, existing technologies such as AI and quantum computing have the potential to simulate/mimic the space environment (microgravity) on Earth which could achieve similar results without leaving terrestrial area.25

However, Deloitte’s 2023 space survey indicates that only 48% of surveyed senior executives believe that in-space manufacturing has the required technologies and capabilities for mass production.26 Currently, there are several significant challenges:

Additive manufacturing technology, which allows the creation of complex objects by building them up layer by layer, has the potential to revolutionize how space-related hardware and components are produced.28 This is possible by enabling the manufacture of complex geometries, reducing the need for specialized tooling, and cutting down on production times and supply chain challenges.

Companies operating in the space ecosystem can consider additive manufacturing to help reduce the cost of space missions by simplifying the manufacturing process and reducing some of the need for specialized tooling, thus making hardware production more affordable. Further, 3D printing technology has the potential to enable the development of new technologies, such as additively manufactured propulsion systems and high-performance materials. Examples of companies experimenting with additive manufacturing include:

However, there are challenges that need to be overcome, such as ensuring the compatibility of materials used in 3D printing with the harsh environment, radiation, vacuum and temperature variations, and microgravity in space, in addition to the control and characterization of the printed materials. With increasing demand for space products, another challenge is the time it takes to 3D print for scaling up production. Additional investment and research may be needed to address these challenges, such as the development of specialized 3D printing techniques that may be better suited for space products and the use of space-qualified materials.

Robotics play an important role in space exploration, enabling the space sector to remotely operate and control spacecraft, rovers, and other devices to explore and study celestial bodies. This technology has advanced significantly over the years, allowing the creation of more capable and versatile robotics systems for space exploration. One of the most significant examples is the use of robotic rovers over Mars. The Mars rovers, such as NASA’s Mars Exploration Rovers and the Mars Science Laboratory, have been used to explore the Martian surface, study the geology and atmosphere of the planet, and search for evidence of past or present life.33

Robotic arms can also be widely used on spacecraft and space stations to perform tasks such as servicing, maintenance, and assembly. NASA’s Shuttle Remote Manipulator System (SRMS), better known as the Canadarm, was used on the Space Shuttle to move payloads and perform other tasks.34 The International Space Station (ISS) also has robotic arms that are used for tasks such as moving cargo and maintenance.35 NASA’s Robotic Refueling Mission (RRM)36 and the European Space Agency’s (ESA) Automatic Transfer Vehicle (ATV)37 have been used to refuel and repair satellites in orbit.

However, declining launch costs and manufacturing costs of satellites could create a challenge for developing robotics for satellite servicing, as the cost of servicing the satellite could exceed the cost of replacing the failed satellite. Nevertheless, retiring failed satellites increase space debris, and on-orbit servicing could be a solution.

A variety of factors, including the launch of new satellites, the collision of existing satellites, and the abandonment of old satellites are resulting in space debris and orbital congestion38—that is the increasing amounts of debris and satellites in Earth’s orbit. Specifically, the launch of new satellites has greatly contributed to the problem of space congestion. According to LeoLabs, a company that tracks satellites and space debris, there are over 6,000 active satellites rotating around Earth as of the end of 2022.39 Another major contributor to debris is the collision of existing satellites. The 2009 collision between the Iridium 33 and Cosmos-2251 satellites is a notable example.40

Space debris includes anything inactive or uncontrolled that is orbiting the Earth—from defunct satellites and spent rocket stages to fragments of broken spacecraft and small debris, such as screws and bolts, that is orbiting the Earth. According to the ESA, about 2 trillion pieces of debris are 0.1 millimeters (mm) in size and 128 million pieces of debris are of 1 mm in size.41 These include non-man-made pieces of debris, such as micrometeorites. Space debris management can be a “need of the hour” for the industry due to expectations of rapidly increasing spacecraft launches in the near future.

This growing space debris poses several threats, but the biggest is to operational satellites. Collisions with debris can damage or destroy active spacecraft in orbit, leading to service disruptions for telecommunications, navigation, and other critical applications. The accumulation of space debris could lead to a phenomenon known as the “Kessler Syndrome” in which the density of debris in orbit becomes so high that collisions between debris objects create even more debris resulting in a self-sustaining cycle of collisions.42 This could make certain orbits unusable for generations and may hinder the continued use of space. Advanced technologies such as AI and ML can help in predicting the satellite and debris position with greater accuracy.

Governments and industry are responsible for tracking space debris and protecting space-based assets and the environment. They could consider measures to mitigate these threats, such as:

The importance of space for national security and the global economy has made space a critical domain for broader strategic competition. This has driven governments to invest in space capabilities that offer greater operational resilience and capability.44

This increased competition is resulting in advancements in technology and a growing market for some space-based products and services. Specifically, there is growing demand for space-based assets and technologies for national security purposes including the use of satellites for reconnaissance, navigation, and communication. Moreover, 98% of senior executives in the survey said that growing commercial launches will benefit military users by enabling capabilities at a lower cost.45

Today, space for national security is not just limited to advanced militaries—many countries are investing in their own space capabilities to improve their national security.46 The House Armed Services Committee’s subcommittee on strategic forces in June 2022 passed proposals for the Fiscal Year 2023 National Defense Authorization Act.47 The strategic forces panel, which covers military space, missile defense, and nuclear weapons policy and programs, advocated for increased use of commercial space technology and data from commercial satellites.48 As a result, militaries may be likely to increase their buying of the best off-the-shelf technology and to partner with commercial firms to invent new technology. In this way, companies could capitalize on renewed demand from governments who are eager to leverage space to protect their nation’s security.

The full potential for companies operating in the space ecosystem is yet to be realized. Recent advances in technology, rapidly increasing private sector investment, and rising demand for space data and related products and services are propelling growth in the sector. The top three areas for likely investment in the short term include national security, satellite communications, and edge computing and artificial intelligence.49 The coming decade could be an era of mega constellations, with thousands of new satellites launching into orbit, resulting in greater satellite connectivity. The planned launches could create demand for new and advanced ground stations to communicate with large volumes of satellites and to monitor debris and sidestep collisions.50

Public-private collaboration as well as international cooperation will be important in scaling these opportunities. In addition, the role of private companies in the space market will likely continue to expand due to emerging trends, such as space data services and in-space manufacturing.51 And to meet growing demand for space data, a new market could emerge to store data in orbit through developing data centers and value-added services such as data refining and processing. Unlocking this potential requires concerted efforts across the broader space ecosystem to prompt infrastructure investment and incentivize demand.

Challenges and opportunities abound for both new entrants and long-established players as the space market unfolds over the coming years. Business and technology innovations are expected to continue to drive down costs and expand access to space. Business models will likely shift from a few, very expensive and bespoke solutions to higher volume, lower cost, and more standard offerings. Companies considering entering the space market, as well as those already established, should evaluate their ability to adapt to these shifting business models and the maturity of their processes and production systems to support higher volumes at lower costs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}