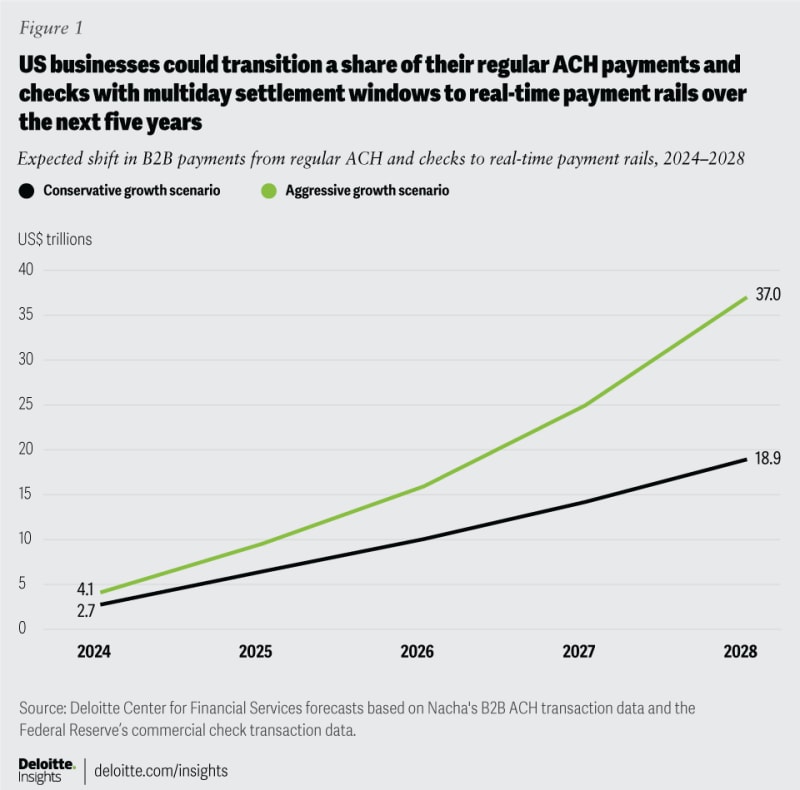

Most B2B payments are slow and vastly inefficient

For decades, paper-based B2B payments have been fraught with inefficiencies. They are slow and often expensive.6 Consider the US$8.9 trillion in commercial check payments in the United States that companies still use for record-keeping purposes.7 Meanwhile, many of the nonpaper-based B2B ACH payments are still handled through an end-of-day batch process and settled within two to three business days. Yet, it remains one of the most cost-effective payment methods, as US businesses made US$52.5 trillion in ACH payments in 2022.8 Same-day ACH can offset some of these inefficiencies for businesses at a domestic level.

And the US$37 trillion cross-border B2B payments9 can be even more complex, expensive, and time-consuming. The challenges businesses had with B2B payments in supply chain financing during the pandemic is one example.

In a survey of global business executives, about two-thirds of respondents said they typically pay US$10–$50 in cross-border fees; a similar proportion paid 0.25%–3% in foreign exchange fees.10 And about 70% reported delays of up to 10 days in receiving or sending cross-border payments, with businesses in Singapore and Germany reporting the longest delays.11 When asked about their payment methods, more than one-half used wire transfers (one of the most expensive methods) and bank transfers; 28% used e-checks; and 17% used physical checks and cash.12

Some of these issues may not just be related to the payment, but to the nature of the transactions and the parties themselves. Transitioning to real-time payments, therefore, may not be a panacea for all challenges, but it should help address some. For instance, real-time payments can improve corporate treasurers’ and finance teams’ payments experience. In a 2022 survey of US finance executives, 47% of respondents said that creating a B2B payments customer experience similar to P2P payments is their most important payment-transformation initiative for the year ahead.13 In another survey of US real estate executives, although only 1% used real-time payments, 84% of them believed that RTP will replace checks for making payments.14

Benefits of B2B RTP could extend beyond payments

In addition to driving business growth across borders and giving access to new markets, real-time payments would also add more transparency to the otherwise fragmented and unpredictable B2B payments landscape. Many RTP systems use International Organization for Standardization (ISO) 2022 messaging standards that enable two-way communication, such as “request for payment,” “request for information,” and “confirmation of payment.” Based on the ISO 20022 standards, RTP would also allow banks to overlay richer insights and value-added services and help modernize B2B transactions end to end, such as automated matching of purchase orders to invoices, virtual account services, e-invoices for payment initiation, and account reconciliation for B2B clients. These value-added services could be even more important in an increasingly networked economy, where businesses are more intertwined, and faster flow of information and faster transfer money go hand-in-hand. They would become table stakes.

In particular, real-time payments could benefit many small and midsized businesses that are challenged by limited transaction visibility, high processing costs, manual invoicing and accounts payable processing, and payment delays in their B2B payments.15 The speed of real-time settlement should free up businesses’ working capital, reduce the need to maintain high cash buffers, and increase the velocity of money in the economy.16 It could also give these businesses flexibility to pay and receive payments closer to the due date. Complementing real-time payments with real-time balance and transaction reporting could improve cash visibility. In addition to faster money flows and richer data, RTP could help businesses mitigate check kiting (where fraudsters take advantage of the float time it takes to settle checks in order to transact against uncollected funds).17

Taking off the runway in the B2B RTP space domestically and across borders

Many banks have started to launch RTP integrations for their corporate clients in the United States. In 2019, Wells Fargo and HSBC offered their US business customers application programming interfaces (APIs) to integrate to the TCH RTP system, allowing them the ability to send and receive faster payments.18

Aiming to be early movers in this space, payments network firms have launched their own cross-border real-time payment services for businesses.19 Similarly, some technology organizations and fintechs are experimenting with digital currencies to facilitate decentralized cross-border value exchange over blockchain.20

Instant B2B payments across borders are in the pilot stage—for now

Cross-border B2B payments is another untapped market with enough room for multiple solutions to coexist at a global level, including truly interoperable real-time payment rails in the next five years. In 2022, SWIFT, TCH in the US, and EBA Clearing in Europe launched a pilot platform for cross-border payments in USD and Euro, called Immediate Cross-Border Payments (IXB).21 This platform aims to expand to other currency corridors as well. In a bilateral exchange, Thailand and Singapore enabled cross-border payments between the two countries by linking their real-time payment networks.22

{kind=link}