The world needs carbon markets. Here’s how to make them work better.

Carbon markets are an essential mechanism for accelerating global decarbonization, but stakeholders should collaborate to make them robust, transparent, and trustworthy.

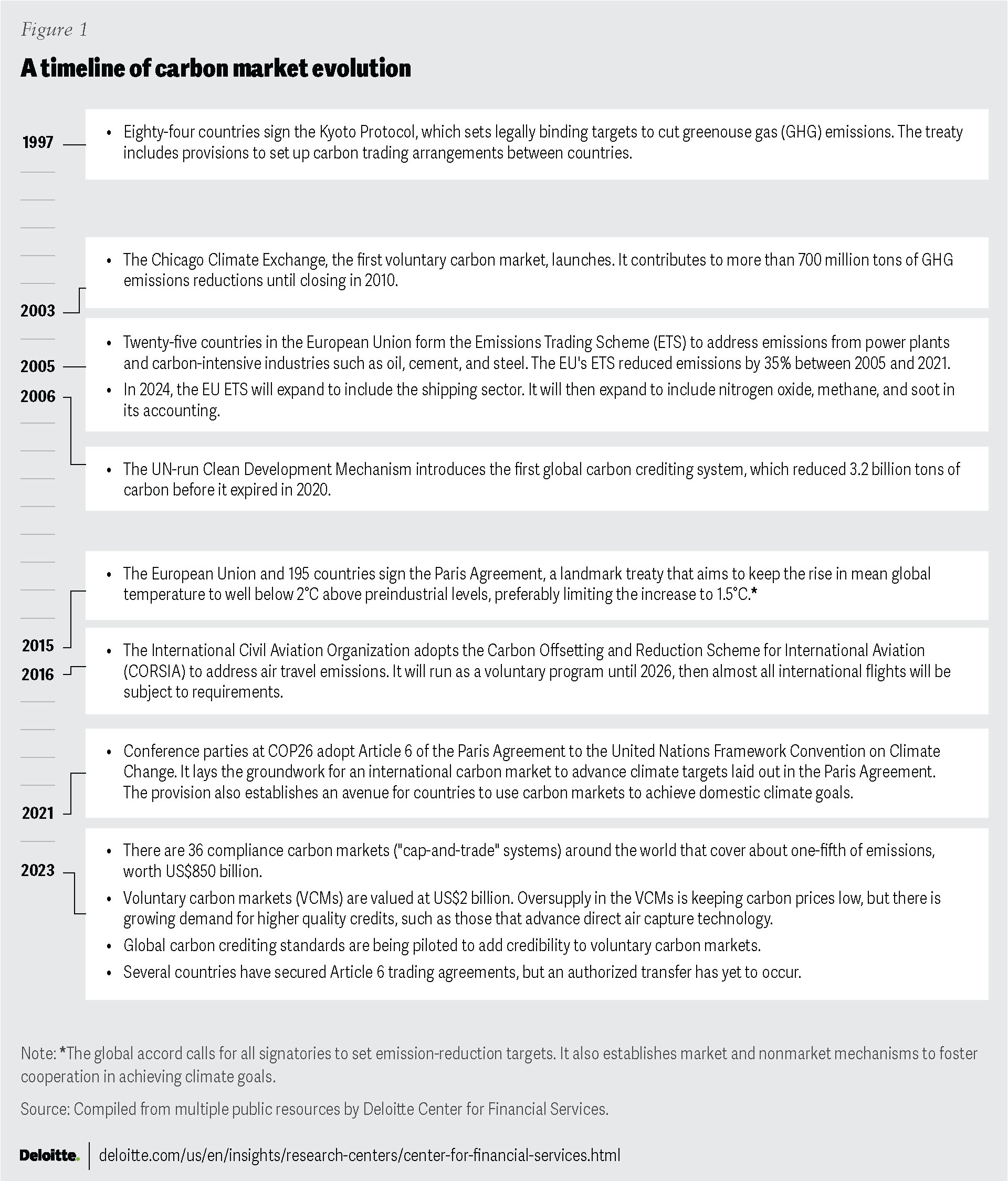

The race to net zero is accelerating by the day, and globally integrated, transparent, and well-managed and efficiently run carbon markets could provide the much-needed boost to reach the finish line. Yet carbon markets are in flux, despite years of international negotiations, significant investments, and widespread consensus acknowledging the role they should play in the global energy transition.

With less than a decade to avert the worst impacts from global warming, though, it’s time to take a fresh look at how carbon markets can support the transition to a low-carbon economy. According to Deloitte’s analysis of the current state of the carbon marketplace, there are several steps stakeholders can take to accelerate this evolution, including: boosting integration across markets and platforms, establishing globally uniform accreditation standards, and bolstering the supporting market infrastructure to make carbon trading easier and more efficient.

Carbon markets offer a critical bridge to long-term climate solutions

While avoiding and reducing emissions should always be the top priority for every country and organization, carbon markets can be a bridge for abating emissions in the decades it may take to develop technologies to complete the energy transition. They can also provide hard-to-abate sectors such as oil and gas, shipping, aviation, heavy industry, cement, and steel a quick and viable path to climate change mitigation while they make concerted efforts to decarbonize.1

Even with drastic cuts in emissions by all sectors in the global economy, there will still be a clear need for carbon credits. For instance, for the 1,000 largest companies to reach their net-zero targets by 2050, they will likely need to reduce gross emissions by 14.5 gigatons per year, the equivalent of about one-third of global emissions today. However, these aggressive abatement measures are unlikely to be enough: These companies would still be left with 7.9 gigatons of residual emissions, which carbon markets could alleviate by funding carbon reduction solutions outside of their value chain.2

There are now 36 “compliance carbon markets” that offer cap-and-trade programs for heavy polluters. Together, these markets represent sectors responsible for nearly 20% of global greenhouse gas emissions.3

The voluntary carbon markets (VCMs), where companies and governments can purchase credits, have grown significantly in the past two years and are currently valued at US$2 billion. By comparison, compliance carbon markets are worth more than US$850 billion.4

What are the different types of carbon credits?

There are two main types of carbon credits: avoidance credits (or reduction credits) and removal credits. Avoidance credits are designed to avert or reduce greenhouse gas emissions through technology, or nature-based improvements in industrial methods and processes. Removal credits, on the other hand, are designed to catalyze either natural or tech-engineered solutions to extract emissions from the atmosphere or water. Carbon removal credits are typically available in much smaller volumes and trade at a premium to avoidance credits, since they have greater longevity and may be more effective in reducing historical emissions.

The voluntary carbon market ecosystem continues to expand in sophistication, complexity, and number of participants. It includes project developers, registries, brokers, exchanges, rating agencies, standard-setters, and financial intermediaries. The sheer number of intermediaries has further exacerbated the fragmentation of voluntary carbon markets, which has driven their structural and operational issues, including a lack of trust in the credibility of carbon credits, and concerns about transparency. This has undermined confidence and suppressed demand: Companies such as Gucci, Nestle, and easyJet have stopped including carbon credits in their climate pledges and net-zero targets.5

Despite these challenges, voluntary carbon markets can still be effective in supporting broader decarbonization efforts. A recent analysis by the climate research and data provider Trove Research found that companies who used carbon credits to neutralize at least 5% of their operational emissions cut emissions twice as quickly as companies that did not purchase carbon credits at all.6

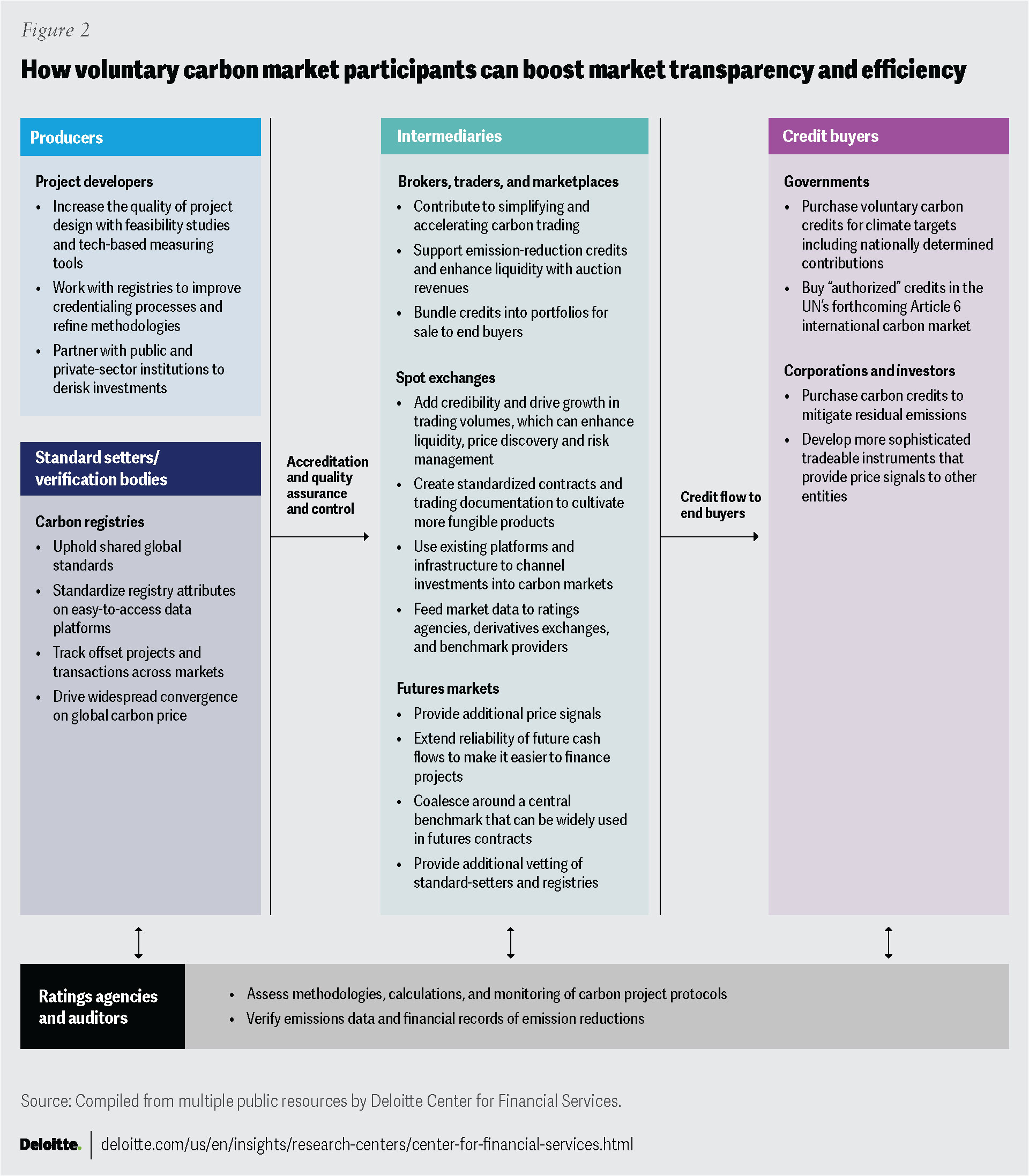

And if designed well, carbon markets could spur investments in innovations that can accelerate decarbonization at scale (figure 2). There is a growing demand, for example, for capital to be directed to a wide array of startups piloting carbon capture and storage and carbon dioxide removal technologies. Every Paris Agreement pathway modeled to limit global temperatures requires advancements in carbon removal technologies in conjunction with robust decarbonization efforts.7

Analysts from BloombergNEF estimate that the value of VCMs could reach US$1 trillion by 2037 if the structure of voluntary carbon markets improve, particularly by relieving concerns about the quality of carbon credits and placing more emphasis on removal technologies.8 Currently, only about 3% of carbon credits are based on pure removal projects. Durable removal credits, which effectively cancel carbon emissions over a long period of time, are rare.9 If carbon markets grow to include more of these credits, they could increase in value quickly and meaningfully.10 Conversely, if supply is limited to low-quality credits (such as if their climate benefits aren’t adequately measured or verified), these markets could falter.

Carbon markets can also accelerate a more just transition. Since many suppliers are located in developing and emerging economies, capital tends to flow from North America and Europe into these regions. Last year, almost 98% of carbon offset retirements—which take credits out of circulation once a stakeholder claims the benefit—originated from Asia-Pacific, Latin America, and Africa.11 In addition, there are also other programs such as the World Bank’s Carbon Initiative for Development that facilitate the flow of private capital for clean energy access in low-income communities.

In a more ideal scenario, carbon project and transaction data would be visible and transparent across registries or platforms so participants can track the certifications, ownership, sale, and benefits claimed by carbon credits. Offering that level of transparency could also hold project developers, brokers, and others accountable to the same standards. Such a system could also support the development of a consistent definition of “high-quality” carbon credits. Several industry-led initiatives, including the Integrity Council for the Voluntary Carbon Market and the Voluntary Carbon Market Integrity Initiative, are already working to address these concerns and build credibility into the supply- and demand-side of the voluntary carbon market.12 Intergovernmental organizations are also bolstering transparency and innovation, such as the Climate Warehouse initiative for designing and testing end-to-end digital infrastructure to support the carbon market ecosystem.

The Paris Agreement Work Program could also bring more consistency to cross-border trading. In particular, Articles 6.2 and 6.4 of the rulebook set up a functional architecture for implementing international carbon markets and clarify how governments should account for credits in national emissions targets. Negotiations over the adoption of these rules have been challenging, however, and new guidance may also bring uncertainty over how voluntary carbon markets fit into a global carbon trade if they are not Article 6-compliant.13

Integrating carbon markets can drive growth

In light of these challenges, it’s essential to evolve the carbon markets to fully meet the needs of a growing and diverse set of market participants. Many global banks are establishing carbon trading desks to explore emerging opportunities and building trading platforms to fortify carbon market infrastructure. Oil companies and commodities traders are also hard at work expanding their carbon trading capabilities.14 These initiatives indicate a strong demand for carbon credits, but every stakeholder should push for greater integration across markets, and greater clarity in frameworks, principles, and standards. They should also focus on refining accreditation standards, harmonizing registry data, and unifying carbon pricing mechanisms.

One step to integrating markets is for governments to leverage bilateral and multilateral trade agreements to mobilize financing and investment, develop common guidelines, and remove barriers to the transfer of technology supporting cooperative approaches under Articles 6.2 and 6.4. For example, Switzerland recently entered into a memorandum of understanding with Ghana and Vanuatu to enable the trading of carbon credits to meet Switzerland’s national climate goals,15 as did Singapore and the Dominican Republic.16 Similarly, the Climate Market Club, comprising national governments and private entities, is aiming to gain consensus on common principles and approaches for piloting activities under Article 6.2.

These mechanisms encourage cooperation between countries and offer flexibility in how participants engage in cross-border transfers. Around the world, 84 countries intend to use Article 6 trading to meet their climate targets.17 As governments execute Article 6 pilots and share support for capacity-building, neighboring countries could see greater collaboration and integration. These regional carbon markets may lay the groundwork for an eventual global carbon trading system.

Creating more “linkages” between cap-and-trade systems could also be beneficial. “Linking,” or connecting of compliance markets, can bring in more participants to buy and sell carbon credits and to enable greater cost savings. Linkages could also boost the premium for high-quality carbon credits and increase market liquidity.18 Linked compliance carbon markets could also lead to carbon price and abatement costs to converge, making it harder for industries to compete for offset units at a bargain. Since all entities receive the same price signals, they are less likely to transfer operations to a country or region with less stringent climate policies or lower emissions costs (what is known as “leakage”).19

In addition, if companies in regions with higher abatement costs can purchase allowances from regions where abatement costs are cheaper, the overall cost of emissions reductions may fall, potentially prompting countries to set more ambitious climate targets for their public and private sectors. An international linkage of worldwide cap-and-trade systems could reduce the total expense of achieving national emissions targets by as much as 32% before 2030, and by 54% before 2050.20

Market convergence can boost efficiency

As carbon markets become increasingly interlinked and governments take greater action to prompt voluntary market participation, fungibility generally improves. This can make trading networks more efficient, credible, and liquid.

On the supply side, carbon credit certifiers are producing more voluntary carbon credits that can be traded in regulated regimes. The Swedish government plans to use voluntary credits to meet some of its national climate targets, for example.21 In addition, countries such as Chile, Colombia, Singapore, and South Africa permit mandated firms to pay the national carbon tax using carbon credits from the voluntary markets.22 Traders that primarily transact in compliance markets are also increasingly buying voluntary carbon credits to hedge for future uncertainties.

Some countries are taking even more assertive action to promote carbon trading. Japan, for example, recently unveiled the GX League, a 10-year initiative that created a voluntary carbon market for corporations. In the future, the program will grow to include a cap-and-trade program and carbon levy.23 So far, companies responsible for 40% of the country’s emissions have chosen to participate since the market became operational in April 2023.24 Similarly, Australia’s government has also put a voluntary carbon market in place that’s primarily centered on Australian government-issued credits.25 Businesses can purchase these credits if they exceed the emission caps established by the Australian government. In both instances, increasing the comparability of credits has made supply more trustworthy and easier to track.

Designing an integrated carbon trading system requires participation from all stakeholders

Evolving to a more robust, efficient, and transparent carbon market will require greater collaboration among various stakeholders. The following is an outline of what each stakeholder group can do to advance these goals.

Governments, policymakers, and regulatory agencies: Clarify guidelines to build confidence

- Act quickly to remediate allegations of misconduct, including “phantom” credits (credits that are traded in carbon markets after greenhouse gas mitigation efforts ended) and carbon credits that overstate the extent of greenhouse gas mitigation.

- Work with peer agencies within and across jurisdictions, such as the US Securities and Exchange Commission, the US Commodity Futures Trading Commission, the European Commission, and the United Kingdom’s Financial Conduct Authority, to align monitoring and oversight protocols.

- Promote the production of centralized trading platforms for voluntary carbon markets. For example, Australia and Japan developed government-issued carbon credits to legitimize assets and promote consolidation.26

- Provide clearer and more comprehensive guidance on how best to participate in emerging Article 6-inspired initiatives.

- Publish strategic priorities and certification standards that will encourage private businesses that seek public funding to direct carbon credit flows to certain projects or geographies.

Industry groups, climate alliances, and associations: Identify and solve shared industry challenges

- Draft and release voluntary standards clarifying how organizations and countries can use carbon credits in their transition plans, specifying the extent to which they fit into net-zero frameworks and how those actions should be disclosed.

- Advocate for stock and futures exchanges to participate in carbon markets e.g., introducing new products, platforms, and listing standards.

- Develop guidance on liquidity and collateral management.

- Provide clarity on contracts (e.g., standardized contracts, trading rulebooks, and terms and conditions) and show how they should treat various types of carbon credits.

- Help participants navigate divergent legal structures in other jurisdictions.

- Accelerate efforts to find convergence on a global carbon price or set a minimum price floor.

- Set and enforce a definitive global threshold for high-quality carbon credits that set out a common approach for project developers’ disclosures. They should also continue to evolve as research on climate change mitigation and the effectiveness of offsetting continues to advance.

Carbon registries: Boost confidence by improving transparency and upholding quality standards

- Make data on projects more accessible to market participants and increase transparency by providing data feeds on the sale and transfer of carbon credits.

- Assess ways to link national and private registries (carbon credits cannot currently be transferred between registries).27

Buyers: Prioritize emissions reductions and take a rigorous approach to vetting offsets

- Reduce emissions across the organization’s value chain first. Then, use carbon credits to account for residual emissions.

- Collaborate to pool investments in early-stage financing of carbon projects, catalyze new types of nature-based activities, and provide upfront investments for nascent technologies (even if they come with long-term contracts).

- Choose carbon credits that have been vetted by registries and other certification bodies to produce equitable outcomes (those that support local and Indigenous communities, respect traditional land rights, and preserve ecosystems) in the locations where underlying projects are carried out.

Sellers and project developers: Spur capital flows

- Offer legal and insurance buffers against common risks including insolvency, and the reversal of sequestration through events like wildfires.

- Trade on public exchanges (instead of making over-the-counter trades) to reach a larger pool of market participants and further establish credibility.

Financial intermediaries, including exchanges, brokers, banks: Improve access to capital and drive efficiencies

- Establish more robust spot price benchmarks and risk management tools. Carbon markets need to continue working toward common benchmarks that can provide a fair market price, facilitate long-term contracts, and reduce information asymmetry. This is similar to how West Texas Intermediate and Brent Crude operate as central benchmarks for crude oil.

- Develop futures contracts to enable greater market participation and more robust risk management. These contracts could also support early-stage climate investments or reduce the cost of capital for project development.

- Enhance high-volume trade infrastructure buttressed by access to reference and market data.

- Continue working to securitize carbon credits and develop tradeable instruments that provide price signals to other entities.

- Provide carbon credits to help customers with their decarbonization goals in addition to hedging and risk management services.28

All stakeholders: Align around collective goals

In addition to using their unique capabilities and expertise to advance carbon markets, stakeholders should proceed with collective goals in mind. Efforts should be made to:

- Expand the scope of carbon credits to include other greenhouse gases, especially methane. Global livestock is responsible for 15% of greenhouse gas emissions, exceeding the entire transportation industry.29 A Swiss company, for example, has issued carbon credits that account for the reduction of methane emissions achieved from switching out cattle feed.30

- Encourage buying and selling of credits that include co-benefits such as supplemental investments in community development, job creation, and biodiversity. In addition, carbon market participants should look for ways to support emerging nature-based markets, since they will likely complement each other (eventually one project could bundle different types of credits with multiple benefits).

- Develop carbon markets in an equitable direction. All participants must act to ensure capital is directed to the indigenous and local communities whose support is needed to maintain the natural ecosystems that many credits are designed to protect. Steps to facilitate carbon equity include: recognizing land rights, including local groups in the design of projects, distributing the benefits of these projects, and adding equity outcomes to data disclosure.31

Despite the challenges of reform, the world’s climate targets hang in the balance. Greater cooperation and collaboration can bring harmony to carbon markets and prompt stakeholders to take greater strides toward shared goals. Governments, industries, financial institutions, and scientists have shown a willingness to work together to address this intractable crisis, and carbon markets have made substantial progress in the last few years alone. Now it’s up to stakeholders to put these good intentions into action with a new sense of purpose and urgency.

{kind=link}

{kind=link}

{kind=link}