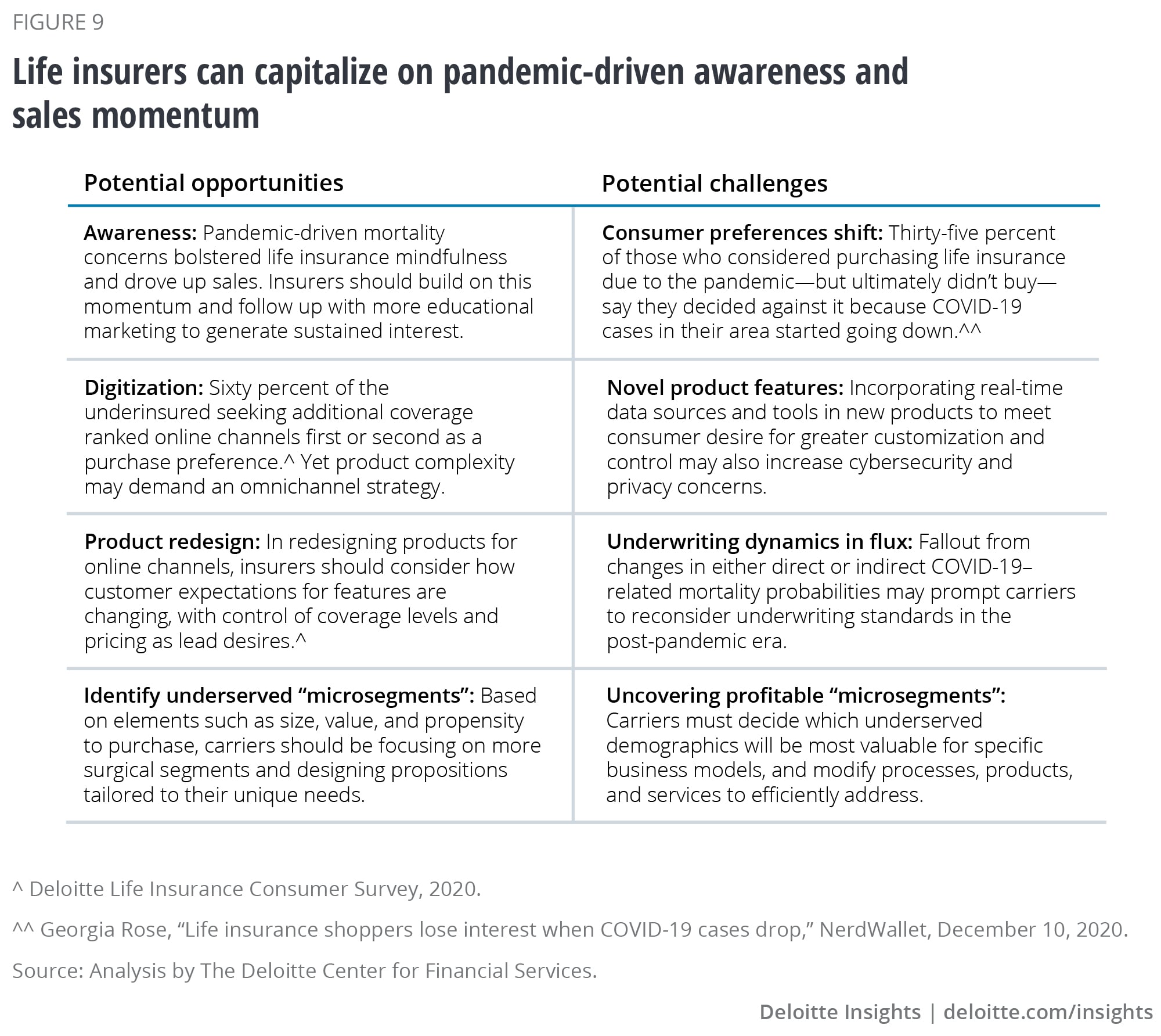

However, as concerns over COVID-19 start to lessen across the United States, life insurers should be building on pandemic-driven innovation to accelerate transformation to more user-friendly policies, platforms, and processes. An estimated life insurance gap totaling some US$12 trillion identified by LIMRA17 remains to be addressed, especially in terms of reaching underserved markets.

Group insurance: Offsets to top-line pressure position carriers to rebound

Since group insurance revenues are tied directly to employment levels, all of the layoffs, business shutdowns, and subsequent benefit plan cancellations prompted by the COVID-19 outbreak could have exerted enormous top-line pressure on insurers. There was also concern over a sharp increase in claims fueled by employees exposed to the virus. However, the overall impact was buffered to some extent by several factors.

First, as opposed to the 2008 financial crisis, there were far more closures last year among smaller businesses that are less likely to offer group benefits. Moreover, some larger companies were able to stave off revenue blows and maintain most of their workforce as government payroll protection programs helped keep millions of employees and their benefits in place.

The impact on claims varied based on a carrier’s product mix. Mortality claims from COVID-19-related deaths did escalate, negatively impacting term life carriers. However, many insured employees shelved various health screenings, dental visits, and other wellness activities during the period, driving claims down in related group lines. Even US maternity claims dropped as people put off having children, with an estimated 300,000 fewer babies expected in 2021.18 The anticipated rise in disability claims related to the virus were balanced out by the insureds who put off elective surgeries, as well as those who had been on disability but now could work from home as a response to the lockdowns.

Throughout all the uncertainty, carriers scrambled to pivot from traditional processes and services to accelerate digital capabilities while accommodating a virtual workforce and online customer interactions. For example, to enable online disability claims, insurers not only had to work out how to convince people to use telemedicine and share electronic health records, but also make them comfortable with digital claims and payments.

Meanwhile, many took the opportunity to upgrade their longer-term digital capabilities. One life insurer, for example, streamlined and automated group administration processes with cloud-based benefits software designed to digitize enrollment, provider directories, and plan configuration via a member portal. In addition, another life insurer offers customers capabilities to use a virtual assistant to check balances of their medical, dental, and vision care accounts.

As all this was unfolding, bidding activity—which businesses use to switch from one group insurer to another—fell as US companies scrambled to address more pressing talent issues. However, while this drove group sales down across the sector, retention was up, with the net impact helping alleviate top-line deterioration.

What’s next for the rest of 2021?

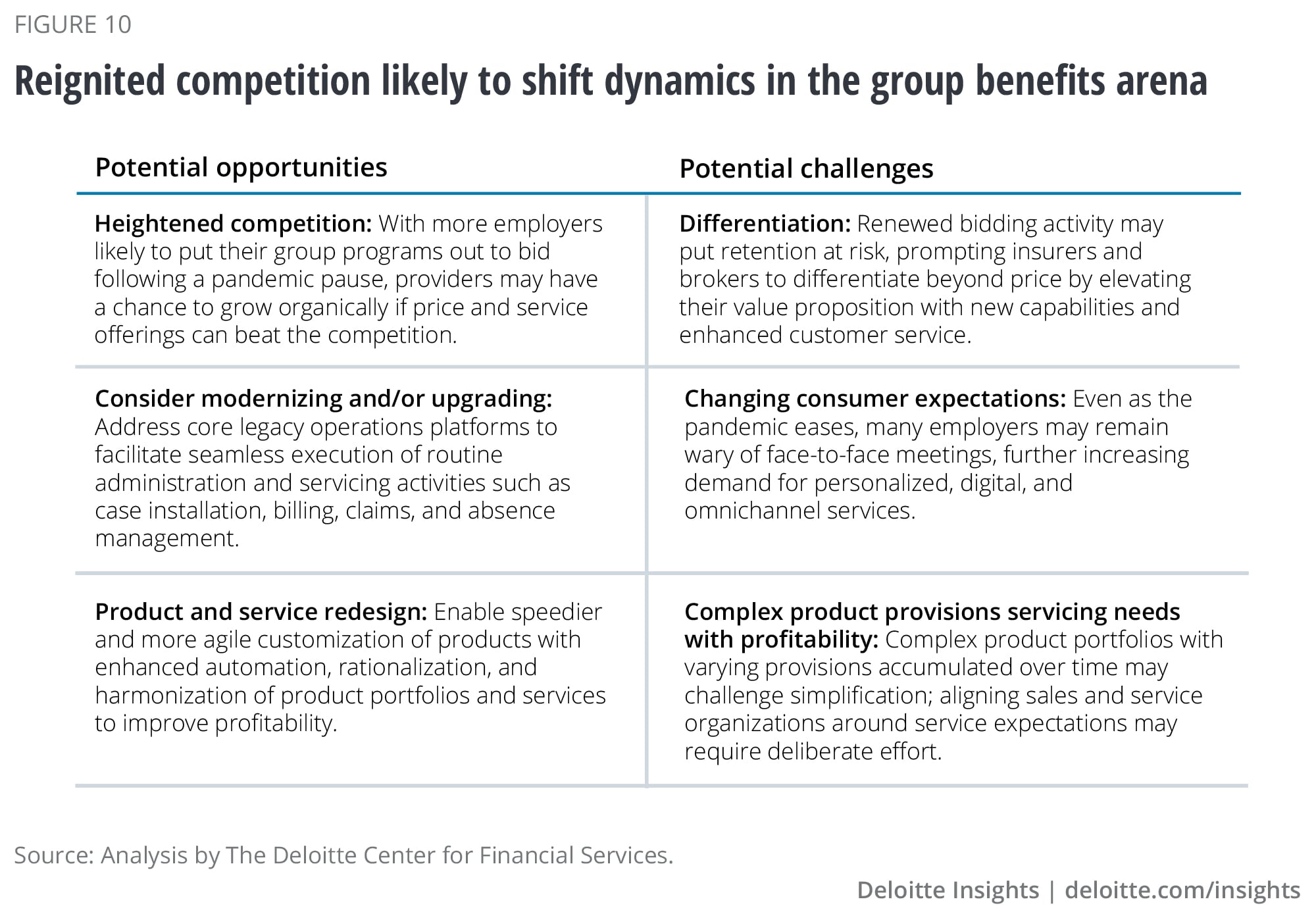

As group carriers pivot from recovery to thrive over the rest of this year, there are a host of opportunities and challenges ahead (figure 10). With millions of laid off employees having returned to the workforce, and many more likely to follow this summer and fall, a rising tide should help lift all boats in the group benefits market.

However, heightened competition is expected as well, as many employers resume plans to put their programs out to bid. This should prompt providers to seek ways to retain accounts and generate new business through product offerings and service differentiation rather than just competing on price.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}