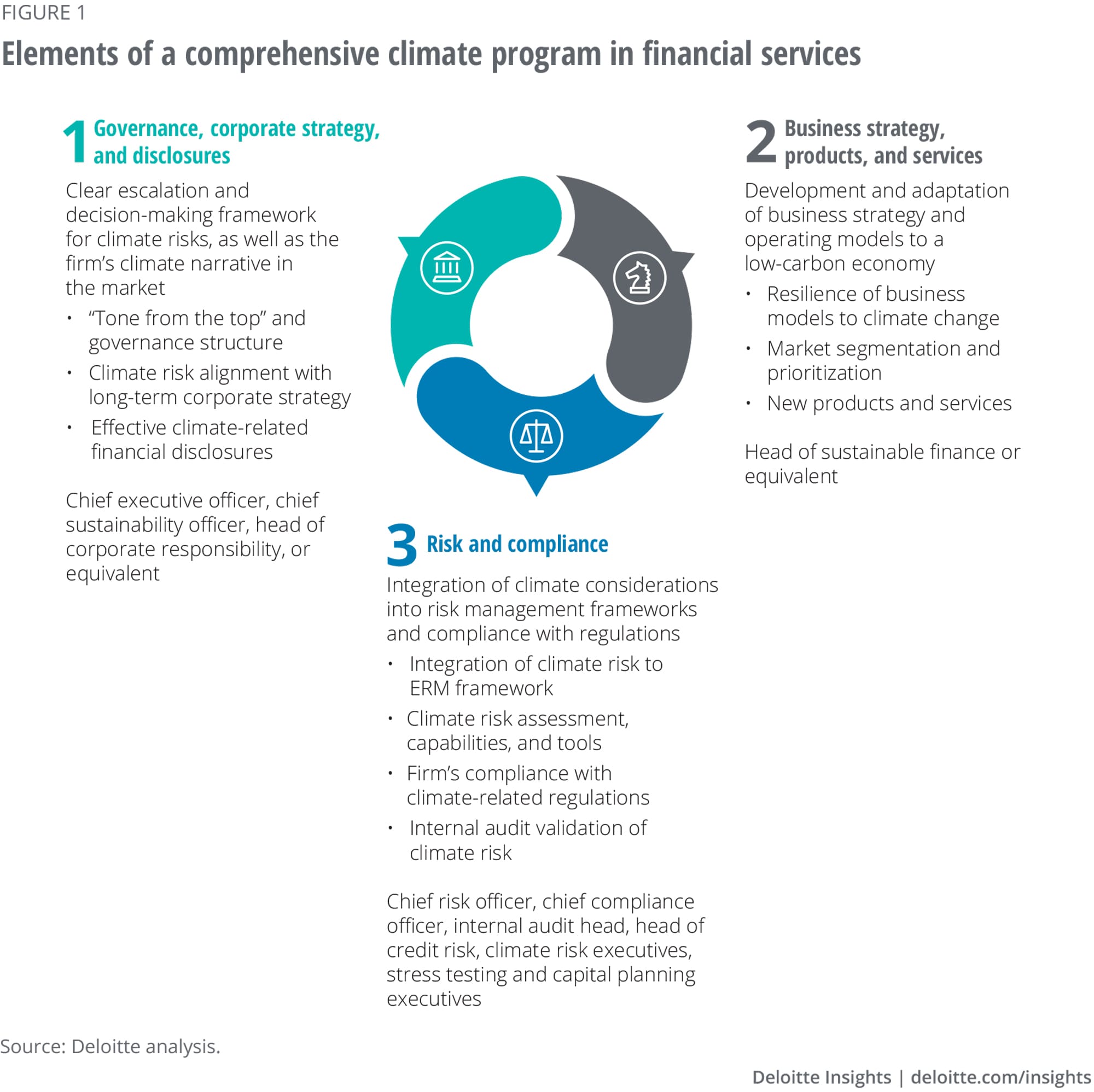

Governance and corporate strategy

A climate-centered firm of the future should have a clear philosophy, position, and intentions related to climate risks. Financial firms will need to realign their business models to integrate climate, as well as other environmental, social, and governance (ESG) considerations, into all business decisions. Climate risks and opportunities will no longer be regarded as separate from the core business; they will become intrinsic to a firm’s success.

The board of directors will play a vital role in setting the right tone at the top. It will need to develop a clearly established structure for climate oversight. Board members will need to become more proficient in climate and other ESG risk matters, and they should be regularly briefed when new issues emerge. This can enable the board to ask relevant and difficult questions that probe management´s direction and strategy.

Specific climate-focused initiatives will be driven by sustainability and climate risk professionals. These will include climate scientists and financial modelers who understand the intricacies and overlap between climate science, policies, and financial risks. Climate-centered organizations may still have a dedicated sustainability team or chief sustainability officer, but they will rely more on issue and topic specialists who will be integrated throughout the company. Meanwhile, the CEO will have overall management responsibility. Climate-related goals will likely cascade down through the organization by aligning them with employee incentive compensation.

Financial firms can use an integrated management reporting system that quantifies the financial implications of climate-related decisions to inform decision-making. High-quality and reliable climate and other ESG disclosures and external communications should provide insights to market participants, consumers, and policymakers into how effectively the company manages ESG impacts and dependencies.

Already, leading financial firms are forming specialized teams to support enhanced disclosure and transparency of climate-related business risks and opportunities,2 and how they are being managed. Firms should widely disseminate this information by using a “stakeholder first” lens to help prioritize and get ahead of multiple evolving expectations. Over time, they should establish clear policies and processes that reinforce their positions on climate and ESG goals.

Finally, a key to each firm’s success in this arena will be their ability to effect broader change. To help accomplish this goal, firms could create or join multisector and multidisciplinary industry partnerships and regulatory collaborations that focus on accelerating ESG and climate risk transformation efforts. Modeled on the work of the Commodity Futures Trading Commission’s Market Risk Advisory Committee,3 these opportunities will bring together stakeholders from all industry sectors, including competitors, to help solve the most challenging issues facing the industry, and can help advance new climate-focused practices. These collaborations should strengthen relationships with regulators and supervisors by helping reduce systemic risks.

Targeted product and service innovation

While investors and regulators expect businesses to have a plan for managing climate risks, customers increasingly want product and service offerings that align with their views and beliefs. Some leading firms have already started creating dedicated businesses and offerings built around sustainability, diversity, and other ESG-related mandates, with climate being one of the most prominent themes.

These efforts should crystalize in the future; firms should offer a full suite of climate-related products and services that tie back to their specific business models. Here’s how that may likely develop in each sector:

Banking and capital markets

Having experience funding low-carbon companies and projects, climate-centered banks and brokerage firms should be able to differentiate among degrees of risk and profitability across their client portfolios. Credit decisions may be based on specific and idiosyncratic variables and expectations, with advanced pricing models linked to transparent and established industry taxonomies to categorize activities across the “brown-to-green” lending spectrum.4 Firms should integrate climate assessments into new product approval processes. They should also continuously assess clients’ existing and potential stranded assets, those prone to write-downs related to climate issues, and use this information in pricing.

Carbon pricing in the United States may become a reality in a few years. With or without a legislative mandate, firms should move forward; they could use derivatives to push more capital toward sustainable investments or allow market participants to hedge risk based on ESG factors.

In fact, an entire market of ESG exchange-traded and OTC derivatives is already developing.5 Many of these products, such as interest-rate or credit-default swaps, have a climate-specific component. While catastrophe and weather derivatives have been used for years to guard against natural disaster losses or provide allowances when temperatures are above or below predetermined thresholds, they will likely become more prevalent and part of the sector’s core offerings and portfolios.

We anticipate retail banks will also tap into consumers’ increased awareness and interest in climate-conscious products. Picture mortgages that incentivize eco-friendly borrowing (for example, to add solar panels to a home), or credit cards that allow borrowers to track the carbon impact of each item or service they purchase.

Insurance

Climate and ESG issues have already become a central focus for the insurance industry. Recent years have witnessed a surge in the number of catastrophic events related to climate change, such as wildfires, heat waves, reduced crop yields, and coastal and inland flooding.

These events will require insurers to develop more dynamic modeling approaches that rely on past loss experience and uncover nonlinear effects, including correlations between climate hazards, social impacts, and economic activity. Climate-centered insurers will likely offer products that cover climate risk more directly, expanding into other ESG effects. To some extent, this is already happening. For instance, you can purchase insurance that protects food supplies against the impact of climate change. In the future, climate-centered insurers will detect, price, and cover a broader range of similar relationships as part of a wider socioeconomic solution.

In addition, insurers will likely expand their offerings from helping customers simply transfer risk to mitigating, preventing, or recovering more quickly from climate-related catastrophes. For example, insurers could offer lower premiums to encourage the use of more resilient construction methods. These firms could collaborate with the public sector (such as municipalities, regulators, and policymakers) to improve construction standards and develop policies that limit growth in areas prone to physical hazards. They could also help governments decide where construction should—and shouldn’t—be developed.

Climate-centered insurers should continue to balance asset and liability management activities, matching risks with corresponding climate- and ESG-driven assets (for example, divesting from thermal coal and reinvesting in green energy alternatives). Insurers will likely focus on optimizing risk pools that minimize the asset and liability mismatch related to climate or other ESG risks, recognizing that climate-related catastrophes have immediate effects on other ESG risks.

Wealth and investment management

The wealth and investment management industry is already developing and distributing solutions that cater to investors seeking ESG and other nonfinancial objectives. Leading investment managers are currently using these two strategies to incorporate climate risk and ESG metrics into their portfolio construction process:

• Integration strategies: Seek to maximize financial return by incorporating ESG principles into the investment process or through engagement activities.6

• Thematic strategies: Aim to make a measurable impact on specific issues through their investments, such as investing in renewables.7

In the future, more wealth and investment managers will likely differentiate their products to cater to the demands of institutional and retail investors. As they continue to broaden their product array, they may develop index funds and customized strategies that are aligned with ESG-related goals, such as the United Nations’ 17 Sustainable Development Goals (SDGs), to track the returns of positive-impact companies).8 For each of these products, investment managers will need to share how they compare to the market in terms of ESG climate metrics and how this impacts performance, or how they perform against broadly utilized ESG ratings (for example, MSCI ESG Ratings). These efforts will likely accelerate the classification of green and sustainable products and should include relevant disclosures.

As part of this evolution, climate-centered wealth and investment managers should actively monitor and engage with target companies and advocate active, visible, and credible climate risk management strategies and capabilities. They should also invest in capabilities to identify true climate and ESG impacts. This is important because, as the risk of greenwashing increases and ESG disclosure becomes more common, it may become more challenging to separate ESG leaders from laggards. The Organisation for Economic Co-operation and Development’s Business and finance outlook 2020found that, for Standard & Poor’s 500 companies, ESG scores from major rating firms are highly variable and show low correlation with actual results. This suggests that raters have fundamentally divergent views about ESG performance.9

Advanced wealth and investment firms should have the content and domain expertise to overcome these gaps, particularly where ESG data is unreliable, not available, or where accepted standards do not exist. They should go beyond incorporating self-reported data or climate/ESG metrics from third-party providers and perform deep sector or even firm-level analysis to create bespoke data sets of firms they invest in. At one leading financial firm, their in-house sector analysts’ expertise in firms’ business models, product strategies, operational nuances, and regional characteristics has become a critical component in evaluating ESG and climate (and financial) performance.10

As other investment firms seek to replicate this kind of success, they will need to be transparent about their methodologies, allowing investors to evaluate the quality and granularity of their data and how it is used to build portfolios. Analytical rigor will likely be a major differentiator that sets leading financial firms apart from their competitors.

Large global firms may also be able to influence the political debate about climate change. Sovereign bond ETFs have been designed to weigh countries on their level of risk from climate change.11 This development may prompt countries to change their approach and policies as the link between climate change and creditworthiness may grow stronger.

Enhanced risk management capabilities

In the future, climate-centered organizations will have the capacity to manage climate and other ESG risks. Financial regulators recognize that a changing climate poses systemic risks to the US financial system. Regulation will continue to evolve and grow, and climate-centered financial services firms should actively contribute to the dialogue.

Firms that develop advance climate risk modeling capabilities may be better prepared, resilient, and ready to manage climate risk as part of their credit evaluations. They will also create products that account for similar hazards. Creating this type of enhanced risk management may allow climate derivatives to hedge better against climate-related risks, enabling firms to efficiently invest in green bonds and other instruments supporting a low-carbon future. In reality, nothing should stop individual firms from creating such structured products, customized to specific client needs, as long as they are well informed about the vulnerabilities.

Climate risk should therefore become a regular feature of risk management discussions. Today, financial firms have defined thresholds for market risks they are willing to bear. These include factors such as issuer default and correlations; liquidity risks, such as intraday settlements and maturity gap mismatches; and credit risks associated with counterparties and underlying issuers. Tomorrow, climate risk will be just as narrowly defined—people will no longer need to explain what they mean by the term. Furthermore, climate risk should be embedded in risk taxonomies that capture climate-related physical, transition, and liability risks, and there should be a comprehensive ERM framework that fully integrates these risks. Frameworks will, of course, take different shapes across sectors. But establishing data quality standards, common models, and operational processes can help set expectations across the industry and harmonize risk taxonomies to incorporate climate risk.

To help develop and infuse these risk capabilities, organizations will need to put dedicated teams in place that explore the overlap of climate change, economics, and financial modeling. The analysis these teams provide may blur the lines between climate change and economic risks, uncovering the intricacies of macroeconomic and microeconomic transmission channels.12 They will work at the client/counterparty level and at the portfolio or fund level, identifying correlations between climate risk and other ESG issues. Climate-centered firms should also consider employing in-house teams of climate scientists to help develop possible scenarios. To complement their analyses, lead economists in financial firms will likely rely on these climate teams as a main source of information.

Digital solutions can help support these efforts. Firms can use several emerging tools and techniques, such as artificial intelligence–driven risk simulations. Firm leaders should incorporate climate risk and ESG into capital allocation decisions. Geolocation and climate exposure analyses and dashboards should aggregate across climate scenarios. Some of this aggregation will likely be standardized across the industry, allowing for interactions and dialogue with regulators.

A fast-moving opportunity

Without a doubt, climate risk is a growing challenge to businesses and society at-large. At the same time, the world is moving toward a cleaner, more sustainable future, and industries of all stripes are transforming their businesses to do their part. Given its vital role in capital formation, we believe the financial services industry has a predominant role in addressing these interrelated challenges. Shareholders, regulators, politicians, employees, and other key stakeholders all recognize this—and they’re beginning to up the pressure on financial firms to mobilize.

But the onus to act is greater than that. There’s an enormous opportunity on the horizon for those who can effectively mitigate climate risk. Differentiation is as difficult as it’s ever been in the financial services industry. Being climate-centered—and building businesses and practices around the end state discussed above—can be a powerful lever to help firms rise above collective commoditization. It’s a simple proposition: Give the world what it wants and needs, and you’re likely to garner success. And the world won’t wait. Already, leading firms are pushing ahead with climate-driven initiatives and putting teams in place. Transformative opportunities are still there for the taking, but they won’t be for long.

{kind=link}