First impressions count has been saved

First impressions count Improving the account opening process for Millennials and digital banking customers

06 September 2017

Little things can add up. A new study shows that Millennials and digital customers see room for improvement in retail banks’ account opening processes. Where were the gaps? And what small steps could banks take to create a better experience?

Serving Millennials and the digital customers of tomorrow

Millions of consumers open new accounts every day with online stores, cable companies, mobile ridesharing apps, and of course, with banks. Now imagine one such consumer—a Millennial named Max—opening a new account at a popular online shopping site. On the same day, Mia—another Millennial—opens a new account at a bank. Who do you think had a better experience—Max or Mia?

If you thought Max, you are likely wrong.

Conventional wisdom suggests that the account opening process at many banks seems to have become burdensome, due to heightened regulatory demands and compliance and control pressures. Banks today collect more customer information than ever before, follow a greater number of steps while onboarding, and ensure strict controls throughout the customer service life cycle.1 Meanwhile, the ease of opening a new account on digital platforms—in online commerce, ridesharing services, and even person-to-person (P2P) payments and online lending, is resetting customer expectations, particularly among Millennials.2

Who exactly wants a better account opening experience?

To better understand how these dynamics impact the account opening experience of retail bank customers, Deloitte surveyed more than 3,000 consumers who opened a bank account recently for three product categories (see appendix for survey methodology).

What did we find? The survey turned up several interesting results. First, consumers view the account opening experience at banks more favorably than registration experiences in many other industries. Second, a vast majority of customers, including Millennials, are aware of regulations related to the account opening process, and also believe them to be beneficial.

However, and perhaps most importantly, though customers of all ages are satisfied with the account opening process, a meaningful share want the account opening experience to be improved (figure 1). Specifically, Millennials, mobile-banking users, and recently acquired existing customers of the bank were most likely to demand improvement.

Why do banks need to do a better job with account opening? A superior account opening experience can be vital for banks to remain competitive and to ensure loyalty—customers who think the account opening process can be made better at their banks are, in hindsight, much more likely to think about taking their business to another bank. The survey also found that consumers who wanted improvement in their account opening experience were less likely to purchase additional products or services at the bank, and were less enthusiastic about recommending the institution to their family and friends. And 75 percent of improvement seekers were below age 50—a commercially critical demographic, as they are the banks’ future customer base.

But what does “a better account opening experience” mean? The most fundamental attribute of an exceptional account opening experience is speed—the faster an account is opened, the less likely the customer is to want improvement. Consumers demand that banks use their existing information to not only speed the process up, but also to cross-sell relevant products to them. Banks should also give consumers clear and concise instructions during the account opening process, and follow up with them to inquire whether they have questions and are satisfied with their accounts.

So, how can banks improve? Banks can achieve specific capabilities that meet customer demands by investing in not only the right capabilities to improve the direct digital interface with customers, but also in technology available to frontline staff to help them be focused and empathetic toward customers. By leveraging some critical new insight, banks should also harness customers’ favorable view of regulations in their messaging strategies to emphasize security, safety, and rigor.

Millennials and mobile-banking consumers are the most demanding

Our survey shows that typical consumers who want improvement are more likely to be Millennials and that they especially have higher expectations when interfacing with banks through digital channels.

While opening accounts on mobile applications is still nascent—only about 5 percent of respondents in the survey opened accounts through a mobile application—consumers who opened accounts on a mobile phone, compared to bank branches and online banking (the two main channels used to open accounts), were much more likely to say that the retail bank account opening process needed improvement (figure 2). And, again, more than half (54 percent) of consumers who opened accounts on a mobile device were Millennials.

While many banks themselves recognize their deficiency in offering robust mobile account opening services,3 clearly, the mobile channel is where the action seems to be headed in the future. Banks should redouble their efforts in this area as a necessary competitive lever, as all types of customers increasingly gravitate to this channel.4

Don’t test the patience of these young, demanding customers

We also found that existing customers with relatively shorter relationships (five years or less since the first account was opened), a cohort dominated by younger respondents, want the account opening process to improve (figure 3)—this holds across all the main product categories (deposit accounts, loans, and wealth/retirement solutions). In contrast, consumers who were opening accounts at a completely new institution, or those who had longer relationships (more than five years) were much less likely to say that their account opening experience could have been better.

These findings suggest that although demanding consumers are capable of being patient during a first account onboarding with a bank, they expect banks to then use the information they already have to streamline follow-on account openings. This expectation appears quite reasonable, and is probably easy enough for banks to establish as a core operating principle.

Consumers view regulations as beneficial, potentially helping banks

A fundamental, yet potentially surprising, finding from our survey is that the lion’s share of customers (81 percent of our sample) are aware that regulations require banks to collect a wide range of information and documentation from customers, and that a majority of customers, including most Millennials, feel that these regulations are beneficial (figure 4).

Even more revealing, many consumers, once again including Millennials, rate the experience of opening bank accounts as easier than signing up for a range of other services in other industries—from the traditional, such as signing up for a new cable service on the phone, to those powered by digital interfaces, such as signing up for app-based car ridesharing services (see figure 5).

In addition to what banks are doing correctly in the account opening experience, two factors might be influencing consumers’ opinions. First, they might be viewing a financial relationship as different from other types of service interactions, inducing an additional level of seriousness and patience in the interaction. And second, the fact that consumers know about regulatory requirements, as noted above, might be tamping down expectations around speed and complexity.

What does improvement mean?

To find out what customers want—especially Millennials—we distilled some salient points in the experiences of demanding customers who thought their account opening experience could be improved.

Understand—and act upon—the need for speed

The time it took to open the account was the single stand-out predictive observation for those who demanded improvement in their account opening experience. For example, a deposit account opened in 45–60 minutes was over five times more likely to draw a demand for improvement compared to accounts opened in less than 15 minutes (figure 6). This positive association between speed of account opening and the demand for improvement also held for consumer loan and wealth management accounts.

Back up your claims with results, or else . . .

The customer who expects more will typically not hesitate to look elsewhere. Customers who sought improvement were much more likely to have opened the account after some external stimuli, such as seeing an ad about the account, a recommendation from a financial adviser, or simply because they liked the bank’s mobile app or website (figure 7). These findings may indicate that consumers often develop high expectations based on these influences, and are then potentially let down by the experience of actually opening the account. They also suggest a potential disconnect between the quality and promise of marketing programs and/or digital advertising, and the actual quality of the account opening experience.

Consumers seeking improvement were also several times as likely to say that in hindsight, they may have gone to another institution to open the account (figure 8). Millennials, again, were the largest component of this group.

Another obvious, but important, message for banks—customers who expect more are likely to think that another bank or an online/digital-only bank would make the account opening process easier or faster. And from a commercial perspective, consumers who sought improvement said they were less likely to purchase additional products or services at the bank, were less enthusiastic about recommending the institution to others, and even less likely to trust their bank.

Provide clear instructions and communication before and during account opening

Our study also revealed that consumers who expected a better account opening experience often felt the bank’s information and documentation requirements were not clear. Importantly, the improvement seekers in our survey also rated themselves as having a high knowledge of banking. This finding suggests that the more that customers believe they know about banking, the more likely they are to expect a better experience.

Be mindful about cross-selling

One of the most interesting findings from our survey is that consumers who were the target of a cross-sell attempt during the account opening process were more likely to think that the experience could be improved (figure 9). Notably, consumers who actually considered a purchase based on a cross-sell attempt—the ones who showed a greater measure of attentiveness to the sales pitch—were also more likely to demand improvement. Together, these data tell us that cross-sell attempts at banks, at least those made during the account opening process, currently appear to be hit-or-miss, and should become more insight-driven.

Follow up!

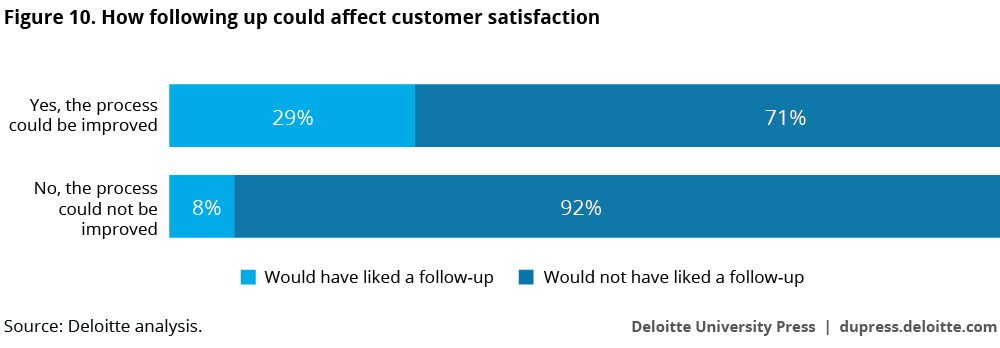

We also observed that the lack of a follow-up by the bank created much greater dissatisfaction among the improvement-seeking group (figure 10). Even more alarming for banks, these demanding customers also had to follow up with the institution on their own, at a rate that was many times higher than other consumers. The reasons consumers gave for following up were wide-ranging, but included information about the account that should have been delivered during the account opening process. These findings show a clear, and frankly elementary, customer service failure by banks.

How can banks improve the account opening process?

The range of data we have examined on gaps in the account opening process highlight a critical fact—many banks seem to still fumble the basics. In that light, the advice below, while not wholly novel, is backed by hard data and primary research rigor to keep the distraction of conventional wisdom(s) at bay:

- Prepare for a mobile future. By any measure, mobile banking is quickly growing to become a fundamental pillar of retail bank offerings, not only to Millennials, but also to older customers.5 Giving consumers the ability to seamlessly open accounts on a mobile device is expected to be one of the cornerstones of outstanding customer service.

- Enable high-quality frontline staff interactions. Our results seem to also highlight the need for attentive and empathetic human interaction by frontline staff during the account opening process. Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations have increased requirements—both for information and documentation. Better systems and tools that enable service representatives to focus on the customer instead of being mired in the minutiae of meeting regulatory and other process requirements might be the most fundamental improvement that banks can make while opening accounts in a branch or on the phone.

- Use data and analytics for a faster and tailored experience. Delivering a faster account opening experience—especially to young existing customers, who tend to be the most demanding—likely relies on fully exploiting information that the bank already possesses. Linking customer data across products and businesses, while simple in concept, may still be difficult for banks to achieve in practice. This deficiency also appears to extend to analytics (“next-best offer” solutions and the like), as evidenced by consumer responses to cross-selling. More sophisticated predictive analytics can enable banks to tailor the customer experience with cross-sell attempts that accurately reflect customer needs.

- Emphasize regulatory rigor. Perhaps the starkest finding of our study is that no matter what banks think about KYC regulations, the vast majority of retail banking customers think that these regulations are beneficial. In this regard, banks might even want to emphasize it in their overall messaging strategy as a benefit that customers don’t get from less regulated non-bank competitors. At a broader level, banks should communicate that customer security, and not just meeting regulatory demands, is the motive for greater inquisitiveness during the account opening process.

- Finally, follow up, and eliminate the need for customers to do it themselves. Following up with customers to resolve any queries and gauge satisfaction with the account opening process is a relatively simple service element that banks should meet. These follow-ups should also give consumers easy access to information on account use or activation, or inform customers on specific features, offers, or promotions associated with the account.

Appendix: Study methodology

For this study, Deloitte surveyed 3,000 retail banking consumers who had opened either a deposit (57 percent of respondents), wealth management (17 percent), or consumer loan (26 percent) account from January 2016 to May 2017. The distribution of respondents, shown in figures 11, 12, and 13, skewed toward a younger cohort—this was to be expected given that individuals opening new accounts would tend to have emerging financial needs.

Forty percent of surveyed consumers opened their accounts at an institution with which they had no prior relationship. This provided us adequate basis to differentiate between their account opening experiences and those of consumers who added an account to an existing relationship.

The survey sample distribution may not be representative of the population of consumers who opened bank accounts in 2016 and 2017—none that we know of exists—making it difficult to estimate sampling error or to weight the sample. Nonetheless, we believe our survey design gives us sufficient basis to make cohort-level and product-level conclusions.

Finally, the survey was tailored to factor in the product for which the account was opened, and importantly, the channel through which the account was opened. The natural fallout of channels used to open accounts shows the enduring popularity of branches, but with online account opening also featuring heavily.