However, these new tools will do little good for insurers or their customers unless claims professionals are trained to derive the most value from them and are prepared to handle more challenging tasks after automation relieves staff of routine data gathering and administrative work.

Many might be repurposed to higher level data analysis—for example, in managing portfolios of risk rather than individual claims. Others could focus more on fraud detection, coverage analysis, and dispute resolution for outlier claims. And rather than devoting all their attention to settling losses after an event, a claims contingent could work more closely with underwriting colleagues who are integrating many of the same emerging technologies and data sources, offering valuable feedback on how policy language, terms, conditions, and pricing are playing out in the market.

Some might even leverage their forensic expertise more proactively to support loss control services. One auto insurer CCO interviewed has aligned the company’s risk engineering and claims departments to create a continuum to keep losses from happening in the first place.

The crucial role of human interaction in the digital claims journey

As more digital tools come online, insurers will likely be able to apply accelerated claims handling and automated decision-making to an increasing proportion of their overall cases, thereby boosting claims professionals’ productivity while freeing up capacity. However, a natural follow-up question that’s likely front of mind for many in claims is whether automation will make them redundant? And the answer is that it depends on whether they can adapt, so they keep adding value to the customer’s claims experience.

With new data and technology at claims professionals’ disposal, their roles and responsibilities will likely change. Traditional activities such as data collection and verification, loss estimation, and claims settlement could take somewhat of a back seat as automation solutions mature.

But this does not mean claims professionals will play second fiddle to emerging technology. In fact, claims professionals armed with these tools would be able to accelerate the pace of claim settlement, which should increase overall customer satisfaction, while supporting the continued evolution of automation solutions. Claims leaders interviewed also repeatedly highlighted the importance of personal engagement when clients need it, which should be a differentiator in an increasingly automated world.

Claims can still make or break insurer reputations

“Here is where I go old school,” declared one personal lines CCO interviewed. “If there’s anything wrong with all this emphasis on new technology, it’s the belief that maintaining one-on-one face time, virtually or otherwise, isn’t as important as increasing efficiency.” While automation can cut time and expenses, this CCO added, “that doesn’t necessarily mean you need to do away with customer interaction, which is an essential element to the overall experience, especially if a problem arises.”

He cited the example of his company’s dedicated catastrophe team. “The last thing you should do is cut those people, as you still need boots on the ground to provide comfort to traumatized customers. You can’t do it all with drones and bots.”

In addition, while an automated system might simply reject a claim because that particular loss isn’t covered under the policy’s terms, a human claims professional might seize an opportunity to provide value-added service. “A denial doesn’t have to be a door slammed in a claimant’s face,” said a homeowners insurance CCO. “We need to create a good experience for those not getting paid, not just for those who do.”

For example, even if an algorithm determines correctly that a policy provides no coverage for a particular loss, claimants may still need help getting a fair damage estimate and reliable contractor. “Yes, that’s a cost,” said the homeowners CCO, “but it can also create customer stickiness and a lot of good will.” The result is more likely to be a positive experience the claimant shares as opposed to complaining about being summarily dismissed by the insurer’s bot. This can make a significant difference, as one technology entrepreneur calculated it takes roughly 40 positive customer experiences to undo the damage of a single negative review.5

Hence insurers should strive to create a flexible digital experience that capitalizes on the many benefits of automation and more advanced technologies while allowing live adjusters and claims managers to seamlessly weave their way in and out as their presence is required.

In the end, claims professionals are very likely to remain the heart of their function at most carriers, only in different ways than before. It’s important to upgrade their skill sets and broaden their horizons to exponential levels, so they can complement automated systems, take advantage of more advanced technologies, and continue to add value for their employers and customers.

Analyzing the impact of emerging technologies on claims skill set needs

So, where might all these new technology tools, alternative data sources, and increased need for customer management leave existing claims professionals in their day-to-day work?

Most of the CCOs interviewed stressed that such enhancements are unlikely to do insurers much good if their claims units don’t integrate them productively or understand when and how to use them effectively. This puts the onus on claims professionals to expand their technical capabilities and adapt their roles to handle a higher level of work and wider array of responsibilities.

“It’s really not about replacing skills; it’s about adding some and amplifying others,” as one personal lines CCO aptly summarized it.

Breaking down the exponential claims skill set

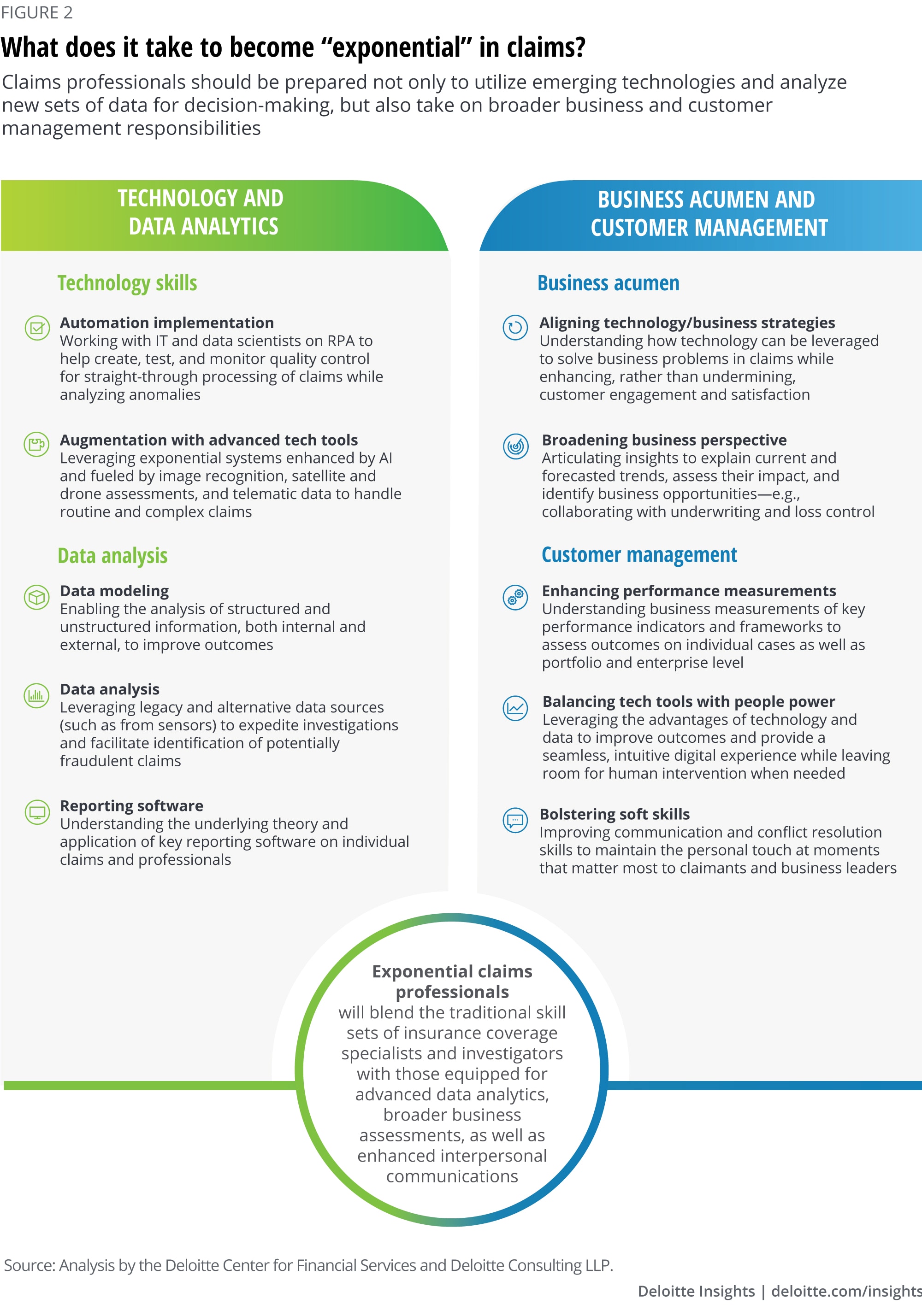

Claims departments should be developing augmented professionals blending elements of four distinct skill sets to reach the exponential levels needed to provide a hybrid customer experience that can be both digital and in-person (figure 2).

Such individuals should possess a mix of business and technology skills, speaking the language of both sides, and able to bridge the divide often separating the two in order to make cognitive systems effective and seamless in a business context.

{kind=link}

{kind=link}

{kind=link}

{kind=link}