Unlocking a potential US$3.8 trillion opportunity for private equity firms

Considerations for how private equity firms facing liquidity challenges can thrive in the next five years

Bryan Hart

Frank Fumai

Sean Collins

Reynaldo Sylla

Some private equity (PE) firms are facing liquidity challenges, evolving investor expectations, and a volatile global macroeconomic environment. These factors can influence the strategic choices they make about fundraising activities, portfolio company (port co) liquidity events, capital distributions, and deal structures to help them thrive and adapt to satisfy the liquidity and performance needs of their limited partners (LPs). If successful, they can potentially unlock 20% annual growth in private equity dry powder through 2028, reaching US$3.8 trillion globally, an all-time high.1 To get there, PE firms may need to utilize different deal structures and exit types to align with investors’ expected returns and distribution time horizons. As current processes evolve to facilitate shorter holding periods and increase investors’ ability to enter and exit a fund more frequently, the suitability of private equity investments may continue to expand to include an even broader investor base, such as additional retail investors.

While interest rates peaked and then started to decline in many developed economies in 2024, potentially causing some investors to rethink cash allocations, fundraising continued to be a challenge. Total global PE capital raised fell to US$573 billion in 2023 after reaching its all-time high of US$619 billion in 2022.2 Recently, small-sized PE funds (less than US$1 billion in size) have been challenged by their larger peers in attracting new capital. The largest PE funds (more than US$5 billion in size) have taken an increasingly greater percentage of total private equity industry fundraising, rising from 33% of all capital raised in 2020 to 53% in the first half of 2024.3 Regardless of the fund size being launched, satisfying the liquidity needs of LPs through distributions can be an important differentiator for private equity firms in this competition. Historically, exit strategies from port cos provide the liquidity that PE funds need to make distributions to LPs. After the US exit value reached a high of US$828 billion in 2021, the total value of all exits in both 2022 and 2023 reached only about 70% of that total.4 Global exit activity experienced a similar drop, with total exit value for the same two years reaching just 90% of its level in 2021.5 As exit activity dissipated, distributions to limited partners did as well, which contributed to a challenging fundraising environment in 2022 and 2023.6

Traditional exit strategies can fall into one of three categories: selling the port co to a corporate buyer, to another sponsor of a private equity fund, or through an initial public offering (IPO). Between 2008 and 2021, the IPO exit method accounted for an average of 21% of the annual exit value of US private equity firms’ portfolio companies.7 However, the share of IPO exit value fell to 2% and 3% in 2022 and 2023, respectively, during a downturn in the public markets.8 Exits through corporate and sponsor acquisitions were insufficient to close the gap. This might suggest that when public markets are supportive of healthy valuations, they can serve as a viable exit option for private equity firms to create a liquidity event for their investors, which in turn can be the catalyst for successful fundraising efforts. Through the three quarters of 2024, the S&P 500’s forward price-to-earnings ratio steadily climbed to exceed one standard deviation above its 30-year average.9 These higher valuations may be supportive of IPOs taking a greater share of PE exits over the near term.

How might new private fund exit strategies drive AUM growth over the next five years?

Ultimately, realizing higher returns than other asset classes for investors will likely continue to drive inflows for private equity. However, the pace at which these returns are realized may determine how fast private equity assets under management (AUM) can grow over the coming years. The Deloitte Center for Financial Services’ Global Private Equity AUM model examines how historical changes in exits, deal activity, fundraising, and dry powder may impact future AUM growth (methodology). The scenarios are driven by whether the percentage of private equity exits conducted via IPOs continue at the historical lows seen for public IPOs in 2022 and 2023, or if the percentage of PE-backed company IPO exits rises toward 2020 and 2021 levels. The forecasted percentage of IPO exits used in the model considers both public and private IPOs of PE-backed companies. In a private IPO, a general partner (GP) sells a minority ownership stake in a specific portfolio company to one or more private investors with the expectation that the GP and management would maintain their majority interest for the foreseeable future.10

As we look at the next five years, there are two main scenarios that emerge.

- Slow AUM growth: Public IPO exits remain near historical lows (3% to 5.5% of all PE exits), and private IPOs fail to have a meaningful effect as an alternative.11

- Fast AUM growth: Historically, high valuations in the public markets persist over the next several years, and private IPO structures become commonplace, leading to public and private IPOs accounting for 40% of all PE exits in 2028.12

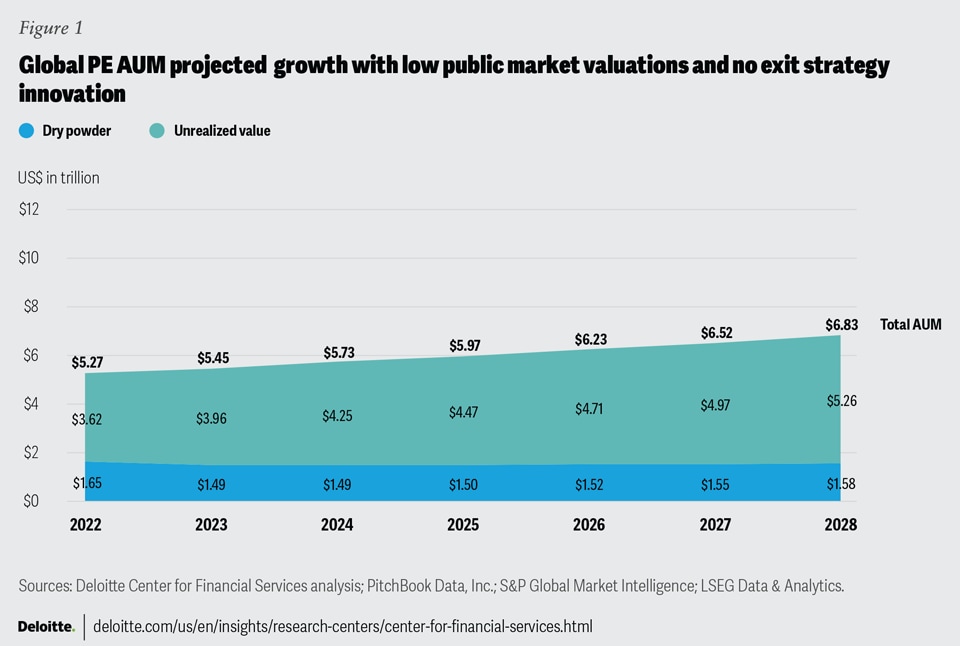

In the slow AUM growth scenario, the liquidity squeeze experienced from 2022 to 2023 is expected to persist through 2028. Per the model, valuations in public markets would fail to remain at historical norms, limiting opportunities to realize gains through IPOs for portfolio companies. Sponsor-to-sponsor and strategic corporate deals could remain as options, but the model indicates that exit value globally could fall to about US$400 billion by 2028, as many fund managers remain on the sidelines. Figure 1 shows the forecasted growth in PE AUM between 2022 and 2028 should the opportunity for exits beyond such deals fail to take hold, and without robust innovation related to port co liquidity events or LP distribution channels. Without sufficient cash flows generated from the realization of gains, distributions to investors could fall to levels not seen prior to 2011. The difficult fundraising environment is expected to continue and grow at a rate of 1.5% per year through 2028. Our model analysis suggests that these cash flow conditions will likely translate to global private equity dry powder increasing to US$1.6 trillion in 2028. While this slow growth scenario may be unlikely, it demonstrates the importance of liquidity creation events for LPs. The model shows that a mix of traditional and emerging exit types within all three categories can help generate cash flows to maintain steady growth in dry powder.

Private equity cashflows may see an uptick, as the IPO markets in the United States and Europe have recently shown signs of a possible rebound after a tough couple of years.13 Some private equity firms are also beginning to take their portfolio companies off the sidelines. During the first six months of 2024, PE-backed IPOs surpassed the value from the previous two years combined.14 In Europe, 13 PE-backed companies have completed an IPO during the first half of the year, compared to 15 for all of 2023.15 However, the IPO markets in the United States and Europe remain well below their respective record levels achieved in 2021, and a catalyst may be needed to propel AUM growth to the next level.16

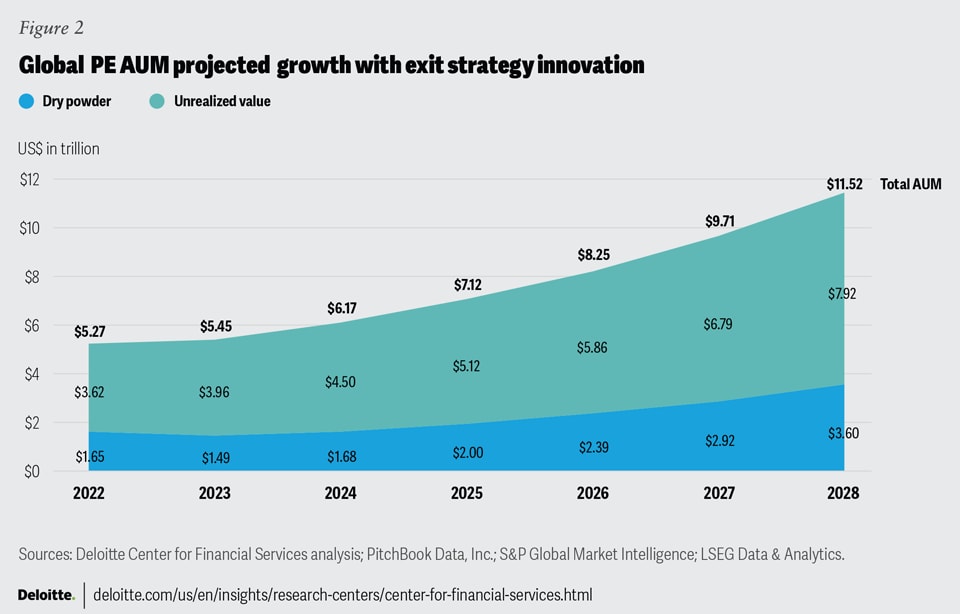

One such catalyst may be the success of private IPO launches for PE-backed portfolio companies. While public IPOs are likely to remain a viable exit option, the development of a structure that can allow for an IPO-like liquidity event regardless of public market valuation conditions will likely be well-received by GPs looking to get off the sidelines. In the fast AUM growth scenario, private IPO structures become widespread throughout the industry, and the mix of an IPO as an exit type is expected to increase from 15% in 2024 to 40% in 2028. Per the model, distributions to investors are expected to climb at a 25% annual rate from US$386 billion in 2023 to almost US$1.2 trillion in 2028. In this scenario, now flush with cash from realized gains, LPs participate in new fund launches, and fundraising is expected to top US$1.5 trillion in 2028, leading to record levels of dry powder and a total AUM of US$3.6 trillion and US$11.5 trillion, respectively (figure 2). Irrespective of the fund’s size, overall satisfaction with private equity fund managers could soar to new highs as additional liquidity from new investors creates more frequent distributions to existing limited partners. As existing LPs would have more cash on hand, they could reinvest in new GP fund launches, which may drive dry powder to new record highs.

Faster AUM growth through greater liquidity

Even as valuations improve and the prospects for a “fast AUM growth” scenario develop, exit activity still lags previous industry levels. Globally, PE exits in the first half of 2024 remained below that of the same period in 2023 by both dollar value and count, a signal that lower liquidity for some LPs persists.17 However, a closer look at the data indicates the tide may be starting to turn for some regions. The average size of PE-backed exits in Europe and the United States were up 21% and 47%, respectively, through the first six months of 2024, compared to the average exit in 2023.18 This lift may be a signal that even if GPs do not innovate to provide additional liquidity events for LPs, holding periods for PE funds as a whole are likely to drop somewhat as the opportunity to exit larger investments continues to materialize.

But if a fund’s port co exits fail to generate enough cash to distribute to investors, the GP may have to create liquidity through other means to satisfy investors’ needs. Elevated competition for new capital will likely drive innovation to increase liquidity at the port co level and access to capital for LPs, alongside stalwarts like a unique value proposition, investing track record, industry expertise, and relationship management acumen. There are already some signs of innovation for port co exits and for returning capital to LPs. Should liquidity innovation take hold, global private equity AUM growth may accelerate at an even greater pace than the “fast growth” scenario forecasts.

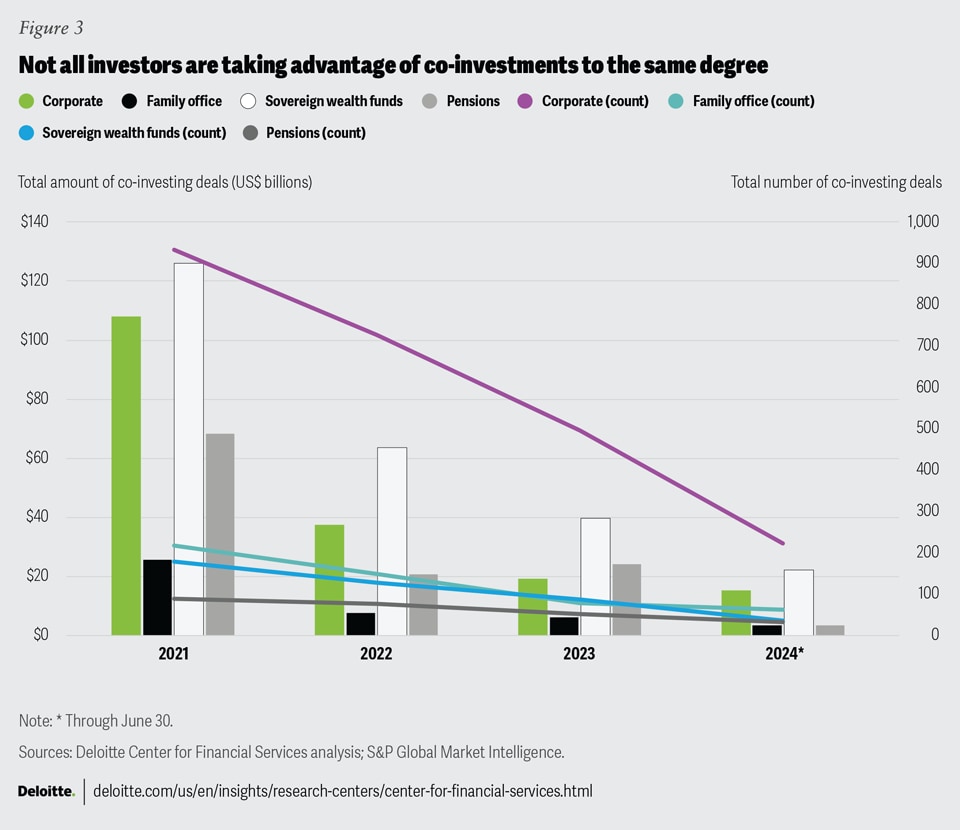

One example is midlife coinvesting, where new or existing LPs are given the opportunity to invest in a piece of a PE firm’s portfolio company.19 In response to demand for additional liquidity from some LPs, PE firms are increasingly facilitating these types of coinvestments.20 As with other coinvestments, the arrangement allows LPs to invest directly in specific deals, bypassing the traditional fund structure and associated fees, while potentially realizing quicker and higher returns. Midlife coinvestments can not only help PE firms raise new capital and provide a liquidity opportunity for existing investors, but also strengthen relationships between GPs and LPs by aligning expectations surrounding investments in specific portfolio companies and corresponding holding periods more closely. However, not all investors are taking advantage of all coinvestments to the same degree, and a better understanding of these differences may benefit PE firms exploring midlife coinvesting as a potential liquidity option.

Sovereign wealth funds (SWFs) participated in about half of all global coinvesting deals by value in the first six months of 2024, while corporate investors accounted for just over a third of the total value, and the remaining portion split about evenly between pensions and family offices (figure 3).21 SWFs coinvested in only 10% of the total number of deals, while corporates invested in about 66%, signaling that SWFs may tend to favor fewer but larger-sized deals, while corporate investors prefer the opposite.22 These deal characteristics of SWFs and strategic corporate investors have remained unchanged even as global coinvesting has fallen from an all-time high of US$260 billion in 2021 to about US$83 billion in 2023.23 While the pace of coinvesting throughout the first half of 2024 slowed from the same period the previous year in both total value and number, the median deal size slightly increased, suggesting investors are maintaining some appetite for such deals.24 GPs could benefit from providing a diverse array of services to meet the specific needs of these investors when considering offering a coinvesting opportunity, including the midlife coinvestment subset.

As interest rates are expected to fall and IPO markets could reignite, GPs may be well served to develop market cycle–insulated exit strategies for portfolio companies. As an example, private IPOs of portfolio companies are an emerging strategy that will likely gain traction. Private equity firm EQT is exploring how a private IPO structure may work for some of their best-performing portfolio companies, allowing them to retain control, yet letting investors enter and exit as desired.25 The demand for private IPO structures is causing traditional dealmakers to explore the concept. For example, Nasdaq Private Market is examining the opportunity to offer private equity and venture capital firms a platform for divesting portfolio company stakes to institutional investors over a set period of time.26 Interest in private IPOs is likely to grow over the next few years and may even rival traditional IPOs as an exit option for private equity firms in the intermediate term.

Some GPs are exploring single- and multi-asset continuation funds. Here, portfolio companies are placed into a new fund that allows LPs the opportunity to exit and receive cash for their investment or continue their investment through the GP’s new or continuation fund. For GPs, this approach can create an opportunity to continue to create value for the portfolio companies, while shielding them from the added complexities and uncertainties of an IPO, while generating a potential return of capital for LPs. During the first six months of 2024, GPs in North America and Europe announced or completed 49 continuation funds, an increase of 48% from the first half of 2023.27 Continuation funds will likely remain an attractive option for GPs looking to create a liquidity event for their investors because it builds relationships with investors through increased active engagement, potentially providing a competitive advantage through investor satisfaction in both existing and new investors alike. However, GPs may benefit from a review of their procedures related to continuation funds as the recently released 2025 US Securities Exchange Commission examination priorities note that the disclosure of conflicts of interest and risk, and the adequacy of policies and procedures will be in focus during the agency’s review of adviser-led secondary transactions.28

Another approach some GPs are focusing on to help extract value out of their underlying holdings and create liquidity for their investors is NAV loans. These loans are revolving credit facilities backed by entire PE fund portfolio holdings. While NAV loans are typically used to make new investments without having to call capital from investors, their usage as a method to distribute cash to LPs is increasing.29 In 2022, the Fund Finance Association estimated the size of the NAV facilities market to be approximately US$100 billion, and some fund finance participants expect the market to grow to US$600 billion by 2030.30 Growth over the next two years in the use of NAV loans is likely to be dependent on interest rates and their impact on private credit, as well as regulatory scrutiny related to the potential for conflicts of interest and a lack of transparency.31 Even so, the ability of GPs to customize the terms and structure of the NAV loan makes them an attractive option to provide LPs with liquidity. GPs are likely to continue to evaluate the costs and appropriateness of NAV loans for their funds and the ongoing willingness from LPs to accept liquidity in this form.

How might increased liquidity contribute to greater opportunity for retail investors into private equity funds?

Greater liquidity in private equity funds may also appeal to a group of investors that have historically been on the sidelines when it comes to private equity: retail investors. This investor group may benefit from having the option to add private equity to their portfolios.32 Since the start of 2024, firms such as Thrivent and Meketa Investment Group have launched funds that give retail investors exposure to private equity.33 These structures manage the illiquidity of their private equity holdings by either limiting the private equity exposure to 4% to 6% of the fund, or operating as an interval fund in which investors may redeem up to 5% of their investment on a quarterly basis.34 While these are solutions meant to work within the current illiquid nature of private equity, this nature may be changing. More exit options may provide GPs with additional foresight to better predict their funds’ cash flow requirements. With greater predictability, some PE firms may take a strategic approach to liquidity and permit investor-initiated liquidity events more often which may appeal to a broader set of investors. Retail investors may benefit as novel PE exit strategies, in lieu of public exits, increase the breadth of private investments available for active funds. Portfolio managers may add to their portfolios with less fear of the long commitment periods typically associated with such investments.

Looking ahead

Underpinning these alternative deal methods and exit strategies continues to be a question around how GPs continue to satisfy LP exit goals and liquidity requirements. The market challenges over the past few years have been a reminder to investors about the importance of maintaining liquidity and capital through economic downturns boosting the opportunity to seize undervalued investments.

How might GPs manage from here? In 2024, fundraising demand has reemerged, and a lower-rate environment will likely bring investors back to the table. GPs who are able to maximize their assets’ returns through both acquisition and IPOs will likely fare well in the years to come. The lack of deal activity in the past few years has brought to the table alternative deal structures and exit strategies that can give LPs a more comprehensive list of investment-related opportunities. This, combined with a potentially reignited IPO market and lower-rate environment, will likely increase liquidity provided by GPs and raise overall satisfaction with private equity fund investors, thereby contributing to dry powder growth and new fund flows for years to come.

Methodology

The Deloitte Center for Financial Services’ Global Private Equity AUM Growth model forecasts global PE AUM using the percentage of private equity exits conducted via IPOs, the percentage change in the dollar value of PE-backed IPOs, and the growth of developed economies’ public equity markets as the explanatory variables. The model utilizes regression analysis to evaluate the relationships between private equity exits from investments, deal activity for new investments, fundraising from investors, and dry powder to forecast global private equity AUM annual growth through 2028.

{kind=link}

{kind=link}

{kind=link}