Increased digitization

Many tax departments function on manual processes coupled with limited digital support for data collection and processing activities. As tax regulations become more interconnected, tax departments may be required to digitize in order to keep up with the flexibility and speed of reporting requirements. According to a Deloitte survey, 70% of survey respondents across industries, including financial services, predict that government revenue authorities will have more direct access to their systems within three years.9 Furthermore, some revenue authorities are shifting to real-time digital tax compliance models requiring a quick turnaround.10 To keep up, taxation systems may need to connect a company’s internal data sources with the compliance systems of revenue authorities. Compliance with emerging real-time data requirements may push tax departments to digitally transform, adding additional operational burdens to an already strained tax department.

Implementation of strategic operating model changes may help tax departments focus resources and increase opportunities to contribute more meaningfully through activities such as strategic planning, tactical business advisory support, and management insights.

Strategic operating model changes can help firms balance cost constraints with talent and technology needs

Filing frequent, digitized, and granular reports and managing the impact of higher global complexities and an evolving regulatory landscape require considerable investment in talent and technology. Tax operating model changes can help firms fill the technology and skills gap and simultaneously realize cost savings.

Technology can help firms more efficiently tackle the highly resource-intensive tax compliance process. It also needs to be agile and scalable to handle the frequent changes in the complex tax ecosystem. Although tax may be a critical function for operations, finance leadership may prefer to allocate resources to functions that contribute more directly to customer success. According to a cross-industry survey, lack of resources and budget top the list of reasons for respondents’ underutilization of technology in tax operations.11 Strategic changes to the tax department's operations can help firms mitigate the costly and burdensome exercise of continuously upgrading technology systems by leveraging the services of an external service provider.

Some companies now expect tax functions to contribute more strategically as they accelerate digital transformation. According to a Deloitte survey, 67% of respondents from the financial services industry expect increased demand for tax advisory support for digital business models.12 To keep up with evolving responsibilities, firms may also need to upskill talent as tax professionals of the future could require a very diverse skill set. The diverse skills required are expected to include global project management, data management, technology application, process optimization, and strategic business advisory.13 Strategic outsourcing can relieve the firm's tax department from talent hiring, retaining, and upskilling responsibilities and allow the retained employees to focus on oversight and higher value-add items.

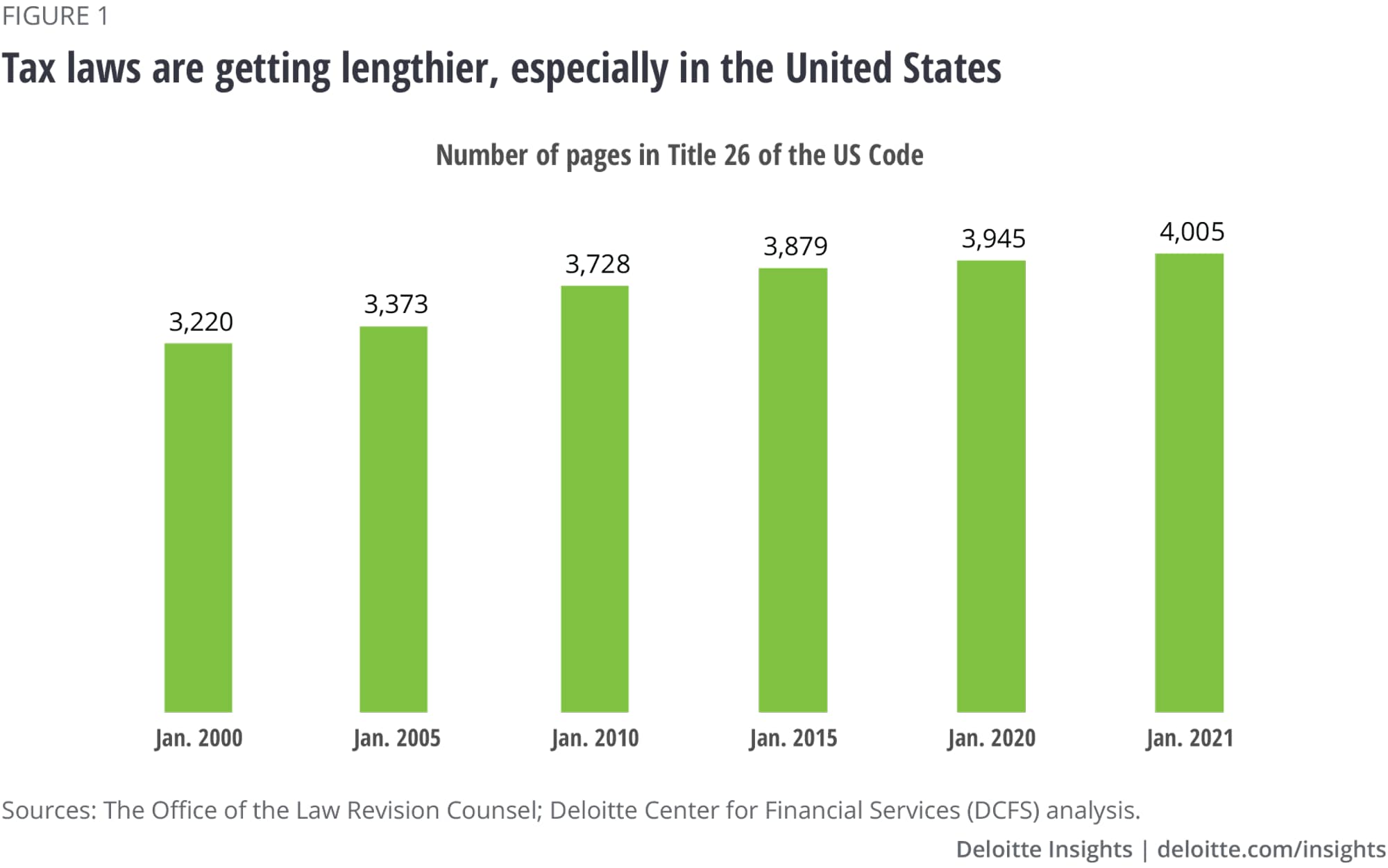

However, one of the most important factors that make a case for implementing strategic operating model changes is the cost savings potential. The Deloitte Center for Financial Services developed a proprietary model that forecasts how much expenditure an investment management firm's tax department can save through these strategic changes. The model predicts savings from as much as 23% to 31% of the tax department's total cost, depending on the firm's current level of outsourcing. Factors that could contribute to savings include better employee utilization, process efficiencies, hiring and replacement cost savings, and other synergies accrued from consolidation of operations to leveraging one service provider. Improved technology and process efficiencies are the major expected contributors to cost savings, not reductions in force. For an industry facing margin pressures, such savings can translate into an operating profit margin rise of 14 to 19bps.14 The model predicts that the realized savings reach their full potential gradually in three to four stages as the transition proceeds, as effective communication, talent transition, and process and technology realignment take time for fruition. Each stage may typically last 3—12 months depending on the organization's size. Furthermore, the model assumes that the level of work remains the same; however, since the tax regulatory environment continues to grow in complexity, the realized savings may exceed the estimates. The model also forecasts that the US investment management industry could potentially save about US$3.5 billion over the next five years through strategic operating model changes in their tax departments, assuming that the sector starts realizing the full potential of savings.15

In a nutshell, these strategic solutions can help firms establish a tax operating model that creates opportunities to save costs and repurpose resources from managing critical operational tasks to performing tasks that more directly drive value for customers and the firm.

{kind=link}

{kind=link}

{kind=link}