Health tech investment trends: How are investors positioning for the future of health? Insights into the quickly emerging health tech sector

16 minute read

12 March 2020

Insights from funding data and investment expert interviews reveal that health care innovators have begun to fill the gap between current and future needs. It's time for health care incumbents to strategize accordingly.

Executive summary

Health care incumbents—providers, payers, life sciences organizations, and transactional players—are working to bend the cost curve and improve care quality. Many leaders say they see consumers and the adoption of advanced technologies as part of future strategies, but they also tell us there are many challenges and barriers to integrating them. The gap between what health care incumbents offer today and what will likely be table stakes in the future of health has created an opening for health tech innovators—nimble, consumer-focused, tech-centric companies. These companies are offering solutions that could help incumbents survive in the new world—whether they become partners or disrupt them (see sidebar, “Health tech defined”).

The Deloitte Center for Health Solutions found that venture capitalists, certain private equity investors, and corporate venture funds are investing in products, services, and solutions that will enable the future of health. We interviewed 15 health tech investors and analyzed data for 2011 through 2019 from Rock Health’s Digital Health Funding Database. We found:

- 2018 and 2019 saw rapid increases in investment into well-being and care delivery innovators, as well as innovators leveraging AI, machine learning (ML), and the Internet of Things (IoT) to enable their products and solutions.

- Investor arms of health care corporations (CVCs) approach investing in health tech innovators differently than traditional venture capital (VC) firms. They often serve as advisers or counselors to early innovators, which can allow the company to have a sounding board and laboratory. At the same time, CVCs tend not to be as ROI-focused as their traditional VC counterparts.

Learn more

Explore the Life sciences collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

Health care incumbents should pay attention to these trends as they plan their strategies for the future. Health tech innovators are developing capabilities, products, and services that will likely be critical to the future of health. And as health tech investors and innovators continue to develop differentiated products and solutions for this market, they should consider where the industry is headed in the future. New archetypes may require new companies and solutions to address aspects of health that go beyond traditional services and capabilities.

Health tech defined

Health tech, as the name suggests, is the convergence of health care and technology. Our analysis of funding for health tech innovators is based on data from Rock Health. Rock Health tracks innovators where technology itself is a product or service. It excludes companies that may have technology as an enabler, but are focused on nontech services and solutions. For instance, the data set doesn’t include organizations like Oscar Health, Clover Health, or One Medical.

Background

Funding for health tech innovators exceeded US$7.4 billion in 2019 and funding data shows that investors continue to be bullish about investing in the health tech field.1

Venture funding to innovative companies is often considered an important barometer of their value propositions and long-term success. Moreover, it can indicate future market performance and emerging trends. To that end, we analyzed where investors—traditional VC firms and CVCs—are placing their bets in the future of health. We interviewed executives from 15 health care and nonhealth care VCs and CVCs and analyzed funding for health tech innovators between 2011 and 2019 using Rock Health’s Digital Health Funding Database. (For details, see sidebar, “Methodology.”)

Methodology

Quantitative analysis: We conducted data analysis of venture capital deals in the health tech space using data from Rock Health. We classified the innovators based on:

- Focus/value proposition of the innovator based on Deloitte’s vision for the future of health business models.

- Differentiated technology, based on the technology that distinguishes an innovator from its competitors:

- AI, machine learning, and deep learning

- Digital medical devices

- Genomics and sequencing

- Internet of Things (includes remote monitoring, telemedicine, wearables)

- Nonmedical device hardware

Executive interviews: We interviewed 15 executives from the investor community, both VC and CVC, to understand their views on health tech investments and the future. Interviews focused on top and emerging areas of investment, challenges facing health tech innovators, and core capabilities needed by innvators to succeed in health care, among other topics.

Investors are focused on the fundamental issues facing the health care industry

Venture investors are often accused of chasing shiny new objects, such as innovators with elaborate technologies or untested products, in pursuit of unearthing the next unicorn—without proper due diligence on the sustainability and impact of their value proposition. In health care though, that may not be the case. Investors we interviewed agreed about the fundamental issues facing the industry. They are backing innovators that align their value propositions to the present and future of health, with technology being the bedrock. Investors repeatedly emphasized that these organizations should:

- Enhance care quality: Key topics included connecting social determinants to health care, increasing patient engagement and driving behavior change, improving patient experience, enhancing adoption of remote patient monitoring, and promoting medication adherence.

- Reduce costs: Improving clinical and operational workflows inside health care, creating point solutions to areas of friction in the system, taking waste out of the system, integrating real-world evidence into solutions using technology, and enhancing clinical trial recruitment and monitoring.

- Improve access to care: Virtual care delivery and telemedicine were two solutions that interviewees often mentioned.

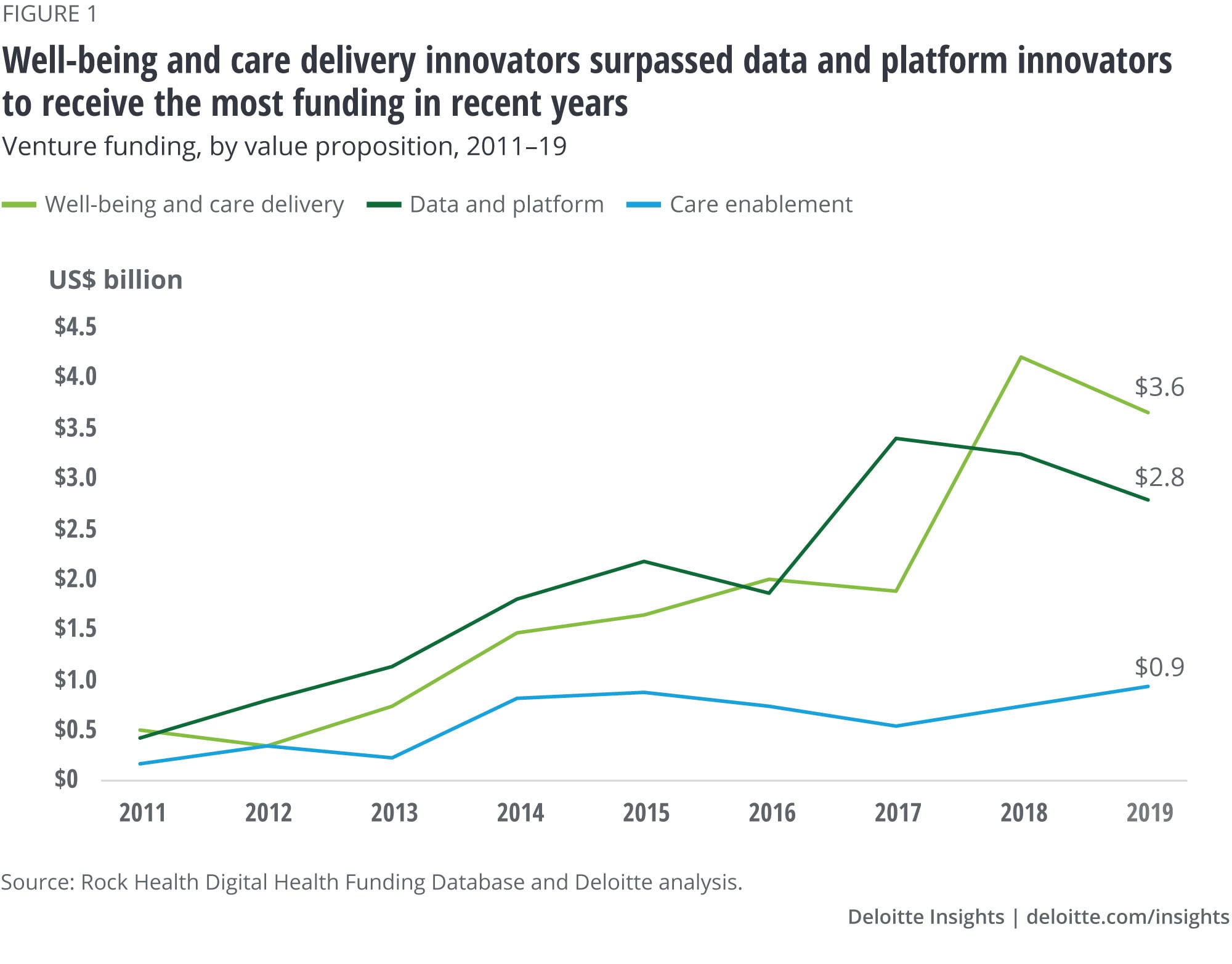

Well-being and care delivery innovators surpassed data and platform-focused innovators to receive the most funding in recent years

By 2040, health care as we know it today will no longer exist, as “health care” will have shifted to “health.” Through this transformation, we predict that new archetypes, or business priorities, for stakeholders in health care, technology, and more will emerge. The archetypes will likely fall into three distinct, but interconnected, categories:

- Data and platforms: These archetypes will be the foundational infrastructure that forms the backbone of tomorrow’s health ecosystem. They will generate the insights for decision-making. Everything else will build off the data and platforms that underpin consumer-driven health.

- Well-being and care delivery: These archetypes will be the most health-focused of the three groupings, made up of care facilities and health communities—both virtual and physical, and will provide consumer-centric delivery of products, care, wellness, and well-being.

- Care enablement: These archetypes will be connectors, financers, and regulators that help make the industry’s “engine” run.

We took Rock Health data on digital health funding from 2011 through 2019 and mapped each company’s value proposition to these three categories. In doing so, we found that historically, data and platform innovators have received the highest funding. But funding in this area plateaued in 2018, while funding for well-being and care delivery innovators accelerated. After steady growth from 2011 to 2017, funding for well-being and care delivery innovators doubled in 2018 to more than US$4 billion from a year earlier. While funding dipped in this category in 2019, it remains well above funding for data and platform innovators (figure 1). (See sidebar, “2018: An all-star year for health tech.”)

Innovators spotlight

HeartFlow is a well-being and care delivery innovator and is transforming how clinicians treat and diagnose cardiovascular disease. It provides a noninvasive test that peeks into a patient’s coronary arteries to diagnose blockages. Traditionally, such a diagnosis involves an invasive, painful, and slightly risky procedure. Using deep-learning algorithms, the test receives comparable measurements from a CT scan. For a US$1,450 test, HeartFlow claims it prevents US$4,000 in further costs. In the United States, commercial plans and Medicare pay for this test. The United Kingdom’s National Health Service (NHS) has rolled out the test in more than 40 hospitals since 2017.2 HeartFlow raised US$65 million in its latest funding round.3

Health Catalyst is a data and platform innovator founded in 2008. Its proprietary “Data Operating System” (DOS) is a data warehousing product that helps health care organizations combine data from different data systems into a single cloud-based platform for decision-making. It also provides add-on AI-driven analytics solutions and services. With data and insights from Health Catalyst, more than 120 health care organizations have improved quality of care, cut turnaround times, and reduced costs.4 For instance, a regional health system achieved a 36.4 percent reduction in sepsis mortality rate using Health Catalyst’s data platform and analytics applications. Similarly, another regional health system saved US$17.4 million by reducing unnecessary blood transfusions through predictive modeling to risk-adjust blood utilization specific to patient case-mix.5 Health Catalyst raised US$100 million in its last round of funding in early 2019.6

2018: An all-star year for health tech

According to Rock Health, 2018 was a record-breaking year for health tech innovators. That year, 380 organizations received funding totaling US$8.2 billion, with an average deal size of US$21.6 million. Much of the difference was that the innovators that eventually conducted initial public offerings (IPOs) in 2019—Livongo and Peloton—raised a combined US$655 million in 2018. As Rock Health puts it, “Moderation, rather than contraction, best describes the trend going into 2020.”7

Technology is a table stake

Several investors we interviewed said that technology will be a critical enabler in the future of health. However, success for health tech innovators may hinge on their ability to pair a differentiated technology with the right value proposition to create a sustainable business model.

“Technology is an enabler of existing workflows and process that haven’t been able to scale historically.”—Health tech investment expert

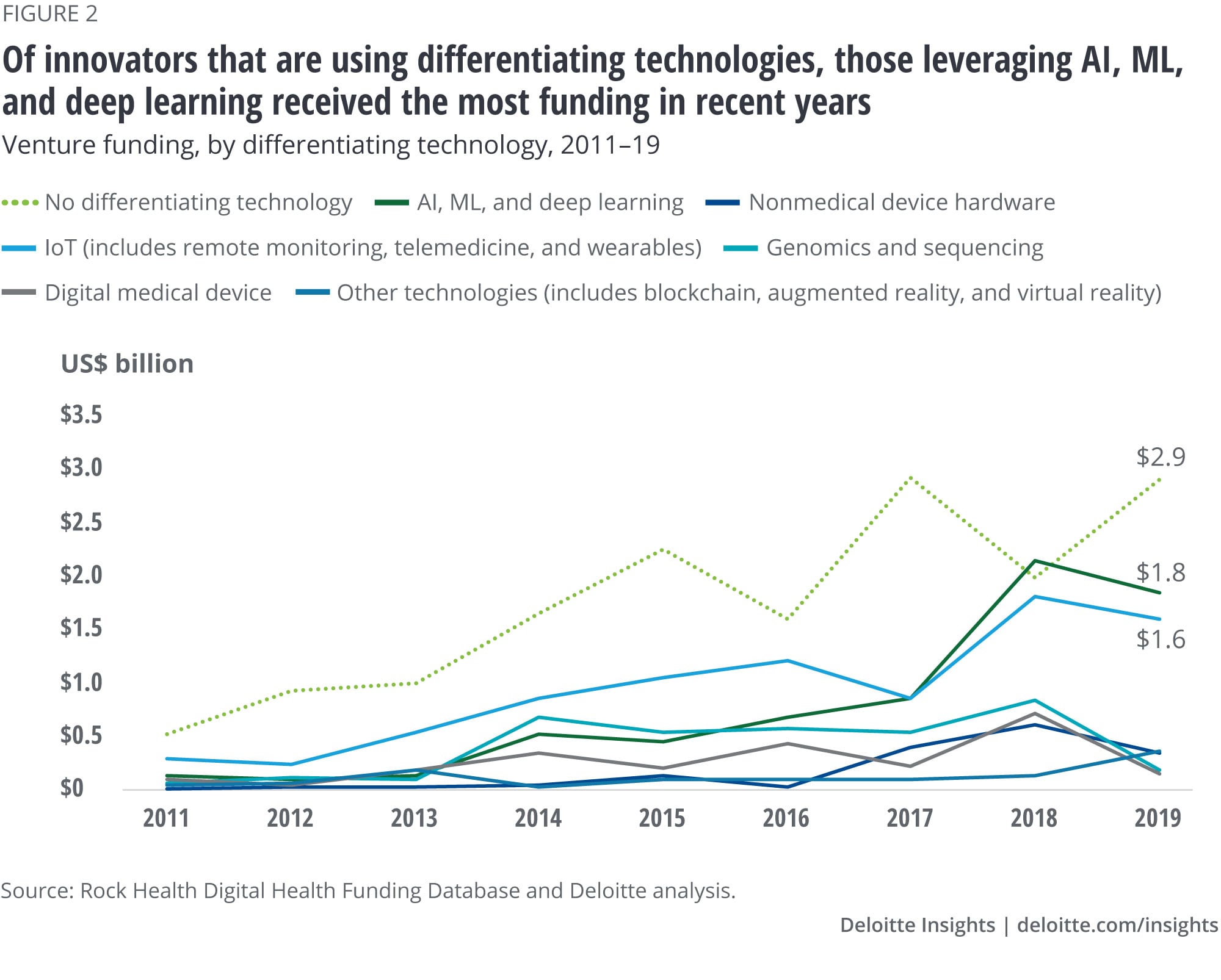

We found that as of 2019, only about half (52 percent) of these organizations are using differentiated technology—emerging technologies that could transform business models—as a foundation for their products or services. Of the innovators with a differentiated technology, those leveraging AI, ML, and IoT received the most funding in 2019 (figure 2). Experts said that proof points from pilots, greater clinical validation, more responsive regulatory frameworks, and fundamental technology changes—such as the exponential increase in computing capabilities coupled with a reduction in costs—are driving greater investment in AI and ML technologies. A few experts said that the exponential increase in funding for this area could be a short-lived hype cycle, however. There is also growing concern from investors around the “black box” problem—that it is too difficult to understand how algorithms make their decisions.

Innovator spotlight

Butterfly Network aims to democratize ultrasound technology. Ultrasound technology is an essential part of diagnosis and well-being monitoring today. But standard ultrasound machines are bulky, expensive, and at times, cumbersome to use. Butterfly Network’s flagship product Butterfly IQ is a handheld device the size of a smartphone and uses a single semiconductor chip instead of typical piezoelectric crystals. Starting at under US$2,000, it is 80 percent less expensive than previous attempts to make ultrasound machines portable.8 By making ultrasound imaging easy to use and more accessible, the company is hoping to give doctors a real-time understanding of the body without some of the harmful risks and delays associated with radiation-based imaging technologies. The company is already making inroads beyond the US market—in Europe, Asia, and even Africa—to provide accessible and affordable imaging to “two-thirds of the world’s population who get no imaging avenues at all.”9

Ginger.io, founded in 2011, is helping Americans cope with mental and behavioral health issues through technology. About 50 percent of all Americans are diagnosed with a mental illness or disorder, such as depression, at some point in their lifetime.10 Ginger.io’s app provides users access to emotional care and counseling by connecting with health coaches through video chats and chat messages, either in real time or through virtual appointments. Ginger.io’s AI algorithms analyze data from the user’s smart phone to relate their behavior with their health. Based on the data and insights, the app creates a personalized care plan with an emphasis on the required behavioral changes for a healthier life. The company claims that 72 percent of its members have shown clinically significant improvements in symptoms of depression within 12 weeks.11

Innovators and investors interested in them face unique challenges in health care

The value and money flow in health care is different than most other industries. In retail, consumers use their money to directly purchase goods from the retailer. Even with banks, which are as highly regulated as health care, the money flows between the consumer and the bank. In health care, this is very different—thus creating one of the biggest challenges for innovators in this industry. As one expert put it, “these organizations have to figure out how to fight on both fronts”—the consumers and the health care system—because money doesn’t flow directly from the patient to the doctor, even if the value does.

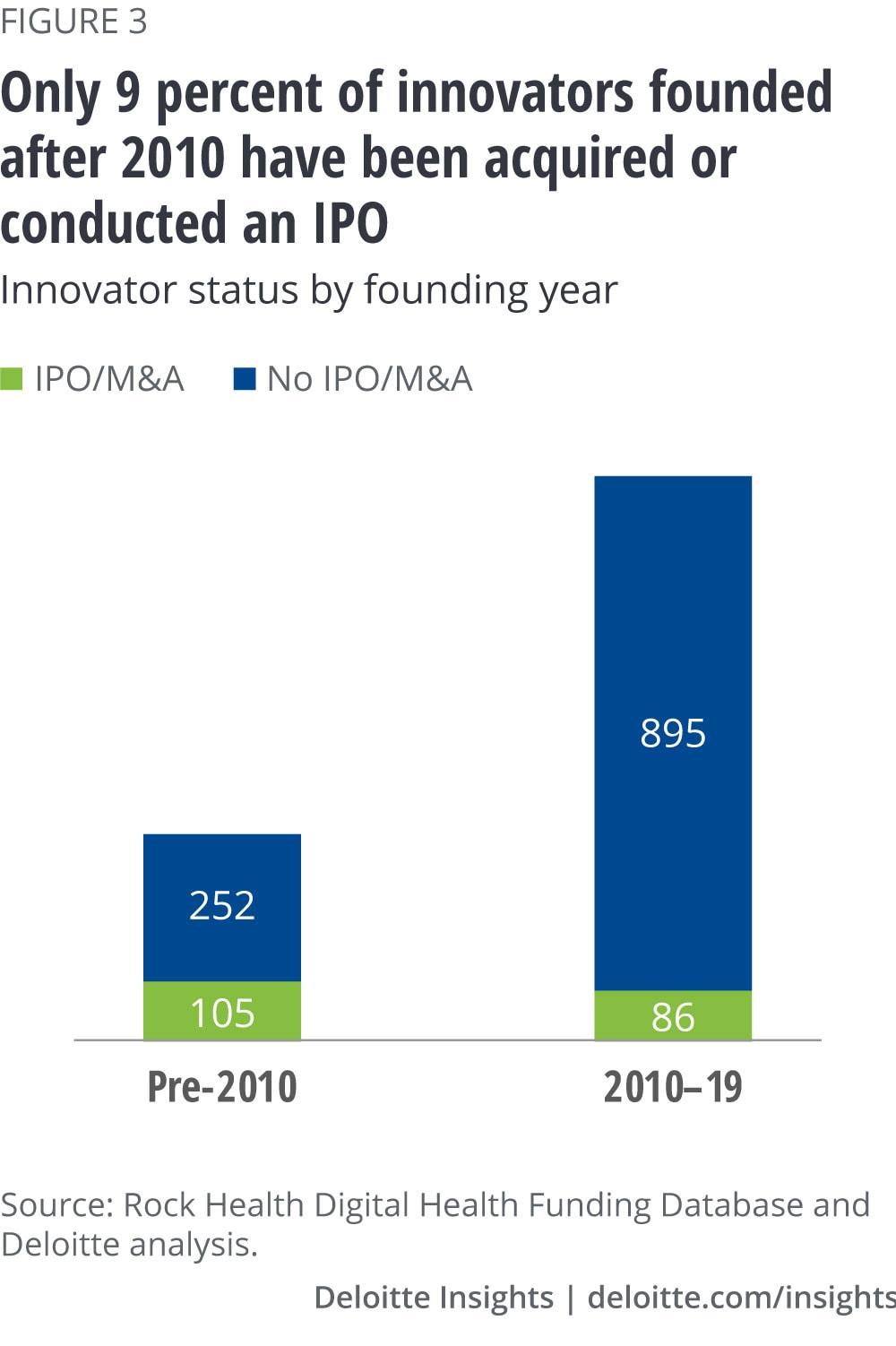

Rock Health analysis confirms the challenges to succeed in this industry: Only 9 percent of innovators founded between 2010 and 2019 have either been acquired or conducted an initial public offering (IPO) (figure 3). Data and platform innovators had the most exits during those years.

2019: The year of IPOs

2019 ended a three-year drought of health tech IPOs. A record-breaking five health tech IPOs took place in 2019: Livongo, Health Catalyst, Change Healthcare, Phreesia, and Peloton.12 Combined, they raised more than US$2.7 billion in cash, at a combined valuation of US$18 billion.13 The valuation is a testament to their winning value propositions—data and platform (Change Healthcare, Health Catalyst), well-being and care delivery (Livongo, Peloton), and care enablement (Phreesia). However, reaching this valuation took time; all but one was founded before 2010.

Health care organizations have a strategic place in the future of health through venture and innovation opportunities

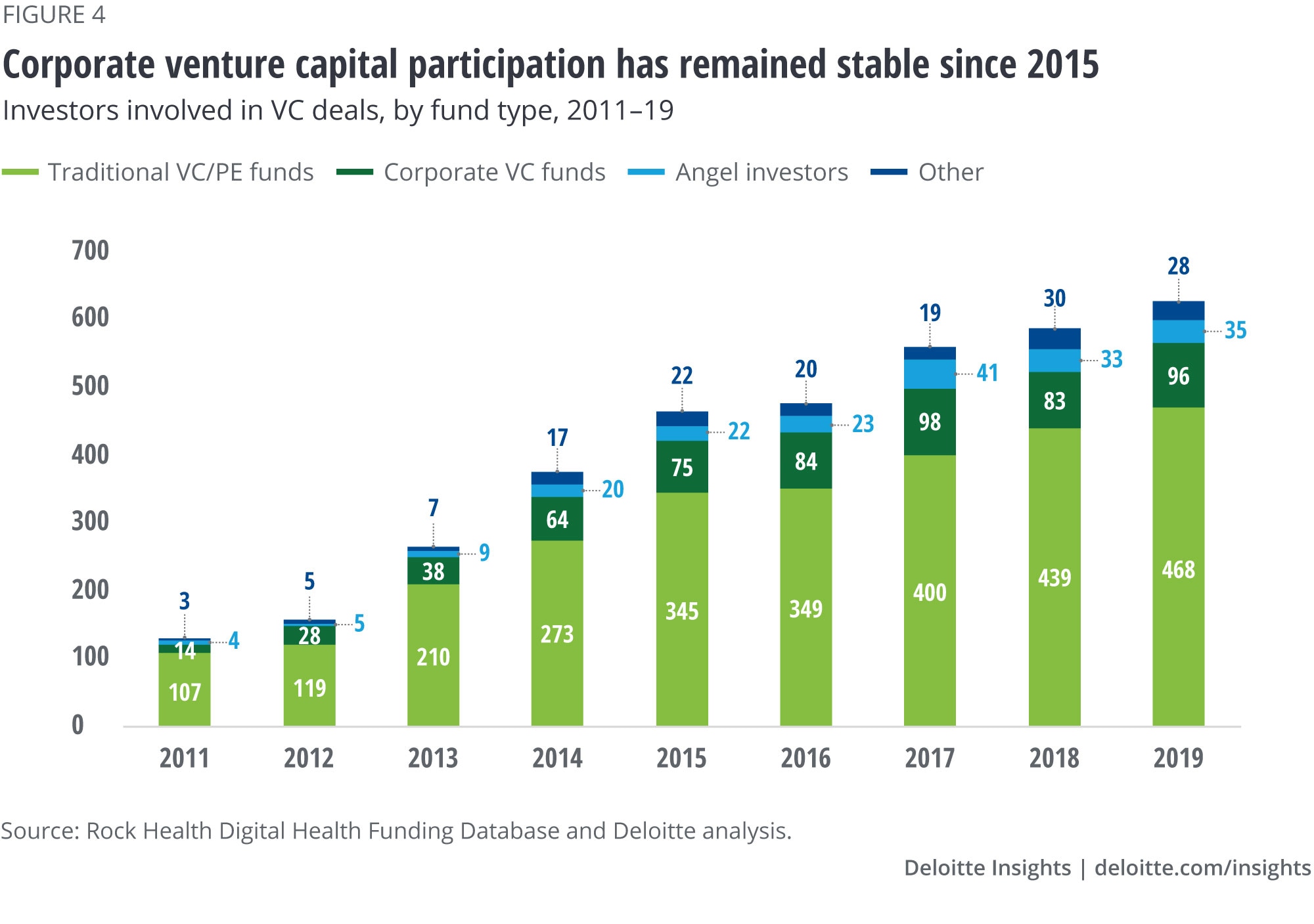

According to Deloitte’s 2019 Health Care CEO Perspectives Study, many leading health care organizations are developing investment funds to prepare for the ubiquitous change ahead, as technology becomes even more integrated into life, work, and culture. However, our Rock Health analysis reveals that while VCs are increasingly investing in health tech, participation of CVCs has remained stable since 2015 (figure 4).

Participation by corporate investors varies by area of focus. For example, investor arms of health care companies have focused on care enablement, as well as well-being and care delivery. Life sciences and technology companies have increasingly participated in data and platform deals. Technology CVCs—nonhealth care entrants seeking to disrupt the health care industry—have invested in data and platform, and well-being and care delivery innovators evenly. (See sidebar, “New entrants: Disrupting health care, not health care organizations.”)

New entrants: Disrupting health care, not health care organizations

Tech giants such as Google, Amazon, and Apple Inc.14 have been trying to get into the health care industry for the last 10–15 years. Some have had early wins, but many have learned it is difficult to disrupt from the inside out due to the inherently complicated nature of the industry (operations, regulations, etc.).

Deloitte’s 2019 Survey of Health Care Strategy Leaders found that 57 percent view competition from traditional and new entrants as their top source of concern. Indeed, disrupters often have the value proposition to tackle waste in health care—they are nimble, efficient, consumer-centric, solution-focused. But interviews with experts indicated that many believe incumbents should be a part of the change for disrupters to be successful. New entrants should work with large incumbents through partnerships and collaborations to blend their value proposition with the right health care expertise and disrupt health care.

According to Deloitte’s 2019 Health Care CEO Perspectives Study, however, many health care CEOs have mixed views. While many admit that the industry is ripe for disruption, and that these companies have the capabilities and dollars to do just that, others believe new entrants are not a threat because they will never deliver complex hospital care.

CVC spotlight

BlueCross BlueShield Venture Partners (BCBSVP), the corporate venture arm of the BlueCross BlueShield Association (BCBSA), invests in emerging companies that align with the BlueCross BlueShield (BCBS) strategy. Thirty-three BCBS entities have pledged more than US$575 million across three funds to invest in companies focused primarily on health tech.15 BCBSVP has 33 active venture partners such as:

- AbleTo: A program intended to increase access to care through virtual behavioral health platforms.

- Lumiata: A health care AI platform aimed at driving affordability and quality of care.

- Physera: An application-based platform providing musculoskeletal telehealth care to lower treatment costs by reducing unnecessary care interventions.16

BCBSVP’s approach is focused on long-term strategic partnerships to drive revenue and distribution, while simultaneously promoting innovation across the industry.

Merck Global Innovation Fund (GHI) is the corporate venture arm of Merck that invests globally in companies with proven technology or business models. Its aim is to increase revenue and enhance value creation. Merck GHI has focused its investments on health tech–centered companies and platforms. It has more than 40 digital health investments and US$500 million in evergreen funds.17 Merck GHI’s investments have concentrated on four major areas: therapy planning, care management, e-clinical trials, and health analytics and AI. Merck GHI’s active health tech investments include:

- Livongo: A company that uses connected devices and digital guidance to increase access to care.

- Preventice Solutions: A company that focuses on creating remote care technology and services to reduce the cost of care and improve health outcomes.

- Arcadia: A company that offers technologies and services to analyze and use data to improve quality of care.

Merck GHI’s strategy is concentrated on investments that have current revenue, are almost profitable, and that pursue growth capital.

What capabilities do health tech innovators need to succeed in the future of health?

Health tech innovators face a crowded market that is getting more challenging every year. While investment in this space continues to hold steady (despite a small dip between 2018 and 2019), health tech innovator should consider the three following capabilities as they take their products and services to market:

- The right value proposition: As one of the experts we spoke with put it: “A lot of companies … are trying to break into health care—but health care is breaking into technology. The reality is that in health care, it will be done the way it needs to be done and technology needs to be subservient to clinical models.”

- The correct metrics to show it: Investors are looking for measurable ROI on products and services. And oftentimes they look for returns within one to two years—this can be remarkably challenging for small innovators to deliver.

- The right people: Many of the experts we spoke with emphasized that health tech innovators should focus less on hiring people with hard skills like engineers and AI specialists—these workers are available now that training programs have caught up with the need. What is more difficult to find are leaders with soft capabilities, such as sales experience and leadership.

“They have to recognize that as people go through their day, their number one issue isn’t their health. No one got up this morning and said, ‘The number one thing I’m worried about is preventing diabetes.’ They’re focused on how busy they are; how stressed they are”—Health tech investment expert

Innovators should also consider the following key questions when building their products and solutions:

- How will it integrate? The products and services should integrate into existing workflow; but changing clinician behavior is very difficult. Many experts also discussed the difficulties innovators face when trying to work with or integrate into electronic health record vendors.

- Who will pay? Even if an innovator figures out the right business proposition to get their product into market, they may need a national salesforce to shop it around. As one expert explained, many early-stage companies fail to understand the heterogeneity of providers and payers. Further complicating the reimbursement strategy is the complicated employer-based model of health insurance in the United States.

- When will they pay? Sales cycles are long. For example, payers often have plans set out for years in advance, so innovators may have to wait years to receive investment.

- How will we change behavior? Patients. Clinicians. Getting the attention of the consumer: This is incredibly hard unless you have a strong value proposition.

- What are the regulatory barriers? For example, device-focused solutions can face lengthy regulatory approvals. Some investors said they avoid products like these altogether due to the added complexity and potential for failure.

Finally, health tech innovators may consider the various benefits of working with CVCs early in the process:

- Advice: CVCs can act as advisers/counselors for innovators. This allows innovators to use CVCs as sounding boards and laboratories.

- Access: They can also provide access to the right resources (e.g., people) to help understand problems from different perspectives.

- Patience: CVCs often aren’t as ROI-focused as their traditional VC counterparts. They give precedence to the change/solution they want to bring in with the innovator, instead of the ROI.

However, according to the experts we interviewed, CVCs can often be very rigid and too narrow in their focus. They might not allow the innovator to be nimble. Hence, such organizations may avoid early-stage funding from a CVC, when they might have to pivot the business on market needs.

“Sometimes they’ll have the best tech, but they’re not really solving a problem that needs solving.”—Health tech investment expert

Where do life sciences and health care stakeholders come in?

Life sciences and health care companies can also work closely with organizations that are working on products and solutions that align with their strategic priorities.

- Help with early-stage ideation: Partner with innovators to help them get the value proposition right before they start shopping their products/services around.

- Bring regulatory expertise: Help innovators understand the regulatory barriers that will exist at the start and as they get deeper into health care.

- Build the right business development, product development, and innovation teams: Leaders should focus on creating teams that make strategic investments. But they also need teams that help inform those investment strategies by identifying ways that innovators’ products and services will integrate into existing business models and processes.

Health care incumbents should pay attention to these trends as they plan their strategies for the future. Health tech innovators are developing capabilities, products, and services that will likely be needed in the future of health. And as health tech investors and innovators continue to develop differentiated products and solutions for this market, they should consider where the industry is headed in the future. New archetypes may require new companies and solutions that address aspects of health that go beyond traditional services.

Deloitte Health Care

Innovation starts with insight and seeing challenges in a new way. Amid unprecedented uncertainty and change across the health care industry, stakeholders are looking for new ways to transform the journey of care. Our US Health Care practice helps clients transform uncertainty into possibility and rapid change into lasting progress. Comprehensive audit, advisory, consulting, and tax capabilities can deliver value at every step, from insight to strategy to action. Our people know how to anticipate, collaborate, innovate, and create opportunity from unforeseen obstacles.

Learn more

Get in touch

- Peter Micca

- Partner

- Deloitte & Touche LLP

- pmicca@deloitte.com

- +1 212 436 5468

Learn more about technology in health care

-

Health care Collection

Health care Collection -

Digital health technology Article5 years ago

Digital health technology Article5 years ago -

Virtual health care Video

Virtual health care Video -

Predictive analytics in health care Article5 years ago

Predictive analytics in health care Article5 years ago -

Showing cybersecurity's value to health care leadership Article5 years ago

Showing cybersecurity's value to health care leadership Article5 years ago -

Creating a treasure trove of data for health plans Article5 years ago

Creating a treasure trove of data for health plans Article5 years ago