Trend 2: Getting partnerships and joint ventures right Looking beyond structure to governance

8 minute read

03 February 2020

With junior miners’ capital constrained, and market capitalizations not reflecting full corporate value, some industry players are consolidating to gain scale. Joint ventures (JVs) can be a natural solution. Yet, even when structured right, JVs often fail due to unclear decision-making processes, ineffective governance, and poor transparency and alignment. Here are some ways to consider how to overcome those common challenges.

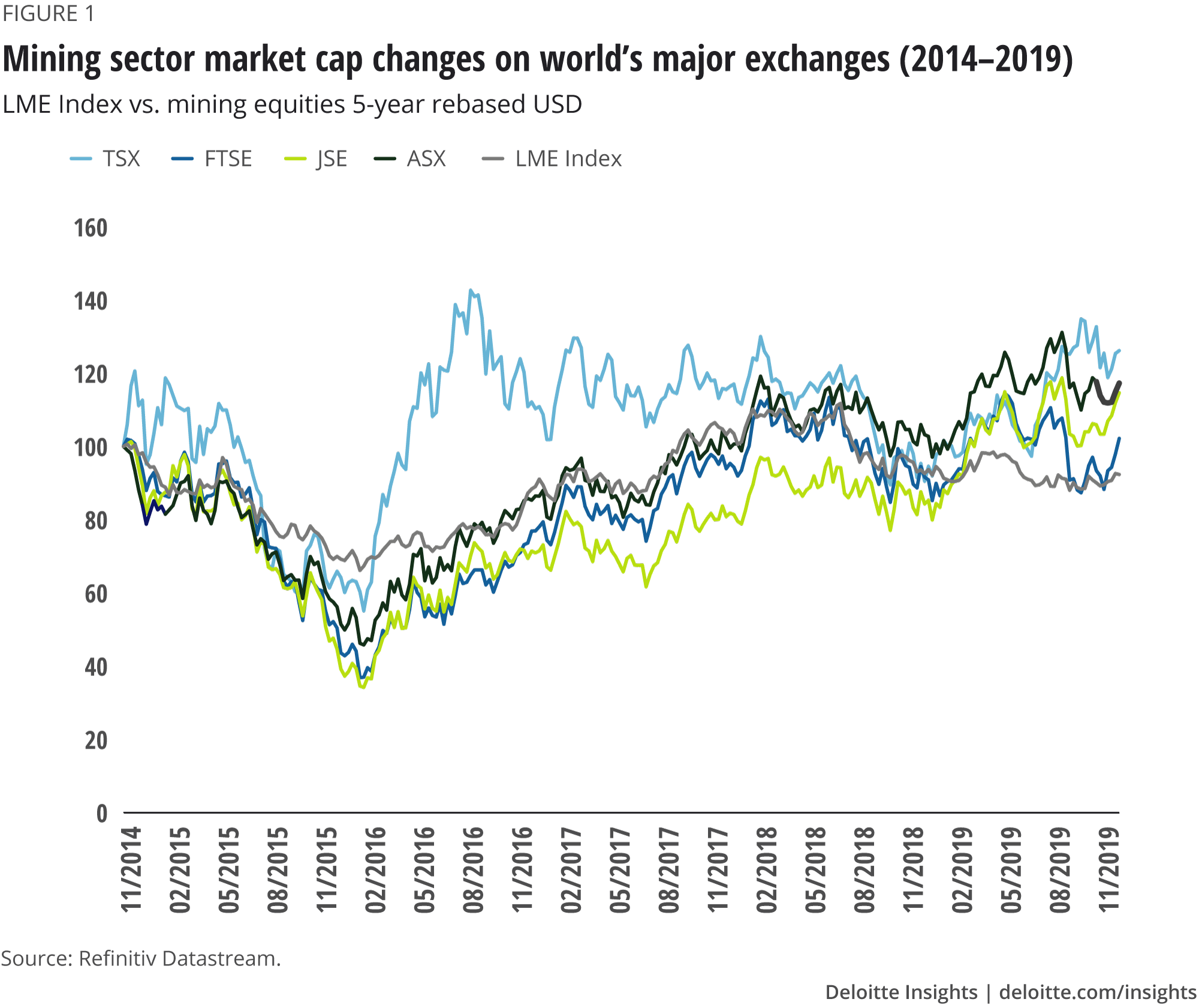

Although mining companies have made significant strides to strengthen their operations, streamline processes, integrate digital technologies, and deliver value beyond compliance, the industry is still often painted in a negative light. The upshot? Market capitalizations in the sector have been declining (figure 1) and companies—particularly juniors—still often struggle to raise capital.

Learn More

Download the full Tracking the Trends 2020 report or create a custom PDF

Join the conversation: #TTT2020

Learn about Deloitte's Energy, Resources & Industrials services

Go straight to smart. Get the Deloitte Insights app

Alternative funding models do exist—from royalty streaming to offtake agreements. Private equity firms, which once shied away from the resources sector, have also been investing more actively in mining companies, providing additional access to financing.

“Most pension funds now have some mining companies in their portfolios, as do a growing number of private equity firms,” says Rajeev Chopra, Global Energy, Resources & Industrials Leader, Deloitte Touche Tohmatsu Limited. “They understand that, while the sector could be volatile in the short term, it can offer strong long-term returns.”

The sector is starting to consolidate

Yet, despite these options, many juniors remain capital starved. This has spurred consolidation as companies attempt to gain the heft they need to attract financing and strengthen their performance metrics.

Merger and acquisition (M&A) activity has been picking up, especially in the gold sector. In the first half of 2019, Barrick acquired Randgold and Newmont acquired Goldcorp. At the time of writing this report, Kirkland Lake Gold announced the acquisition of Detour Gold, subject to regulatory and shareholder approval1. More transactions are likely to follow. Global deal volume in the mining and metals sector is also in line with previous year numbers (687 deals in first half of 2019 vs. 691 in first half of 2018), although deal value declined from US$48.2 billion to US$31.4 billion.2

Joint ventures (JVs) are on the rise too. Barrick and Newmont partnered to combine their assets in Nevada—creating the world’s largest gold complex.3 This is a classic example of companies finding synergies in the co-location of their assets. There has also been an increase in Chinese miners entering into JVs in different locations around the world. Juniors with promising deposits have also been increasingly successful in attracting the attention of majors interested in expanding their exploration portfolios. In fact, several large miners—such as Rio Tinto4 and South325—have explicitly committed to collaborating with junior and mid-tier companies on exploration projects around the world.

“Beyond access to funding, joint ventures can help juniors tap into critical expertise, relationships, and capabilities,” notes Chris Lyon, Partner, Financial Advisory, Deloitte Chile. “This can allow them to leverage digital technologies and alternative energy platforms, address sustainability issues, and meet mounting stakeholder expectations.”

And it’s not just juniors that stand to potentially benefit from these JVs. Given the size of capex projects in the mining sector, their location in remote regions, and the growing complexity associated with accessing many ore bodies, companies of all sizes can benefit from partners to finance projects, source critical skills, build local relationships, and share risks. Similarly, for investors, JVs can deliver shorter paybacks amid commodity price volatility, as well as security of supply for critical resources. The sector is likely to see more JVs going forward, making this an important competency area firms will likely need to build.

Avoiding the pitfalls

However, structuring a joint venture and successfully governing it to achieve corporate aims are two separate things.

“Companies understand they need to get advice to structure an effective joint venture,” explains Sunil Kansal, Partner, Consulting, Deloitte Canada. “There’s a lot of guidance around designing an appropriate capital structure and creating the shareholder agreement. Where joint venture partners typically run into trouble is in operationalizing these structures.”

To avoid common pitfalls, and maximize the success of a JV, companies should gain consensus around three operational elements.

1. Decision-making processes

Without a clear delegation of decision-making authority, well-articulated conflict resolution processes (particularly in a 50:50 JV), and agreement around decision approvals, JVs can struggle to take decisive action, resolve exceptions, or run productive meetings. To help mitigate these risks, partners should:

- Empower their governing bodies to optimize workflows, limit meeting frequency, and clarify delegation authority.

- Agree on the role of the non-operator in the JV structure.

- Give teams the flexibility to make certain decisions around budgets, work parameters, and staffing—and to act swiftly in urgent situations (e.g. health and safety issues or reputation management)—without the need for board approval.

- Create advance resolution strategies for common areas of conflict and build in escalation policies to avoid deadlocks.

- Proactively address the differences in each partner’s business strategies, values, processes, capabilities, risk appetites, and cultures.

- Reduce staff time spent in meetings and encourage online collaboration as opposed to frequent in-person meetings.

2. JV governance

Another area where partners can face difficulty is around governance of the JV. Negotiations can quickly devolve into key legal clauses without partners taking the time to step back and think through the bigger principles of the JV. Once the JV is in motion, partner and board interaction with the venture can lead to inefficiencies—such as inundating staff with urgent requests for custom reports or asking for one partner’s work to be prioritized over venture projects. In other cases, roles and responsibilities may be poorly defined, leading to duplication and overlap, conflicting decisions, and inconsistent workflows. Improper team composition and accountability can also lead to poor performance, high churn, and roles filled by quotas rather than skills and fit. To address these issues, partners should:

- Align early on the really big issues and create a key set of principles around issues such as exit options, point of views on environmental and government issues or how the JV might deal with unforeseen issues like subpar operational performance.

- Align activities between board members and management by appointing liaisons from each party to manage interactions.

- Standardize documentation and set agreed times for responses.

- Allow roles and responsibilities to evolve throughout the venture lifecycle to adapt to changing needs.

- Leverage each partner’s strengths to fill roles, assign responsibilities, avoid overlaps, and build transparency.

- Foster commitment to the venture by requiring full-time employment commitments and using venture key performance indicators (KPIs) for compensation and incentives.

- Ask seconded personnel to serve multi-year terms with the venture.

- Give venture leaders the authority to build their own teams, monitor performance, and assign work.

- Harmonize staffing levels by creating standard requirements for all roles.

3. Transparency and alignment

Most organizations understand the challenges associated with building an integrated organizational culture that promotes collaboration and fosters information sharing. Realizing this ideal can be even more challenging for multinational JVs staffed by multicultural teams. Cultural differences, different hierarchical norms, disparate communication processes, and possibly clashing approaches to privacy and transparency can create unintentional misunderstandings and miscommunication. To overcome these obstacles, partners should:

- Create a shared vision of what trust looks like for JV participants.

- Capitalize on cultural differences rather than demand similarities by recognizing the strengths of each partner while encouraging empathy and fairness.

- Have the JV develop its own mission, vision, values, purpose, and brand supported by a stand-alone marketing strategy.

- Develop consistent operational, technology, and governance approaches for the JV.

- Implement an integrated IT system to eliminate information silos and establish one source of truth.

- Set up a strong assurance function capable of resolving issues before they escalate.

What good looks like

“Even companies that engage in a lot of joint ventures struggle to transfer the knowledge gained from existing ventures to newly established ones,” Lyon notes. “To realize the full value of these relationships, their governance models should provide operational flexibility and facilitate rapid decision-making, while evolving the maturity of its governance model over time.”

Although it takes work, companies that get this right stand to possibly benefit from operational continuity, effective decision-making, streamlined conflict resolution, and empowered teams: critical outputs miners should consider investing in as they come to rely more heavily on joint venture arrangements.

How partnerships can create value beyond compliance

Beyond joint ventures, some mining companies are considering other ways to distribute the risks associated with major capital projects. One emerging model is to allocate project assets and liabilities across a full ecosystem of partners—from mining companies, original equipment manufacturers (OEMs), and service providers to local communities and governments.

The idea is not simply to de-risk project finances. It’s to de-risk project relationships by leveraging the skills of every ecosystem partner to extract greater value across the board. For instance, OEMs and service providers don’t simply contribute equipment and labor. They also share in decision-making and project milestones. Similarly, community stakeholders don’t simply approve mine activities or assist in its operation. They also earn a portion of the value created, which can be used to drive sustainable economic development.

This type of shared value collaboration allows companies, governments, communities, and other key stakeholders to work together to strengthen local economic clusters, achieve greater social impact, and increase the return on social investment. However, reaching this end goal is clearly a journey, which is why mining companies should start small before adopting a model that pools all funds and integrates governance structures.

In this regard, collaboration should be approached as a continuum across aspects such as initiative selection, implementation, funding, partners, decision-making, governance structures, and measuring impact (figure 2). It may also be useful to leverage technologies such as blockchain to enhance transparency and establish cross-organizational trust.

Considerations for JV success

- Lay the proper foundation. If properly structured, JVs can give juniors the opportunity to increase their percentage of ownership in the venture over time, so that by the time the mine is actually built they’re positioned to realize a measurable return on investment based on the work they’ve done along the way. To maximize the upside potential of these arrangements, however, it’s important to understand their financial implications from the outset. This means conducting financial modeling and assessing potential tax consequences up front.

- Select the right partners. A partner can change the trajectory of a JV, so choosing the right partner can be especially important. In some cases, the right partner is defined by their ownership of a critical asset, such as presence in a market or intellectual capital. Cultural fit should also be taken into account. While a culture clash shouldn’t necessarily derail a deal, knowing it exists informs the need for more detailed negotiations and alignment on governance and performance monitoring.

- Adopt the right KPIs. In addition to monitoring the performance of key JV initiatives, venture partners should aim to foster continuous governance improvement by expanding their KPIs beyond traditional measures. Consider tracking supplementary metrics, such as the number of projects identified, in the pipeline, or implemented; the average time it takes to resolve disputes and make decisions; the frequency of approval delays within a certain time period; and the number of issues that remain undecided each quarter.

Energy, Resources & Industrials

Deloitte’s Global Energy, Resources & Industrials specialists provide comprehensive, integrated solutions to all segments of the Oil, Gas & Chemicals, Power & Utilities, Mining & Metals and Industrial Products & Construction sectors. Offering clients deep industry knowledge and a global network.

Learn more

Get in touch

- Andrew Swart

- Global Mining & Metals Leader

- Deloitte Canada

- aswart@deloitte.ca

- +1 416-813-2335

© 2021. See Terms of Use for more information.

Explore the collection

-

Trend 4: Dynamically managing risk Article5 years ago

Trend 4: Dynamically managing risk Article5 years ago -

Trend 5: The path to decarbonization Article5 years ago

Trend 5: The path to decarbonization Article5 years ago -

Trend 6: On the road toward intelligent mining Article5 years ago

Trend 6: On the road toward intelligent mining Article5 years ago -

Trend 9: Leadership in an Industry 4.0 world Article5 years ago

Trend 9: Leadership in an Industry 4.0 world Article5 years ago -

Trend 10: Tax tribulations Article5 years ago

Trend 10: Tax tribulations Article5 years ago