Trend 3: Seize opportunity amid uncertainty Why miners should prepare for the next downturn now

5 minute read

03 February 2020

Commodity prices rise and fall in tune with economic trends, which are currently foreshadowing a potential global downturn. To avoid being blindsided, there are some bold plays mining companies can consider to prepare.

Learn More

Download the full Tracking the Trends 2020 report or create a custom PDF

Join the conversation: #TTT2020

Learn about Deloitte's Energy, Resources & Industrials services

Go straight to smart. Get the Deloitte Insights app

It seems the mining industry has barely recovered its stability before once again facing slowing economic growth. Globally, trade volumes are down and geopolitical tensions remain high. The inversion of the yield curve in the US, Canada and UK bond markets over the third quarter sent a strong market signal that a downturn might be in store.1

Concerns about China’s economic revival remain front and center. For the third quarter of 2019, the country’s GDP grew only 6 percent year-over-year—its slowest gain in more than 27 years.2

Several key forces appear to be driving this current level of economic uncertainty. Growing income disparities around the world seem to be giving rise to more nationalistic and populist governments. This is spurring a trend away from multilateralism. Free trade has even given way to protectionism in some countries, and the global economy is resetting to this new norm.

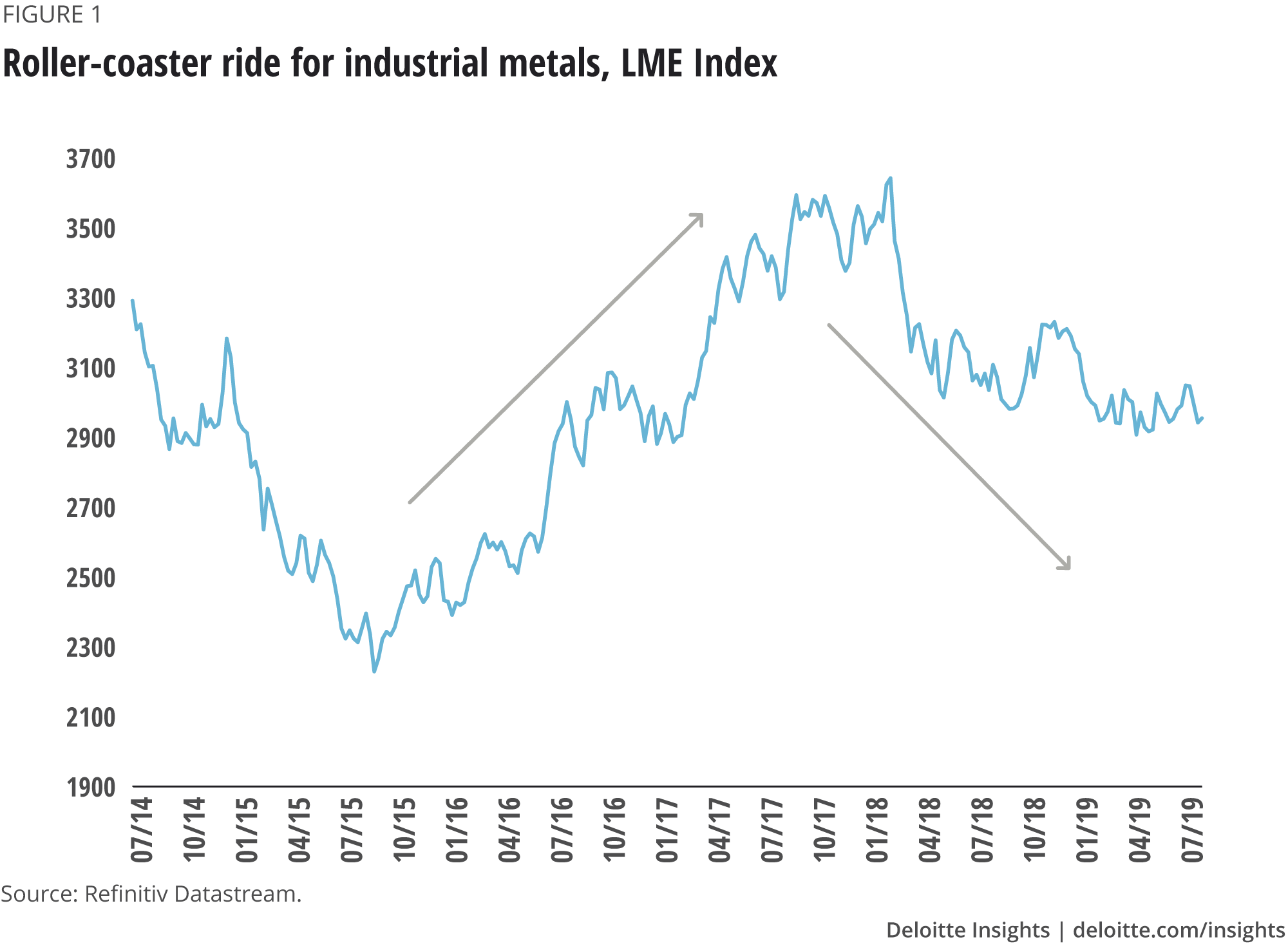

These macroeconomic headwinds are weighing on the industrial metals sector. Volatility across the sector has been rising, from base materials to bulk commodities, with some commodities being supported by supply side constraints (figure 1). For their part, precious metals have been benefiting from the investment community’s flight to safety.

Despite these variable fortunes, however, one thing is clear: commodity prices rise and fall in tune with global economic trends, and, right now, those trends may be heralding a downturn.

Bold plays for consideration

“If miners are to learn from history, the time is ripe to begin shielding against a downturn,” says Andrew Swart, Global Mining & Metals Leader, Deloitte Touche Tohmatsu Limited. Companies with commodity portfolios that may continue to soften should think about taking proactive action so they can emerge from any potential downturn more robust and in a better position to take advantage of the cycle.

Organizations can lay a foundation for this future through various bold plays.

1. Future-proof tomorrow

A downturn offers a clear opportunity to build the muscles to forge the future, not just react to it. Here’s how:

- Prepare, don’t predict. Since 1988, the IMF has never forecast a recession in a developed economy more than a few months ahead.3 That’s why it makes sense, instead, to prepare for a range of plausible scenarios rather than one generic “downturn” scenario.

- No plan ever survives contact with the enemy. To determine the reliability of their existing strategies, mining companies should stress-test those strategies against the “enemy” of volatility by asking how various scenarios might affect their strategies, how competitors are likely to react, and at what point they should shift their plans.

- Build institutional muscle. Both scenario planning and stress testing are exercises that, like interval training, build institutional muscles that can be critical regardless of economic conditions. Leadership teams that engage in these exercises can get to know each other’s strengths, weaknesses, thought processes, and biases, allowing them to build cohesion and identify ways to make the business stronger.

2. Don’t abandon innovation

When the going gets tough, many companies abandon their innovation and research & development (R&D) portfolios, seeing these as longer-term plays that don’t drive short-term value. It’s hard to resist this temptation. However, most downturns only last four to six quarters, and keeping that innovation focus now can position the organization for competitive advantage. Digital programs can also be refocused around key areas that drive short-term value, such as:

- Automation. The business case for automation in key areas of the organization is clear, and companies can benefit from continuing down this path.

- Analytics. Optimizing key portions of the process using big data analytics can yield substantial value. We typically see double-digit savings in optimizing different metallurgical processes.

- Waste removal. Focus in on key processes where there is often redundancy and where more streamlined processes can drive greater efficiencies. These are areas like integrated planning or driving short interval controls.

There are, of course, many other examples where innovation and digitization can add key value in the short to medium term. Companies should remain laser focused on driving these.

3. Don’t burn—redesign

Drastic cost cutting during a downturn can see companies trimming muscle, rather than fat. Typically companies that go through drastic cost reductions without redesigning the underlying processes see all that cost come back within a year to 18 months. Organizations need the muscle and, in the absence of rethinking how the work gets done, the cost will likely return. To avoid this:

- Take the time to redesign. Companies would be wise to look at the major workflows in their organization to identify alternative ways to get that work done—perhaps by automating, outsourcing, or using contract employees. The aim is to create something sustainable to position for lasting change.

- Preserve key talent. When leaders become overwhelmed by economic pressures during a downturn, they often neglect to invest in employee experience and reduce workforce management to an income statement exercise. To encourage employees to remain loyal through the bad times, companies should focus on helping employees find meaning in their relationship with work—even when the going gets tough.

4. Relook at your relationships

Downturns provide a great opportunity for companies to relook at their relationships and decide which ones to invest in, which ones to abandon, and perhaps which ones to renegotiate:

- Invest in the ecosystem. The easy answer might be to squeeze the supplier base for more savings and better prices. The harder, but potentially more value-creating, option might be for companies to look at new ways to create different incentives and work with their supplier base to achieve their goals. Making suppliers part of the solution rather than treating them as a commodity can help set miners up for longer-term value creation.

- Collaborate. Now might also be a good time to create collaborative relationships with competitors who might also be feeling the downturn. Very often, they are facing similar challenges and have a similar cost focus.

5. Acquire resources

The instinct is always to cut and reduce, but now might also be the time for companies to invest in key resources—specifically, assets and people:

- Take advantage of M&A. Mining companies going into a downturn with balance sheet strength have considerable advantage. Making strategic acquisitions at depressed multiples can create long-term accretive value. Many firms, however, leave it too late and find themselves acquiring when the market has already turned. Take the long view.

- Recognize people as tremendous assets. Whether it’s from within or outside of your industry, downturns can be great opportunities to make strategic hires. Now is the time for companies to think through their longer-term vision for the kinds of talent that can enable their long-term strategy and use the next 18 months to hire strategically.

“A period of volatility may offer unique opportunities that businesses can leverage if prepared. The key is to harness both the energy and constraints of volatile conditions to solve tough challenges and spark innovation.” says Bill Marquard, Director, Monitor Deloitte US.

Ways to help companies thrive during a downturn

- Align the executive team. Staying the course and taking advantage of opportunities requires an aligned management team. A regular cadence to review strategy, review the scenarios, and pivot accordingly can serve companies well.

- Own the narrative. These are uncertain times for everyone in the organization. Over-invest in communication, town halls, and one-to-one meetings. People long for transparency and, in the absence of clear communication, will create their own narrative.

- Create board alignment. Many of the actions discussed here may be counterintuitive to some. Creating a strong alignment with the board will often be critical for any management team.

Energy, Resources & Industrials

Deloitte’s Global Energy, Resources & Industrials specialists provide comprehensive, integrated solutions to all segments of the Oil, Gas & Chemicals, Power & Utilities, Mining & Metals and Industrial Products & Construction sectors. Offering clients deep industry knowledge and a global network.

Learn more

Get in touch

- Andrew Swart

- Global Mining & Metals Leader

- Deloitte Canada

- aswart@deloitte.ca

- +1 416-813-2335

Explore the collection

-

Trend 1: The social investor Article5 years ago

Trend 1: The social investor Article5 years ago -

Trend 6: On the road toward intelligent mining Article5 years ago

Trend 6: On the road toward intelligent mining Article5 years ago -

Trend 7: Modernizing core technologies Article5 years ago

Trend 7: Modernizing core technologies Article5 years ago -

Trend 8: The intersection of talent and community Article5 years ago

Trend 8: The intersection of talent and community Article5 years ago -

Trend 9: Leadership in an Industry 4.0 world Article5 years ago

Trend 9: Leadership in an Industry 4.0 world Article5 years ago