Due to financial challenges, many oil, gas, and chemicals companies may need to rethink how they approach their portfolios. Based on our analysis of 500 companies across the sector, we found what worked in oil and gas did not necessarily work for chemical and specialty companies. While there were commonalities, the differences loomed large:

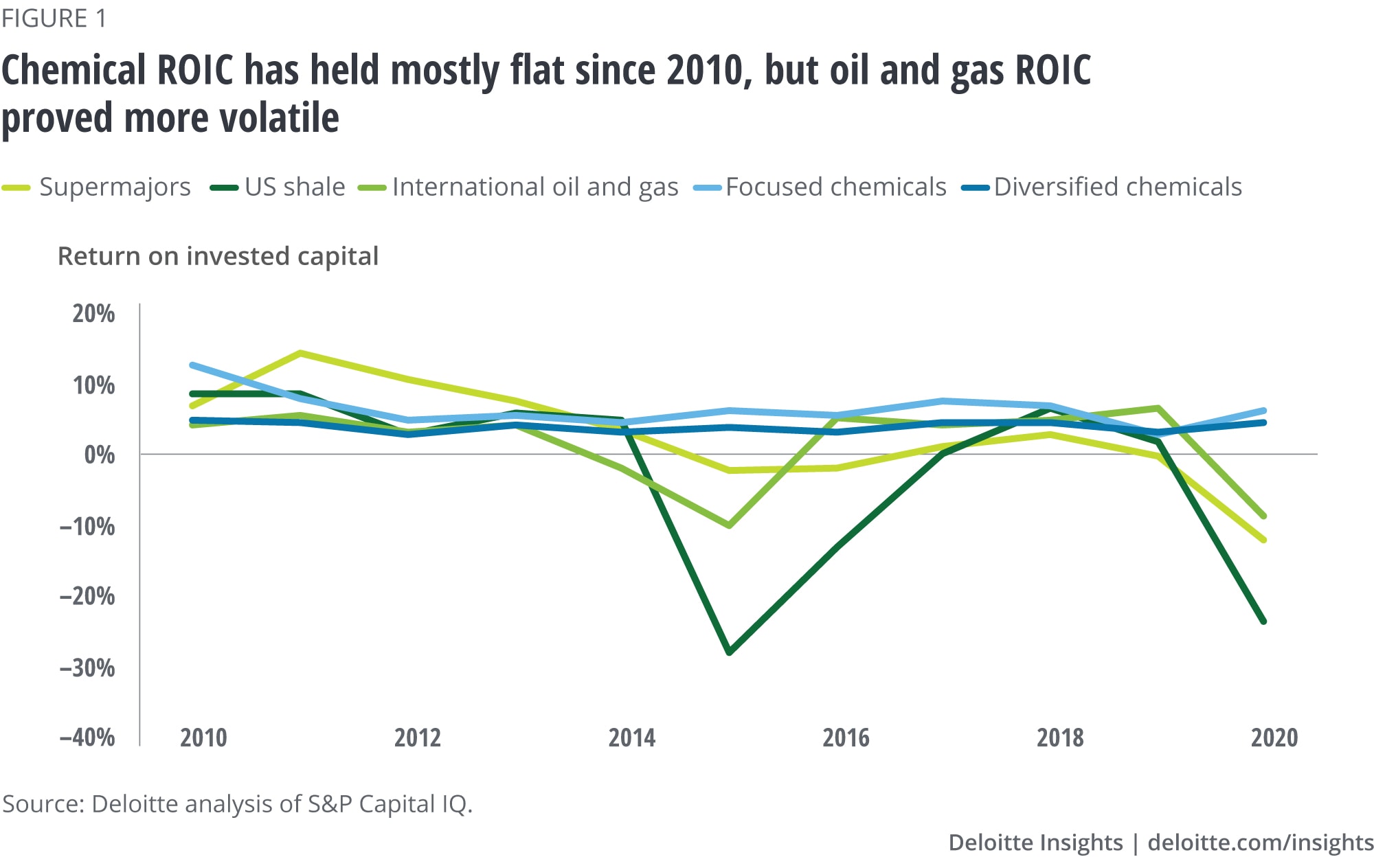

- Chemical and specialty materials companies that had a focused portfolio outperformed those that were more broadly diversified. That was not necessarily true for oil and gas. While larger, more integrated companies did not outperform the broader sector, neither did many smaller, more focused companies. For example, no shale-focused companies had top quartile financial performance.

- Being focused but agile proved beneficial for many chemical and specialty material companies. While diversified companies could benefit from multiple growth avenues, their complex portfolios often led to slower growth and higher costs. Those who effectively pivoted from one end market to another to pursue new opportunities outperformed their peers. The same was not true for oil and gas, where companies that shifted their portfolio strategy actually underperformed their peers on average, with only 16% of those companies having top-quartile performance.

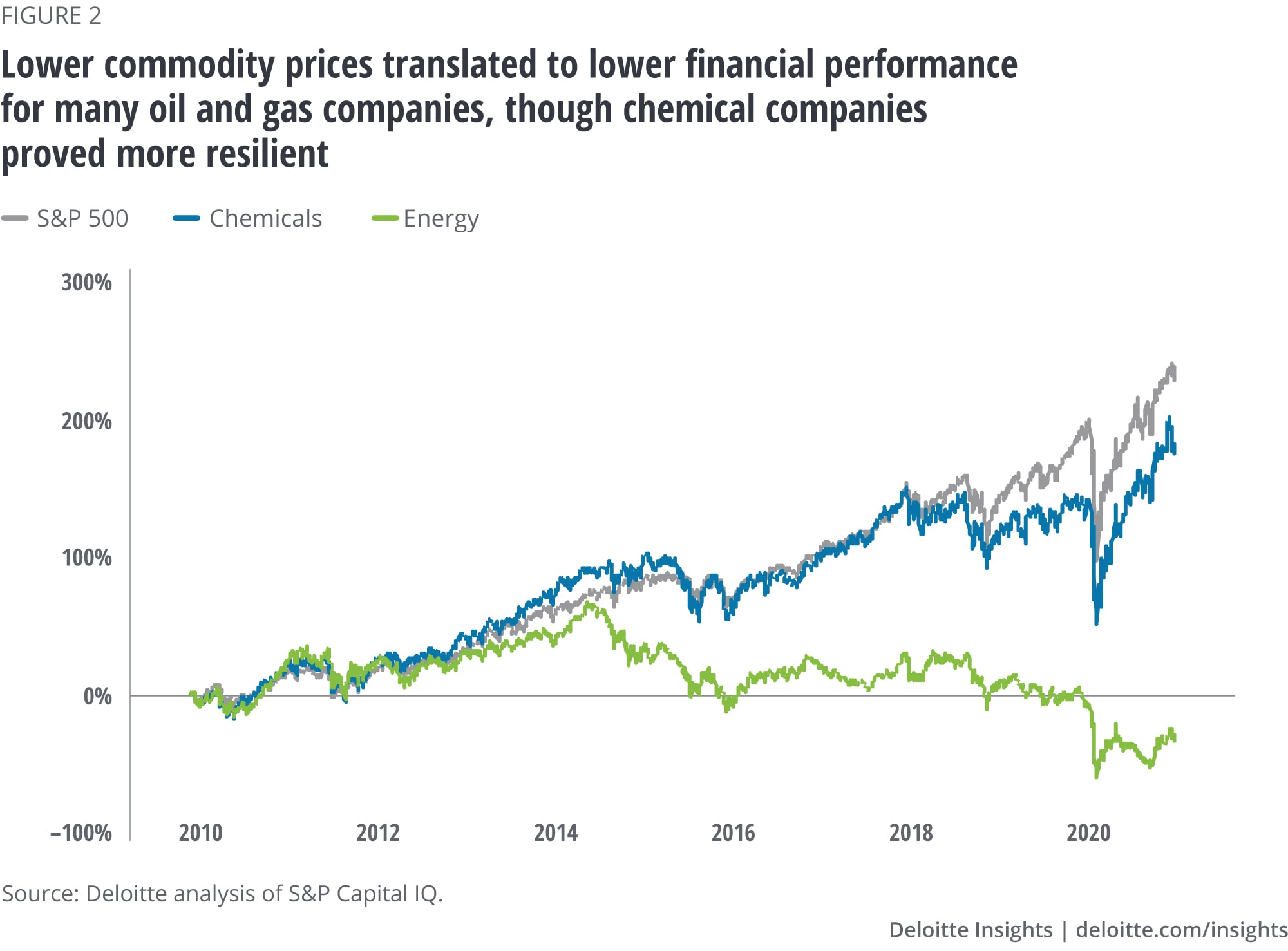

- Low cost did not consistently translate to better returns for chemical companies. Natural owners—chemical companies that have an advantaged feedstock position—generated shareholder returns almost 50% higher than other chemical companies. But their financial performance also proved much more volatile, with distinct underperformance during economic recessions.

- For oil and gas, however, access to low-cost sources of supply led to significantly better performance—80% of companies with larger conventional asset portfolios, which are typically much lower cost than shale or deepwater, had above-average financial performance. Only 5% were in the bottom quartile.

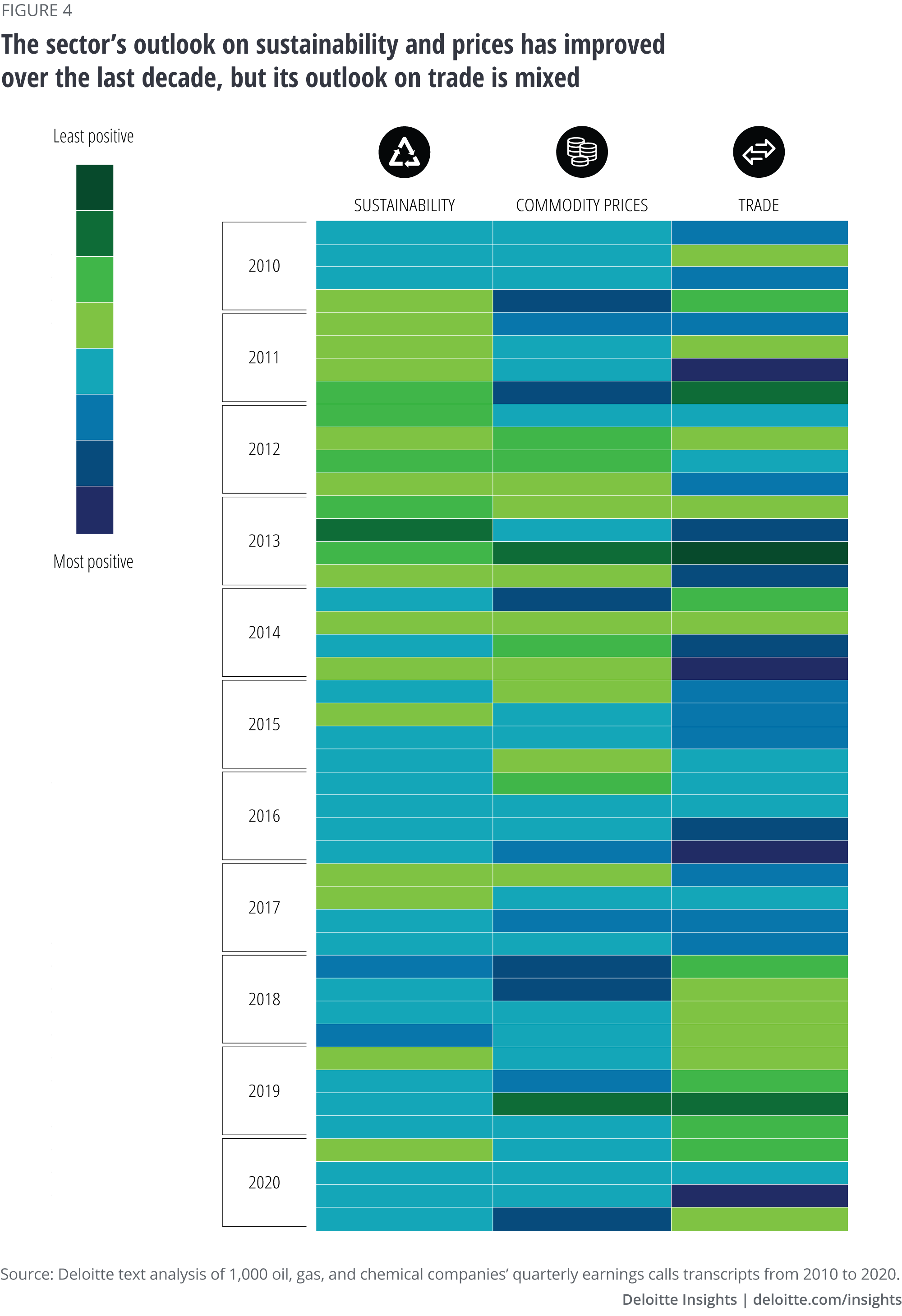

- Greener oil and gas companies tended to underperform their peers, with only 9% having top-quartile financial performance. However, that may change over the next decade as their lower-carbon investments mature. In the case of chemicals and specialty materials, companies with higher environmental, social, and governance (ESG) scores did not have meaningfully different performance than other companies. For oil and gas as well as chemicals and specialty materials, early investment in lower-environmental footprint assets, products, and services has not yet translated into better performance—though that may change as ESG investors more closely scrutinize companies’ emissions and expect faster performance improvements.

How to build a better portfolio

Oil and gas as well as chemical and specialty materials companies need to deliver a stronger growth story. Crafting a compelling narrative will likely require further honing of portfolios to improve financial performance and accelerate growth. That includes not just divesting noncore assets, but also investing in higher value-added opportunities. For chemical companies, that may mean drilling down into key end markets and products where technical and market know-how can be combined with economies of scale to drive margins higher. For many oil and gas companies, asset differentiation may prove more difficult, but lower-carbon technologies, such as carbon capture and renewable power generation, can complement their investments in more traditional fossil fuel projects, such as shale, liquefied natural gas, and refining.

While each company faces its own idiosyncratic challenges, taking a well-structured approach to optimization will be critical for many. Oil, gas, and chemical companies should focus on balancing the scope, scale, and growth opportunities. There can be tradeoffs between the three because as companies broaden their product and services portfolio and end markets they target, their ability to scale becomes increasingly difficult, and potentially costly. To balance those tradeoffs, each company must decide how its portfolio drives its overarching strategy.

Companies have already begun to adapt, with many rebalancing their portfolio to incorporate more future-focused assets to support a stronger growth narrative. However, as we found, neither bigger nor greener companies consistently delivered higher financial performance. The key is balancing future-focused portfolio opportunities and core-focused ones (figure 3). Investing in new areas requires a tradeoff, though, and increased scope may mean decreased scale. For example, more spending on renewable power generation could lead to reduced spending on, and increased divestments of, traditional oil and gas assets. Similarly, if a company invests in recycling or zero-waste products and services, it will likely need to reduce spending in other parts of its business. The success of the pace and degree of the shift from core- to future-oriented assets will depend on a company’s current market positioning and operational flexibility.

{kind=link}

{kind=link}

{kind=link}

{kind=link}