A ripe time for municipal gas and waste renewable natural gas partnerships

Strategic partnerships between public gas utilities and waste facilities could position renewable natural gas to play a crucial role in decarbonization and resiliency.

Jim Thomson

Daniel Bolgren

Kate Hardin

Carolyn Amon

The renewable natural gas landscape for public gas utilities

Renewable natural gas can potentially play a key role in public gas utility decarbonization efforts. It introduces circularity in the production of a fuel that can be used in existing gas pipeline and power plant infrastructure, natural gas vehicles, and thermal applications for commercial, residential, and industrial customers. The municipal owners of gas local distribution companies also own and run most of the country’s solid waste and wastewater facilities, which account for more than three-quarters of renewable natural gas feedstock by volume (73% and 4%, respectively).1 Renewable natural gas can support energy security and resiliency by increasing local control of supply in areas where municipal utilities both produce and utilize it. It can provide less carbon-intensive options, and in some cases carbon-negative options, to customers while supporting municipal decarbonization targets and improving local air quality. Renewable natural gas could also be key to utility compliance with emerging state-level clean heat standards. Monetization pathways at the federal level and various state levels for the sale of renewable natural gas to vehicle fleets are well-established, with new pathways in transportation and other sectors on the horizon.2

The renewable natural gas landscape for municipal wastewater treatment plants and landfills

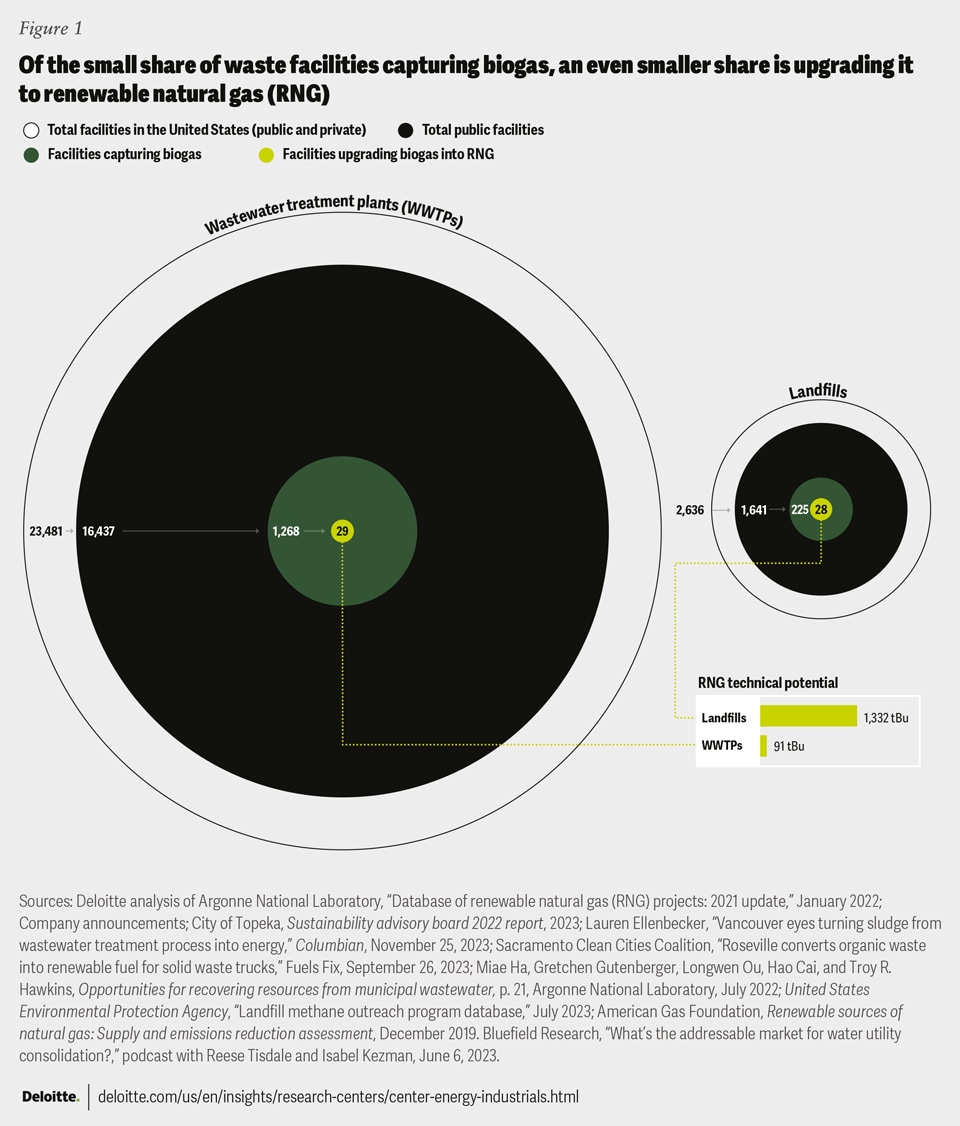

Waste from landfills and wastewater treatment is the third largest source of US methane emissions,3 which are still mostly uncaptured, unutilized, and unmonetized. Biogas capture for energy use instead of flaring creates value while decreasing emissions. Less than a tenth of the country’s municipal wastewater treatment plants currently capture biogas, and only 2% of these plants upgrade the captured biogas to renewable natural gas use (figure 1).

{kind=link}

Similarly, few landfills produce renewable natural gas relative to facilities capturing biogas. Of the 1,641 publicly owned municipal landfills in the United States, 225 capture biogas through anaerobic digestion, mostly for electricity generation.4 Only 28 produce renewable natural gas. Meanwhile, a third of privately owned landfills, which account for a third of all landfills, capture biogas, and 55 of these 283 landfills upgrade to renewable natural gas,5 suggesting significant untapped renewable natural gas production potential at municipal landfills.

Renewable natural gas production from waste plants flows to the natural gas vehicle market, mostly through pipeline injection.6 Ten renewable-natural-gas-producing wastewater plants and five renewable-natural-gas-producing landfills serve local demand, highlighting an opportunity to increase local usage through public gas utility support. For example, the utilities could fuel municipal natural gas bus and truck fleets, including refuse trucks collecting the waste feedstock for renewable natural gas production.

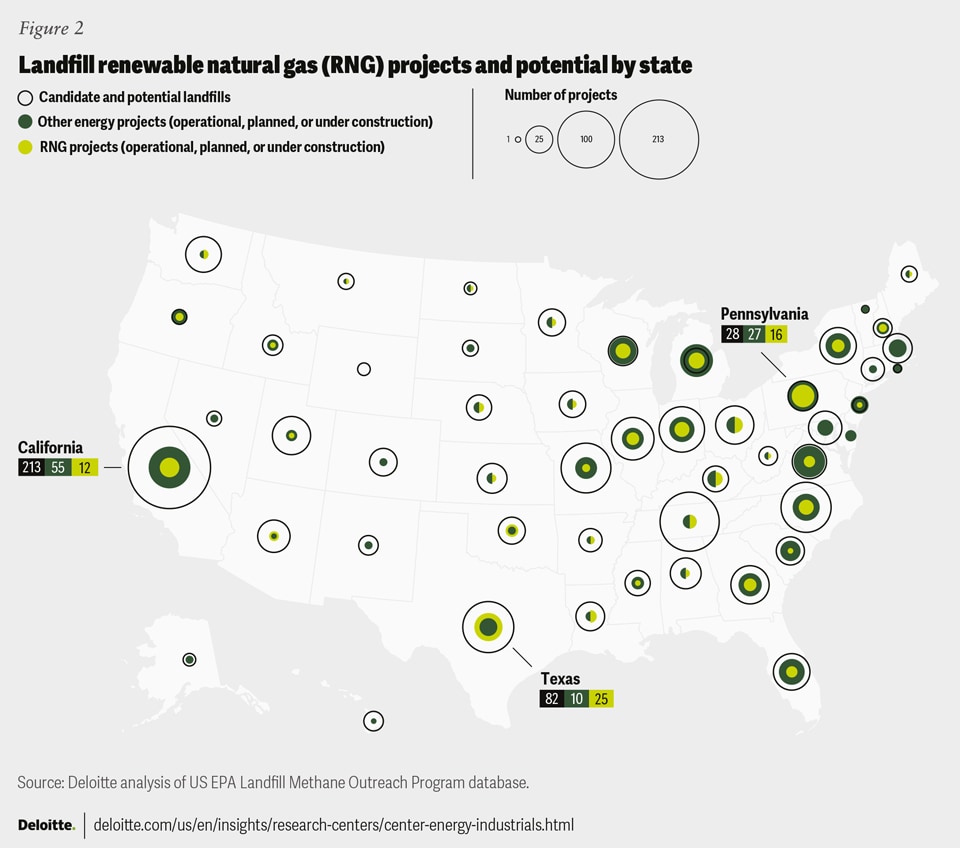

Most states have waste renewable natural gas projects, and all have opportunities to develop more. Wastewater reclamation facilities are producing renewable natural gas in a dozen states, while landfill renewable natural gas projects operate in half of the states.7 Projects currently planned and under construction are on track to double the number of landfill renewable natural gas projects across 37 states (figure 2). Landfills are capturing biogas for energy projects in all but one state. And 1,538 landfills countrywide range from having some potential for an energy project to being a strong candidate with a million tons of waste or more. Two-thirds of these landfills are publicly owned.8

{kind=link}

Potential market for renewable natural gas from waste

Given the current gap between biogas capture and renewable natural gas production, municipal gas utilities and waste facilities appear to have an opportunity to partner and catalyze the renewable natural gas market for municipal use.

A 2023 study found the country’s largest municipality, New York City, could replace up to 27% of the fossil gas it purchases with carbon-negative renewable natural gas produced from wastewater biogas co-digested with food waste—more than enough to power the city’s entire municipal heavy-duty truck fleet.9

Recent state-level studies have similarly found that municipal waste facilities could feasibly produce enough renewable natural gas to supply significant shares of gas demand. For example, a study for the Michigan Public Service Commission estimated the state’s wastewater treatment plants and landfills could feasibly produce enough renewable natural gas to replace 8% of fossil gas consumed in the state’s residential, commercial, industrial, and transportation sectors.10

At the national level, Deloitte estimates that renewable natural gas from waste could displace around 4.4% of current total US fossil gas demand, and 16.5% of core gas customer demand, and more than half the demand in the chemicals subsector—the industrial sector’s largest gas consumer— if all public and private landfills and wastewater plants captured biogas and upgraded to renewable natural gas production. If facilities with more feasible potential are considered, the yield would be closer to half these shares.11

Implementing new technologies at facilities could help accelerate this transition. Co-digestion of wastewater with food waste improves the nutrient balance and biogas yield from wastewater, enhancing renewable natural gas production.12 New York City is taking steps toward those implementations to meet climate goals. Its Newtown Creek Wastewater Facility and the Victor Valley Water Reclamation Authority are using co-digestion of solid and water waste to produce renewable natural gas while meeting state and municipal goals to divert solid waste from landfills.13

Tax policy impacts on project costs and returns

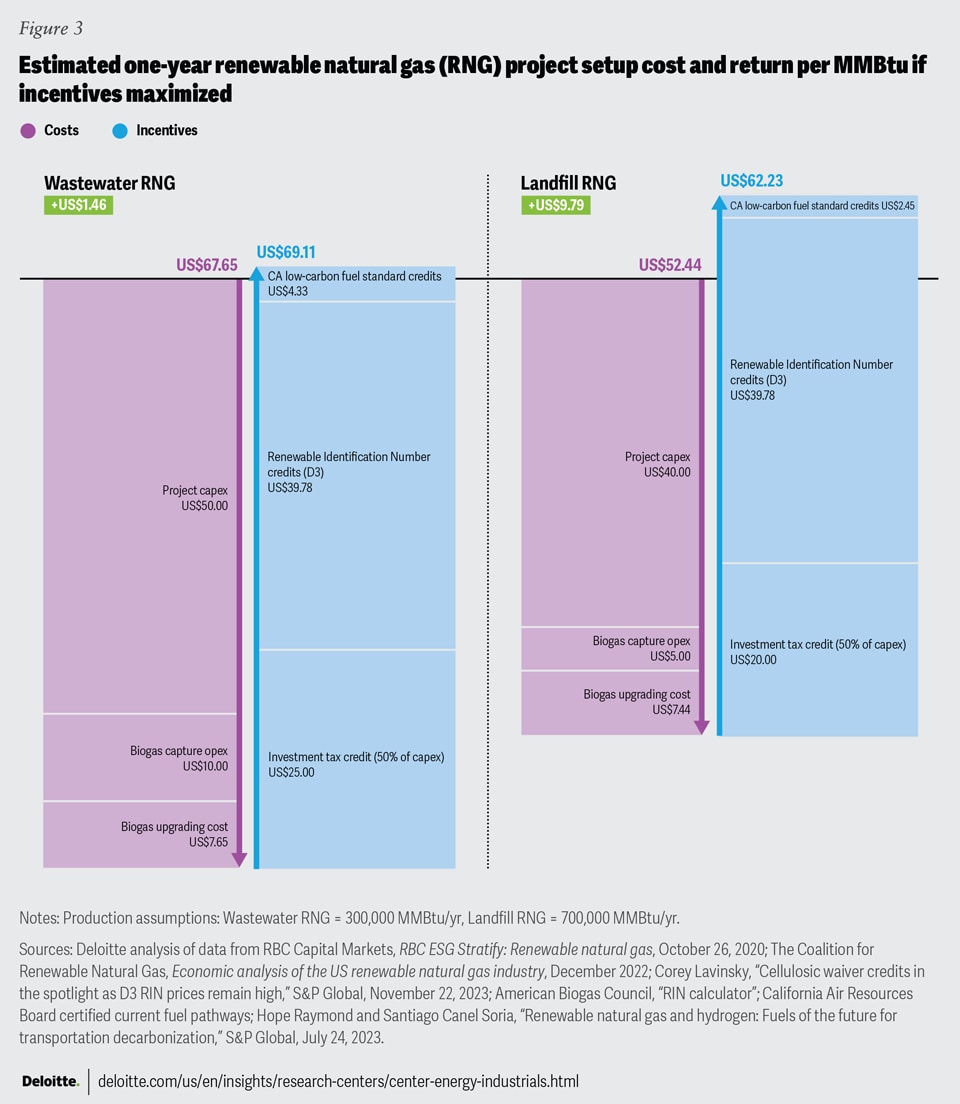

Renewable natural gas project costs can vary widely depending on the type of facility and size of project. Assuming average annual production of 300,000 MMBtu per year for wastewater treatment plants and 700,000 MMBtu per year for landfills, one-year renewable natural gas project costs are, respectively, US$42.65 per MMBtu and US$32.44 per MMBtu, including anaerobic digestion and upgrading equipment installation and operation (figure 2).

Municipal waste facilities without anaerobic digestion or biogas capturing equipment can capitalize on incentives to reduce costs, particularly at sites identified as ideal candidates for biogas projects. Inflation Reduction Act tax credits can cover up to 50% of the value of qualifying biogas property. Capturing the full credit requires meeting requirements on prevailing wages and apprenticeships (five times multiplier—increase from 6% to 30% Investment Tax Credit), domestic content (10% adder), and energy communities (10% adder). Only new facilities with a single owner currently qualify for the full credit, although the industry is pushing for final guidance to extend eligibility to projects adding gas upgrading equipment to existing energy property. Municipal owners of gas and waste facilities would qualify as single owners even if they rely on engineering, procurement, and construction partners to build and operate the plant, and on external entities to manage incentives.14 Qualifying biogas property must begin construction15 before December 31, 2024, which leaves a short window for municipal waste facilities to seize the opportunity. The Inflation Reduction Act has also enabled tax-exempt entities such as municipalities to receive direct reimbursement of capital costs under the Investment Tax Credit.

Beginning in 2025 through 2027, renewable natural gas may also qualify for the section 45Z clean fuel production tax credit if it is used in the transportation sector. The size of the credit depends on the fuel’s greenhouse gas emissions and whether producers meet prevailing wage and registered apprenticeship requirements. Assuming the latter is met, the credit ranges from US$0.20 per gallon of nonaviation fuel emitting 40 kilograms of CO2e per MMBtu to US$1 per gallon of zero-emission fuel.16

At current incentive prices,17 the one-year initial project return for wastewater treatment plants and landfill projects is estimated to be US$1.46 per MMBtu and US$9.79 per MMBtu, respectively. Selling the renewable natural gas at current spot market prices of US$29 per MMBtu18 can further raise returns. However, the order-of-magnitude gap between renewable natural gas and fossil gas spot prices limits the offtake market. Negotiation of longer-term, fixed-price offtake agreements offers a pathway to narrow the gap.

{kind=link}

Municipal waste and gas utility partnerships can help catalyze the market

With new incentives and technologies increasing efficiencies, public gas utilities may seize opportunities to partner with waste facilities in their respective municipalities to produce and distribute renewable natural gas into local distribution networks.

Potential market offtake

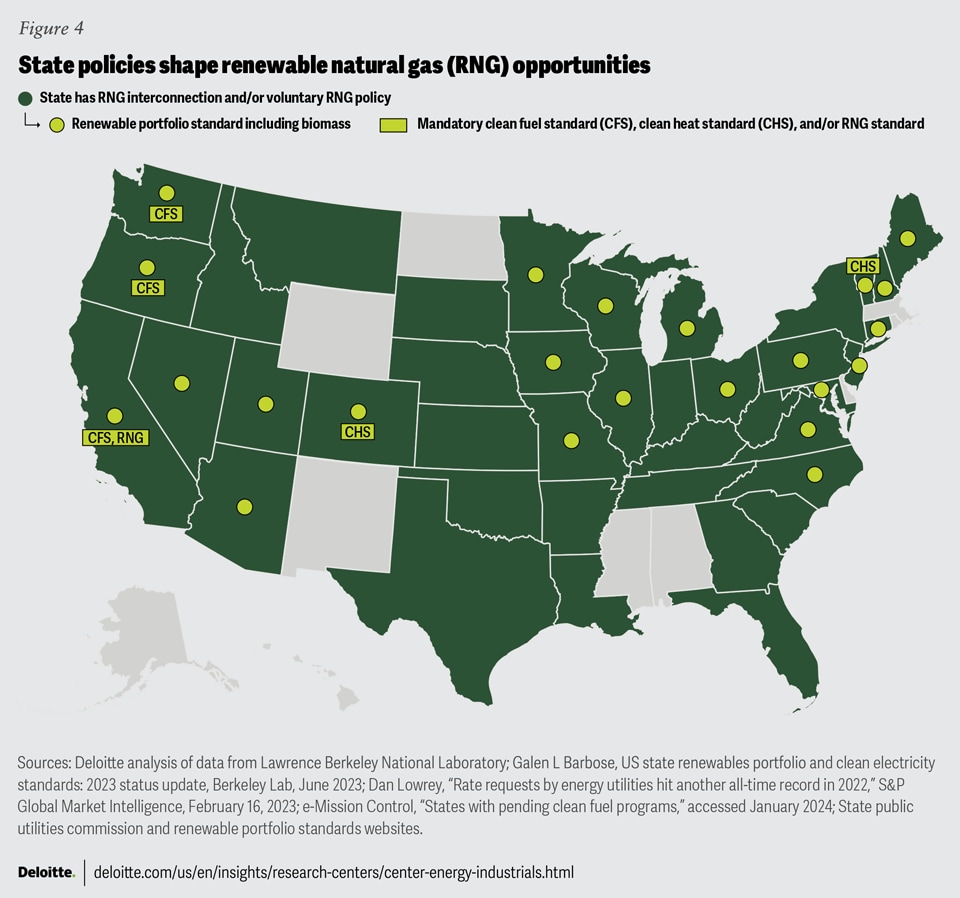

States, corporations, and utilities with decarbonization targets are fueling a growing voluntary market for renewable natural gas. Emissions from combustion of biogenic sources do not count toward an organization’s scope 1 emissions since they are considered part of the natural carbon cycle.19 State policies shape the extent to which utilities can serve this market. Forty states have an interconnection standard or tariff and/or a voluntary utility or residential renewable natural gas program facilitating renewable natural gas integration and delivery to customers via existing gas infrastructure and cost recovery mechanisms (figure 4). Half of these states have a renewable portfolio standard inclusive of biomass. Three have a renewable fuel standard driving renewable natural gas’ 98% penetration of gaseous fuels in the transportation sector in California, and 48% nationwide.20 Clean heat standards in two states could spur greater demand for renewable natural gas beyond transportation, as will the country’s first mandatory renewable natural gas standard established in California. The standard requires state utilities to procure renewable natural gas equivalent to 12% of core gas customer demand by 2030.21

{kind=link}

Revenue from renewable natural gas production credits

Renewable natural gas production can create several potential revenue streams for both public utilities and municipal waste facilities. Renewable natural gas can generate federal renewable energy credits under the Environmental Protection Agency’s Renewable Fuel Standard. The D3 category of renewable identification numbers are the most valuable and are created when renewable natural gas is used as a transportation fuel.22 The value of D3 renewable identification numbers reached US$39.78 per MMBtu of renewable natural gas at the end of 2023.23 The EPA’s latest rules more than doubled D3 cellulosic biofuel mandates for renewable natural gas from 0.63 billion gallons in 2022 to 1.38 billion gallons in 2025, boosting project development.24 The Western Virginia Water Authority and Roanoke Gas Company recently entered a partnership to create renewable natural gas for vehicle fuel use, and both parties share the revenue from the sale of generated renewable energy credits in spot markets.25

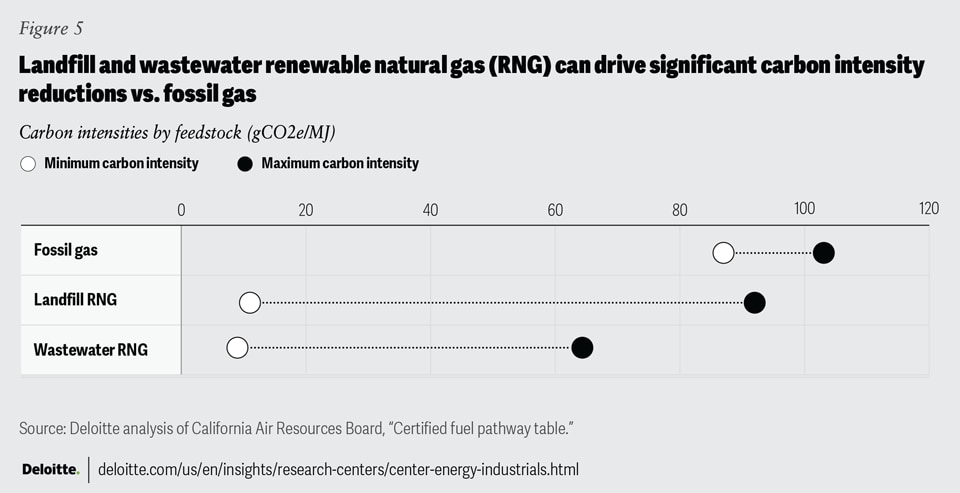

Another transportation compliance market option is to sell renewable natural gas into one of three state-level renewable fuel programs, the largest of which is California’s low carbon fuel standard (LCFS).26 Renewable natural gas producers in any state can sell into the LCFS markets, although California is considering an instate feedstock requirement.27 California’s LCFS credit values are based on feedstock carbon intensity (figure 5). Federal and state credits can be combined to help create optimal returns. LCFS credit values are estimated to average US$4.33 per MMBtu for wastewater treatment plant gas and US$2.45 per MMBtu for landfill gas.28

{kind=link}

Revenue from offtake agreements

Longer-term offtake agreements between municipal waste and gas facilities are another potential revenue stream. For example, Keystone Sanitary Landfill in Pennsylvania partnered with a large energy company to commission a renewable natural gas facility at the site, producing over 4 million MMBtu annually. Long-term offtake agreements were negotiated with several parties to sell 80% of the renewable natural gas production at the site over periods of up to 20 years each.29 While the producing landfill is privately owned, the opportunity is there for municipal bodies to partner and negotiate long-term offtake agreements that can help secure stable pricing for buyers and reliable, consistent revenue for producers.

In another example, the Richland Horn Rapids Landfill in Washington is converting raw biogas into renewable natural gas to be distributed by a regional investor-owned gas utility, with additional offtake negotiated with a specialty renewable natural gas distributor. The city of Richland will receive a US$6,000 monthly royalty while the system is operating,30 injecting dollars back into the local economy. Such agreements can provide another revenue stream for municipalities.

Emerging opportunities

Renewable natural gas opportunities are expanding. Recent Treasury guidance enables landfill renewable natural gas used in hydrogen production to qualify for Section 45V tax credits if it directly supplies hydrogen producers. Further study would be required for wastewater reclamation facilities’ renewable natural gas to qualify.31 Meanwhile, the EPA is mulling provisions enabling electricity derived from biogas or renewable natural gas to qualify for electric renewable identification numbers if used to power electric vehicles.32 The EPA also started releasing funding to replace and retrofit diesel vehicles with zero-emission and clean technologies, including renewable natural gas in the form of adsorbed natural gas, which requires relatively little capital investment in fueling infrastructure.33

With favorable federal tax credits expiring at the end of 2024, now could be the time for public gas utilities and municipal waste facilities to assess renewable natural gas opportunities. Areas to evaluate include potential partners, incentives, mandates, and offtakers. Projects could support municipal decarbonization, public health, and resilience goals.