Financing today, banking on tomorrow

The recent rise in US credit card debt may not be the warning signal headlines are making it out to be, but America’s debt culture does come with some risk

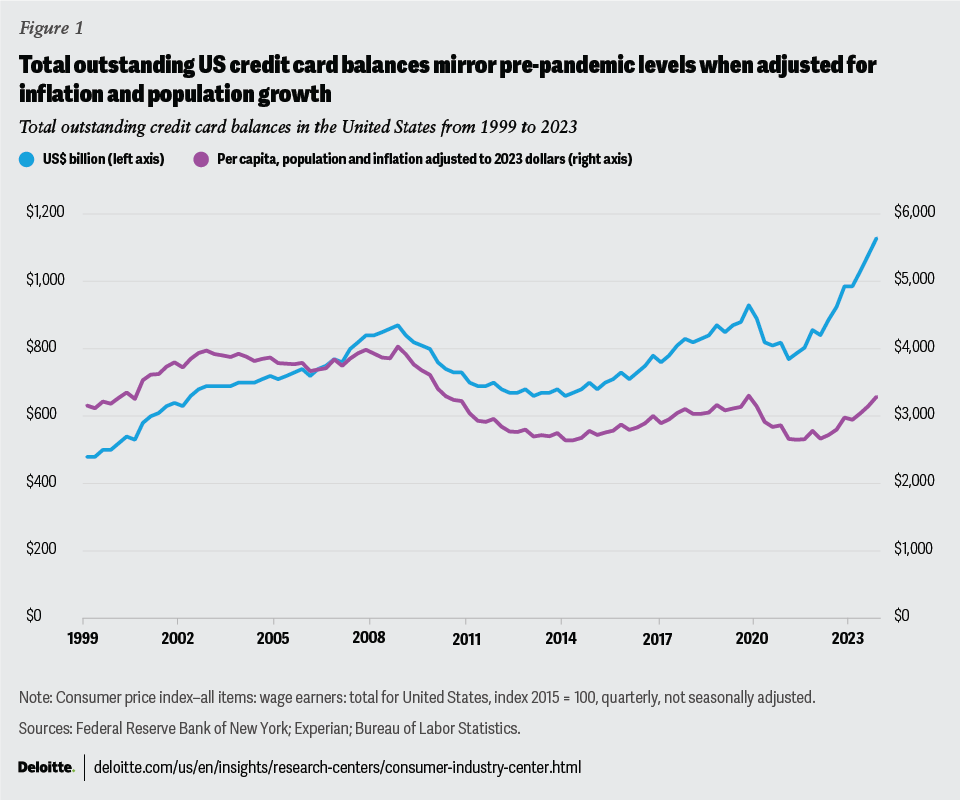

Credit card debt is getting much attention in the United States—and for good reason. Over the past three years, total outstanding balances spiked from US$770 billion to US$1.13 trillion (figure 1). According to the Federal Reserve, credit card delinquencies are rising above pre-pandemic levels, signaling some financial stress.1 Given recent inflation pressures, headlines continue to take record credit card debt as a telltale sign that more Americans are reaching the end of their financial rope.2

But is that the case for most credit card users? Some signs suggest financial hardship isn’t the key driver behind rising credit card balances.

Credit card debt is only at record levels in nominal dollar amounts. However, adjusting for inflation and the growth in the number of credit card users, outstanding credit card debt per capita is far from its peak in 2008, just before the Great Recession (figure 1). In 2023 dollars, credit card debt per capita more closely mirrors levels right before the pandemic.

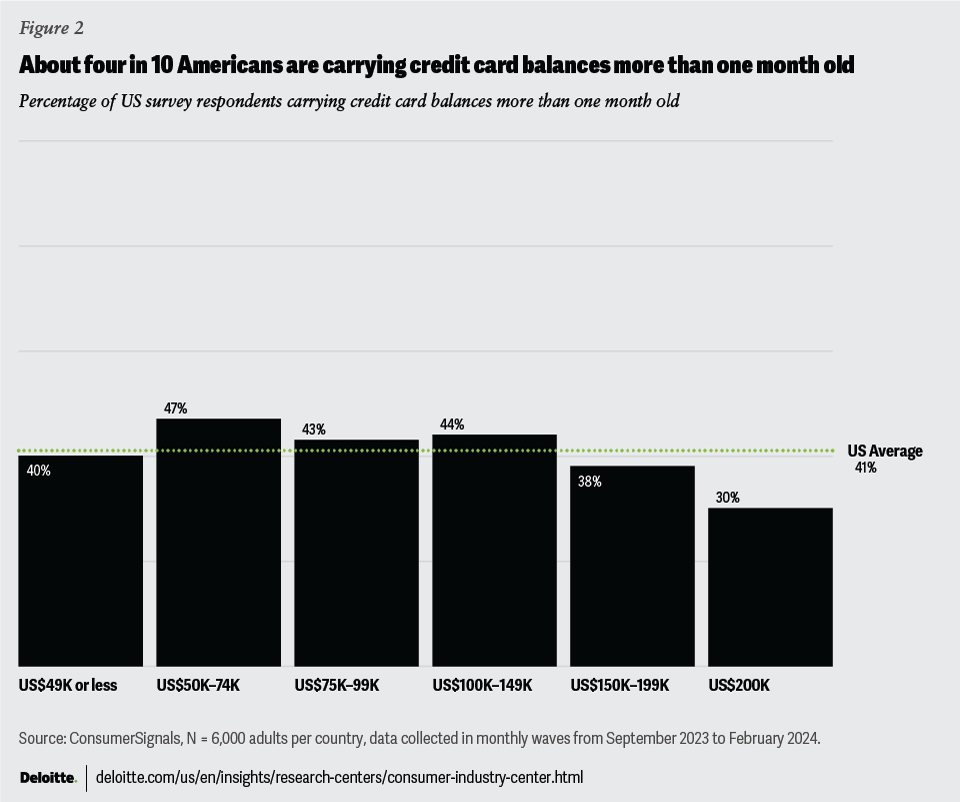

Demographically, if more Americans were leaning on credit card debt to stretch their paychecks, the behavior might be more prominent among lower- and middle-income Americans than higher earners. But there is little evidence of that trend. Roughly four in 10 Americans surveyed say they’re carrying revolving credit card debt (figure 2). And that figure is generally consistent across income bands, dipping only slightly among households earning US$200,000 or more annually.

More broadly, levels of immediate financial stress have been relatively stable in the United States. The percentage of Americans concerned about making upcoming payments is roughly one in five.3 Though this number could be better, it’s unchanged from four years ago.

The figure did jump to one in three during the summer of 2022 when peaking inflation rates sparked affordability concerns. But worries largely subsided once inflation rates began to ease, and over the past year and a half, Americans’ sense of financial well-being has generally plateaued. While financial sentiment hasn’t improved much, it hasn’t worsened either. It is worth noting that the US unemployment rate is still very low.

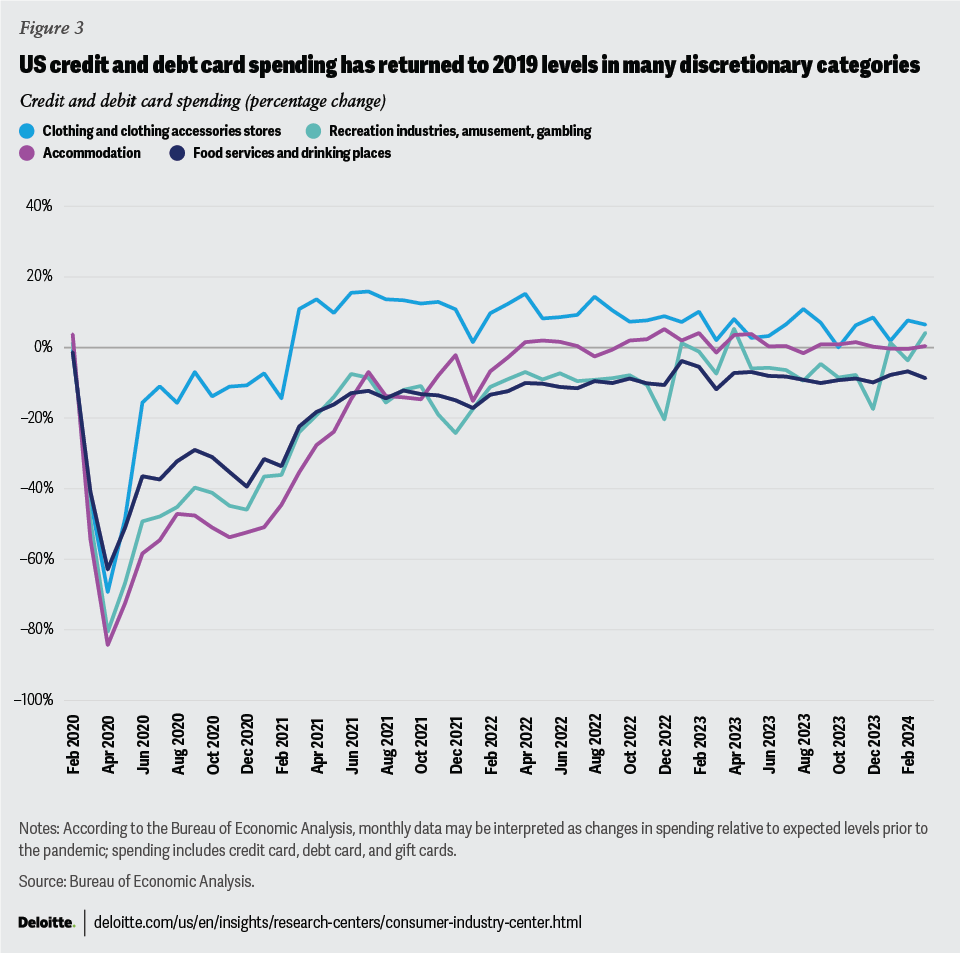

Finally, credit card transaction data signals spending confidence rather than financial strain. Even as Americans pay higher prices for essentials like housing and groceries, credit card spending data from the Bureau of Economic Analysis sits at pre-pandemic levels in major discretionary categories, including recreation, restaurants and drinking places, hotels, and clothing and accessories (figure 3). Of these categories, only restaurants lag slightly behind 2019 levels.4

Forces at play

Some of the attention around credit card debt isn’t just about the amount but the recent rate of climb in per capita credit card debt, which has increased by 18% over the past two years.5 And that type of jump hasn’t happened in two decades.

While that may look bad, there are reasons why this sudden jump might not be a dire warning signal.

It may be a potential pandemic bullwhip effect. Outstanding credit card balances fell throughout 2020 when pandemic lockdowns limited consumer spending avenues, and Americans’ savings rates hit a historical high.6 Pandemic lockdowns likely helped many Americans pay down their credit card debts. Once lockdowns eased, outstanding credit card balances quickly regained pre-pandemic equilibrium. And spending rushed back to sorely missed in-person categories like travel, recreation, and restaurants. In 2023, the Transportation Security Administration screened the most US flight passengers on record.7 The unique circumstances of the pandemic and the fact that these events happened within a short time make it different from previous periods and help explain the rate of climb.

Overall, consumer spending generally remains healthy,8 aided by a strong labor market.9 And that’s a solid nod to consumer resilience, particularly in the face of higher prices. The slowdown that some economists and business leaders have long anticipated has yet to materialize.10

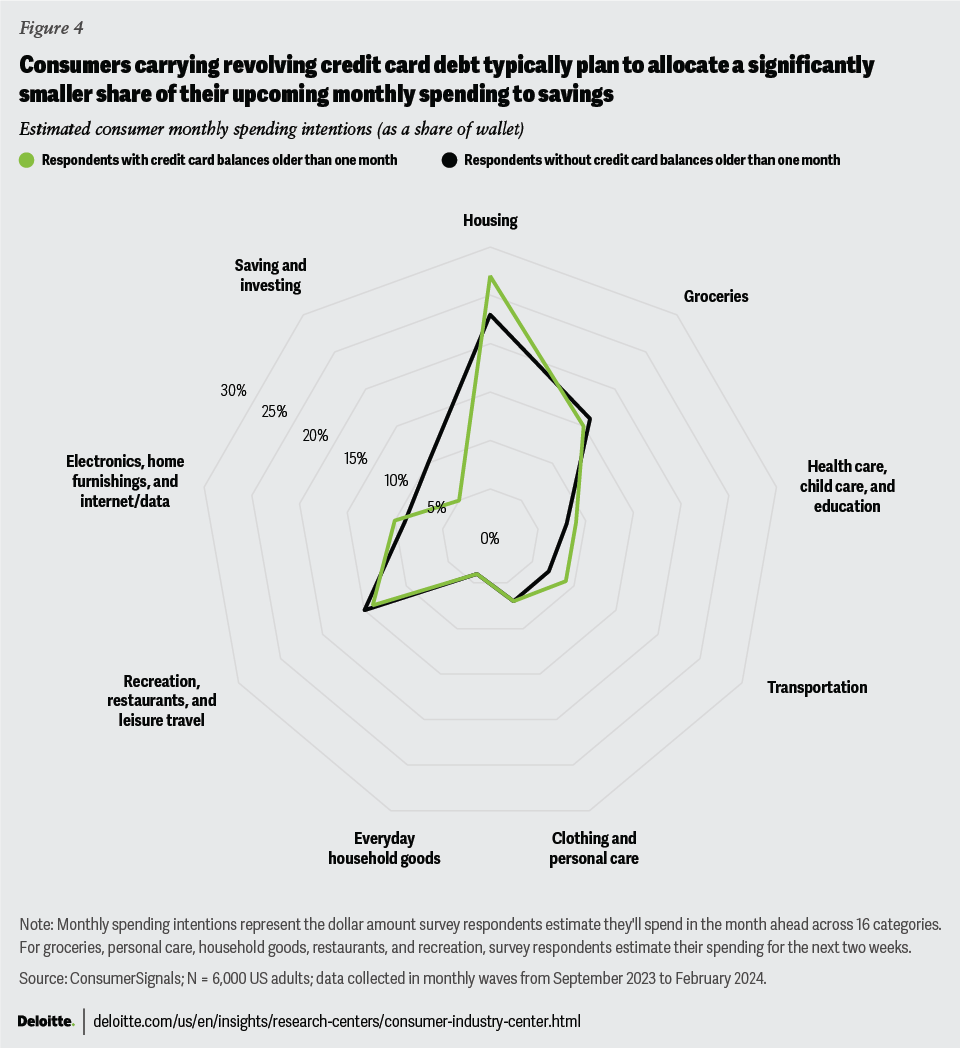

Consumer confidence is up compared to last year11 and signs of that confidence can even be found among Americans carrying credit card debt. Many might expect Americans with revolving, high-interest credit card debt to signal intentions to tighten their spending on the nice-to-haves. But that sentiment isn’t present in the data. In fact, from September 2023 through February 2024, Americans with revolving credit card debt planned to allocate the same share of their upcoming monthly budgets to categories like recreation, restaurants, leisure travel, and clothing, compared with Americans who weren’t carrying a balance (figure 4). And that trend holds for higher and lower earners.

So why is this spending sentiment important? It’s another sign that rising credit card debt doesn’t necessarily equate to dire times for consumers. Particularly, as Americans confront a world that has become 20% more expensive seemingly overnight,12 spending sentiment suggests many consumers are leaning on credit card debt for lifestyle continuity, not necessarily as a lifeline.

Banking on tomorrow—the good and the bad

Of course, America’s relationship with credit cards may reflect the broader consumption culture, the economic times, and the individuals’ unique contexts.

Some Americans have a greater level of comfort with credit card debt. Among the four in 10 Americans surveyed with revolving credit card debt, about half say they’re concerned about it.13 The other half say they aren’t or are indifferent.

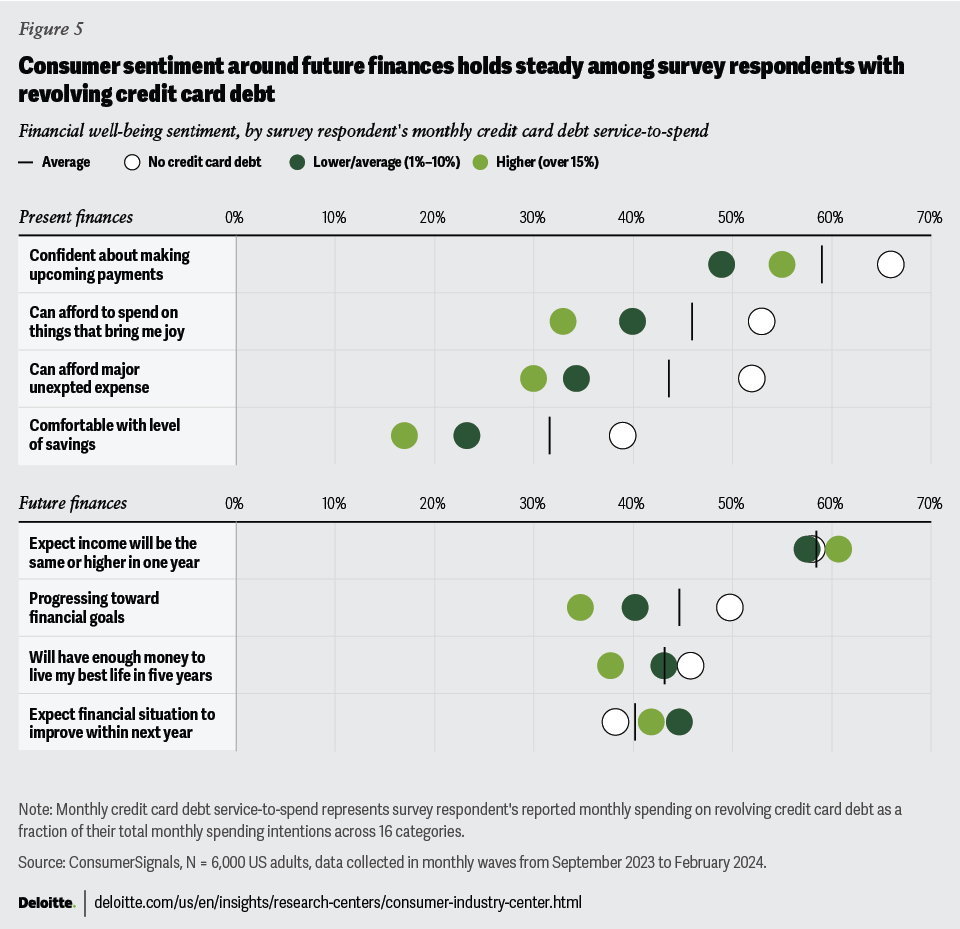

In a way, some of this comfort with debt is likely an extension of the spending confidence currently helping fuel the economy. Even in the face of higher prices and interest rates, many Americans with revolving credit card debt are spending and borrowing today because they feel pretty good about the future, despite feeling less financially secure in the present. Relative to many developed economies, more Americans expect their earnings to increase (or at least stay the same) in the year ahead (figure 5). Nearly half expect their finances to improve in the future (in both one-year and five-year time horizons). But most telling is that confidence in the future doesn’t erode among consumers with revolving credit card debt or even those spending above average on monthly debt payments (figure 5).

From this perspective, perhaps it isn’t so surprising that Americans are still spending and taking on more credit card debt. A population of consumers confident about their economic mobility may struggle to pare down their spending on vacations and restaurants just because life has become more expensive.

However, past recessions (and a pandemic) have exposed the longer-term risk to American spending behavior. Comfort with spending and debt when times are relatively good is likely an important factor in why many Americans may be ill-equipped to weather financial shocks. Based on the consumer intentions captured on our ConsumerSignals platform, consumers financing their spending habits with high-interest debt do not intend to save at the rate other consumers do (figure 4). It is the most significant difference between how they allocate their share of wallet versus those who do not carry a credit card balance, echoing the Federal Reserve’s observation that depleted savings correlate with higher credit card balances.14

So, while consumer companies (and the broader economy) will likely benefit from a stretch of healthy spending confidence, rising delinquencies and any potential future downturns will likely expose some consumers’ underlying financial fragility and take a toll on their financial well-being sentiment.

And how Americans feel about their finances is important. Financial well-being sentiment likely influences how consumers think about future spending—where they’ll spend and how much—even when controlling for important factors like income. When financial well-being improves, the average consumer budgets more for leisure travel, restaurants, recreation, electronics, home furnishings, and clothing. They plan to save more, which, in turn, contributes to their sense of financial well-being. Improvement in financial well-being also appears to significantly influence lower-income households as they spend on goods and services they may have avoided during leaner times. (Read our previously published article, “Living in inflation’s wake” to learn more.)

Therefore, it’s reasonable to expect when financial well-being weakens, non-essential services will likely see the lion’s share of the pullback in consumers’ incremental spending intentions and their ability to save is hampered. Obviously, if financial well-being weakens, many consumers are likely to forgo putting lifestyle continuity on credit and make more challenging budget choices.

A historic per capita view of credit card debt and a strong labor market suggest consumers still have room to run. That should be a comfort to many consumer companies and credit card issuers. However, just because consumers continue to put things on credit doesn’t make them any less mercurial (and possibly vulnerable). That’s why it’s worthwhile to keep an eye on their broader sense of financial well-being, and we suggest you do, too.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}