{kind=link}

Streaming services+tax: Rules shift rapidly across the United States has been saved

Thanks to Jeff Loucks, Brooke Auxier, Gautham Dutt, Rithu Thomas, and Shubham Oza for their help in producing this story.

Cover image by: Jaime Austin

Over the last five years, traditional and cable TV have posted steady declines in viewership.1 Where are audiences going? They’re cutting the cord in favor of streaming services.

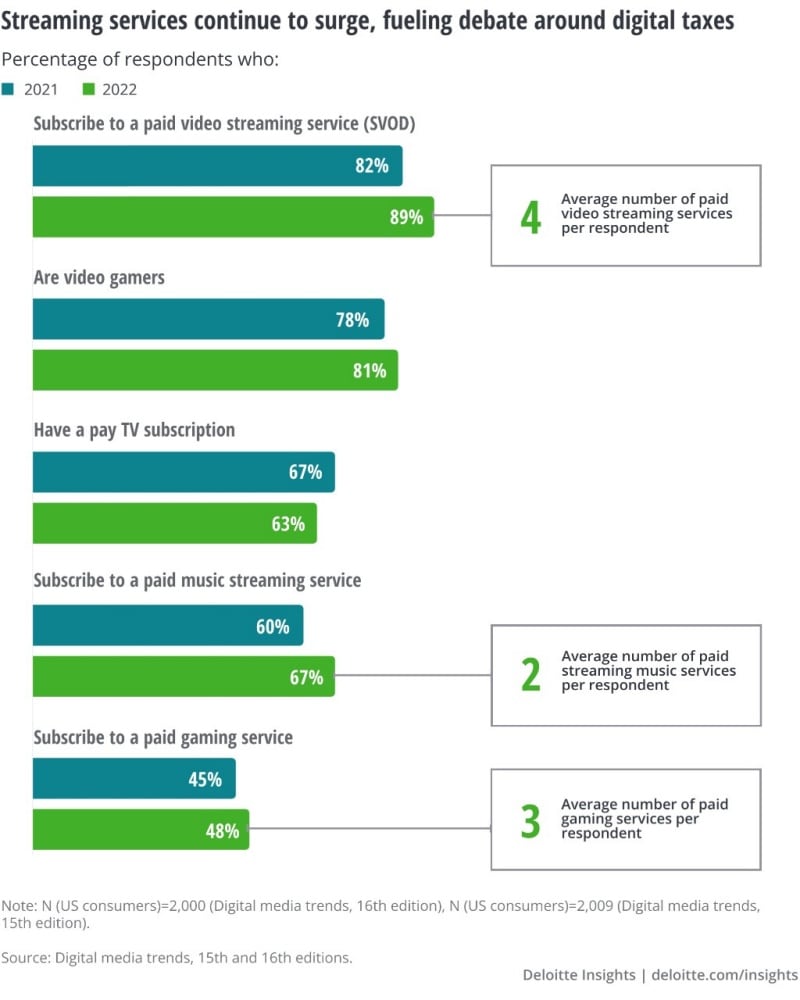

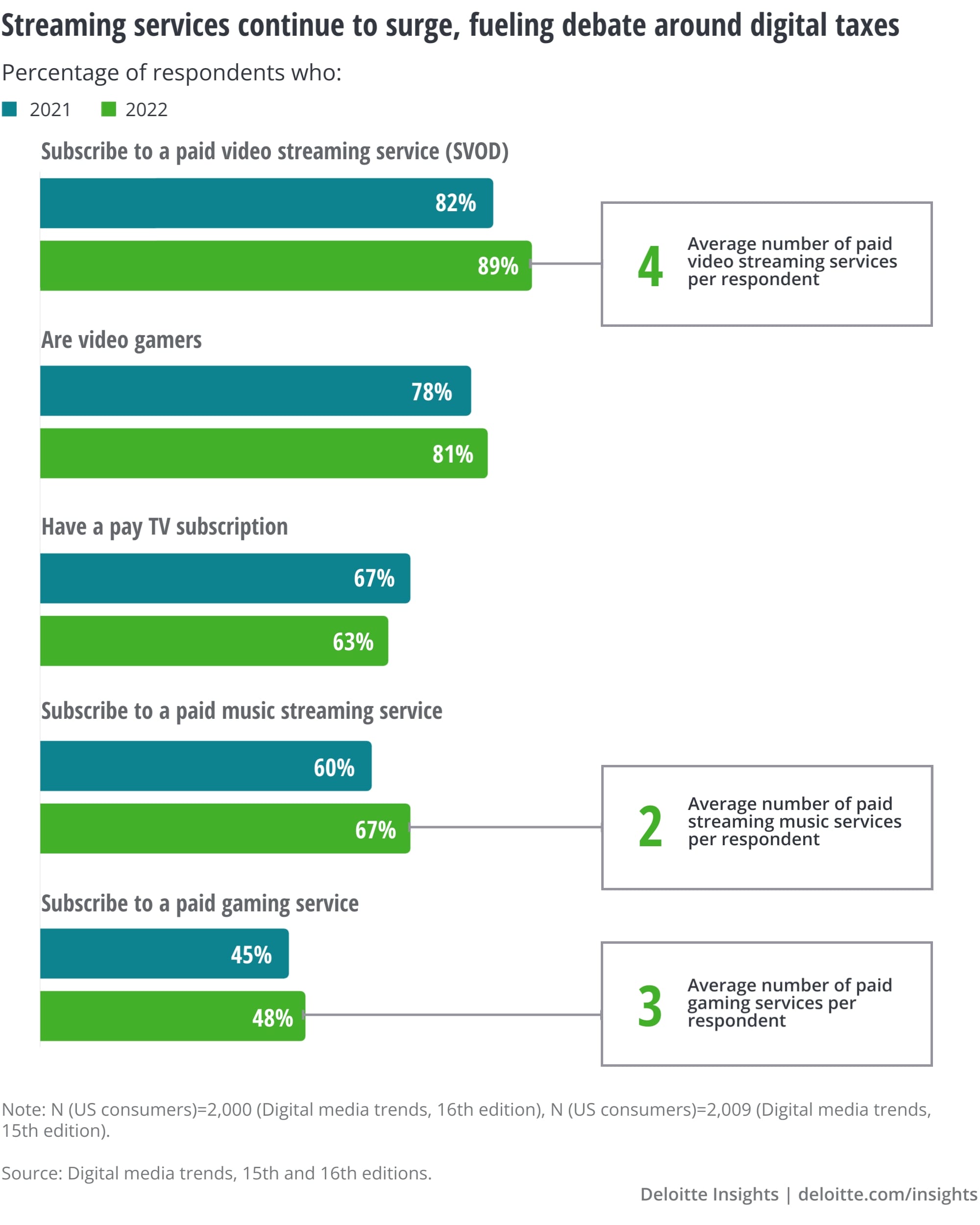

In Deloitte’s 2022 Digital media trends survey, use of subscription video-on-demand (SVOD) streaming services increased over last year from 82% to 89%, with the average respondent subscribing to four services (figure).2 The survey revealed increases in streaming music and gaming as well. Only pay TV showed a decrease, and the shift has many state and local governments scrambling to make up lost tax revenue.3

Some 33 states require streaming services to collect sales tax, but many states are struggling to recoup revenues from the gross receipts franchise fees—up to 5%—they collected from cable TV providers (who needed state land to lay cable). Some cities have banded together in class-action lawsuits to require streaming services to pony up that 5%, but in states like Arkansas, California, and Texas, the major streaming providers have argued successfully that they don’t use municipal resources.4

Some state and local governments have found novel ways to tax streaming services. Florida applies a communications tax on streaming, Kentucky applies a special video tax, while the City of Chicago applies an amusement tax originally designed for concerts and sporting events.5

Bundling adds another wrinkle to the calculation. According to the Digital media trends survey, more than half of respondents secured “free” streaming subscriptions as part of their home internet or mobile subscriptions.In New York, for example, streaming video is exempt from sales tax, but streaming video games are not, so some streaming services began applying state sales tax in late 2021.6 Now providers and bundlers have to monitor the features in every service package and figure out the tax impact.

Yet another complication arises when users engage in password-sharing. In an earlier Deloitte survey, 22% of consumers overall (and 31% of Gen Z) admitted to sharing their streaming video service logins to save money.7 If a subscriber in New York shares a password with someone in Chicago, for example, which regime’s rules apply? Generally, providers are expected to designate the customer’s billing address as the taxable location. Although updated guidance for digital goods has been requested by the industry and proposed in Congress,8 these bills have not advanced thus far. Until Congress provides more clarity, confusion regarding the proper sourcing of customer charges is likely to linger.

Streaming across national borders brings a host of additional challenges. In Europe, many countries have implemented a digital service tax (DST), which, among other digital activities, taxes gross revenues derived from online placement of targeted advertising. DSTs have also been implemented in Africa, Asia, and Latin America. In a few jurisdictions, these DSTs may be applied to revenues from streaming services as well.9

The result is a massive amount of complexity, where streaming services may be hit with numerous new tax requirements in the coming years.