Updates: Past TMT Predictions’ greatest hits and (near) misses

TMT Predictions revisits previous predictions on enterprise edge computing, 5G telecom, women’s sports, quantum-resistant encryption, and the geopolitics of open-source semiconductors

Duncan Stewart

Karthik Ramachandran

Prashant Raman

Jennifer Haskel

Ariane Bucaille

New for 2025 is our series of shorter articles on topics we’ve covered in previous editions. Sneak peek: We did well with past predictions, but nobody bats 1.000. Read on to hear what’s new with these oldies:

- Generative AI comes to the enterprise edge: ‘On-prem AI’ is alive and well

- (Re)defining the investment case for women’s sports

- Fixed wireless access: Contrary to popular opinion, adoption may continue to grow

- 5G standalone appears to be at a standstill: Will 6G run late?

- Open RAN mobile networks and vendor choice: Single vendor now, multivendor when?

- Despite quantum’s slow start, don’t be slow to start your defense with post-quantum cryptography

- RISC-V: Closing the geopolitical gen AI loophole

Generative AI comes to the enterprise edge: ‘On-prem AI’ is alive and well

Owning their own servers gives companies a more private, secure, flexible, and possibly cheaper IT environment for AI

Duncan Stewart, Karthik Ramachandran, Gillian Crossan, and Jeff Loucks

Deloitte predicts that in 2025, although generative AI via the cloud will continue to be a dominant option, about half of the enterprises worldwide will add AI data center infrastructure on-premises (on-prem)—an example of enterprise edge computing. This could be, in part, to help protect their intellectual property and sensitive data and comply with data sovereignty or other regulations, but also to help them save money. This is a continuation of what we observed in late 2024: About 45% of one source of gen AI chips was going to the hyperscalers, while 55% were from a mix of consumer, internet, and enterprise players.1 According to our 2024 State of Generative AI in the Enterprise Q2 report, 80% of companies with very high AI expertise report spending more on AI in the cloud. However, 61% are investing more in their own hardware.2 We predict enterprise on-prem AI servers could approach a US$100 billion market in 2025.3

The 2021 and 2023 editions of TMT Predictions discussed how enterprises were expected to invest in edge AI solutions to perform and run computational tasks faster.4 Latency (the time it takes for an AI to see an input and get a response back) was a key driver of earlier enterprise edge applications.5 Latency does not seem to be a significant driver this time around: Most gen AI requests take thousands of milliseconds to process, so turnaround time isn’t usually a challenge.6

Instead, the demand for private, sovereign, and secure gen AI is now driving enterprise edge to an altogether new wave of growth.

As enterprises scale their investments and efforts in gen AI,7 the cloud providers, hyperscalers, telecom companies, and AI and tech companies are building out data centers to help meet the demand surge and are expected to spend over US$200 billion in chips and data centers in 2025.8 But many global enterprises seem to be adopting a hybrid approach: using both third-party cloud solutions and investing in hardware to do some portion of the training and inference on their own premises, which may provide a more secure, controlled, sovereign, and a flexible IT environment.9 Processing data locally versus relying on an external cloud infrastructure can enable enterprises to accelerate response times and address privacy and security issues with regard to gen AI implementations—which Deloitte uncovered in the State of Generative AI in the Enterprise Q3 report.10

A variety of enterprise use cases and opportunities make gen AI at the edge viable and relevant. For example, banks and financial services companies often prefer to keep their volumes of sensitive data on-premises to address data security concerns and have better control of gen AI models.11 Media and entertainment companies are already using natural language AI-infused solutions to spur creativity in the fields of animation and content creation (for example, writing first draft scripts or prose), gaming, and entertainment (for example, using patterns in movies’ subtitle content to enhance recommendation engines for end users).12

What does the enterprise edge look like for gen AI in 2025? Some portion of enterprise spending for on-prem gen AI will be toward devices such as employee smartphones and PCs that increasingly are expected to have specialized gen AI chips on them.13 But there are other options, and they have implications for how much enterprises might spend for on-prem solutions, as well as adaptations they might need to make in their data closets or data centers, as the new versions tend to use more power, are physically bigger, and sometimes require liquid cooling, which is a relatively new solution.

In 2024, many enterprises had a gen AI box (there were many possible options and vendors) that was about the size of a home printer, weighed about 300 pounds, consumed roughly 10 kW, cost just under US$500,000, and was capable of approximately 30 PetaFLOPS in processing power.14 In 2025, some companies will likely buy similar boxes, but some will buy larger and more powerful boxes—larger than a (big) refrigerator, weighing over 3,000 pounds, drawing 160 kW and needing liquid cooling, costing more than US$3 million, and over 1.3 ExaFLOPS.15

To be clear, enterprises are not building these machines themselves. Both gen AI chipmakers and multiple-server original equipment manufacturers are offering these rack-scale servers and will install them on-prem.

Non-AI on-prem computing can often be cheaper than

cloud, and there’s no reason to expect gen AI computing to be different over

time.

Spending US$3 million on an exascale gen AI supercomputer may seem like a lot of money in one way, but it may not be. Large enterprises across all industries could have IT budgets in the billions of dollars. Training large language models can cost from US$1 million to US$100 million.16 And cloud gen AI computing power, whether for training or inference, is hardly free.

It’s unlikely that an enterprise would solely use an on-prem gen AI solution. It’s likely that many will use the cloud at least some of the time. Further, it’s likely that cloud could be the bigger portion of total AI computing. As is often common in IT architectures, hybrid is likely the ultimate outcome: On-prem may offer benefits around security, latency, resilience, and privacy, while cloud may offer benefits around choice, flexibility, scalability, and experimentation.

But for those who want to own their own hardware, does it make financial sense to buy an on-prem AI solution from a return-on-investment perspective? It might: Non-AI on-prem computing can often be cheaper than cloud,17 and there’s no reason to expect gen AI computing to be different over time. Even if the “hard” ROI is not there, the advantages around ownership of IP, privacy, security, and resilience may make on-prem worth it. Moreover, new types of training and inference techniques like split learning and split inference can distribute gen AI workloads across edge devices, optimizing computational needs and reducing latency, as well as addressing privacy and security issues.18

Bottom line

Some companies may believe that although they have no short-term need for on-prem gen AI computing, over the long term, on-prem may be inevitable. In that case, the time and money they spend now in learning how to best use on-prem processing as part of a hybrid cloud and on-prem approach could justify the cost of the hardware.

One question concerns the possibility of a gen AI bubble. With many players investing in hardware at the same time, with a view that underinvesting may be a bigger risk than overinvesting, it’s possible that there will be significant overcapacity, at least in the short term. If that happens, what would enterprise companies that have invested in on-prem gen AI servers do? It seems more likely that they would use their own hardware (which is already paid for and being depreciated), rather than spend on cloud gen AI computing.

Most of the prediction is anchored on how, for example, a major company might have its own on-prem gen AI IT infrastructure to run a part of its processes and operations (banks, auto manufacturers, health care companies, public sector agencies, and so on). That’s what we (mainly) mean by edge. But there is an additional market, which some consider to also be edge: the telco edge. As we wrote in September, over 15 telecom companies globally have announced that they are building gen AI data centers, some with capacity they’ll use for their own needs, but some of which they’re aiming to sell to enterprises: gen AI as a service.19 Therefore, enterprises could (1) buy from cloud providers, (2) have on-prem hardware, or (3) buy from a gen-AI-as-a-service provider.

Finally, there is the question of sustainability and the inherent trade-offs. An enterprise edge gen AI server is the same in many ways as a box in a hyperscaler’s data center. But having a thousand servers in a thousand enterprises can spread out the electrical load and could put less stress on the electrical grid than deploying a thousand (or ten thousand) servers in a single building.20 On the other hand, the companies that run hyperscale data centers tend to be more efficient in running them with power usage effectiveness (PUEs) of 1.2 or 1.3 (and they tend to be able to buy low-carbon energy at scale, which may be harder for a smaller enterprise to access21). Meanwhile, the average enterprise data centers’ PUE ranges from 1.67 to 1.8, suggesting that a thousand different gen AI boxes in a thousand different enterprises could have a larger carbon footprint than the same number in a hyperscaler data center.22

(Re)defining the investment case for women’s sport

Rising women’s sports revenue fuels investor interest and valuation records

Jennifer Haskel, Pete Giorgio, and Amy Clarke

The increasing professionalization and commercialization of women’s sports around the world is garnering the attention of fans, sponsors, and—importantly—investors. In last year’s edition of this report, Deloitte predicted the women’s elite sports market would generate over US$1 billion in revenue in 2024, a rise of more than 300% on the previous valuation of revenue earned in 2021.23

This growth in revenue has led to record valuations and a rise in the scale of capital flowing into the sector,24 which has helped increase the visibility, regulation standards, and sponsorship innovation in elite25 women’s sports.

In 2025, we expect to see an expanding group of investors—including institutional investors, private equity, and high-net-worth individuals—take note.

In Deloitte UK’s report, Future of Sport 2024: Seizing the moment, 65% of global sports leaders surveyed pointed to women’s sports as the largest growth opportunity in the sector. Women’s sports are rapidly evolving, garnering more attention, viewership, revenue, and investment than we had initially predicted.26

And while future growth is expected, it is not a given.

Rising valuations influenced by structural setups

North American sports leagues, including the Women’s National Basketball Association (WNBA) and National Women’s Soccer League (NWSL), are setting a high bar for franchise valuations.

In 2024, the “Caitlin Clark Effect” swept through the WNBA, attracting new fans and sponsors to the league.27 Following growth in viewership, app downloads, and engagement, the WNBA reportedly agreed to a US$2.2 billion new media rights deal—more than triple the previous agreement.28

As visibility increases and more fans engage with the league, some investors are capitalizing on the growth opportunity. In August 2024, the Dallas Wings lingered at the bottom of the league record but were valued at US$208 million after two investors bought a 1% stake in the team at US$2.08 million.29 Prior to this deal, the Las Vegas Aces held the crown for most valuable franchise with a US$140 million valuation.30 The Aces were bought by Mark Davis in 2021 for US$2 million, and after investing heavily into the franchise, including a US$40 million investment into a team-specific practice facility, his team may now be worth more than 70 times what he paid to acquire it.31 Part of this supporting investment thesis is a belief in the continued growth of WNBA fandom, with tailwinds looking favorable. The Golden State Valkyries, an expansion team slated to start play in 2025, have already sold a record 17,000 season ticket deposits, proving that demand is expected to continue into the foreseeable future.32

In September 2024, the WNBA announced an additional expansion franchise in Portland, Oregon, which will start play in the league in 2026.33 The team will be owned and operated by Raj Sports, and led by Lisa Bhathal Merage and Alex Bhathal, who also own the Portland Thorns of the NWSL.34 The group paid US$125 million for the franchise, a steep increase from the US$50 million paid for the Golden State and Toronto franchises entering play in 2026.35

As visibility increases and more fans engage with the league, some investors are capitalizing on the growth opportunity.

In the NWSL, clubs are experiencing the benefits of a new broadcast deal as well. The league agreed to a new four-year media rights deal beginning in 2024 with broadcasters ESPN, CBS, Amazon Prime Sports, and Scripps’ ION Network, worth a reported US$60 million annually (US$240 million total).36 This deal represents an increase from the previous cycle, a three-year agreement with CBS worth US$4.5 million total.37

Fueling this growth may be the increased levels of sponsorship and sophisticated investment across the league. In 2024, multiple clubs changed hands, with valuations increasing throughout the year. In June, private equity firm Carlyle, in conjunction with the ownership group of Seattle Sounders FC, completed the purchase of NWSL club Seattle Reign for a reported US$58 million.38 The previous ownership, OL Groupe, paid approximately US$3.5 million when it acquired the club in 2019.39 In July, Willow Bay, dean at the University of Southern California, and her husband Bob Iger, CEO of Disney, were announced as the new controlling owners of Angel City FC following an investment deal that valued the club at US$250 million, the highest valuation ever for a women’s professional sports team.40 Angel City FC reportedly paid an expansion fee of US$2 million when it joined the NWSL in 2022.41

European women’s soccer has grown over the past few years. Revenues across some of Europe’s top clubs increased 61% in the 2022–23 season compared to the prior season.42 The opportunity to invest into standalone women’s soccer entities is often rare across Europe, with the current combined structure limiting focused investment into the women’s side as prospective investors would need to invest through a men’s team.43

However, some investors are challenging the status quo by investing in some of Europe’s elite women’s teams. In 2024, Michele Kang completed her acquisition of a 52.9% stake in eight-time UEFA Women’s Champions League winners, Olympique Lyonnais Féminin.44 In this groundbreaking transaction, Kang agreed to a 50-year licensing fee for use of the Olympique Lyonnais intellectual property (IP) and branding.45 The acquisition adds to Kang’s already growing multiclub ownership model across global soccer, having acquired the NWSL’s Washington Spirit in 2022 and one of the few standalone English women’s clubs, London City Lionesses, in 2023.46

In the English Women’s Super League (WSL), Chelsea Women also announced a new strategic growth plan that would see the team repositioned to sit alongside, rather than beneath, the men’s side in the club’s overall business structure.47 This can allow for capital investment directly into the women’s side, as opposed to investing through a men’s team, and it’s possible that other affiliated women’s sides could follow suit to allow for direct investment channels.

Bottom line

Women’s sports are expected to continue their growth trajectory into 2025. Last year, a handful of bold organizations and investors made moves across the market. More stakeholders may need to follow suit, to help capitalize on the opportunity and push the market past one-off examples of investment. Select women’s sport properties have been traded at higher valuation multiples than is typically seen across the broader industry, but as revenue grows, these multiples are likely to decrease in future transactions. In the next year, more rights holders could evaluate their investment structures, as market appetite is expected to grow in line with accelerated revenues and fan engagement.

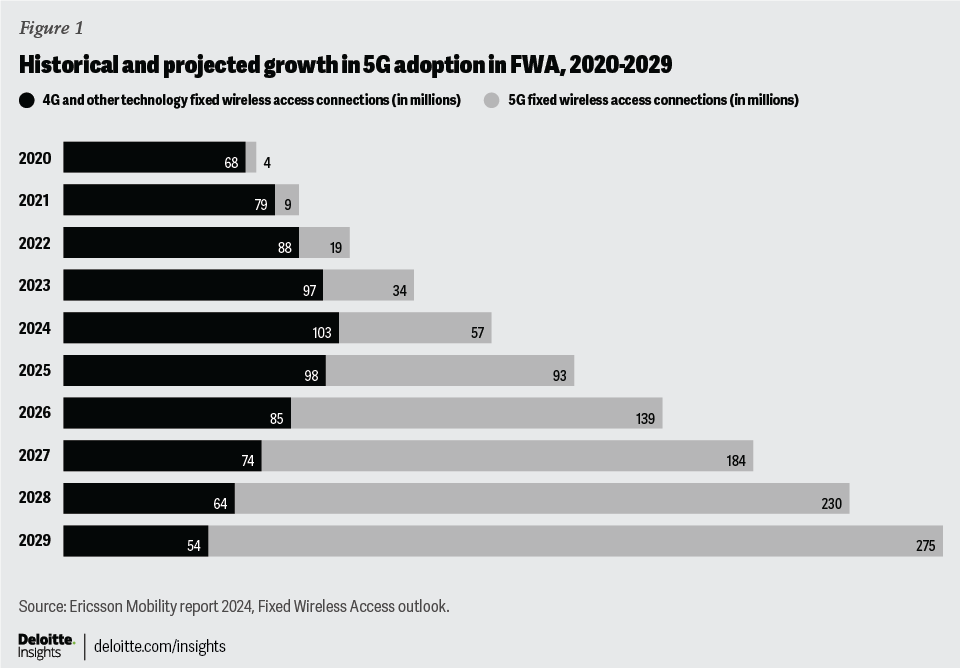

Fixed wireless access: Contrary to popular opinion, adoption may continue to grow

With US FWA net adds likely being slightly lower than last year, and some markets not expected to take off until 2026 … there may be pockets of unrealized or potential growth out there, both in the US and globally

Duncan Stewart, Dan Littman, Jack Fritz, and Hugo Santos Pinto

Fixed wireless access—when consumers get their home broadband over a fixed cellular device (mainly 5G) rather than via wires—has been a big 5G growth story over the last few years in the United States, with well over 10 million homes expected to be connected by the end of 2024.48 Consumers seem to have been attracted by competitive prices and speeds that are “good enough,”49 and carriers find it more affordable to provide broadband in areas where population densities make fiber optic less attractive.50

But with fixed wireless access (FWA), net additions (also referred to as net adds, or quarterly new subscribers less those who have canceled) in the United States during the first quarter of 2024 were less than in Q1 2023,51 and with the Indian FWA market (which is the other global market expected to drive a large number of net adds, with some projections of 100 million subscriptions by 2030) still nascent, many are expecting 2025 to be a year of lower growth for FWA.52

Deloitte’s 2022 TMT Predictions forecasted FWA growth at almost 20% annually to reach under 100 million subs globally (mostly 4G) in 2023.53 Actual growth has been roughly in line with that, with more than 150 million total subscriptions worldwide expected by the end of 2024 (with about 30% coming from 5G).54

Deloitte predicts that global FWA net adds in 2025 and 2026 will continue to rise by about 20% each year. This expectation is driven by three trends identified:

- Some FWA growth is escaping the global headlines. The United States and India are both large markets. FWA net additions in the United States are nearly one million per quarter.55 As FWA numbers in India grow, quarterly additions may be even larger.56 But there is FWA growth in other markets, too—for example, quarterly FWA net adds of 100,000 in Italy may make few headlines outside of that market,57 but on a per household basis, Italy’s FWA growth rate is only marginally lower than that of the United States.58 Italy’s FWA rate is high relative to most countries in the rest of Europe, Latin America, Southeast Asia, and Africa,59 but even so, millions of additional net adds in 2025 and 2026 are expected outside of the United States and Indian markets.

- Enterprises are increasingly opting for FWA. So far in the United States, most of the growth in fixed access wireless has come from consumers. Recently, there’s been a shift to more enterprise (mainly small and medium businesses) FWA connections.60 Some enterprises are finding FWA increasingly interesting, offering a single point of contact, consolidated billing, and more robust security.61 Deloitte predicts over a million enterprises will connect to FWA in each of 2025 and 2026 in the United States alone.62

- New tech raises the ceiling on the number of customers that can use 5G in each market. For the last few years, some believed that there was a natural ceiling on US FWA: Given the existing 5G technology and available spectrum (mainly at 2.5 GHz and 3.5 GHz), it might be difficult for there to be more than about 10 million 5G FWA subscriptions in the United States without affecting both the fixed and mobile wireless subscriber experience.63 It was thought that, in the near term, in some areas, operators would be forced to stop offering FWA to additional subscribers.64 However, even as that number of subscribers becomes closer, customer downstream speeds are improving.65 A number of 5G technology upgrades, mainly around the advanced use of radio technologies, indicate that up to 20 million US homes (19% of about 106 million US broadband homes)66 could be connected to FWA using current spectrum, suggesting the current US FWA run rate of about 3–4 million new subscribers per year might be able to continue for at least a few more years.

Bottom line

The continued growth of FWA could be a tailwind for telecom companies seeking to monetize 5G investment. Other than FWA, most 5G services with the potential to grow revenues are small as of 2025.67 For context, the average price of FWA in the United States is about US$50 per month and adding 4 million more FWA subs in 2025 translates to an additional US$2.4 billion in incremental revenues, plus the benefit or reduction of mobile churn via bundling.68

On the other hand, those who offer other kinds of broadband access (coaxial cable, copper DSL, fiber optic) are likely to continue to see competition from FWA, which could result in subscriber losses or difficulty in maintaining or increasing prices. FWA has been a competitor to this access in multiple markets, and those hoping FWA was nearing the end of its growth phase may have to wait a while yet.

The continued growth of FWA could be a tailwind for telecom companies seeking to monetize 5G investment.

5G standalone appears to be at a standstill: Will 6G run late?

Telecoms reassess investments in 5G standalone and delay 6G progress amid ROI concerns

Prashant Raman and Duncan Stewart

The deployment of 5G standalone networks is progressing more slowly than initially expected.69 Telecom companies may be hesitant to invest heavily in this next generation of 5G in part due to underwhelming returns on their existing 5G investments. For now, the rollout of 6G seems further away than ever.

As of March 2024, 49 operators (out of 585 that have launched 5G globally) have deployed, launched, or soft-launched 5G standalone (SA) networks, or 8%.70 This slow adoption rate suggests that carriers may be reluctant to spend on SA given uncertain returns on capital, at least in the near term. Additionally, the lack of monetization of 5G SA use cases may pose a challenge for adoption. Operators are putting the brakes on 5G SA deployment and may be hesitant to invest heavily in 5G SA infrastructure without clear revenue streams from its applications.71 As a result, Deloitte predicts that fewer than 20 additional networks are expected to be upgraded to standalone in 2025, keeping 5G SA at around 12% of all 5G deployments.72

5G was launched in 2018, and during the initial launch, most operators opted for non-standalone (NSA) architecture, where the 5G network is built on top of an existing 4G infrastructure, to help expedite the rollout of their services.73 This approach primarily stemmed from the unavailability of fully developed 5G SA equipment and the desire to leverage existing infrastructure.74 Consequently, the NSA rollout allowed for a quicker and more cost-effective deployment of 5G services, enabling operators to help provide enhanced network speeds and connectivity, although without the full feature set of 5G SA.75 In 2022, Deloitte Global predicted that the number of mobile network operators investing in 5G SA networks—with trials, planned deployments, or actual rollouts—would double from more than 100 operators in 2022 to at least 200 by the end of 2023, but that has not happened.76

Delays in 5G SA deployment may impede the development and testing of these technologies, affecting progress toward 6G.

Current 4G and 5G NSA networks can efficiently manage the most heavily used current consumer and enterprise applications, which may be diminishing the urgency for operators to invest heavily in 5G SA.77 On the enterprise side, despite the longer-term potential for revolutionizing different industries, the slower-than-expected pace of development and adoption of emerging 5G-based solutions that require SA has led to a more cautious approach to 5G SA deployment by operators.78

5G SA infrastructure is essential for testing and validating the technologies that will be foundational for 6G.79 It supports key use cases envisioned for 5.5G and 6G that require low latency, high reliability, and network slicing.80 Delays in 5G SA deployment may impede the development and testing of these technologies, affecting progress toward 6G.

Telecom companies are struggling to achieve ROI from 5G due to high costs and slow monetization and consumer and enterprise adoption of 5G.81 Additionally, the anticipated revenue streams from additional 5G services such as 5G network application programming interfaces haven’t materialized yet.82 With 6G use cases still under development, mobile network operators are likely focusing on maximizing 5G potential and recouping investments, which could push 6G development and deployment further down the timeline. Although various studies and standard setting are expected to occur before then, it has generally been accepted that the first commercial 6G rollouts at scale would occur around 2030.83

Bottom line

As mobile network operators plan for 5G SA, it’s important to consider how to continue optimizing the performance of their existing 5G NSA networks. A phased investment approach for 5G SA, targeting regions or sectors with higher demand, can help manage costs and focus resources more effectively. Additionally, exploring new revenue models, such as offering 5G SA as a service to specific industries or bundling it with cloud, AI, and edge computing, could open new opportunities. Collaborating with enterprise clients to help develop industry-specific solutions, particularly in sectors like manufacturing, health care, and logistics, can also help drive the adoption of 5G SA and support further investment in this technology.

Governments and regulators should be aware that the deployment of SA is an ongoing process and is taking longer than expected. This likely has implications for the move to 5.5G and 6G, and they may want to reconsider their approach to planning for next-generation network requirements and spectrum. Telecom equipment manufacturers were, to some extent, counting on deploying SA networks to help provide ongoing revenues in the anticipated spending trough between peak 5G investment in 2021 and the next wave of spending in the late 2020s or early 2030s.84 If SA continues to occur slowly, that trough may become deeper or longer than expected, with potential implications for equipment makers' revenues and profitability.

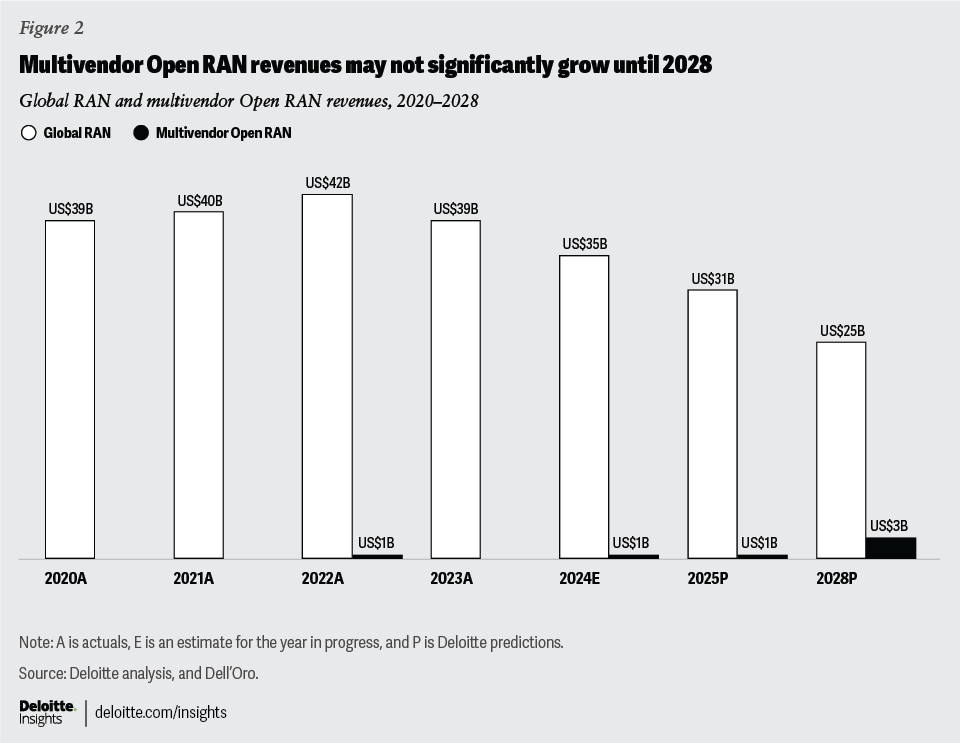

Open RAN mobile networks and vendor choice: Single vendor now, multivendor when?

Open RAN’s journey toward a diverse, multivendor ecosystem is marked by slow growth and complex challenges

Prashant Raman and Duncan Stewart

Open Radio Access Network (Open RAN) aims to democratize networks by providing mobile network operators (MNOs) who build RANs with greater choice and more flexibility, hopefully leading to better networks and lower prices. Despite high expectations and endorsements, the transition toward a diverse, multivendor ecosystem is proving slower and more complex than some initially anticipated.85 Realizing true multivendor Open RAN may take a while, as Deloitte predicts that there will be no additional multivendor Open RAN networks deployed or even announced in 2025.86

The Radio Access Network (RAN) is an important component of cellular networks that manage radio communications between mobile devices and the core network, and historically it was a closed and proprietary solution. The entirety of a network was from one vendor, and no other vendor’s gear would work with it.87 Open RAN emerged as a transformative concept in the telecommunications industry, aiming to standardize and democratize the design and implementation of network components.88 It gained momentum in the late 2010s with the establishment of the O-RAN Alliance in 2018, which was formed to help promote more open and interoperable RAN architectures.89

By 2028, single-vendor Open RAN solutions are expected to comprise 15% to 20% of total RAN revenues, while multivendor Open RAN solutions are expected to make up only 5% to 10%.

In 2021, Deloitte predicted that global active public network Open RAN deployments would double from 35 to 70.90 The forecast was too optimistic: As of March 2024, the ongoing public network Open RAN deployments and trials stand at 45, with only two networks globally being multivendor Open RAN.91

A goal of Open RAN was to provide operators with a more open alternative, fostering competition and diversity in the market.92 However, the reality has not yet lived up to the aspirations. Many operators continue to purchase radios and baseband products for any given site from the same vendor, and the impact of pure-play Open RAN companies has been minimal so far; the five biggest RAN vendors currently account for around 95% of the market.93

In 2024, Open RAN is projected to represent only 7% to 10% of the total RAN market, or about US$2.5 billion to US$3.5 billion, of a projected US$35 billion.94 Moreover, single-vendor solutions are anticipated to continue to be more widely used than Open RAN revenues in the near future. By 2028, single-vendor Open RAN solutions are expected to comprise 15% to 20% of total RAN revenues, while multivendor Open RAN solutions are expected to make up only 5% to 10% of the market, with traditional RAN still making up 80% to 85% of the market.95 Although many in the industry still think the long-term potential of multivendor Open RAN remains strong,96 achieving this vision could take more time.

Navigating the Open RAN landscape can involve integrating various hardware for high-capacity performance and cost efficiency. Operators historically preferred one-stop shopping from traditional RAN vendors who took care of everything and provided a single source of accountability.97 Sourcing from multiple providers could pose challenges, especially for smaller operators.

However, the Open RAN market is part of the broader US strategy to help enhance economic security and reduce reliance on foreign supply chains, particularly in critical sectors like telecommunications.98 Open RAN technology may be pivotal in this effort, aimed at breaking the current market concentration dominated by a few major players, mostly non-American.99 Geopolitical tensions have led to the exclusion of some of these companies from significant markets, including the United States and Europe, thus limiting vendor options and underscoring the need for supply chain diversification.100 Open RAN helps address this by enhancing competition and innovation within the domestic market. Reshoring through Open RAN could be a strategic opportunity to help encourage domestic production of telecom equipment and maintain its leadership in the global telecommunications infrastructure market.101

Bottom line

Most MNOs already have Open RAN on their planning agenda. It’s been talked about for years now.102 Some have started the steps below; others are expected to start in the next year or two. MNOs can explore Open RAN in a low-risk and experimental way by gradually integrating its components into less critical areas of their networks. Collaborative testing with other operators and vendors or alliances can help address the technical challenges of deploying multivendor solutions. Working closely with emerging Open RAN vendors as well as existing RAN vendors could also provide an opportunity to help develop solutions that meet specific network needs. Additionally, investing in building internal capabilities and expertise around Open RAN technologies, whether through staff training or hiring specialists, could likely help navigate the complexities of a multivendor environment.

Existing large RAN vendors will likely want to balance being “open.” At one level, Open RAN could be considered a threat to their existing business, but if Open RAN is inevitable, they may want to consider disrupting themselves, before someone else does it. Original equipment manufacturers (OEMs) are already focusing on developing interoperable products that can seamlessly integrate with existing network infrastructures103—and they will likely continue to partner with smaller players and startups in the Open RAN space. Staying engaged with industry alliances can help OEMs and emerging Open RAN vendors keep their products aligned with evolving standards and trends.

One of the benefits of multivendor Open RAN was increased vendor diversity, especially vendors outside Europe and Asia.104 If Open RAN continues to proceed slowly for now, that geographic balance of vendors is unlikely to change materially in the near term, and other tools may be needed to help diversify the existing RAN supply chain.

Despite quantum’s slow start, don’t be slow to start your defense against it

Quantum drug discovery and financial modeling are likely several years away, but the time needed to upgrade cyber defenses for the quantum age likely necessitates prompt action

Colin Soutar, Duncan Stewart, Scott Buchholz, and Gillian Crossan

The 2019 and 2022 TMT Predictions reports discussed quantum computing105 and mentioned the attendant cryptographic threats in the 2022 edition.106 Some of those expectations have become actualities. Current quantum computers are not yet reliable enough for real use cases;107 heightened attention is being placed in the cybersecurity domain;108 and as predicted by Deloitte in December 2023, various aspects surrounding cyber standards came to fruition this year.109 For example, the National Institute of Standards and Technology (NIST) recently issued post-quantum cryptography standards.110 (NIST is widely considered the gold standard for cybersecurity and cryptography, particularly in the development and adoption of encryption and digital signature algorithms, protocols, and frameworks that ensure secure data communication and transaction protection.) One cybersecurity risk relates to a specific algorithm—Shor’s algorithm, an algorithm developed in 1994 specifically to harness quantum effects to crack public key encryption schemes rapidly111—being implemented on a quantum computer.

Deloitte predicts that the number of companies working on implementing post-quantum cryptography solutions is expected to quadruple in 2025 compared with 2023, and their spending also is expected to have quadrupled. This is a conservative estimate, based on projected costs between 2025 and 2035 to migrate federal systems112 and ongoing efforts in the financial services industry to mitigate this risk.113

The timelines for both the positive quantum use cases and the defense against quantum cyberthreats should be considered. The question as it relates to timelines often has less to do with how and when a quantum computer will be used to implement positive use cases and for Shor’s algorithm, but more so: How long will it take for organizations to adopt and implement the recently issued NIST standards, to rely on cloud hyperscalers, specialized security components, and on “homegrown” applications that leverage cryptographic libraries for security features such as confidentiality and trust? To help answer this question, some organizations are starting their journey toward quantum cyber readiness by understanding what their exposure could be to this threat, by planning roadmaps for updates that meet their specific mission statements and business operations, and by working through the potential procurement and contractual requirements.

Contributing to the timeline uncertainty further are state or state-sponsored actors (and others) who are purportedly harvesting encrypted data now to decrypt it later when a cryptographically relevant quantum computer exists (also known as “harvest now, decrypt later” attacks).114 It should be interesting to see how organizations deal with this “sleeping threat” and whether they will proactively adopt the NIST standards to help prevent a future threat of data spills, especially in cases where such data is expected to have a long protection life cycle, such as personal information.

Interestingly, some large-scale providers are starting to introduce post-quantum cryptography into their platforms.115 It’s likely that other messaging services that currently offer end-to-end encryption will also roll out post-quantum cryptography in 2025 and beyond. Further, hyperscalers are offering services that can allow customers to benchmark, prototype, or understand the performance impact of quantum-resistant cryptography on cloud services.116

Bottom line

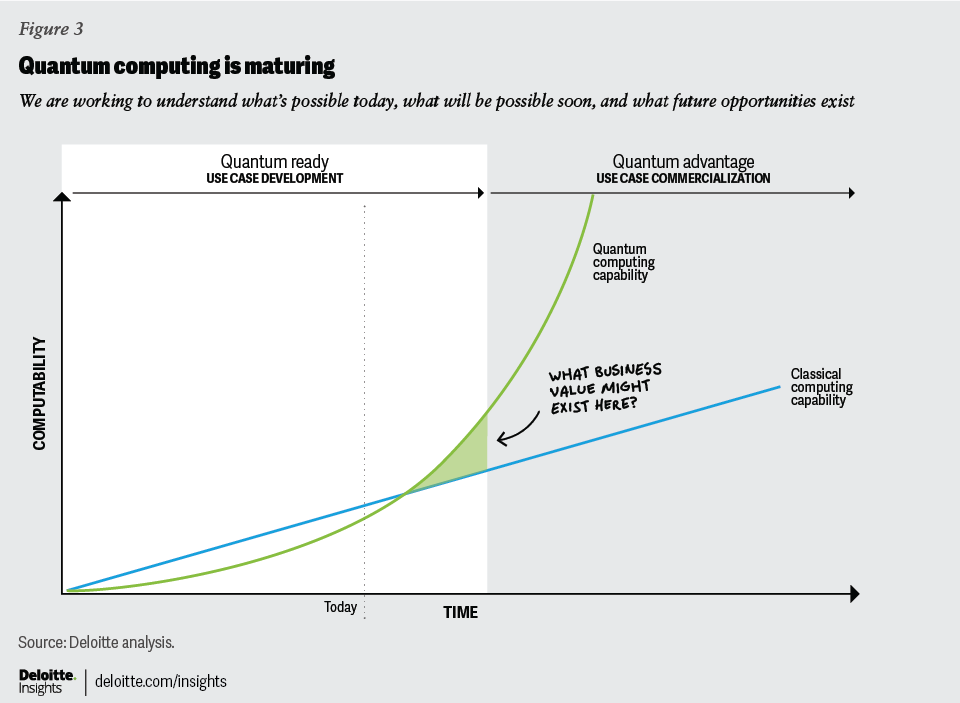

Quantum advantage, in which quantum computers have a large advantage for solving useful problems over classical computers, likely remains a few years off, barring any unexpected breakthroughs (figure 3). As the blue-shaded area in figure 3 gets closer, between use case development and use case commercialization, organizations should consider taking a risk-based approach to help address the threat to cryptography. They should understand how this risk compares with others they’re facing and proactively mitigate the risk accordingly.117

The organization that develops a cryptographically relevant quantum computer will be unlikely to advertise that it has one and can use it. So, there may not be a warning. This should make it more important to act sooner, lest organizations find themselves needing to react to an event at a time when resources may be scarce and systems may need to be shut down.118

Although working on post-quantum cryptography could be the necessary near-term implication of quantum computing in 2025, organizations can still work on their processes in preparation for the day when quantum computers offer quantum advantage and organizations can work on use cases that could bring positive benefit to many industries such as the financial sector and health care.

The organization that develops a cryptographically relevant quantum computer will be unlikely to advertise that it has one and can use it.

Quantum technologies can offer hope for solving long-standing challenges via more effective drug discovery and the predictive modeling of financial or environmental disturbances. The attendant cybersecurity threat shouldn’t overshadow the potential for such positive benefits—especially when cryptographic upgrades that can help protect against the threat can be implemented in a methodical, gradual, even systematic manner.

RISC-V: Closing the geopolitical gen AI loophole

An open-source alternative to proprietary chip design is gaining popularity among CPU designers. Its potential role in gen AI for markets under export restriction is a new twist for a new technology.

Duncan Stewart, Christie Simons, Jeroen Kusters, and Gillian Crossan

The 2022 TMT Predictions report included a chapter on RISC-V, which forecasted that open-source instruction set architecture (ISA), the set of rules and specifications that dictate how a computer’s central processing unit (CPU) operates, would see strong growth. The report predicted that the number of RISC-V chips would double year over year from 2022, and that revenues could “approach US$1 billion by 2024.”119

The industry organization, RISC-V International, in late 2023 estimated that RISC-V-based system-on-chip (SoC) shipments were 1 billion in 2023 and could be close to 2 billion in 2024.120 As predicted, revenues are still nascent, and RISC-V chip revenue is expected to be under US$1 billion for the calendar year 2024.121 Given that global chip revenues for the year are predicted to be over US$611 billion for 2024, RISC-V remains niche for now.122 Longer term, some forecasts are optimistic, with one calling for RISC-V to represent 25% of the SoC market by 2030, or more than US$100 billion.123

While RISC-V has the potential to capture a significant share of the SoC market, there are national security risks associated with this technology. US lawmakers serving on the bipartisan House Select Committee on the Strategic Competition Between the United States and the Chinese Communist Party have urged the Commerce Department to use its export control authorities to regulate or restrict the transfer of RISC-V technology to China. This approach aims to protect and promote collaboration on RISC-V technology between the United States and its allies as well as protect their mutual national security interests.124

In order to learn why, we should revisit what ISAs are, where they are found, and how this connects with AI.

ISAs are the heart of CPUs. In many laptops and most data centers, the dominant CPU ISA is the x86 architecture. In most smartphones, the dominant ISAs are CPUs based on the RISC ISA, which is being used in some laptops and data center CPUs, although x86 has larger market share.

Generative AI generally requires special computer processing chips for both training and inferencing of large language models. Most readers may already be aware of the role that graphics processing units (GPUs) can play in performing gen AI computing as their robust computing power handles the intricate calculations required by these models.

Although GPUs do the computational “heavy lifting,” there is also usually a CPU (or two) needed to orchestrate data flows and perform other coordinating tasks, and the “attach rate” (the number of GPUs per CPU) seems to be changing, and CPUs are becoming relatively more important. For example, the first version of gen AI accelerating hardware from Nvidia paired 8 GPUs with 2 CPUs (a 4:1 ratio) with a choice of proprietary x86 ISAs.125 And by early 2025, Nvidia is expected to offer a new kind of tray that consists of four next-generation GPUs and two CPUs (a 2:1 ratio).126 Unlike the first generation, these CPUs were designed by Nvidia itself and are based on the Arm ISA.127

The United States has imposed multiple export restrictions on IP, talent, chipmaking equipment, and certain chips. In early 2023, the United States restricted the export of the most-advanced GPUs at the time (typically, manufactured at process nodes of 10 nm and below and capable of certain levels of chip-to-chip data transfer rates),128 and later that year, the United States restricted the export of additional advanced CPUs, both x86 ISA and Arm ISA.129

China currently cannot import or manufacture GPUs or CPUs that are state-of-the-art advanced process nodes at 7 nm and below and required for gen AI training or inference.130 Although RISC-V is a niche ISA today, it’s possible that over time, future generations of gen AI computing infrastructure could use RISC-V CPUs as controllers. China would still need to make state-of-the-art GPUs; restricting RISC-V exports to China could be considered an extension of current US restrictions. And if RISC-V is not restricted by the United States, it could be a loophole or workaround for other restrictions including the ones on CPUs and GPUs at advanced process nodes. Further, China is exploring RISC-V in other areas, for example, developing CPU controllers for gen AI processing–which could be something the United States restricts as well.

Bottom line

Gen AI hardware solutions use GPUs plus CPUs (or GPUs with CPU cores on the same die). Most CPUs are based on x86 ISA, and the rest are Arm ISA, but none seem to be using RISC-V as the main ISA, for now (some use RISC-V cores for other functions). As such, export restrictions in 2025 may be more focused on closing future loopholes.

RISC-V International moved from the United States to Switzerland in 2020,131 so it is still unclear exactly how US export restrictions might work or be enforced. However, the US government is reported to be reviewing potential risks and assessing what actions could both address potential concerns and not harm US companies that are part of the international groups working on the technology.132

China has already made headway in RISC-V and appears well-positioned in this space.

Finally, while China’s use of RISC-V could be restricted, it is noteworthy that China has long been interested in and a leading proponent of RISC-V, with over half of premium-level RISC-V International members being from China (12 out of 22).133 Further, as of 2022, over half of the 10 billion RISC-V cores made that year were from China.134

China has already made headway in RISC-V and appears well-positioned in this space. At the same time, it will be interesting to see how it navigates any potential adverse impact that could stem from possible RISC-V curbs in the future.

{kind=link}

{kind=link}

{kind=link}