2025 global telecommunications outlook

The industry appears to want to shift into growth mode with gen AI, control the shape of 6G and be able to monetize it, deploy new technologies in a measured way, and use M&A in some new ways

Doug Van Dyke

Dan Littmann

Jack Fritz

Duncan Stewart

Prashant Raman

Telecom stocks increased in value during 2024, up about 11% for the year.1 However, this fell short of the S&P 500 or NASDAQ gains, which were up about 25% and 30%, respectively.2 At trade shows like the Mobile World Congress (MWC) in Barcelona, in the press, and in meetings, telecom CEOs are asking, “How can we turn ourselves into a growth industry once again, and see higher stock valuations?”3

The telecom industry has experienced higher periods of revenue-growth cycles over the last 100 years, driven by wireline a century ago, and more recently by providing mobile connectivity and internet broadband. At other times, the industry is seen as a slow but steady sector, with single-digit revenue growth, solid dividend yields (about 4% globally on average,),4 and often being able to cut costs so that profitability rises slightly faster than revenues.

That’s where the industry is in 2024, and as it looks at 2025 and beyond to 2030, telecoms are expected to work to keep cutting costs, keep capital expenditures under control, monetize their past investments, and use mergers and acquisitions (M&A) to drive value.5 Growth-oriented telecoms will likely also find ways to grow revenues faster than core connectivity growth would suggest. However, the market for telecoms is rapidly evolving. As new technologies and digitization of the economy continue to flourish at rapid pace, telecoms will be faced with difficult investment choices.

This outlook focuses on three of those difficult choices, and we have a full chapter on each:

- In 2025, the most discussed source of growth for many industries is generative AI, and telcos are asking how they can share in that excitement.6

- At the same time, telcos are roughly at the midpoint between the launch of 5G and the expected launch of 6G, and they want to confirm that they can shape 6G to be more profitable than 5G has so far been.

- Finally, after years of divesting noncore assets, telcos are getting primed to deploy M&A strategies in pursuit of growth.7

Telecom “fast facts”

Below, we’ve put together some “fast facts” that give an overview of some important statistics that make up this critical but sometimes underappreciated industry:

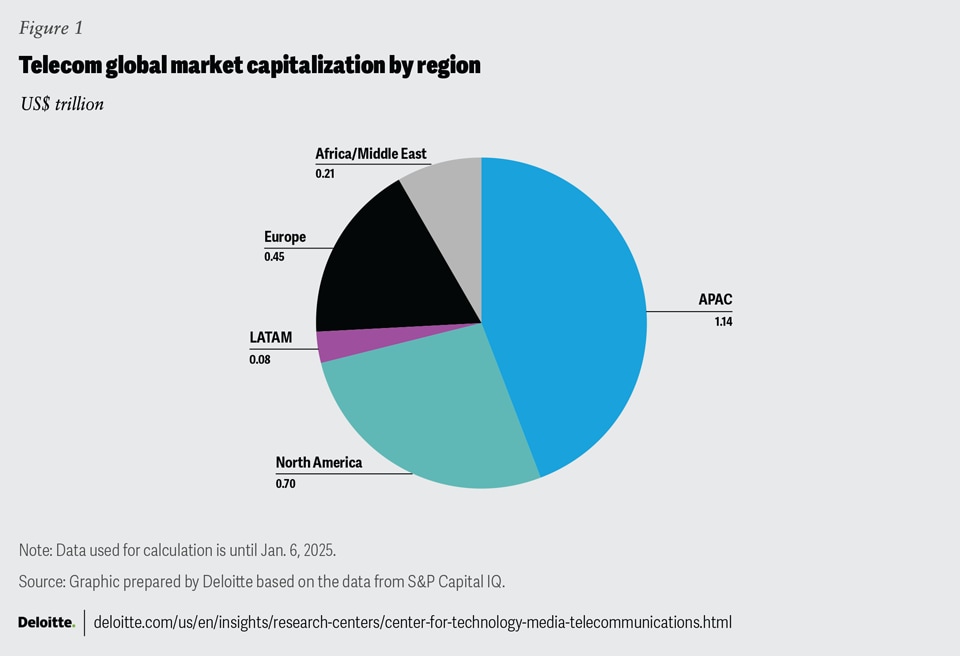

- Globally, the telecommunications industry is expected to have revenues of about US$1.53 trillion in 2024, up about 3% over the prior year.8 Both in 2024 and out to 2028, growth is expected to be higher in Asia Pacific and Europe, Middle East, and Africa, with growth in the Americas being around 1% annually. All three regions are expected to surpass half a trillion dollars in revenue each by 2027.9 By market cap, the sector is about US$2.6 trillion globally (figure 1).

- Telco stocks globally were up about 11% in 2024, but there was significant regional variation: North American telcos were up over 20% while Latin American and Caribbean telcos were down about 14%, with Asia-Pacific and European players up by 11% to 12%, and Africa and the Middle East remaining flat.10

- Global telecoms are experiencing positive financial conditions: Revenues are growing, operating expenses are being contained, capital expenditures are declining, average revenue per user (ARPU) is up a bit (by 2%, to about US$28) and earnings before interest, taxes, depreciation, and amortization (EBITDA) margins were just over 38% in early 2024.11

- By the end of 2025, it is expected that just under 5 billion people will have mobile internet access, up from 4.6 billion in 2023.12 Although 96% of the world’s population have mobile internet available in 2023, that means that 4%, or about 350 million, experience a coverage gap (which only represents where they live, not where they travel, suggesting the actual coverage gap is even larger).13 Further, 39% of the population, or 3.1 billion people, have mobile connectivity available, but are nonetheless not connected for a variety of reasons, which is the usage gap.14 Around 19 million jobs were directly supported by the mobile ecosystem in 2023.15

The US Communications Infrastructure Index (CII)

US and global communications infrastructure providers have a century-plus track record of innovating and scaling to meet existing consumer and business connectivity needs and investing to meet future needs, most recently handling the spike and shift in demand due to COVID-19–driven restrictions.

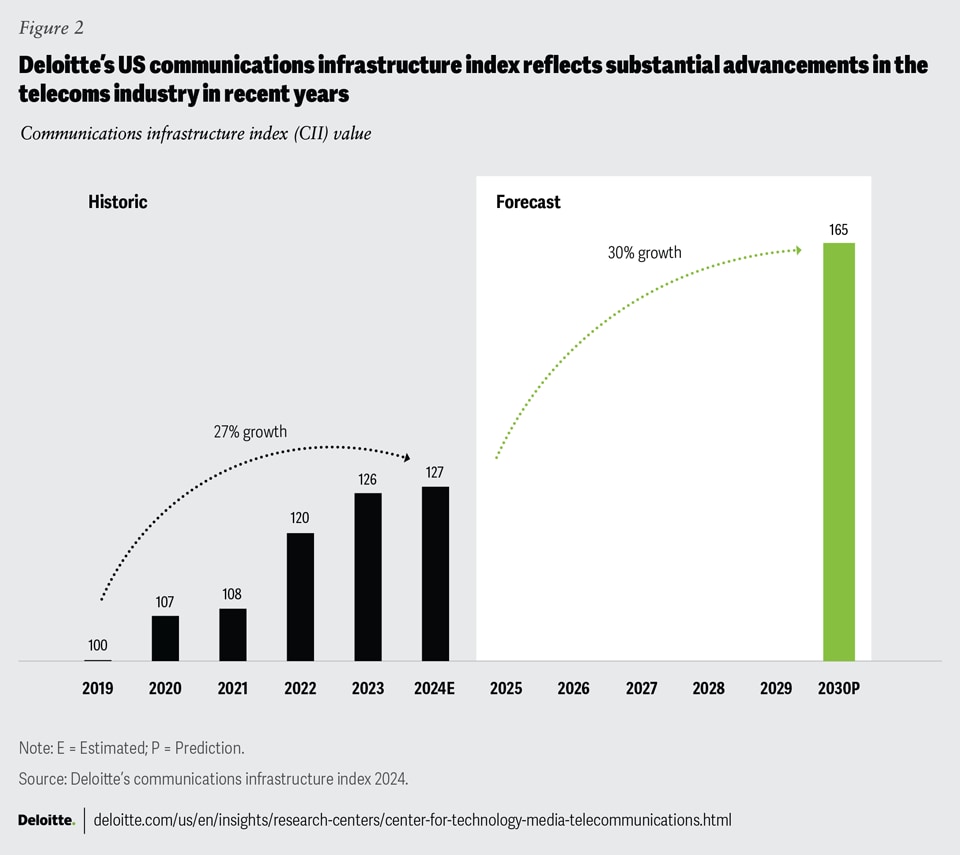

To answer the question “Are we prepared for another shift?” Deloitte has created the communications infrastructure index for the United States. Composed of 20 key metrics, updated annually, the CII shows almost 30% growth across the combined metrics from 2019 to 2024, and even sets an aspirational goal for further growth to 2030 (figure 2).

Telcos and gen AI: How can the industry profit from this tech?

Telcos are using gen AI to reduce costs, become more efficient, and offer new services. Some are building new gen AI data centers to sell training and inference to others. What role does connectivity play in these data centers?

There is a gen AI gold rush expected over the next five years. Spending estimates range from hundreds of billions to over a trillion dollars on the physical layer required for gen AI: chips, data centers, and electricity.16 Close to another hundred billion US dollars will likely be spent on the software and services layer.17 Telcos should focus on the opportunity to participate by connecting all of those different pieces of hardware and software. And shouldn’t telcos, whose business is all about connectivity, be able to profit in some way?

There are gen AI markets for connectivity: Inside the data centers there are miles of mainly copper (and some fiber) cables for transmitting data from board to board and rack to rack. Serving this market is worth billions in 2025,18 but much of this connectivity is provided by data centers and chipmakers and have never been provided by telcos.

There are also massive, long-haul fiber networks ranging from tens to thousands of miles long. These connect (for example) a hyperscaler’s data centers across a region or continent, or even stretch along the seabed, connecting data centers across continents.19 Sometimes these new fiber networks are being built to support sovereign AI—that is, the need to keep all the AI data inside a given country or region.

Historically, those fiber networks were massive expenditures, built by only the largest telcos or (in the undersea case) built by consortia of telcos, to spread the cost across many players.20 In 2025, it looks like some of the major gen AI players are building at least some of this connection capacity, but largely on their own or with companies that are specialists in long-haul fiber.21 Telcos may want to think about how they can continue to be a relevant player in the part of the connectivity space, rather than just ceding it to the gen AI behemoths.22 For context, it is estimated that big tech players will spend over US$100 billion on network capex between 2024 and 2030, representing 5% to 10% of their total capex in that period, up from only about 4% to 5% of capex for a network historically.23

Where the opportunities could be greater are for connecting billions of consumers and enterprises. Telcos already serve these large markets, and as consumers and businesses start sending larger amounts of data over wireline and wireless networks, that growth might translate to higher revenues. A recent research report suggests that direct gen AI data traffic could be in exabyte by 2033.24

The immediate challenge is that many gen AI use cases for both consumer and enterprise markets are not exactly bandwidth hogs: In 2025, they tend to be text-based (so small file sizes) and users may expect answers in seconds rather than milliseconds,25 which can limit how telcos can monetize the traffic. Users will likely pay a premium for ultra-low latency, but if latency isn’t an issue, they are unlikely to pay a premium.

Telcos may want to think about how they can continue to be a relevant player in the part of the connectivity space, rather than just ceding it to the gen AI behemoths.

A longer-term challenge is on-device edge computing. Even if users start doing a lot more with creating, consuming, and sharing gen AI video in real time (requiring much larger file transmission and lower latency), the majority of devices (smartphones, PCs, wearables, or Internet of Things (IoT) devices in factories and ports) are expected to soon have onboard gen AI processing chips.26 These gen accelerators, combined with emerging smaller language AI models, may mean that network connectivity is less of an issue. Instead of a consumer recording a video, sending the raw image to the cloud for AI processing, then the cloud sending it back, the image could be enhanced or altered locally, with less need for high-speed or low-latency connectivity.

Of course, small models might not work well. The chips on consumer and enterprise edge devices might not be powerful enough or might be too power inefficient with unacceptably short battery life. In which case, telcos may be lifted by a wave of gen AI usage. But that’s unlikely to be in 2025, or even 2026.

Another potential source of gen AI monetization is what’s being called AI Radio Access Network (RAN). At the top of every cell tower are a bunch of radios and antennas. There is also a powerful processor or processors for controlling those radios and antennas. In 2024, a consortium (the AI-RAN Alliance) was formed to look at the idea of adding the same kind of generative AI chips found in data centers or enterprise edge servers (a mix of GPUs and CPUs) to every tower.27 The idea would be that they could run the RAN, help make it more open, flexible, and responsive, dynamically configure the network in real time, and be able to perform gen AI inference or training as service with any extra capacity left over, generating incremental revenues.28 At this time, a number of original equipment manufacturers (OEMs, including ones who currently account for over 95% of RAN sales), telcos, and chip companies are part of the alliance.29 Some expect AI RAN to be a logical successor to Open RAN and be built on top of it, and may even be what 6G turns out to be.

Strategic questions to consider:

- How can telcos deal with disintermediation from big tech companies who are building their own long-haul point to point fiber networks?

- Should telcos build their own gen AI data centers and sell training and inference as a service to third parties? Equally, if they deploy AI RAN, can they make money from selling underutilized gen AI processing capacity?

- Will consumer gen AI move from its current low need for connectivity (small files, latency doesn’t matter) to something that might drive connectivity revenues with larger files to transmit and latency becoming important?

- Equally, will the rise of on device gen AI processors for smartphones, computers and IoT devices increase the need for connectivity, or decrease it?

Between generations: Telcos get to say what they want (and don’t want) in 6G

Higher speeds and costs without use cases or monetization may not be the answers for 6G in 2030 and beyond. What might be, and how can telcos shape the standard?

The year 2024 marked the halfway point for the 5G wireless standard: six years since it first launched, and six to go before the expected launch of the next generation standard (6G) in 2030. Globally, telcos are becoming increasingly clear and vocal on what they don’t want from 6G.30

Some have indicated they don’t want another wholesale upgrade, requiring hundreds of billions of dollars of worldwide spending, delivering speeds higher than most consumers or enterprises need or will pay for, with no near-term monetization, and eventual monetization relying on use cases that are either far off, unlikely, or niche.31

To be clear, each successive wireless generation is an intentional overshoot: You don’t define a standard to barely meet customer needs in year one and still have it be useful a decade later. In the first year or two after launch, telcos complained that 3G and 4G offered speeds and features that no one needed or would pay for.32 But it is now six years since 5G launched, and telcos are often (aside from providing fixed wireless access for home broadband) unable to find large use cases that require 5G speeds and features.33

What may be more worrying is that not only were there seemingly few additional use cases driving 5G adoption and monetization in 2024, but there may not be many more for 2025 or even 2026 either. Things that require extreme speeds, low latencies, network slicing or high device densities, such as augmented or virtual reality (AR/VR) goggles, self-driving cars, or remote telesurgery are not expected to see broad adoption until the end of this decade, if at all. As an example, AR/VR sales actually declined in 2024, with products being canceled and design teams being shrunk or eliminated.34

One possible source of 5G or potential 6G demand is generative AI.35 But probably not in 2025: most gen AI applications are small text files that have latency measured in seconds rather than the milliseconds 5G can provide.36 One estimate (from an equipment vendor) suggests that direct consumer and enterprise gen AI data traffic could be a few percent of global wide area network (WAN) traffic—but not until 2033.37

In Deloitte’s view, what might 6G look like if it were more focused on meeting customers’ future needs and generating positive returns on investment (ROI) for telcos?

- Premium performance features for gen AI services that enterprises and hyperscalers would find valuable enough to pay extra for.

- Tech features that can flow directly through to the business support systems (BSSs) that customers can buy on demand.

- 6G—in line with 5G and 4G before it—could see the cost per gigabyte of data fall yet again, ideally by about an order of magnitude, or more or less a 90% reduction.

- It should not only support but be optimized for heterogenous networks, or het nets. Any given transmission should be able to be seamlessly and rapidly switched between or even carried across a mix of connection technologies, ranging from terrestrial cellular, satellites, and especially Wi-Fi, both in the home and workplace, and increasingly outdoors. The majority of wireless traffic for consumers are already being carried on Wi-Fi.

- 6G should be even more sustainable, consuming less energy per GB than 5G, ideally another order of magnitude in reduction.

- 6G should be more affordable, reducing the global usage gap (those who live where cell service is available, but do not subscribe, in part due to affordability of services) from over 2 billion people in 2024.

- Historically, each new generation of wireless was accompanied by making available large blocks of new spectrum. Additional large blocks of desirable spectrum are unlikely to be available when 6G launches, so 6G will likely need to work in shared bands (for example, with military having priority, but cellular able to use it when not used by the military) or sharing data transmission across multiple spectrum bands simultaneously.

One possible source of 5G or potential 6G demand is generative AI.

Strategic questions to consider:

- How can telcos best make their 6G vision and need for monetization clear to the industry bodies that will be defining the 6G standard?

- If the 6G standard evolves differently from 5G’s, does that mean it will no longer be defined in the late 2020s and deployed around 2030, as previously expected? If 6G is delayed, what impact would that have on wireless infrastructure and the need for spectrum?

- More specifically, the OEMs that make wireless network equipment tend to see revenues rise when each new standard is deployed: If 6G comes late, or doesn’t need new equipment, what would that mean for the OEMs?

Telecom M&A: Lots of deals and new PE partners with creative structures may be likely

The industry has been doing large numbers of M&A deals annually for the past five years, but in 2025, private equity could become even more active as partners begin to implement more creative deal structures.

Globally, telecom M&A has been at high levels for the last decade. Along with acquisitions to drive growth, some companies have been looking to shed noncore assets, hoping to improve their return on invested capital, reduce debt, and become more focused.38 People who invest in telecom companies may not be valuing certain assets as highly as new financial partners, specifically as private equity (PE) investors might.

Telcos shedding assets is not new: As of 2023, 97% of all cell towers in the United States and Mexico were owned by someone different from their original telco owners—often by PE and infrastructure funds.39

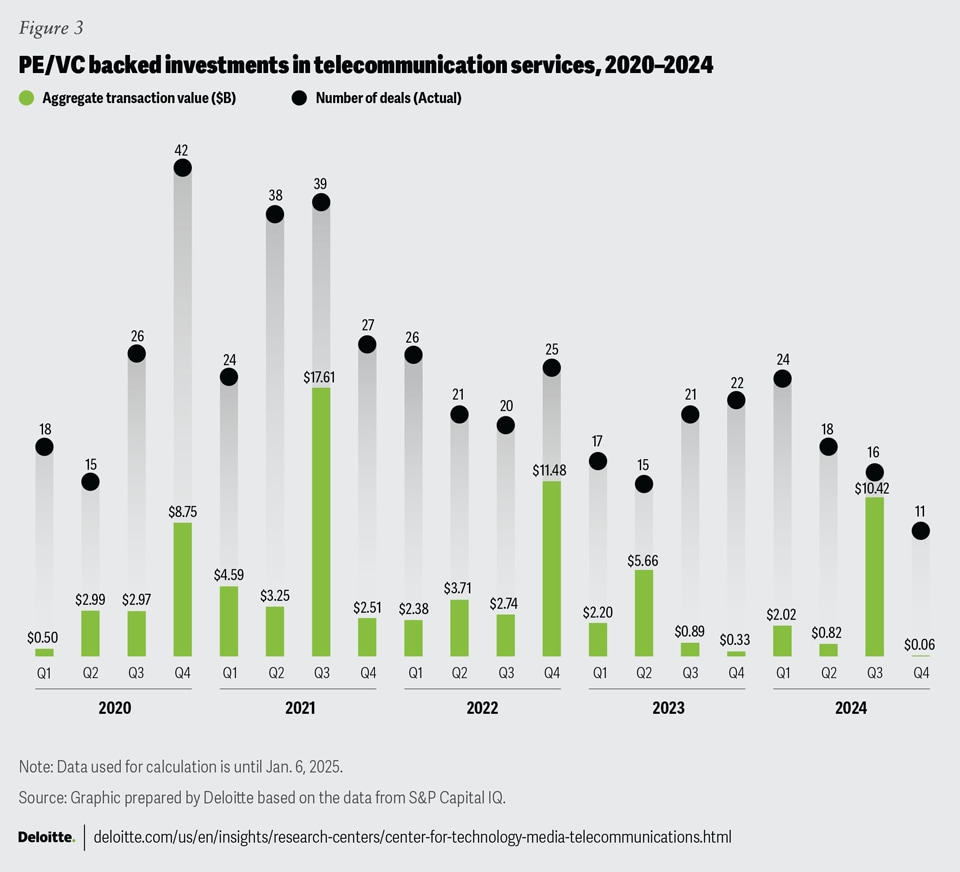

But what has been fluctuating is the level of PE activity (figure 3). For context, the share of financial buyers for telco M&A has grown from just over 60% in 2021 to over 80% in the first half of 2024.40 There was US$28 billion of PE-backed telco M&A deals globally in 2021 and US$20 billion in 2022.41 Rising interest rates and a pause after a divestment wave saw activity slow down to just US$2.7 billion during the second half of 2023 and the first half of 2024.42

But as telcos start divesting again, PE is back with record levels of dry powder— over US$300 billion of available capital to invest in longer-duration, high-yield infrastructure assets.43 Telco deal value soared to over US$11 billion in the second half of 2024.44 Not only is activity higher, but there are new types of deals, as well.45

Telcos have opportunities to unlock value from assets previously considered core which is likely contributing to deeper conversations about what is core and noncore (as opposed to tower divestment, which was perhaps a more obvious decision). As an example, Canada’s Rogers Communications announced it had sold a minority interest in a portion of its wireless backhaul transport infrastructure for US$5 billion, with more than one US PE firm apparently bidding.46 This is a relatively new trend: Deals are being structured to match the criteria of specific types of financial buyers—joint ventures (JVs), structured as “devcos” (a type of private sector development partner that helps build and grow companies in specific markets) are an example.

Going forward, PE investors are also likely to be more heavily involved as telecom companies look to build and connect generative AI data centers. M&A around data centers has recently doubled from 2019 to 2022.47

In the telco sector, this creates opportunities for telcos to partner with PE firms that tend to have a lower cost of capital and can share in the upside from value creation. As one sample market, over 15 global telecoms have announced they will build their own gen AI data centers, using the training and inference capacity to offer new services, and selling gen AI as a service to others, largely driven by data-sovereignty needs.48 Some PE firms are already participating in these initiatives, which includes hyperscalers that have been taken private by PE firms over the last three years.49 While PE investors offer several advantages, a trend from PE often includes more scrutiny on price, governance structure, management, and technical teams. This can include exploring how telcos’ natural advantages in connectivity can be leveraged when creating gen AI factories.

Another potentially interesting market will be connecting these and other gen AI data centers, both at the continental level and also via subsea fiber optic cables. Fiber optic deals represented the largest subsector share (11.3%) of all closed M&A infrastructure deal volume during 2024, ranking even ahead of data center activity, which only represented 10.7% of total infrastructure M&A activity.50 These fiber optic deals were completed primarily in Europe and North America, which represented 46.4% and 24.6% of closed fiber optic deal activity in 2024, respectively.51 This market is capital-intensive and is increasingly being viewed by as an emerging asset class by some PE and infrastructure investors, although (as discussed in the section on AI monetization) big tech players are increasingly building their own networks, rather than relying on or even partnering with telcos.52

Strategic questions to consider:

- How can telecom companies achieve more than their share of growth by partnering with PE investors to access new markets and strategies?

- What opportunities exist to monetize legacy assets and free up capital to invest in growth-oriented projects?

- Is it better to divest of noncore assets completely, or structure into a new JV with PE investment to provide fresh growth capital while maintaining a controlling interest in legacy assets or businesses?

What’s new in 5G and gen AI devices for 2025?

Some industry trends like fixed wireless access (FWA) are staying strong, some like Open RAN and 5G Standalone (SA) are staying slow, while others like gen AI smartphones and B/OSS modernization are a whole new thing.

In 2025, we predict the telecommunications industry will likely see continued growth in FWA and generative AI integration on smartphones. While FWA is expected to expand globally, providing connectivity to millions, the US market will likely experience more measured growth. Additionally, telecom providers are expected to prioritize modernization efforts to enhance operational efficiency and customer experience through their BSSs and OSSs (operational support systems), paving the way for a more integrated and responsive digital infrastructure.

However, the journey toward multi-vendor Open RAN and the rollout of 5G SA networks will likely remain slow, potentially having impacts on vendor choice and even the eventual rollout of 6G.

FWA is making waves in the United States, capturing the attention of both consumers and telecom providers alike. This technology, which uses 5G to deliver internet to homes and businesses, has become a cost-effective alternative to traditional broadband, especially in less densely populated areas. In fact, by the end of 2024, it’s anticipated that over ten million homes in the United States will be connected through FWA.53 The benefits of FWA include competitive pricing and decent speeds for consumers, and lower deployment costs for broadband providers. However, after an initial surge, FWA growth slowed slightly in early 2024, and some analysts expect 2025 to see a slower expansion rate in the United States.54 Despite this, Deloitte predicts that FWA will maintain a steady momentum globally, with net additions rising by about 20% annually in 2025 and 2026.55 This growth will likely be driven by enterprise demand and technological advancements, helping FWA remain a vital telecom revenue stream, even as it shakes up the traditional broadband market. As an example, in our new CII, fixed wireless has had an impact on broadband pricing as ARPUs have come down in the United States.56

However, the changes in telecoms go beyond FWA. Telcos are now rethinking their foundational infrastructure to keep up with shifting customer expectations and the pursuit of digital growth. Historically, telecom providers have operated separate BSSs and OSSs, creating a somewhat fragmented system that wasn’t always agile or cost-effective.57 Now, modernization is on the horizon. Providers may be increasingly looking to integrate automation and intelligence, with the potential to merge BSSs and OSSs into a single, seamless platform. This shift could help streamline processes and capture new revenue streams in a rapidly evolving digital landscape. Deloitte predicts that, by 2025, the combined OSS and BSS market will be worth US$70 billion, with cloud-based solutions, application programming interfaces (APIs), and a unified, service-centric model leading the way.58 This push toward modernization could accelerate growth and offer providers greater efficiency, enhanced security, and, importantly, a better customer experience.

As telecoms evolve and embrace new technologies, smartphones—billions of consumers’ constant companions—are also experiencing a shift.59 Smartphones have revolutionized daily life, replaced multiple devices, and changed how individuals communicate, work, and even play. Yet, in recent years, updates have been tended to be incremental, leaving some wondering if there’s anything new to get excited about. Major smartphone providers are now experimenting with on-device gen AI to add new, intelligent features, promising a more personalized and adaptive user experience.60 Deloitte predicts that this new tech will help boost global smartphone shipments by 7% in 2025, as consumers explore what gen AI can do.61 Early adopters are already enthusiastic, though widespread adoption could hinge on whether gen AI can deliver genuine value. For now, gen AI offers the potential to make smartphones more intelligent and more attuned to individual needs. The coming year should be exciting for telecoms and consumers as we see how this technology transforms personal computing.

As telecoms evolve and embrace new technologies, smartphones—billions of consumers’ constant companions—are also experiencing a shift.

Amid rapid advancements in FWA, gen AI, and BSS/OSS modernization, the shift to multi-vendor Open RAN is progressing at a more cautious pace. Multi-vendor Open RAN has historically been seen as a game-changer for telecom, aiming to give mobile network operators more flexibility in choosing equipment vendors. In theory, Open RAN’s multivendor approach could allow operators to select from a wider range of providers, fostering competition and innovation. However, the reality is a bit more complex.62

Deloitte’s predictions indicate that the shift to Open RAN is expected to be slow, with no new major multi-vendor deployments likely in 2025.63 While many telecom operators are exploring Open RAN, integrating its components isn’t straightforward, and for now, the market is still dominated by a few big players.64 As part of US strategy, Open RAN is intended to boost economic security and reduce dependence on foreign suppliers, but building a fully functional multi-vendor environment will take time.65 To be clear, many of the Open RAN principles have been accepted by larger OEMs, and they are integrating these features into their products.66 While this isn’t yet multi-vendor, it could be considered “mission accomplished” for Open RAN given new innovations promised in xApps and rApps (network automation tools that maximize the network’s operational efficiency).67

While multi-vendor Open RAN faces its own set of challenges, the rollout of 5G SA networks isn't faring much better. As of March 2024, only 49 out of 585 operators had deployed or launched 5G SA networks, which offer full 5G capabilities but also require a significant financial commitment.68 Many operators are holding back on large-scale 5G SA investments, likely due to uncertainties about revenue generation. Deloitte predicts that fewer than 20 additional 5G SA networks will come online by 2025, especially as current 4G and 5G non-standalone (NSA) networks meet most application needs.69 Yet, delays in deploying 5G SA could slow 6G development, making it important for operators to consider phased investments and innovative revenue models that support future tech while meeting today’s needs.

As the telecom industry navigates these innovations and challenges, the future is a blend of promise and uncertainty. Open RAN, 5G, FWA, infrastructure modernization, and gen AI–enhanced smartphones, each represent a piece of the evolving puzzle. And while the transformation may be happening one step at a time, the future looks bright for a more flexible, efficient, and user-centered telecom industry.

Strategic questions to consider:

- How can companies design and implement a comprehensive digital transformation roadmap that seamlessly integrates BSSs and OSSs, ensuring minimal disruption to ongoing operations?

- How can companies develop a comprehensive risk management framework to address the complexities and potential vulnerabilities associated with multi-vendor Open RAN?

- What innovative use cases and applications can be developed to fully leverage the capabilities of 5G SA networks, driving new revenue streams and market opportunities?

- How can companies capitalize on the initial success of FWA to sustain long-term growth, and what strategies can be implemented to counteract the anticipated slower (but still strong) expansion rate of FWA in 2025?

- Could telcos decide to skip 5G SA altogether, and move directly from 5G NSA to 6G?

Signposts for the future

We’re taking a new approach, to the signposts for 2025: making them much more precise, quantified, and with some attempts to predict what will happen in the year for each signpost.

- After a couple of years of underperforming, both in terms of overall indices and especially tech stocks, we will be seeing how telecom stocks do. Telcos usually pay high dividends and trade at low multiples and are historically seen as defensive stocks. If 2025 has less robust market performance than the last two years, this could be a year for telcos to shine, at least on a relative basis.

- Fifteen telcos have announced that they will build gen AI data centers. Will many more follow, and what kinds of revenues will they be able to generate by selling gen AI as a service? We predict we might see a few more join, but it seems unlikely that most telcos will choose this path.

- AI RAN is a variant of the AI factory, and only a couple of telcos have started deploying it in 2024. We are skeptical that we will see mass adoption of AI RAN in 2025 but will keep our eyes open.

- We expect FWA to keep growing globally at about 20% year over year. We think it’s unlikely to do much better than that, but after a couple of years of strong growth we will be looking to see if growth weakens suddenly. We don’t think it will, but as the sole current path for 5G monetization, any unexpected FWA weakness would matter.

- Equally, we expect new multi-vendor Open RAN and 5G SA deployments to remain slow, but any surprise on the upside on either of those might suggest some big shifts in the OEM market. In our 2023 Outlook, we said that low levels of RAN spending might mean OEM consolidation. That hasn’t happened yet, but if RAN spending doesn’t pick up soon, it remains a likely outcome.

- Finally, we’re expecting our new US-only CII to record small but reasonable growth. From an estimated 127 in 2024 (up slightly from 2023) the index could creep up to 132 in 2025, although low capex and weak employment figures are likely headwinds.

{kind=link}

{kind=link}

{kind=link}