Earning trust as gen AI takes hold: 2024 Connected Consumer Survey

Consumers appreciate the benefits of digital life and are excited by the potential of generative AI, but respondents feel it’s up to tech providers to dispel lingering concerns about data privacy and security.

Jana Arbanas

Paul H. Silverglate

Susanne Hupfer

Jeff Loucks

Prashant Raman

Michael Steinhart

In this fifth edition of Deloitte’s Connected Consumer study,1 we continue to report on US consumers’ digital lives. The Deloitte Center for Technology, Media & Telecommunications surveyed nearly 4,000 US consumers in June 2024, asking them about their tech-device and -services spending, online activities, perspectives on digital life, digital boundaries, data privacy and security concerns, use of generative AI, and trust in tech companies (see “Methodology”).

In 2023, we reported that consumers were struggling to find the right balance between their digital and physical lives.2 Respondents were streamlining their household devices and cutting back on device purchases in the face of economic uncertainty. Most believed their devices made a positive impact on their lives and helped them build meaningful connections, and many continued to embrace virtual health visits and remote work. But at the same time, they were trying to manage the drawbacks of too much tech—including tech fatigue and worries about well-being and data security.

Digital activities take up a big part of consumers’ everyday lives, and this year, we’re seeing increased appreciation of their benefits. Nearly four in 10 consumers surveyed have dived into using generative AI. They’re excited by new capabilities and report that gen AI tools are helpful at work and at home. As inflation eases, respondents are more confident of their tech-spending plans, and fewer report tech-affordability issues.

But we’re also seeing greater awareness of the potential harms of digital life. Since 2023, consumers have grown more worried about data-security risks and location- and behavior-tracking. More are experiencing security failures, and more are taking protective actions. They’re also setting more boundaries on their digital use—and that of their children. Consumers are increasingly looking to tech companies to help them find the right balance, give them more control over their devices and data, and ensure that digital life is worth the effort. According to our analysis, tech companies that prioritize transparent data privacy and security policies along with ease of control may be able to earn greater consumer trust and affinity.

Digital spending plans show signs of optimism

Consumers devote a lot of time and attention to their digital experiences. On average, they spend eight hours engaging in online activities daily—about half of their waking hours. Gen Zs and millennials report spending even more time online—nine hours each day, on average—while Gen X, boomers, and matures spend seven, six, and four hours online, respectively. About seven in 10 respondents say they go online every day for general web browsing, communicating with friends and family, and using social media. Seventy-four percent of Gen Zs and 68% of millennials say they check their social media feeds at least several times a day—as do 57% of Gen Xers and 39% of boomers. Twenty percent of Gen Zs say they check their feeds at least hourly, and other research has revealed that Americans check their smartphones 144 times a day, on average.3 Sixty-one percent of consumers surveyed say they watch entertainment (movies, TV, sports) on a streaming service daily, and 48% say they listen to music or podcasts daily.

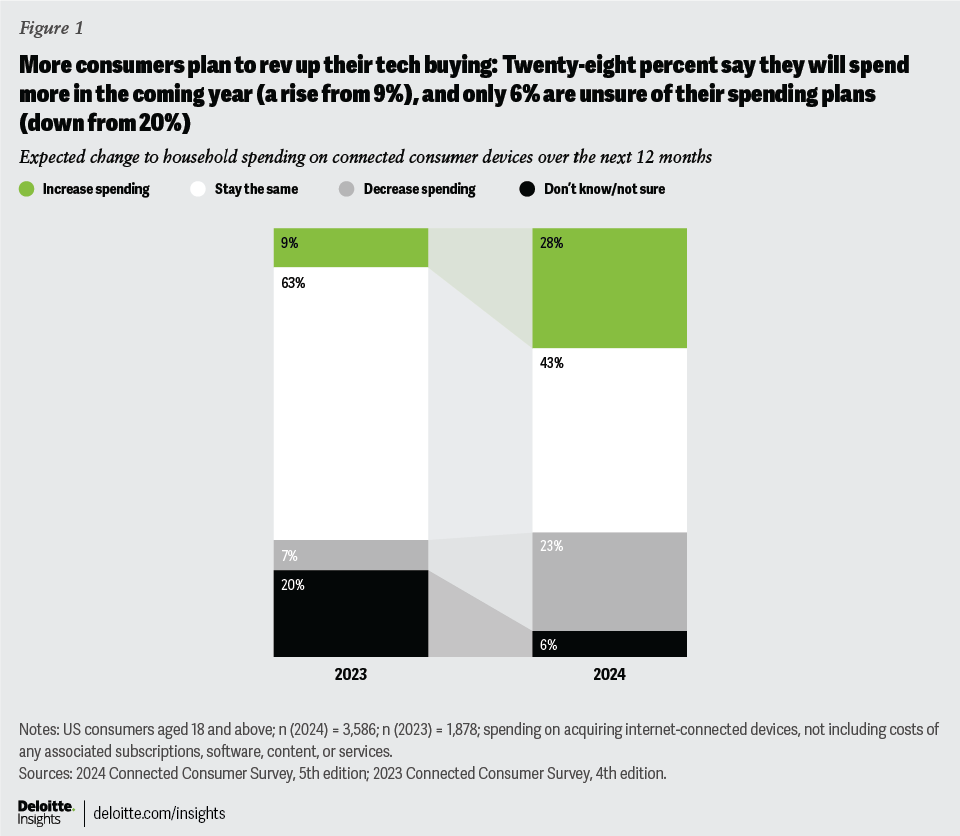

Our study shows that US households, on average, spent approximately US$760 on acquiring connected devices in the past year—a slight drop from US$800 in 2023. Following a decline in consumer technology spending between 2022 and 2023, due in part to sluggish economic growth, higher inflation, and pandemic-driven supply chain disruptions, projections foresee a comeback with a 1% revenue increase in 2024 and an additional 4.4% expected in 2025.4 Our survey confirms this positive outlook, revealing that 28% of respondents plan to increase their device spending in the coming year, up significantly from 9% in 2023, while 43% expect spending to stay the same, compared with 63% in 2023 (figure 1).

On the other hand, more people are looking to cut back on device purchases (23% compared with 7% last year), indicating ongoing financial pressures in some US households.5

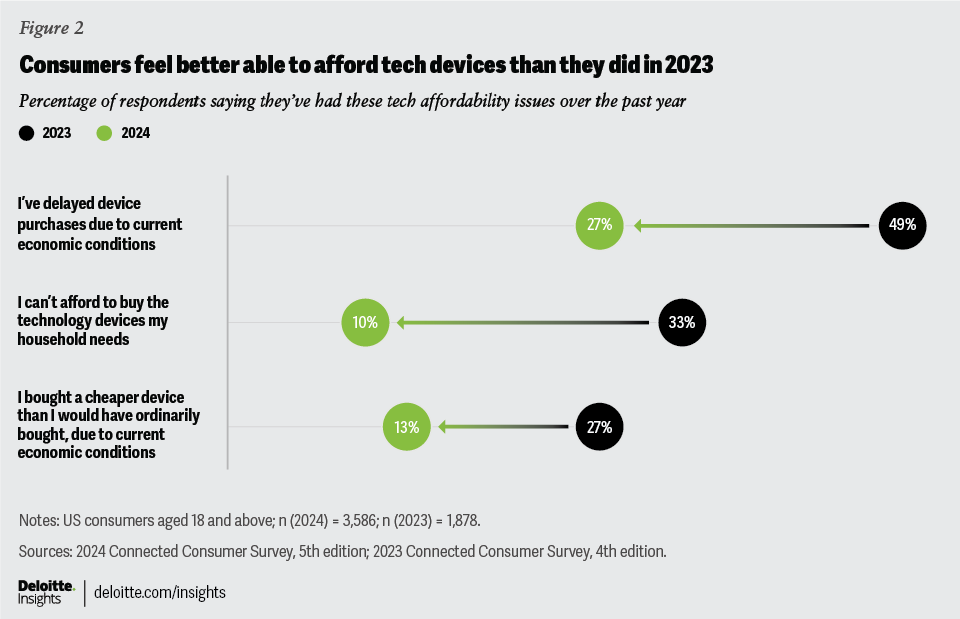

In another sign of optimism, our survey revealed that tech-affordability issues have eased significantly for many consumers (figure 2). Compared to last year, consumers are much less likely to postpone device purchases, to choose cheaper devices, or to feel like they can’t afford the technology their household needs.

As new AI technologies and features are embedded in consumer devices, the industry may see device-refresh cycles accelerate. Tech companies are beginning to sell laptops, tablets, and smartphones with embedded AI chips designed to help improve functionality (for example, summarizing information in real time, generating photos and videos, and instantly translating foreign languages).6 When asked whether AI functionality will have any effects on their plans to upgrade devices, approximately one-third of our survey respondents say they’re more likely to upgrade sooner.

Beyond purchasing tech devices, consumers also spend significant amounts monthly on tech services, subscriptions, and software. US households in our survey average US$175 on digital services like internet connectivity, mobile plans, cloud storage, and antivirus protection. We see additional signs of optimism here, too: Seventy-two percent of surveyed consumers expect to keep their spending on tech services and subscriptions steady over the next year, and 14% plan to increase it. Further, while 23% said they had cut back on tech services and subscriptions in the past year due to economic conditions, only 10% plan to decrease this spending in the coming year.

Consumers enjoy their digital lives but are realistic about potential drawbacks

Consumers love being online—engaging with social media, shopping, consuming entertainment, and building and maintaining relationships. They’re also more aware of the potential downsides of tech—checking feeds obsessively, feeling like they may be wasting time, and worrying that online activities may take a toll on their mental and physical health.

Seventy-eight percent of our survey respondents reported that digital experiences have a somewhat or very positive impact on their lives. Among teens between ages 14 and 17, 86% share this sentiment—a five-point increase from 2023. As connected devices and digital activities take hold among older consumers, their attitudes are trending up, too. Seventy-five percent of boomers and 69% of matures report positive impacts of digital experiences, up six points and 14 points, respectively, from the previous year. Across generations, the top-ranked benefits of online activities include online shopping, building and maintaining social relationships, managing daily tasks, accessing entertainment, and getting the latest news.

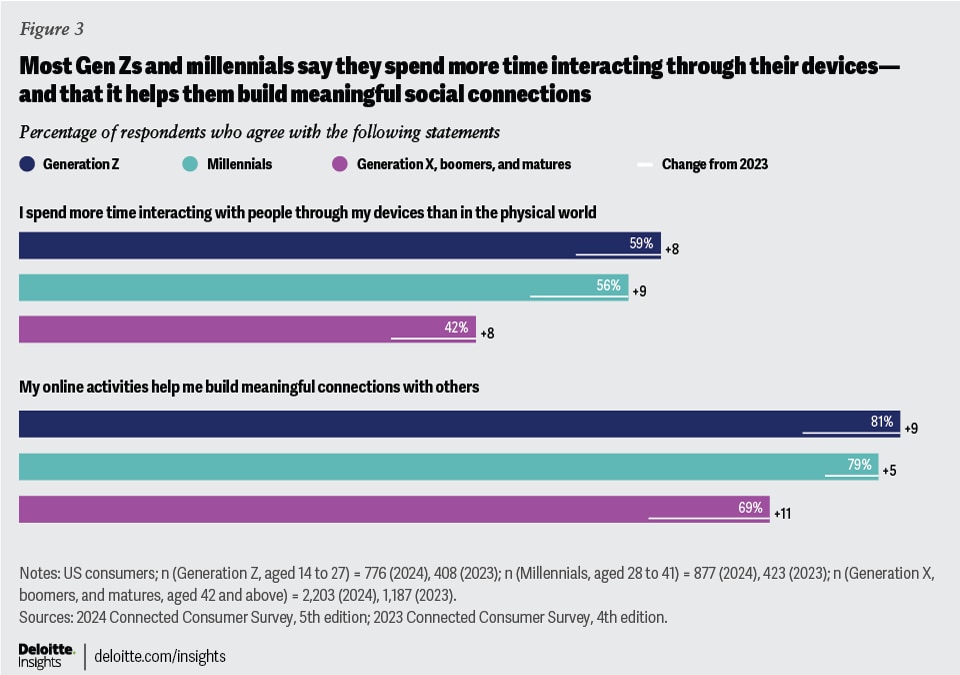

Last year, we pointed out the phenomenon of consumers spending more time interacting with people online than in the real world. This trend has intensified across age groups: Fifty-nine percent of Gen Zs, 56% of millennials, and 42% of older consumers now report that they spend more time interacting via devices than in person (figure 3). At the same time, most respondents believe that these online activities help them forge meaningful bonds: Digital relationships can be, in essence, just as “real” as face-to-face connections.

Consumers are aware of the downsides that could come with all this online time. Forty-four percent of respondents overall and 56% of Gen Zs and millennials say they struggle to limit their screen time to levels they’re comfortable with—up six and four points, respectively, from last year. Forty-two percent of respondents are concerned that their digital activities could negatively impact their physical condition, and 35% share the same concern about their psychological condition. Gen Zs and millennials worry more, with roughly half fearing potential negative effects on both their physical and psychological well-being. Overall, 37% of respondents expressed worry that their digital activities could expose them to harmful content or people (up eight points since 2023)—and 43% of Gen Zs and millennials share this concern. Thirty-one percent of respondents worry that their online time could harm their social connections and engagement in the physical world (up four points since 2023)—and 41% of Gen Zs and millennials fear the same.

In response to these worries, consumers are more actively setting boundaries around their digital activities. Eighty-three percent have put at least one measure in place (up five points from last year), and each action we asked about shows an uptick. Half say they put devices away during activities with family and friends, and the same number say they take regular breaks from screens. Thirty-six percent said they turn off notifications at select times, thirty-five percent said they take breaks from apps and accounts, and 30% keep their smartphone out of their bedrooms or set it to “do not disturb.” While they value the benefits of online engagement, consumers are taking more responsibility for their behavior and working to balance digital and offline lives.

Digital divide between parents and kids may be narrowing

Teens, who spend more time online relative to other age groups, also express the most upbeat impressions of digital life in our survey. Nearly 90% say that digital activities have a positive impact on their lives and that their online experiences help them build meaningful connections. Most parents also have favorable impressions of their children’s online activities: Sixty percent said they have a positive impact and 67% said they help children build meaningful connections.

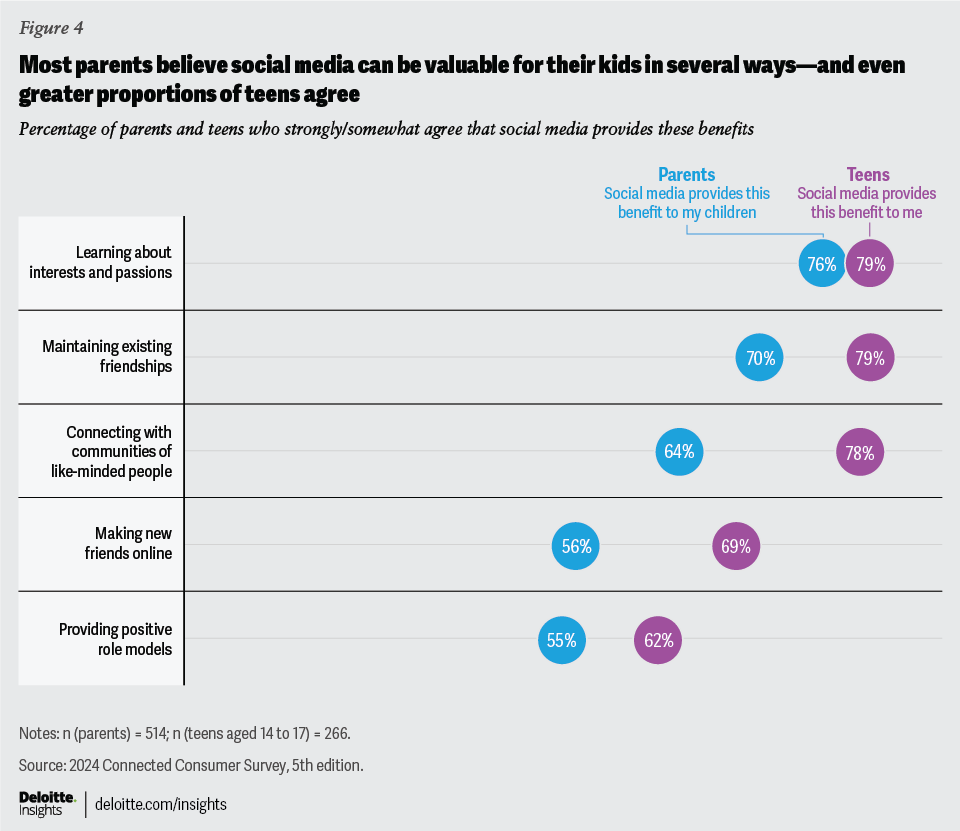

Parents and teens are also aligned on the benefits of social media (figure 4). Significant majorities of each group agree that social media helps kids learn about topics of interest, maintain friendships, and connect with like-minded communities.

However, one drawback of social media is the tendency for users to refresh feeds and scroll endlessly. In our survey, 60% of teens said they seem to check their feeds “constantly,” and 57% of parents said the same about their kids. Fifty-one percent of parents said they struggle to limit their children’s screen time to comfortable levels, and the same number of teens admitted to grappling with the issue—a seven-point jump from last year.

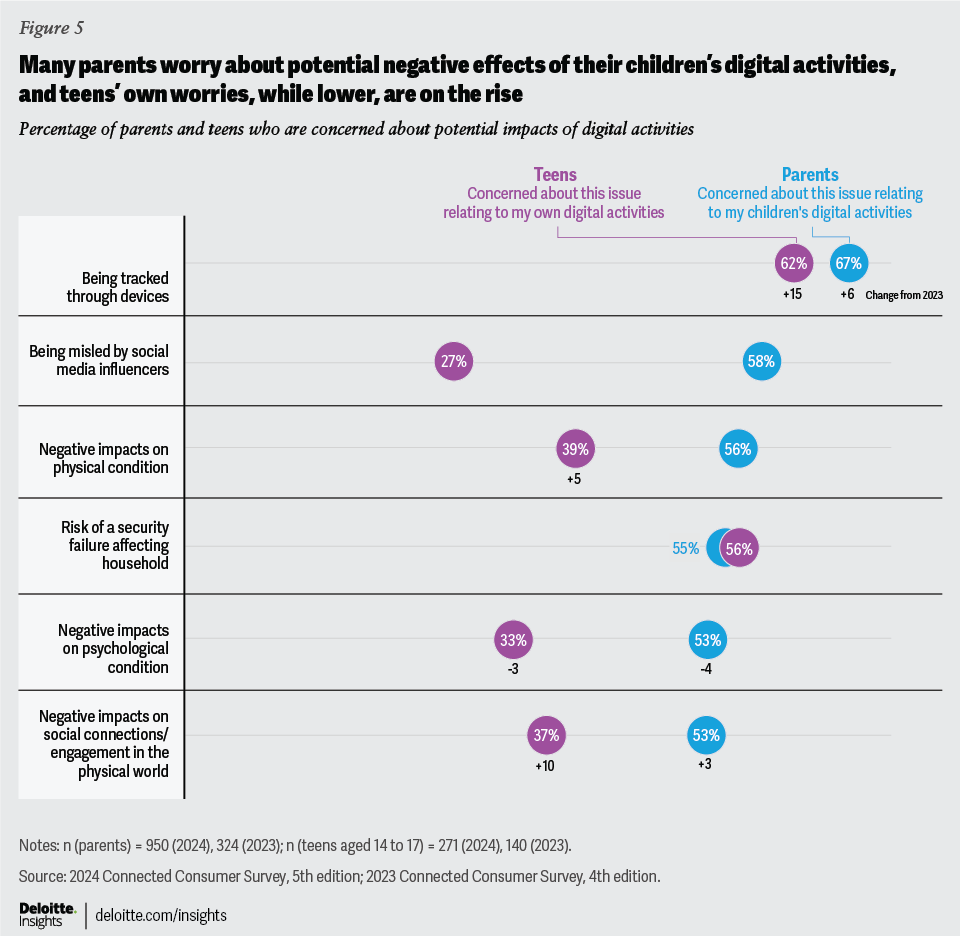

Parents and teens both worry about a range of possible harms from digital activities (figure 5). Roughly two-thirds of parents and teens alike worry about location tracking; for teens, this concern surged by 15 points in the past year. An increasing number of teens are worried about negative impacts on their physical condition and real-world social engagement, and more than half of teens and parents worry about security failures causing some leak of household data.

Much attention has been paid in the past two years to the potential for social media use to take a negative toll on teens’ mental health.7 Forty-three percent of parents who took our survey admitted that they struggle to keep up with the social networks and apps that their children use.

Roughly six in 10 parents are concerned about their children being exposed to harmful ideas, images, videos, and people online. Teens share these worries, although to a lesser extent: Forty-four percent of teens surveyed say they worry about being exposed to harmful or inappropriate content or people online. While almost six in 10 parents say they’re worried about their kids being misled by social media influencers, only about a quarter of teens share that concern. And while a majority of parents are concerned about the effects of digital activities on their kids’ psychological condition, only one-third of teens expressed the same worry—with both groups showing slight dips in concern from last year’s study.

Twenty-six percent of teens report that they’ve experienced cyberbullying or online harassment, versus 18% of respondents over 18 years of age. Compared with those who have not experienced cyberbullying, respondents who have are more likely to worry that digital activities may harm their physical condition (56% versus 38%) and psychological condition (55% versus 30%). These amplified concerns may reflect a need for better anti-bullying technologies and awareness-building among user bases of all ages.

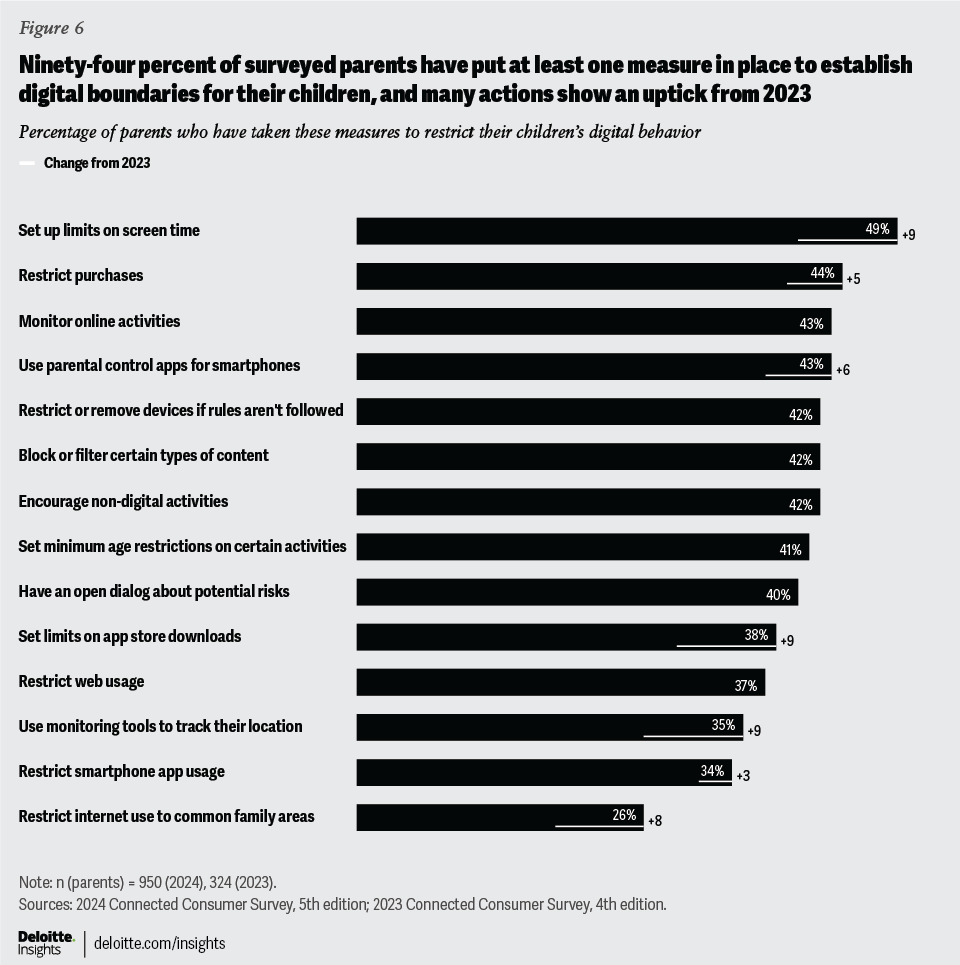

Parents are not sitting idly when it comes to online harms (figure 6). Nearly all have set digital boundaries for their children, with many measures increasing since last year. Common strategies include setting screen time limits, restricting purchases, monitoring online activities, and using parental control apps for smartphones. Forty-one percent of parents surveyed said they enforce age restrictions on certain digital activities, as endorsed by health professionals,8 such as limiting social media use, smartphone access, and unsupervised internet use for younger children.9

The data underscores a growing trend among parents to manage their children’s digital engagement more actively. Year-over-year increases may indicate heightened awareness of potential risks, easier access to parental controls, and growing concerns about online safety. The trend is positive, yet our survey shows that tech companies still have more work to do to promote safer and more inclusive digital experiences.

Generative AI gains fans and exceeds consumer expectations

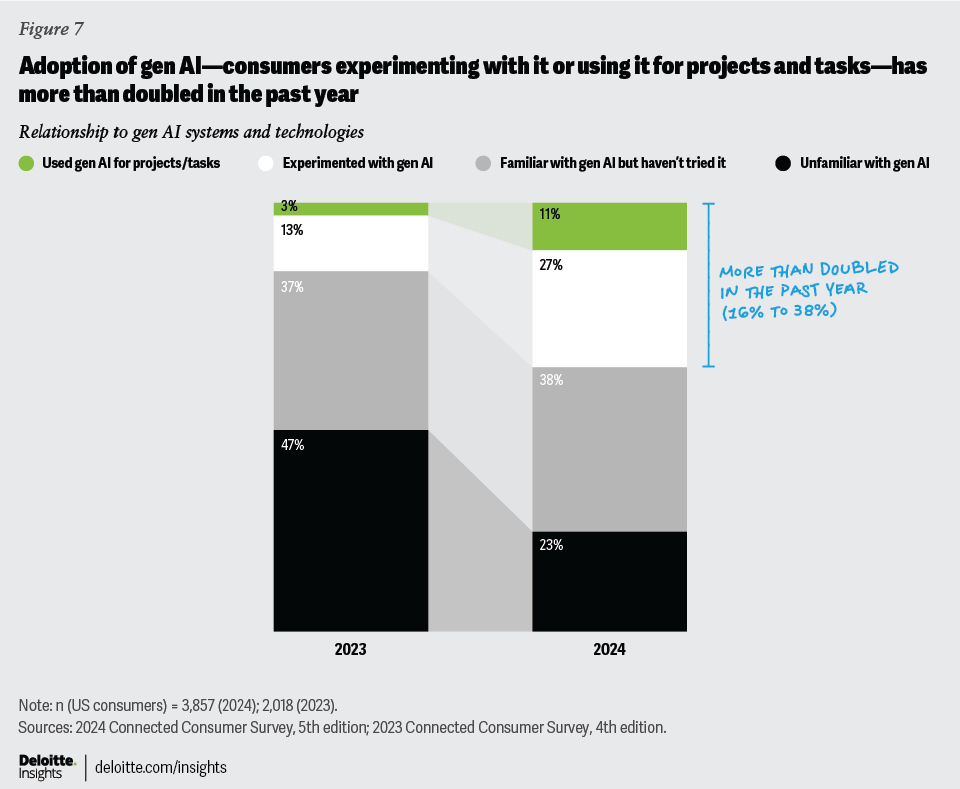

Gen AI started capturing consumers’ attention in late 2022 with the arrival of gen AI chatbots, and it’s rapidly earning a place in consumers’ digital lives.10 Adoption of gen AI has more than doubled in the last year—with 38% of respondents now saying they’ve experimented with gen AI or used it for projects or tasks beyond experimentation (figure 7). Adoption is more pronounced among younger generations, with half of Gen Zs and millennials surveyed using or experimenting with gen AI, compared with 38% of Gen Xers and 22% of boomers. Further, 42% of Gen Zs and millennials who use gen AI for projects say they do so every day.

Among users, 85% utilize gen AI for personal purposes (up 13 points from 2023), 34% for job-related tasks (up 18 points), and 24% for educational projects (up three points). The top four gen AI use cases for work and school are: document editing, web searches, summarizing materials, and research assistance. For personal use, document editing and web searches remain popular, while chatbot conversations and image generation round out the top four uses.

Professional use of gen AI has seen a sharp increase over the past year: Our 2024 survey finds 24% of employed respondents saying they experiment with or use gen AI for work purposes, compared with just 6% of employed respondents in 2023. This jump could suggest that many employers are embracing the potential of gen AI in the workplace. Many workers use gen AI with their employer’s encouragement and training, viewing it as a productivity booster. Seventy-five percent of those who use gen AI for work report that their company encourages its use, and 68% say their company invests in gen AI training for employees. A decisive majority (83%) of those who use gen AI on the job believe it boosts their productivity—with 53% reporting a “substantial” boost.

The rapid adoption and integration of gen AI into workflows is also reshaping user expectations and satisfaction, with most respondents reporting positive experiences. Two-thirds of gen AI users said it exceeds their expectations, and one-third said it’s “significantly better” than expected. Gen Z and millennial users seem especially enthusiastic, with 70% saying gen AI exceeds their expectations and 39% calling it “significantly better” than expected. Overall, only 8% said gen AI is worse than they expected. The high satisfaction rate earned by gen AI underscores its potential to enhance productivity and innovation.

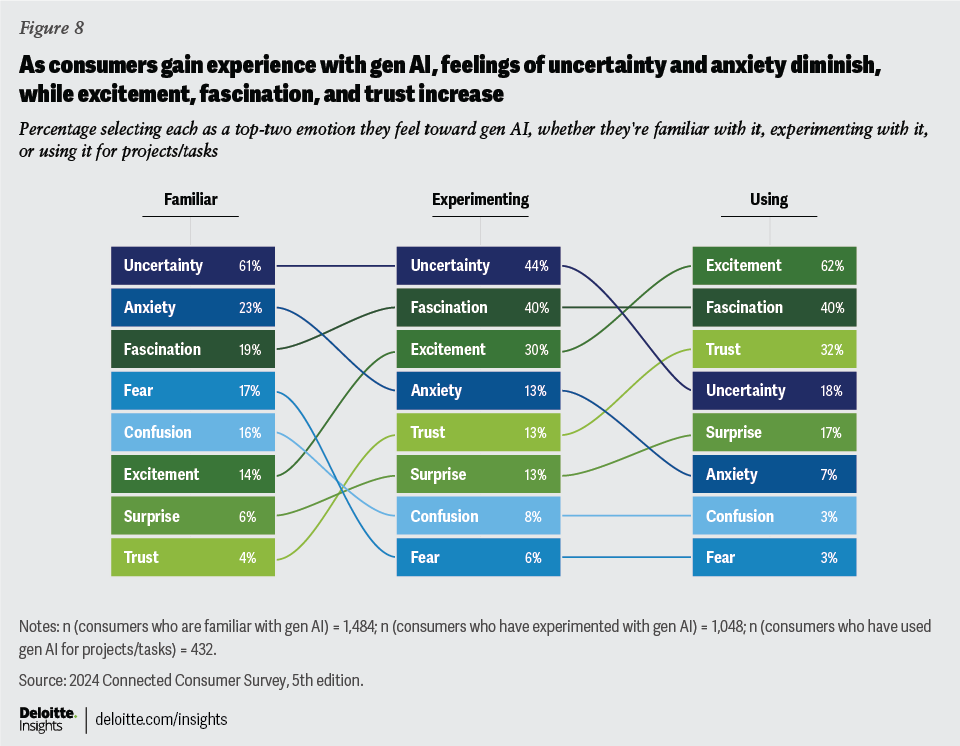

Consumers’ feelings toward gen AI appear to transform as they gain more experience with the technology (figure 8). For respondents familiar with the concept, but who haven’t yet experimented with gen AI, emotions of uncertainty and anxiety are paramount, followed by fascination. As users begin to experiment and then start using gen AI for projects and tasks, initial apprehension gives way to greater fascination and excitement. Very few respondents feel “trust” toward gen AI before they use it, but for regular users, trust is the No. 3 emotion. There’s still room for trust to grow, however; only a third of regular users selected it.

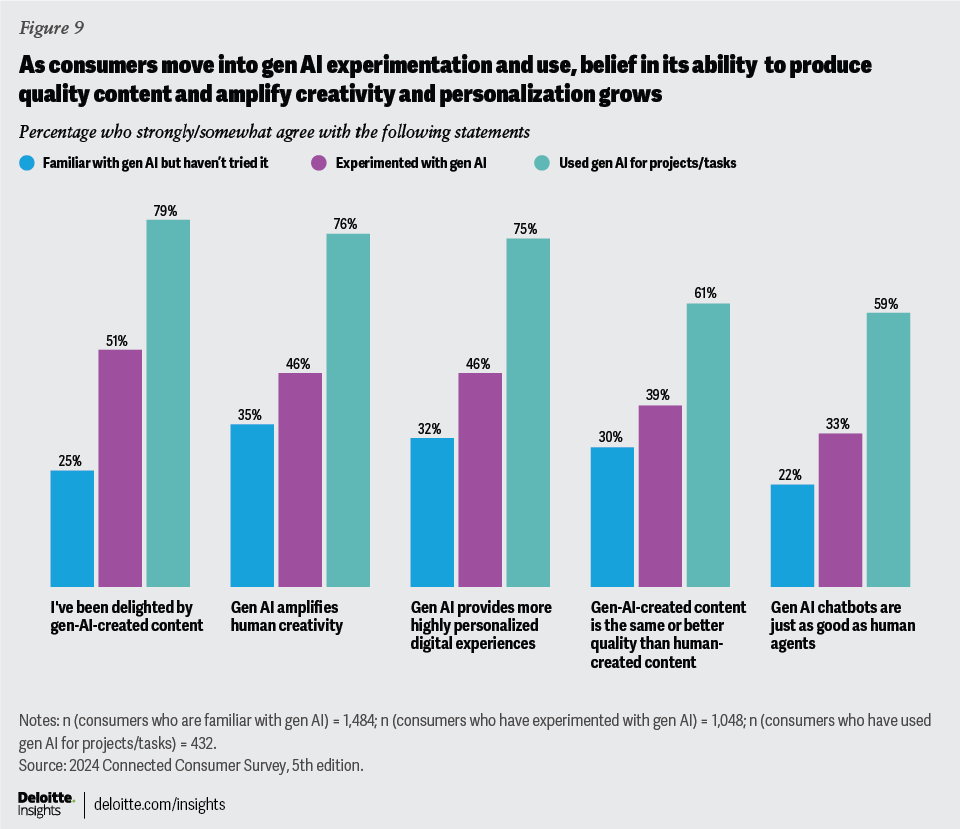

Hands-on use of gen AI for projects or tasks appears to drive positive impressions of the technology (figure 9). Generative AI users generally view the technology positively, believing it enhances creativity and offers highly personalized experiences. Many users think AI-created content matches or surpasses human-created content and that AI chatbots are as good as human agents. Those who are experimenting with gen AI but not yet using it for actual projects and tasks aren’t yet as convinced of its potential.

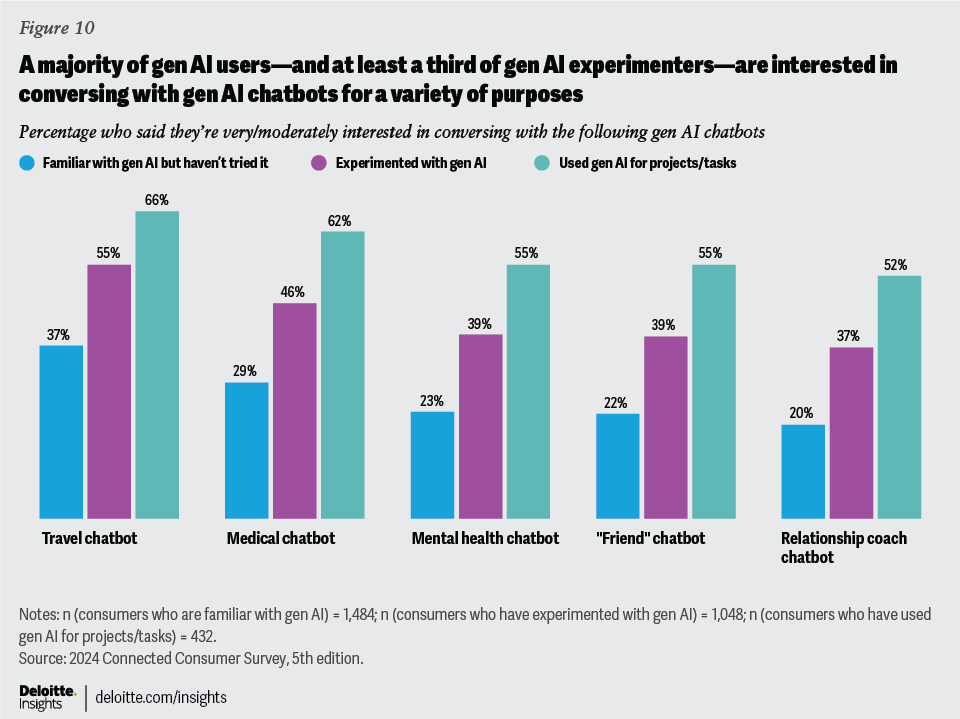

Gen AI’s ability to deliver highly personalized experiences and human-like conversations is reshaping how consumers interact with technology. When it comes to engaging with gen AI-based chatbots for personal issues, Gen Zs and millennials are about twice as likely as older generations to say they’re interested in talking to a chatbot “friend” (44%, vs. 23%), relationship coach (42%, vs. 21%), or mental health counselor (44%, vs. 24%). Here, too, the more experience users have had with gen AI, the more comfortable they are with the idea of conversational AI (figure 10). Indeed, for gen AI users across generations, their willingness to talk with gen AI chatbots about personal medical topics (62%) is nearly as high as their interest in talking with chatbots about less-sensitive travel plans (66%), and a majority expressed interest in talking with gen AI chatbots for mental health support, friendship, and relationship advice.11

This highlights a growing comfort level with turning to AI for nuanced interactions that used to require human intervention. Our survey also revealed that nearly two-thirds of users are interested in using gen AI for personalized fitness and nutrition plans, shopping help, and financial guidance. The landscape seems to be shifting toward AI-enhanced solutions that are customized to meet individual preferences and needs.

Amid growing data privacy and security concerns, tech companies can work to earn trust through transparency

‘Hacking and tracking’ worries are on the rise

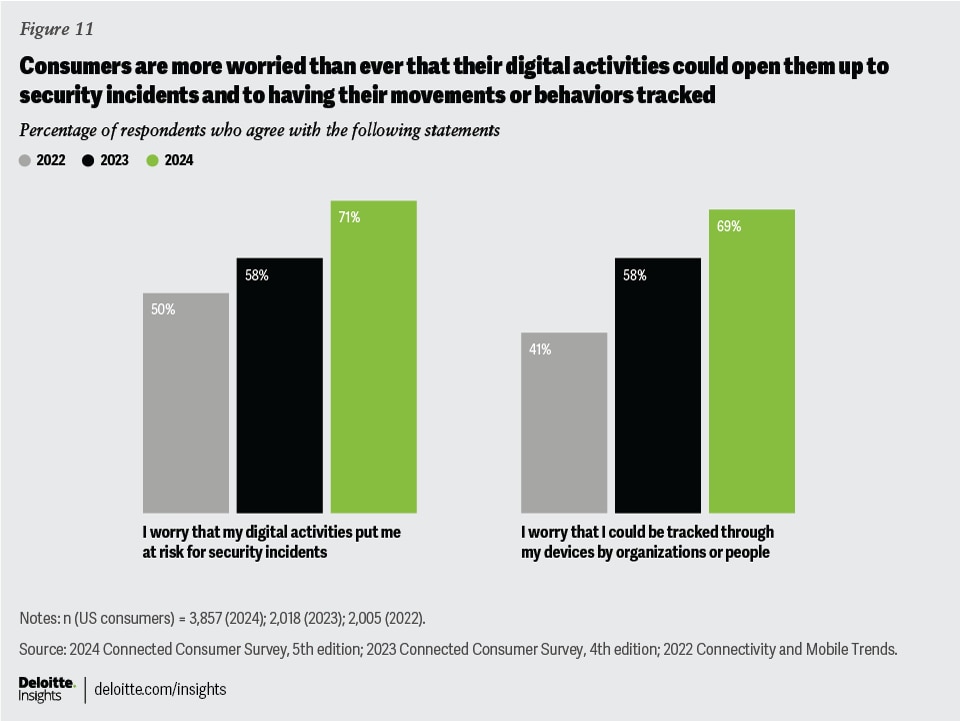

In last year’s report, we discussed consumers’ growing concerns that digital activities put them at risk of security incidents and tracking by organizations or individuals. This year, the worries seem to be intensifying (figure 11). Moreover, tracking fears are increasing among both parents and teens. Sixty-seven percent of parents said they worry that their children may be tracked through their devices (up from 61% in 2023), and 62% of teens between ages 14 and 17 are concerned that they could be tracked (a jump from 47% in 2023).

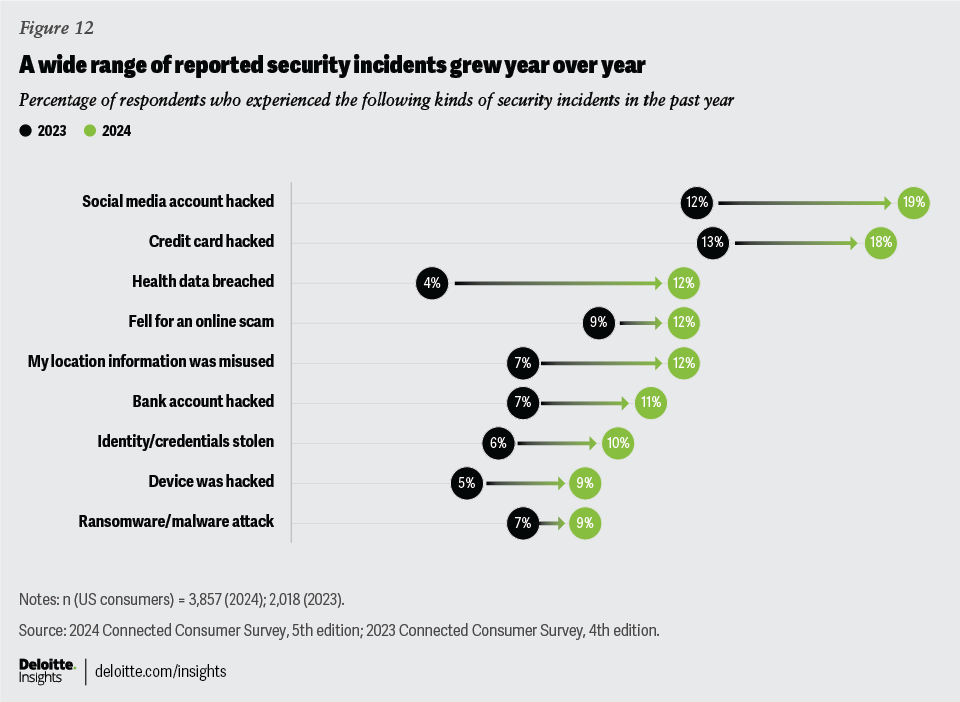

These growing fears appear warranted in light of expanding security threats. The number of breaches reported in the first half of 2024 is outpacing the same period last year by 14%, affecting an estimated one billion people.12 Almost half (48%) of our survey respondents experienced at least one kind of security incident in the past year—a jump from 34% in 2023. Twenty-seven percent suffered two or more kinds—up from 16% in 2023. Across a range of potential security incidents surveyed, each type showed an uptick (figure 12).

While older adults may be considered ripe targets for digital scams, our analysis revealed that Gen Zs in our survey were actually more likely to fall victim to security incidents.13 Reflecting on the past year, Gen Z respondents were more than twice as likely as boomers to say their social media account was hacked (29% versus 12%), they fell for an online scam (17% versus 7%), their location information was misused (17% versus 6%), their identity or credentials were stolen (13% versus 6%), or their device was hacked (12% versus 4%). Reasons for the heightened vulnerability include Gen Z spending more time online, as well as a tendency to engage with more apps and share personal information more freely.14

Consumers shore up defenses—but many feel it’s an uphill battle

Facing the persistent threats of hacks and scams, consumers are getting better at strengthening their defenses. This year, 85% of respondents reported that they had taken at least one action in the past year to address concerns around data security (up from 79% in 2023 and 71% in 2022); and 45% had taken four or more (up from 28% in 2023 and 21% in 2022). On average, respondents took 3.7 actions out of 17 that we probed.15

The top defensive actions are: implementing two-step authentication for apps and services (42%); blocking a website from installing cookies or cleaning browser cookies regularly (39%); turning off location-based services on a device (38%); changing privacy settings on browsers, applications, or social media accounts (34%); using software to enhance security (27%); and turning off Bluetooth on a device (26%).

Consumers also indicate they’re ready to turn off services if they’re uneasy about security. Nineteen percent said they had paused or deleted a social media account in the past year (up four points from 2023), and 20% said they had deleted another type of account (up six points from 2023). Over one-third (35%) said they don’t feel that the benefits they get from online services outweigh their data-privacy concerns.

Much as last year, seventy-five percent of our survey respondents feel they should be taking more steps to protect their data, but they reveal it’s an uphill battle. The top reasons they gave for not doing more indicate a sense of futility: Twenty-six percent feel that companies can track them, and 21% feel hackers can hack them, no matter what actions they take.16 Mirroring 2023, 25% indicated that they don’t know what protective actions they should take. Financial considerations are an issue, too: Sixteen percent reported not wanting to pay for software or services to increase protection.

Users want more control over their data and more help from tech companies

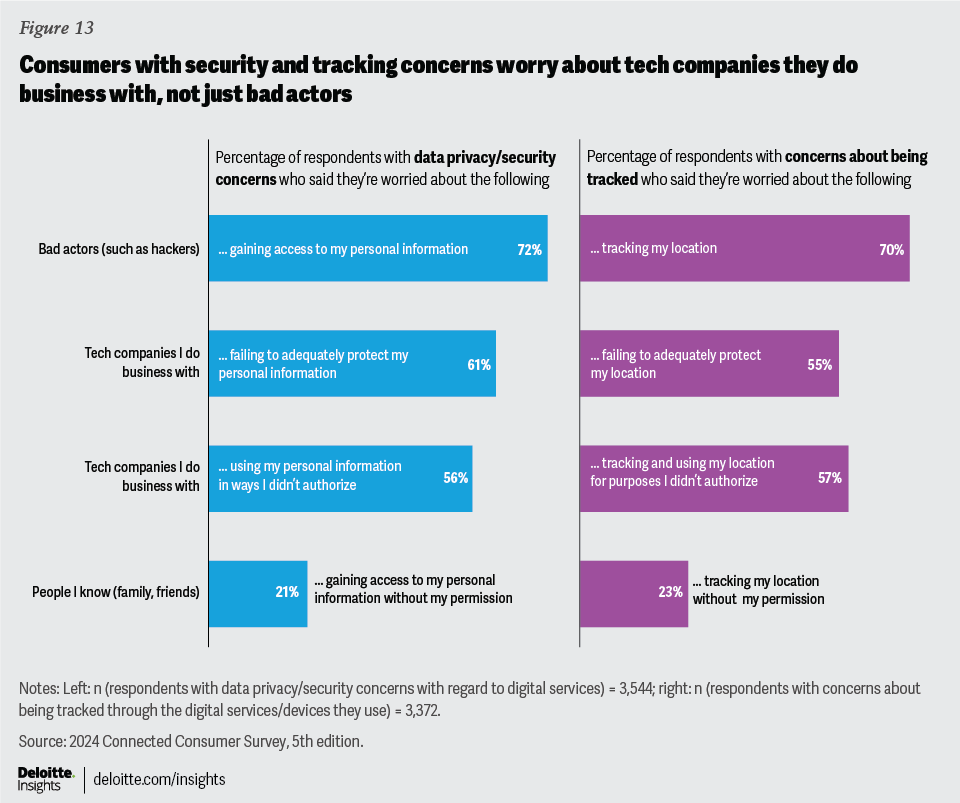

It’s not just hackers who are fueling these worries (figure 13). Most respondents worry about unauthorized access to their personal information by bad actors; a majority also worry about potential data breaches or unauthorized use of their personal data within tech companies themselves. On top of that, 21% worry about friends or family gaining access to their personal information without permission. Location tracking is another significant concern, with individuals expressing fear of being tracked by various entities including bad actors, tech companies, and people they know. Teens, in particular, are anxious about unauthorized access and tracking by friends or family: Thirty-two percent of teens with data privacy concerns worry that friends or family could access their personal information, and 29% of teens with location tracking concerns worry that friends or family could track them.

Consumers overwhelmingly want better data protection and control over how their personal data is used. Ninety-one percent believe they should be able to view and delete the data that companies collect about them, and 83% feel they deserve to be paid by companies that profit from it.

Ninety percent of respondents believe that device makers should do more to protect data privacy and security (up five points from 2023), and the same number feel that application and online service providers should do more. Eighty-four percent want the government to do more to regulate the way companies collect and use consumer data (up seven points from 2023).

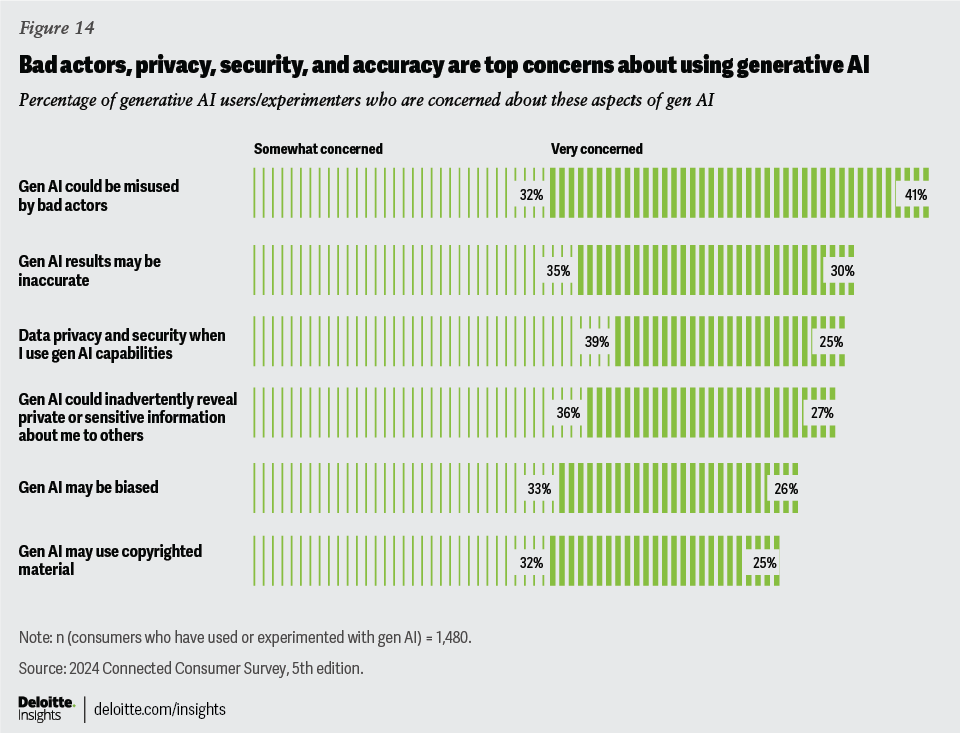

Gen AI users worry about data privacy and security, as well as misuse

For those experimenting with or using gen AI, the biggest concern is potential misuse of the technology by bad actors, and many also worry about the privacy and security of their personal information (figure 14). Other concerns include the potential for inaccuracies in gen AI outputs, algorithmic biases, and copyright violations. Eighty-one percent of those using or experimenting with gen AI believe that tech companies should take more action to address these risks, and 76% say the government must do more, as well.

Transparency and ease of control correlate with higher trust and higher spend

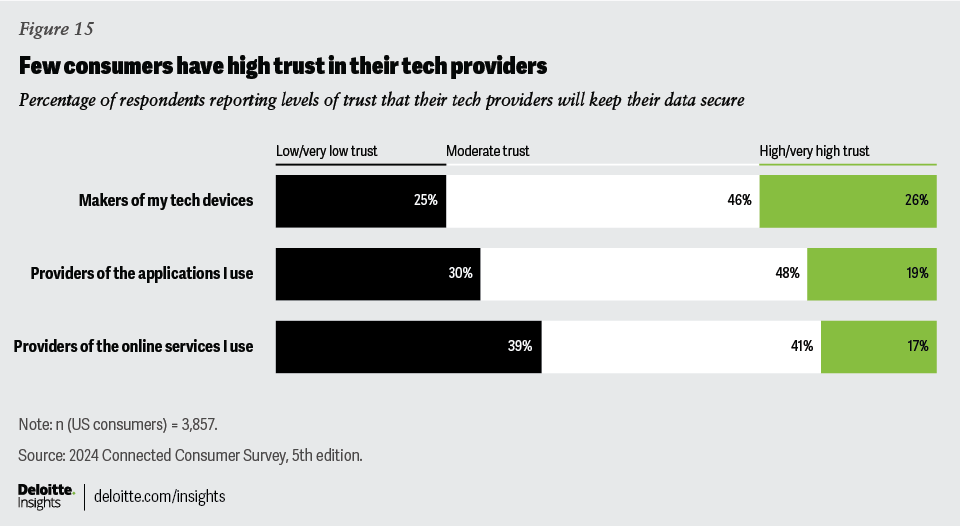

In last year’s study, we noted signs of decreasing consumer trust in tech companies selling devices and services. This year, we probed deeper and found that few consumers have “high” or “very high” trust that their tech providers will keep their data secure (figure 15). To help build trust, tech companies should take actions to address consumer concerns around hacking and tracking. The competitive stakes could be significant: Nearly two-thirds of respondents (64%) said they would be very or somewhat likely to switch to a new tech provider if an incident diminished their view of a current provider’s trustworthiness (for example, a breach of personal information, or misleading consumers about how their information is used).

There are notable generational differences around trust: Thirty-four percent of Gen Zs and millennials say they have high or very high trust that device makers will protect their data, compared with just 20% of older consumers. On average, 27% of Gen Zs and millennials report high or very high trust in application providers and online service providers. But just 12% of older consumers say the same. Convincing older consumers to purchase and make greater use of digital technologies (such as GPS tracker watches, fall detection, smart lights, home monitoring systems) could depend partly on earning greater trust. Gender differences are also significant: Thirty-one percent of men trust device makers, versus 22% of women. Twenty-four percent and 22% of men trust application providers and online service providers, respectively—compared with just 15% and 13% of women. With women controlling or influencing an estimated 85% of consumer spending, tech companies should work to builder greater trust among this powerful cohort.17

Building trust may depend at least partially on improving the transparency of tech companies’ data privacy and security policies, as well as making it easier for consumers to control their personal data. As consumers go about their digital activities—interacting with tech devices like smartphones, smart watches, and smart home gadgets, as well as engaging with apps and services such as e-commerce sites and social media networks—they’re constantly revealing personal information, such as location, behavior, purchasing preferences, social contacts, and demographics. When asked to reflect on their tech providers’ data privacy and security policies, 79% say those policies are not very clear—that their device makers, app providers, and online service providers don’t make it very easy to understand what data they collect and how they use, share, and protect it. Further, 79% feel it’s not very easy to control the data that their tech providers collect about them, such as limiting what gets collected and saved, and customizing how it may be used.

There’s room for tech providers to improve both the transparency of their data policies and the ease of controlling user data—and a potentially big upside when it comes to trust. As figure 16 illustrates, 26% of our survey respondents feel that their tech providers supply clear data privacy and security policies and make it easy for them to control their data. Fifty-two percent of that cohort report high or very high trust that their tech providers will keep their data secure, and only 10% report low or very low trust. In contrast, 44% of respondents rate their tech providers’ data privacy and security policies as unclear and feel that it’s difficult to control their data. Only 5% of this cohort reports having high or very trust in their tech providers, while 52% report low or very low trust.

In addition to helping with customer retention (as mentioned earlier), higher trust levels also correlate with tech spending: Consumers with high or very high trust in their tech providers spent approximately US$1,040 on connected devices in the past year (versus about US$695 spent by consumers with low or very low trust). Forty-eight percent expect to increase their tech device spending over the next year, versus 23% of those with low or very low trust.

Building trust in gen AI

When we looked more closely at consumers who experiment with or use gen AI, only 17% of these adopters say that their gen AI providers are “very clear” about data privacy and security policies and facilitate “very easy” control over their data. Just as we discussed above, perceptions of high clarity and control seem to translate into increased trust: Among this group, 69% express high or very high trust in their gen AI providers’ ability to secure their data, while just 8% report low or very low trust. In contrast, among the 83% of gen AI users and experimenters who don’t consider their providers’ policies on data privacy and security to be very clear or who find it hard to control their data, only 16% report a high or very high level of trust, while 44% report low or very low trust. This disparity highlights a path forward for gen AI providers: To help earn user trust and broader acceptance, they should not only enhance the security features of their offerings but also work to ensure that these data policies are communicated clearly and that it’s easy for users to exert control over their data (for example, to limit or customize what data gets collected).

The increasing ubiquity of AI-generated content is stoking another kind of consumer trust issue. Half of respondents said they’re more skeptical of the accuracy and reliability of online information than they were a year ago. Among those familiar with or using gen AI, 70% agree that AI-generated content makes it harder for them to trust what they see online. Nearly as many (68%) of these respondents harbor concerns that AI-generated content could be used to deceive or scam them, highlighting a growing wariness of the technology's implications. Furthermore, 59% admit difficulty in distinguishing between content created by humans and that generated by AI, underscoring the need for clear demarcations in AI-generated content. Eighty-four percent of consumers familiar with gen AI advocate for mandatory labeling of AI-generated content, reflecting strong consumer demand for transparency to help navigate the complexities of digital information authenticity.

Our research indicates that tech companies should do more to strengthen data security and clarify their data collection and utilization policies, while also streamlining consumer control over this information. Tech providers can engage users at suitable moments to permit informed decisions regarding their data.

Considerations for tech companies

Consumers enjoy myriad benefits from their digital experiences, but they’re very aware of the potential drawbacks—and would like more help from their tech providers. For their part, tech companies have an opportunity to build a safer and more inclusive digital world:

- Fears about hacking and tracking have gone up year over year. Device makers, app providers, and online services have an opportunity to build more trust and affinity by enhancing data security measures and communicating transparently about data-handling practices.

- Almost every respondent says they want more choice about how their data is used. Tech companies can streamline that process and give consumers easy-to-understand settings and options to limit or customize what data gets collected and saved, whether it’s shared with other parties, and how it’s used.

- Parents and teens worry about a range of possible harms from digital activities, and we noted a correlation between experiences of cyberbullying and fears about negative impacts on physical and mental health. Social networks, especially, have an opportunity to invest in real-time monitoring of content and exchanges on their platforms, especially among younger users, to reduce instances of cyberbullying and access to harmful content.

- On the gen AI front, adoption continues to accelerate, along with concerns about data collection and misuse of the powerful technology. The providers that label content clearly and communicate their data policies transparently may earn greater consumer trust and help shape the space for gen AI tools going forward.

Enhancing transparency and trust isn’t just the right thing for tech companies to do—it could pay dividends by boosting device sales, accelerating adoption of new technologies, and conferring a competitive edge as consumers grow more discriminating.

Methodology

To understand consumer attitudes toward digital life, the Deloitte Center for Technology, Media & Telecommunications conducted a survey of 3,857 US consumers in the second quarter of 2024. This is the fifth annual edition of the survey. All data was weighted to the most recent US census to arrive at a representative view of US consumers’ opinions and behaviors. To gain a more detailed understanding of various consumer groups, we also segmented respondents into generational groups defined by their birth year: Generation Z (1997 to 2009), millennials (1983 to 1996), Generation X (1966 to 1982), boomers (1947 to 1965), and matures (1946 and prior). “Teens” refer to respondents between the ages of 14 and 17 years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}