Balancing act: Seeking just the right amount of digital for a happy, healthy connected life

Connected consumers feel digital fatigue, but want well-being, data privacy and security from their devices. The “just right” balance between virtual and physical worlds remains elusive.

Jana Arbanas

Paul H. Silverglate

Susanne Hupfer

Jeff Loucks

Prashant Raman

Michael Steinhart

Consumers embrace connected devices and virtual experiences for the long term

Our 2023 study finds that consumers are optimizing their tech usage to find the right balance between digital and physical worlds.

In this fourth edition of Deloitte’s Connected Consumer Study,1 we continue to report on US consumers’ digital lives. We researched their attitudes and behaviors around adopting connected consumer devices (technology, entertainment, and smart home), engaging in virtual experiences (remote work and learning, virtual health care visits), using wearables and smartphones to improve health and well-being, and enhancing home and mobile connectivity with 5G (see sidebar).

In our 2021 Deloitte Connectivity and Mobile Trends report, we explored how many consumers, who had been plunged into a pandemic, adapted to their homes becoming headquarters for virtual working, learning, fitness, health care, shopping, socializing, and entertaining. They purchased new devices, upgraded their networks to improve connectivity, and made the best of a difficult situation. Our 2022 report found that, with fewer people working and learning from home, pressure on people, devices, and networks had diminished. Many of the acute challenges of virtual experiences and connectivity improved.2 Consumers were gaining mastery over their digital lives, optimizing the devices they use, and choosing to move forward with the virtual experiences that held the most value for them.

Sources: Deloitte ConsumerSignals; US Bureau of Labor Statistics.

Place holder for notes:

Table of contents

- Introduction: Consumers embrace connected devices and virtual experiences for the long term

- Digital life often delivers daily benefits, but can also fuel tech fatigue and well-being worries

- Consumers seek the “just right” balance between digital and physical worlds

- Data privacy and security worries are on the rise, while trust is down

- Consumers make their homes smarter, with a focus on security

- Hybrid workers seek the best of in-office and remote work

- Remote learners gain experience and find success with virtual classes

- Virtual health and fitness find their rhythm

- Future of 5G: Consumers have rapidly adopted 5G, but are waiting for killer apps

- Epilogue: Immersive 3D and generative AI are shaping the digital future

About the survey

To understand consumer attitudes toward “digital life,” the Deloitte Center for Technology, Media & Telecommunications surveyed 2,018 US consumers in Q2 2023. This is the fourth annual edition of the survey, which was previously known as Connectivity and Mobile Trends. Aspects of digital life that the survey covered include devices (technology, entertainment, smart home, smartphones), connectivity (home internet and mobile), virtual experiences (work, school, and health care), wearables (fitness trackers and smart watches), and challenges of managing it all. All data was weighted to the most recent US Census to arrive at a representative view of US consumers’ opinions and behaviors. To gain a more detailed understanding of various consumer groups, we also segmented respondents into generational groups defined by their birth year: Generation Z (1997–2009), Millennials (1983–1996), Generation X (1966–1982), Boomers (1947–1965), and Matures (1946 and prior).

Our 2023 survey finds that, like a modern-day Goldilocks, consumers are struggling to find the right balance between their digital and physical lives. They’re continuing to streamline their household devices, and in the face of economic worries, they’re slowing device purchases. Many have embraced virtual experiences for the long term. At the same time, they’re trying to manage the drawbacks of too much tech—and where they can use tech companies’ help.

Streamlining devices

It’s no surprise that consumers continue to rely heavily on digital devices. However, they’re also still streamlining the devices they own, aiming to maximize benefits while minimizing downsides. We found that, on average, each US household now has 13 device types and 21 devices—each down one from last year. This represents further pruning from the pandemic peak of 2021, when households had 25 devices on average.3 According to respondents, the top reasons for removing devices were that their functionality could now be handled by other devices, they were too costly, or they were too outdated.4

Mastering virtual experiences

Even as 2023 marks a continued return to in-person experiences, the pandemic has led to lasting changes in consumer behavior. People are choosing to carry on with virtual experiences that have worked well for them, including remote work and learning, and attending virtual medical appointments. They have continued to become more proficient at these, but here too, many are still striving to find just the right balance between their virtual and physical worlds.

As many employers urge or even require at least a partial return to offices,5 many workers have embraced hybrid working models (a mixture of in-office and remote work): More than half of our respondents worked at least partially remotely over the past year. Nearly a quarter of households have at least one member learning from home at least some of the time.6 Both remote workers and learners say that challenges of communication, culture, distractions, and stress have improved. When it comes to accessing health care, virtual visits have dipped from their pandemic highs, but satisfaction with such visits has increased steadily. Consumers continue to use wearables, but their focus has shifted from monitoring health metrics to tracking fitness.

Virtual experiences endure by choice, if no longer by necessity: At least two-thirds of those who engaged in virtual work or school over the past year would like remote or hybrid options in the future, and a majority of those who have had virtual health care visits said they prefer remote or hybrid options for certain kinds of health visits in the future, such as for therapy, counseling, and chronic conditions.

Managing the downsides of tech

Most respondents say their connected devices have a positive impact on their lives and help them build meaningful connections (fostering relationships with friends, family, or communities with shared interests). But too much time spent on devices can also stoke tech fatigue and concerns around well-being, data privacy, and security.

Since last year’s survey, consumers have grown more worried that their devices could open them up to security breaches and to having their movements or behaviors tracked. Moreover, households with greater numbers of devices report higher levels of well-being concerns and more data breaches. Indeed, people may be hitting a “device ceiling,” where they may not view adding more devices as bringing enough benefit to make up for the cost, security concerns, and maintenance challenges.

This suggests an area where tech companies can help consumers find the right balance. By making devices more affordable, simpler to secure and interoperate, and easier to set aside when one needs a break, tech providers can help consumers get the most out of their digital devices and experiences—without being overwhelmed.

There’s also a red-flag warning for tech companies: As consumers struggle to protect their data, their trust in tech has declined from 2021 levels. Consumers surveyed want more security and control over their data, but they’re less likely to feel that they’re getting it. Tech companies should double-down on efforts to shore up consumer trust in their devices and services—for example, by enhancing data security measures, communicating transparently about their data-handling practices, and giving consumers more choice over how their data is used.

Slowing device purchases

Facing the economic pressures of 2023—high inflation, risk of recession, and personal financial worries—consumers are tapping the brakes on device purchasing. According to Deloitte’s Global State of the Consumer Tracker, 38% of US consumers feel their financial situation worsened over the past year.7 In our survey, nearly half (49%) of our respondents said they have delayed device purchases in the past year, and 33% feel they can’t afford to buy the tech devices their household needs (up from 25% in 2022).

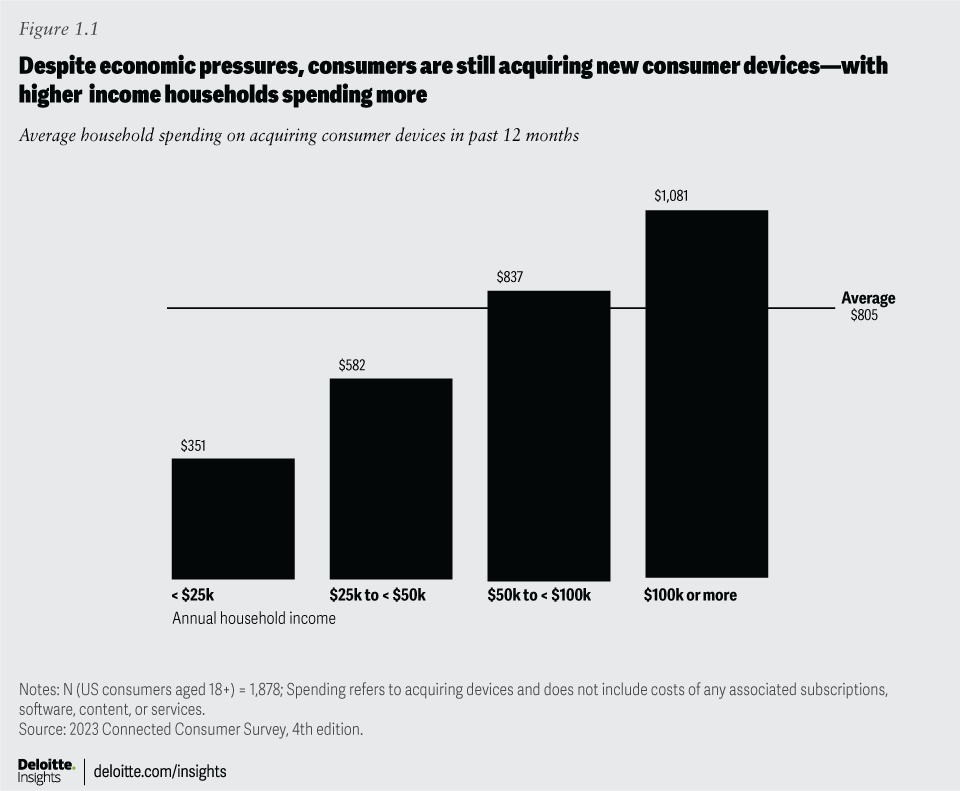

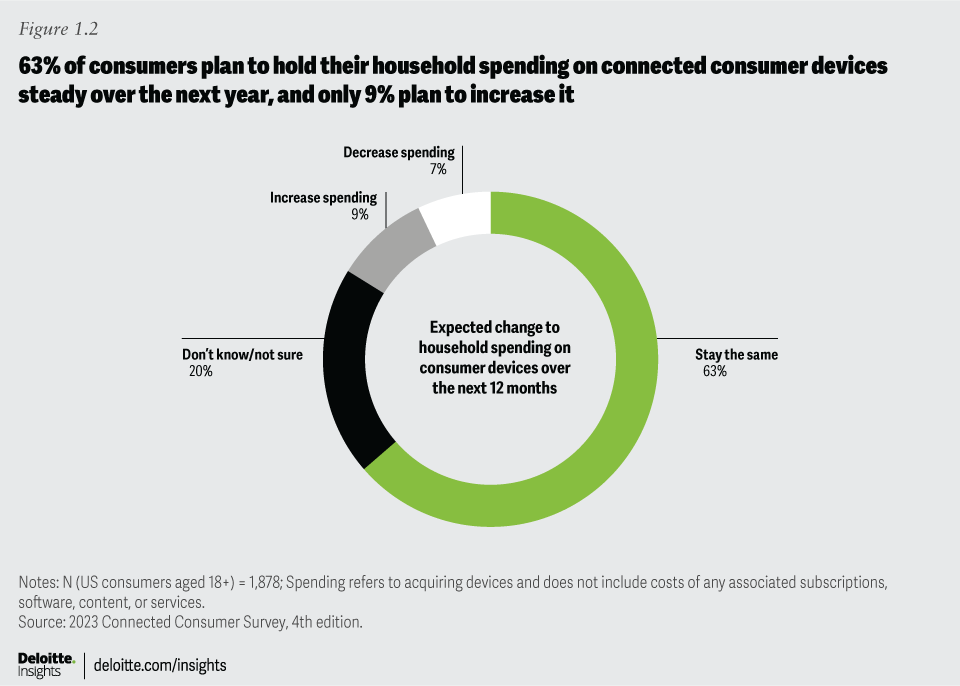

Consumers haven’t closed their wallets entirely, however: Over the past year, 32% have purchased one or two connected devices and 16% purchased three or more. Only three in 10 respondents have bought cheaper devices than they would have purchased ordinarily. Our research found that, on average, US households spent approximately US$800 on acquiring connected devices in the past year (figure 1.1). Looking toward the next 12 months, most consumers (63%) expect their device spending to remain steady, and 7% expect to reduce spending (figure 1.2).8

Since we sounded the alarm last year about privacy and security, screen overload, and tech fatigue,9 consumer discontent seems to have gotten worse. Technology companies, device makers, app developers, and service providers all have an opportunity—some might say an imperative—to help make consumers’ digital lives easier, safer, and more sustainable. If they can make devices easier to use and administer, aid users in controlling their screen time, make data security and privacy simpler to understand and manage, and give users more control over their own data, they may be able to build trust and differentiate themselves in a crowded market. If they fail to meet consumer needs, however, disruptors may step in to take advantage of the opportunity.

Digital life often delivers daily benefits but can also fuel tech fatigue and well-being worries

People rely on technology devices and appreciate their benefits, but “too much digital” can have drawbacks.

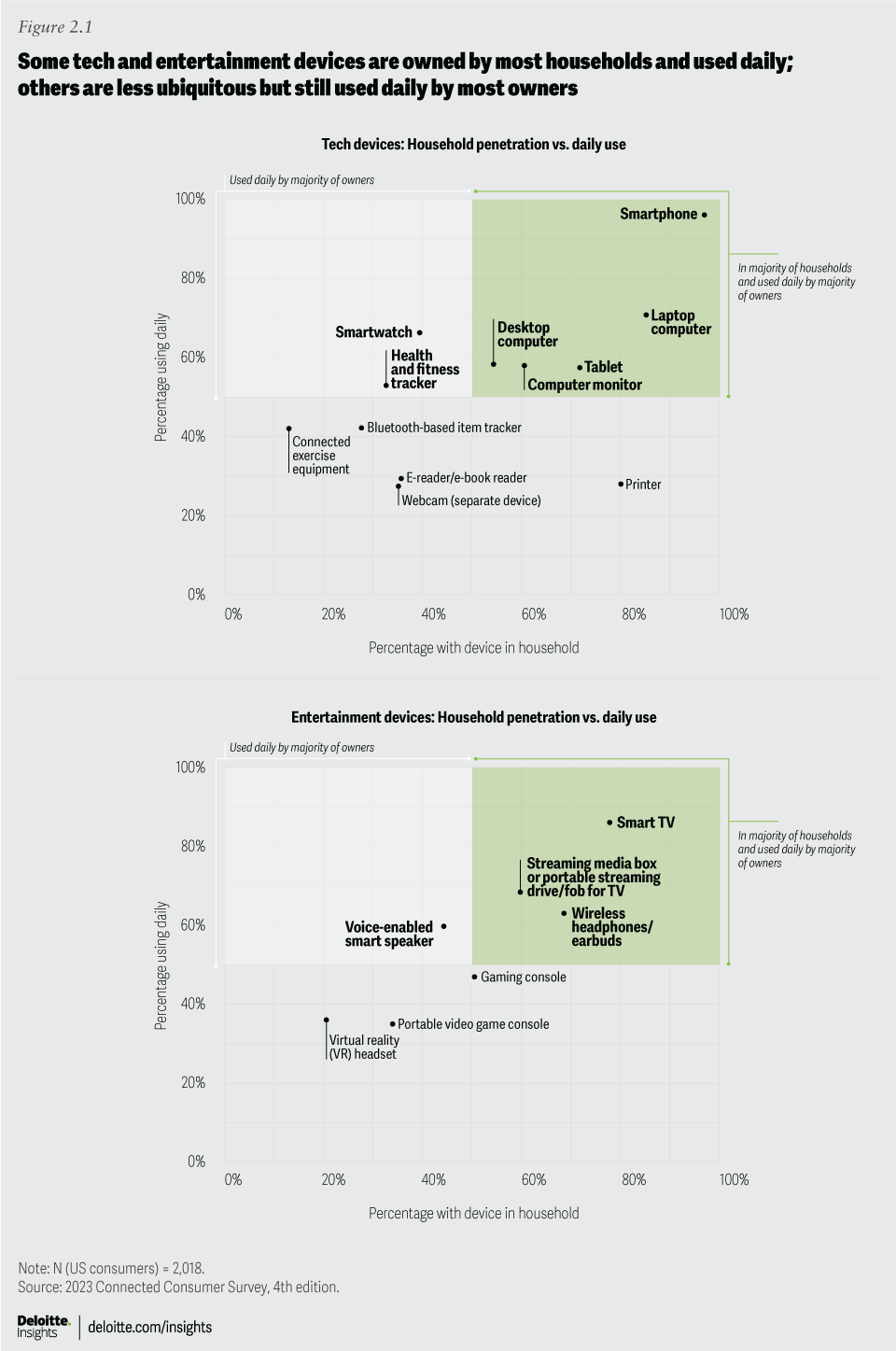

Connected devices are an integral part of everyday life. Some tech and entertainment devices—such as smartphones, laptop and desktop computers, tablets, and smart TVs—are owned by most households and used daily by most owners (figure 2.1, upper-right quadrants). Gaming consoles are owned by just over half of households and are used daily by nearly half of owners; we’re likely to see them shift into the upper-right quadrant in the next year or two.10 Other devices—such as smartwatches, fitness trackers, and voice-enabled smart speakers—haven’t yet been adopted by a majority of households, but most respondents who own them use them every day. A third group of more specialized devices—including connected exercise equipment, e-readers, and virtual reality headsets—haven’t secured a foothold in most households and aren’t yet used daily; time will tell whether they become more popular.

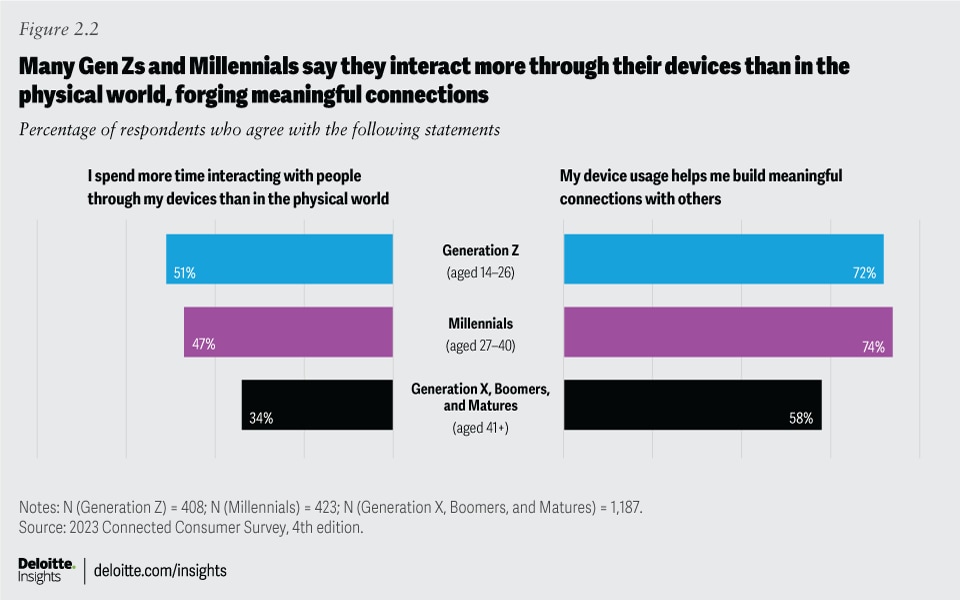

For many people, devices are essential to how they socialize and communicate. In fact, 40% of our survey respondents said they interact more with people through their devices than in the physical world—and that’s true for over half of Gen Zs and nearly half of Millennials (figure 2.2). Nearly two-thirds (64%) of respondents reported their devices help them build meaningful connections with others, whether friends, family, or people with similar interests; more than seven in 10 Gen Zs and millennials feel the same way.

With high usage of voice and video calls, social networks, and messaging apps, it may not be surprising that 80% of smartphone users say the devices help them feel very or somewhat connected to others. What may be more surprising is that a majority of gaming console and connected exercise equipment users—and four in 10 smartwatch/fitness tracker users—also say those devices help them feel very or somewhat connected to other people. On gaming devices, playing multiplayer games, chatting, and sharing game content and clips can all promote connection. Connected exercise equipment can foster a feeling of connection through live streaming, on-demand classes, and leaderboards; and smartwatches and fitness trackers can encourage connection through competitions, challenge groups, leaderboards, and activity sharing. Gen Zs outpace other generations when it comes to feeling connected to others through their gaming consoles (74%) and smartwatches or fitness trackers (64%).

Three-quarters of our survey respondents believe their connected devices have a positive impact on their lives, enhancing convenience, comfort, enjoyment, and safety. Younger generations expressed the most favorable view, with 84% of Gen Zs and 83% of Millennials reporting that their devices have a positive impact, versus 76% of Gen X, 69% of Boomers, and 55% of the cohort we call “Matures” (born in 1946 or earlier). More than eight in 10 respondents say their devices save time and keep them informed, while seven in 10 say devices enable new experiences that they wouldn’t otherwise have.

Too much of a good thing?

When it comes to digital devices—how many a household owns and how much time is spent on them—consumers signal that they may be reaching their comfort limit. The number of connected devices in the average household now stands at 21—down from the pandemic peak of 25 in 2021. Although they have continued to buy new devices, primarily replacing aging ones, most consumers haven’t been expanding their collections.

Current economic unease may be one factor, with pocketbooks only opening so far. But another likely reason is that the significant time spent on devices raises concerns relating to tech fatigue and well-being.

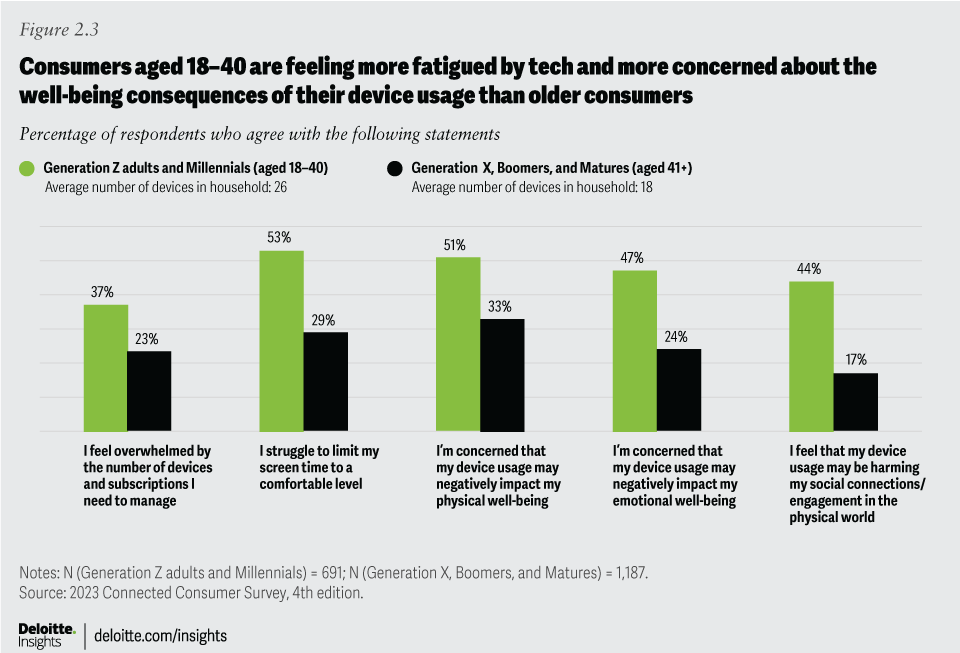

Just as we noted in our 2022 report, people continue to feel frustrated by the complexity of managing their digital lives. Forty-one percent of consumers revealed that they dislike managing their devices (for example, updating software, handling security, or fixing problems). Twenty-eight percent said they’re overwhelmed by the devices and subscriptions they need to manage—an uptick from 24% in 2022 but not quite reaching the 32% we saw in 2021, when households had even more devices. Adults aged 18–40 are feeling more overwhelmed (37%) than older generations (23%) (figure 2.3). Some of this sentiment may stem from 18- to 40-year-olds managing a larger collection of household devices (26 on average) than older generations (18 on average).

The struggle to control screen time is another sign of tech fatigue and has implications for well-being. Studies have highlighted the potential negative impacts of too much screen time on children and adolescents, including disturbed sleep, increased rates of obesity, and poor stress regulation.11 There is less research on how excessive screen time may affect adults—but some studies point to eye strain, impaired sleep, and worsened mental health.12 With screen time estimated to be up 60–80% from prepandemic levels, any potential negative consequences are likely to be exacerbated.13 Overall, 38% of our respondents said they’re struggling to limit their screen time to a level they feel comfortable with—on par with 2022—but this view is much more pronounced among 18- to 40-year-olds (53%) than older generations (29%) (figure 2.3).

Many device users are concerned about potential adverse effects of too much digital time on their well-being: Overall, 39% of our respondents worry that their device usage may negatively affect their physical well-being (for example, causing them to be more sedentary and spend less time exercising), and one-third were concerned that their device usage may negatively affect their emotional well-being (for example, contribute to feelings of anxiety or depression). Our survey analysis uncovered a link between screen time struggles and well-being concerns: Six in 10 of those who feel they spend too much time on screens worry about the effects on their physical and emotional well-being, while just two in 10 of those who say they don’t struggle with screen time express the same worries.

With that said, nearly three-quarters of respondents overall (73%) reported they’re not concerned that their device usage may be harming their social connections and engagement in the physical world. However, 40% of those who said they interact more through their devices than in the physical world do express this worry. As with tech fatigue, 18- to 40-year-olds are more likely to worry about well-being and social harm than older generations (figure 2.3).

In “Consumers seek the ‘just right’ balance between digital and physical worlds,” we take a look at measures consumers take to place boundaries on their digital activities, and we also examine how parents can help their teens find a healthy balance. The sentiment that excess device usage may impact well-being creates opportunities for device and app makers to amplify features that can help. Consumers must typically search for settings and configure usage limits manually; tech companies could assist by providing automatic reminders about screen time and prompts to take digital breaks.

Consumers seek the “just right” balance between digital and physical worlds

Many consumers are taking steps to set boundaries on their own (and their children’s) digital behaviors

Although digital devices are widely viewed as enhancing our lives, they can lead to tech overload and well-being concerns, as we discussed in “Digital life often delivers daily benefits but can also fuel tech fatigue and well-being worries.” More devices may not always be merrier: Our analysis revealed that, as households own more of them, tech fatigue and well-being concerns—such as feeling overwhelmed by the devices and subscriptions one needs to manage and feeling worried that device usage could harm physical and emotional well-being and social engagement with the physical world—also rise. This suggests that adding new devices (without eliminating others) comes with costs of greater management time, more screens vying for attention, and less time participating in the physical world. Respondents to our survey indicated that the total number of their households’ devices has dropped by four in the past two years, suggesting that they may be hitting a ceiling on the number of devices they feel comfortable handling.

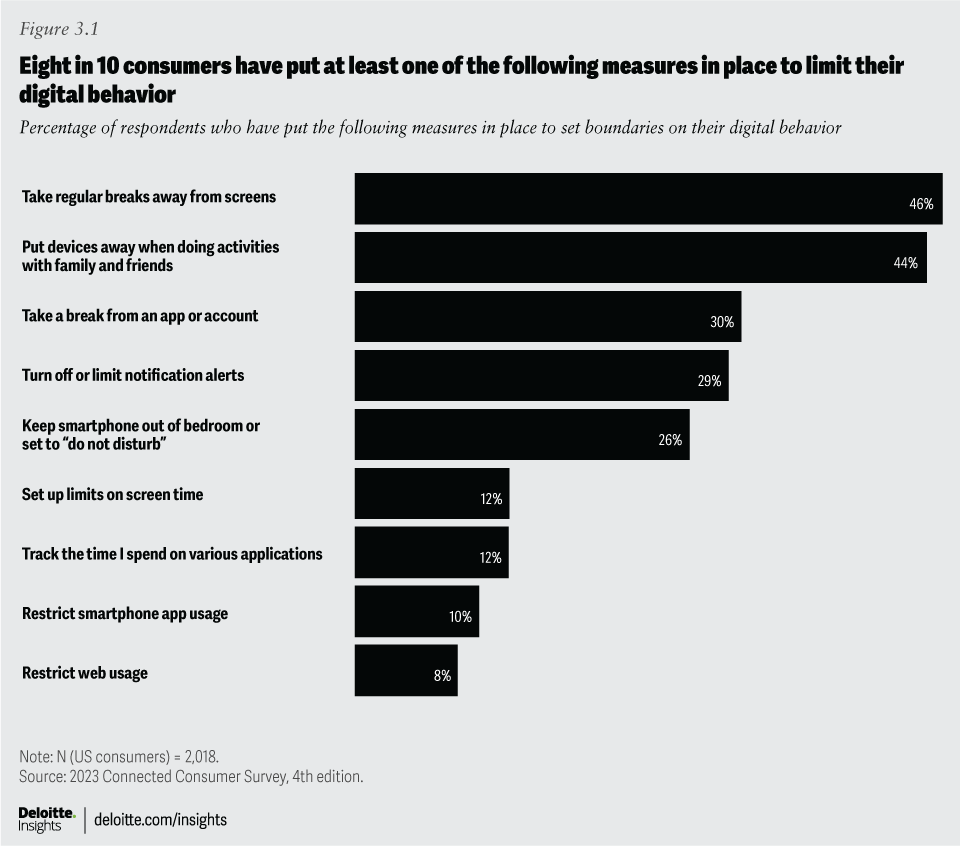

In an effort to help restore some balance, 78% of consumers surveyed have put at least one measure in place to set boundaries on their digital activities, and 42% have put three or more measures in place (figure 3.1). The two most common techniques are physical actions: taking regular breaks away from screens (46%) and setting devices aside when engaged in activities with family and friends (44%). About three in 10 respondents said they’ve taken a break from an app or account, and the same number said they’ve limited notification alerts. Only 12% use digital techniques for setting limits on screen time or tracking the time they spend on applications. There may be an opportunity for tech providers to simplify these tasks—and perhaps suggest digital breaks even if someone hasn’t set up limits. In the future, perhaps AI can be employed to learn user preferences and assist people who want to take regular well-being breaks from their technology, even recommending physical exercises or meditation activities.

In addition to helping consumers with their screen time management, there may be an opportunity for device makers and app providers to simplify device administration, ease data security and privacy management, and improve interoperability. Consumers are likely to place greater value on devices and apps that make their lives easier in these ways and may gravitate toward them when it’s time to refresh their tech.14 Devices that function better together, such as smart home devices that interoperate, could lead to more devices in the home without adding to tech fatigue.

Teens may need help finding the right balance

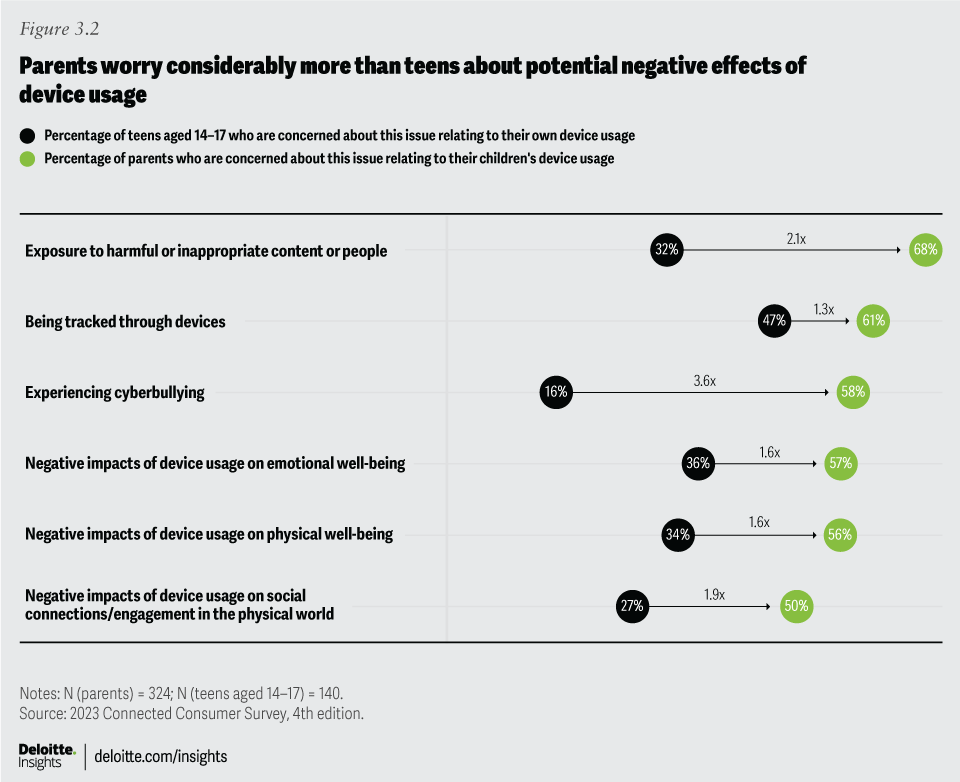

Most parents believe that connected devices enhance their children’s lives: Seven in 10 parents feel their children’s device use enhances learning and enables new experiences, and half feel it helps their children build meaningful connections and stay organized. However, parents also worry about the potential negative effects of device usage—at a much higher level than the teens we surveyed. Fifty-three percent of parents report they struggle to limit their children’s screen time vs. 44% of teens who said they struggle to limit their own screen time. A majority of parents surveyed worry about a wide range of potential negative consequences of their children’s device usage: exposure to harmful content, cyberbullying, tracking, and adverse impacts on emotional and physical well-being (figure 3.2). Teen respondents are concerned about these issues too, but to a lesser extent than parents. Interestingly, almost half (47%) of the teens we surveyed are concerned about being tracked through their devices, as are 61% of parents.

Nine in 10 parents said they have put measures in place to monitor and set boundaries on their children’s digital behavior. The top techniques are checking online activities (44%), encouraging nondigital activities (44%), setting up screen time limits (40%), and blocking or filtering certain types of content (40%). Fewer than four in 10 parents restrict purchases, set parental controls for smartphones, and restrict web and smartphone app usage. This is an area where device and app providers could help parents achieve a healthier balance for their children by making settings easier to find and more intuitive to use.

Data privacy and security worries are on the rise, while trust is down

Consumers are concerned about privacy and security, but right now they feel it’s an uphill battle.

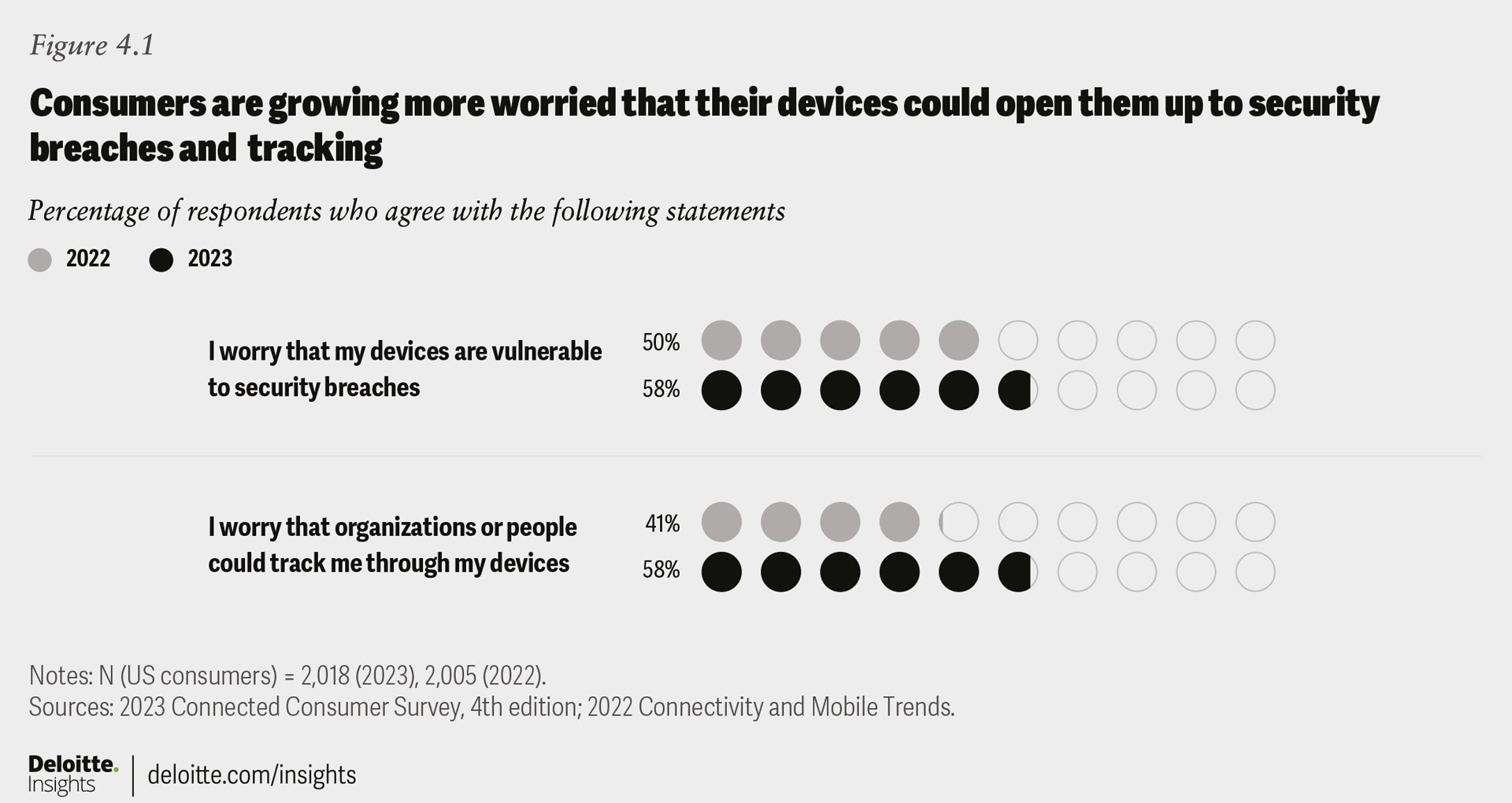

Consumers are increasingly concerned about being “hacked and tracked” through their tech devices. Nearly six in 10 respondents to our survey worry that their devices are vulnerable to security breaches (for example, hackers stealing personal data), and the same number are concerned that organizations or people could track them through their devices (figure 4.1). The concerns are elevated considerably from what we found in our 2022 survey.

Sixty-seven percent of smartphone users worry about data security and privacy on their phones, and 62% of smart home users worry about the same on their smart home devices—up 13 and 10 percentage points, respectively, from 2022. A majority (52%) of smart home users are concerned about the possibility that someone could control their smart home devices (for instance, hackers breaking into smart locks). Almost half (48%) of smartwatch/fitness tracker users are concerned about data security and privacy on those devices—a jump of 8 percentage points from 2022. Location tracking is a significant concern, too: More than six in 10 respondents worry that their movements or behavior could be tracked through their smartphones or smart home devices, and half worry about location tracking through their smartwatches or fitness trackers.

These security fears appear well-founded. 2021 set a record for total data breaches, and the incidents in 2022 affected an even greater number of people.15 One-third of our survey respondents said they experienced at least one type of breach or scam in the past year, and 16% fell victim to two or more kinds—on par with the numbers we reported in 2022.16 Our analysis revealed that the likelihood of a breach increases as households add more devices. Eleven percent of households with 1–15 devices reported experiencing two or more breaches in the past year, compared with 16% of households with 16–30 devices and 29% of households with more than 30. In an eye-opening experiment, researchers found that a smart home full of Internet of Things devices could experience thousands of hacking attempts in a week.17

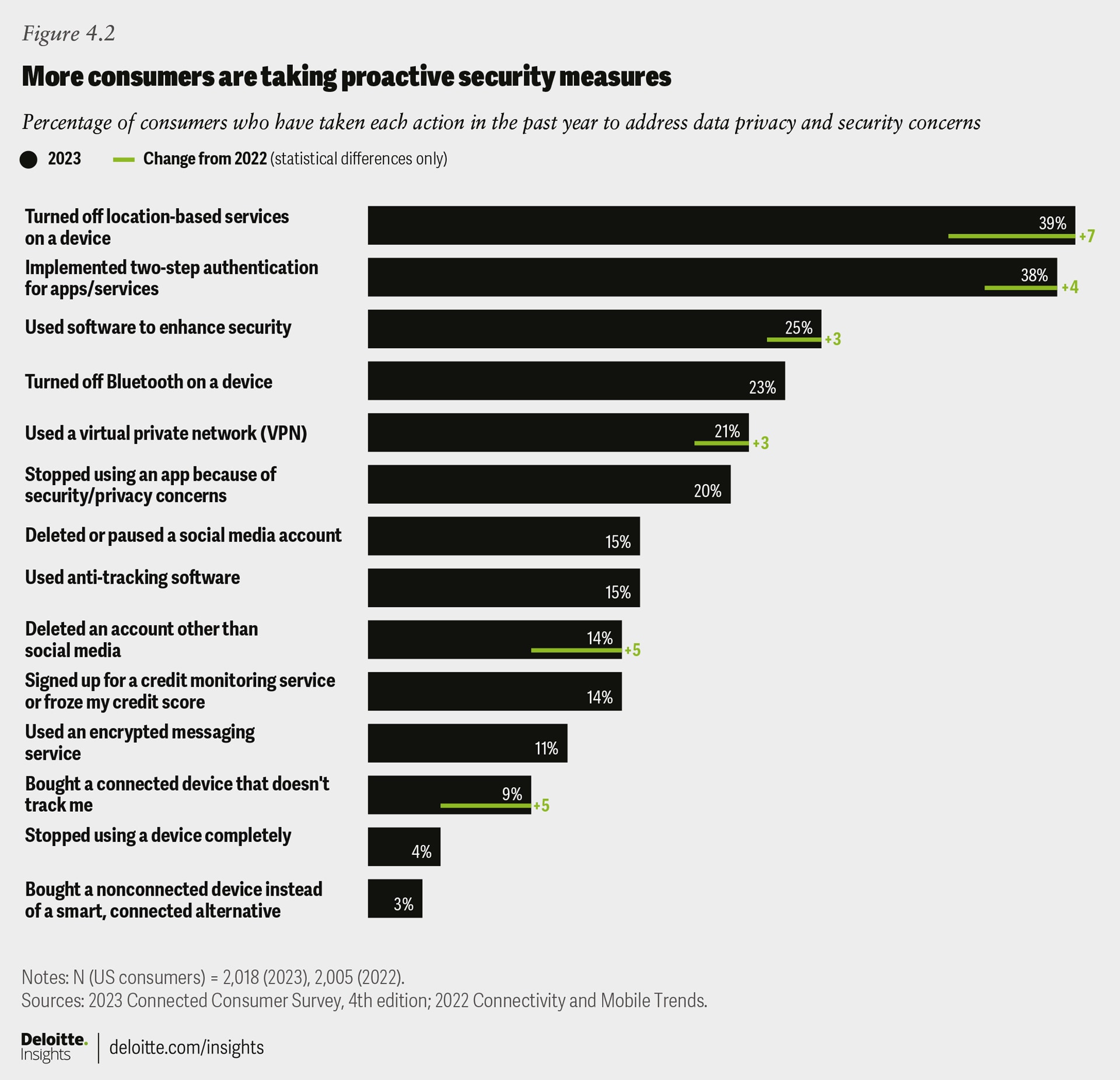

Against the persistent threat of hacks and scams, more consumers are taking protective actions. We identified 14 measures consumers could take to protect their data, from using two-step authentication to turning off location and Bluetooth connections, to installing security software (figure 4.2). This year, 79% of respondents reported they had taken at least one of these actions (up from 71% in 2022), and 28% had taken four or more (up from 21% in 2022). Notably, the two most popular measures are those that are prompted by mobile operating systems. If devices provided more prompts and help (for example, an alert that an app has been reported for privacy concerns, or a suggestion to use a virtual private network while on a public internet connection), people might adopt more security measures.

Three-quarters of our survey respondents agreed they should do more to protect themselves. Why, then, aren’t they taking more steps? Their top reasons revealed a sense of futility. Twenty-seven percent feel that companies can track them no matter what they do, and 17% feel hackers can access their data no matter what actions they take. A quarter said they just don’t know what actions to take to protect themselves. There are also financial considerations. Eighteen percent reported not wanting to pay for software or services to increase protection.

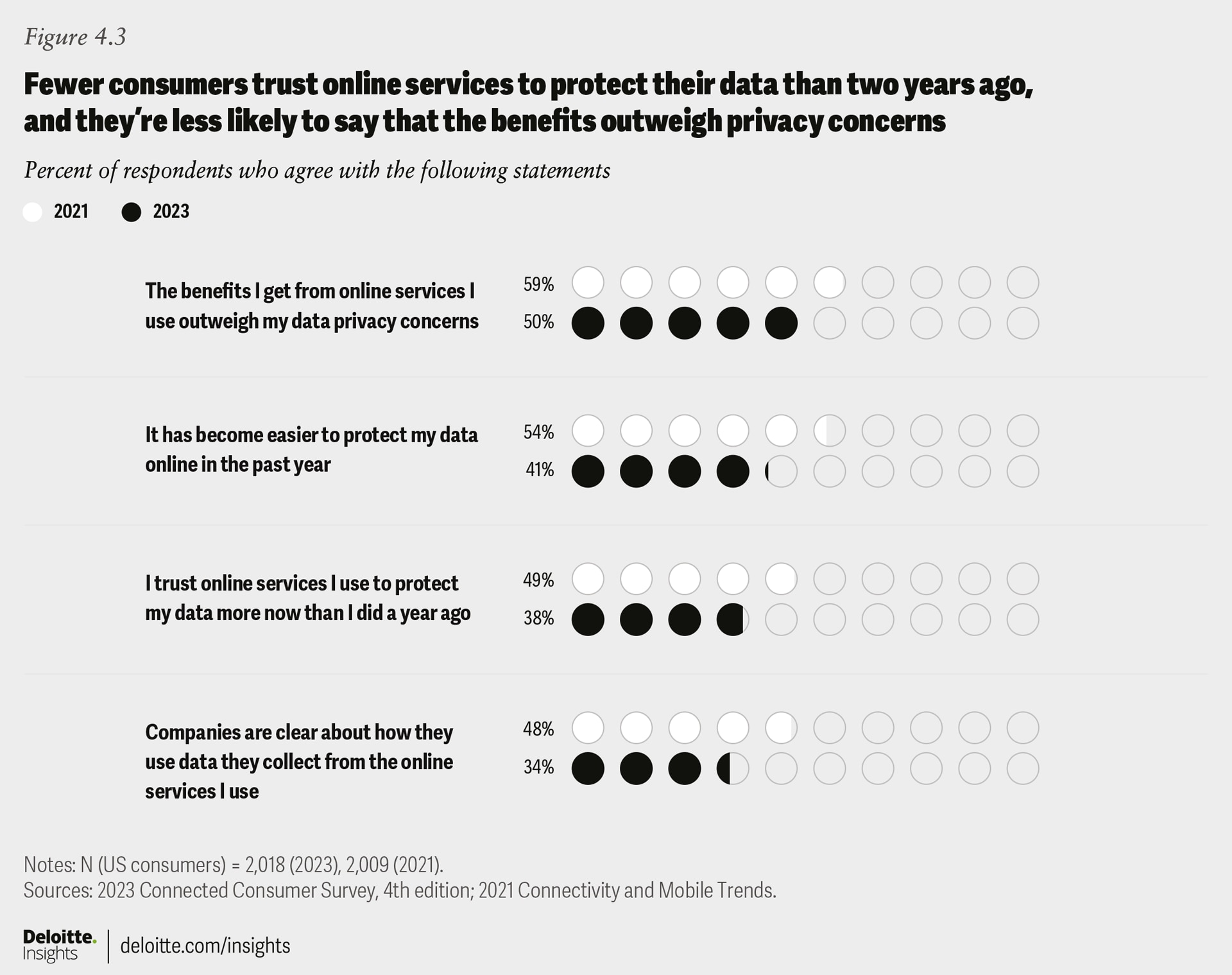

Fewer consumers trust companies to protect their data

Consumers aren’t just worried about hackers; their trust in companies that sell devices and online services is wavering, too. Only half of respondents feel that the benefits they get from online services outweigh their data privacy concerns—a drop of 9 percentage points from 2021 (figure 4.3). There are other signs of eroding trust: Only 41% think it has become easier to protect their online data in the past year, and a mere 34% feel companies are clear about how they use the data they collect from online services. Each finding represents a double-digit percentage-point drop from 2021. Lastly, 9% of respondents said they bought a device in the past year that doesn’t track them (figure 4.2). It’s a small cohort, but a notable jump of 5 percentage points since 2022.

There are some interesting generational differences when it comes to trust. Five in 10 Gen Zs and Millennials say they trust online services to protect their data, versus just three in 10 older consumers. Six in 10 Gen Zs and Millennials feel the benefits they get from online services outweigh their privacy concerns, but only four in 10 older consumers feel the same way. The path to convincing older consumers to make greater use of connected tech (such as GPS tracker watches, fall detection, smart lights, smart security systems) likely relies partly on gaining their trust.

Regardless of generation, the vast majority of respondents want more protection and control over how their data is used. Almost nine in 10 agree they should be able to view and delete the data that companies collect about them, and 80% feel they deserve to be paid by companies that profit from their data. Eighty-five percent think device makers should do more to protect data privacy and security on the devices they sell, and 77% want the government to do more to regulate the way companies collect and use that data.

To help win back trust, device makers and service providers should respond to the growing consumer concerns around hacking and tracking, as well as their desire for more transparency and control over their data. Organizations should consider prioritizing robust data-security measures and communicating their data-handling practices more effectively. Making it simpler for consumers to understand what data gets collected and how it’s used, along with providing easier ways to control that use, may create a competitive advantage. Companies could prompt users at appropriate points to make informed choices about the use of their data. Failure to help people shore up their data security and privacy could leave companies open to disruption by competitors that make it part of their mission to protect consumer data. Beyond wanting companies to help, consumers would also welcome more regulations that force the issue, and these seem inevitable.18

Consumers make their homes smarter, with a focus on security

While smart home device adoption is not yet widespread, many users find their features indispensable.

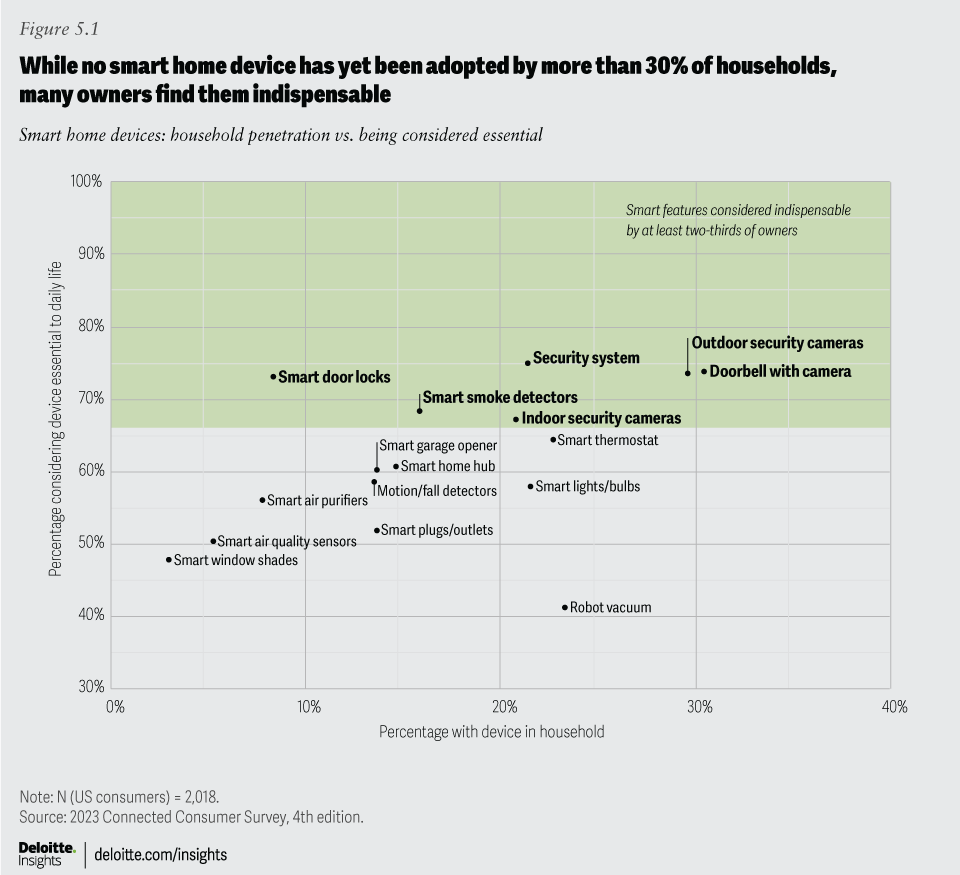

While some tech and entertainment devices, such as smartphones, computers, and smart TVs, are commonly found in households, devices designed to make the home smarter are still gaining a foothold. No single smart home device has reached more than 30% of households yet, but many owners find the smart features they offer indispensable (figure 5.1). Smart home users appear to be prioritizing home security over comfort and convenience. Looking at the smart home devices that at least two-thirds of owners consider essential for their daily lives (the blue shaded area in figure 5.1), all of them relate to security and empower homeowners to monitor and protect their environments.

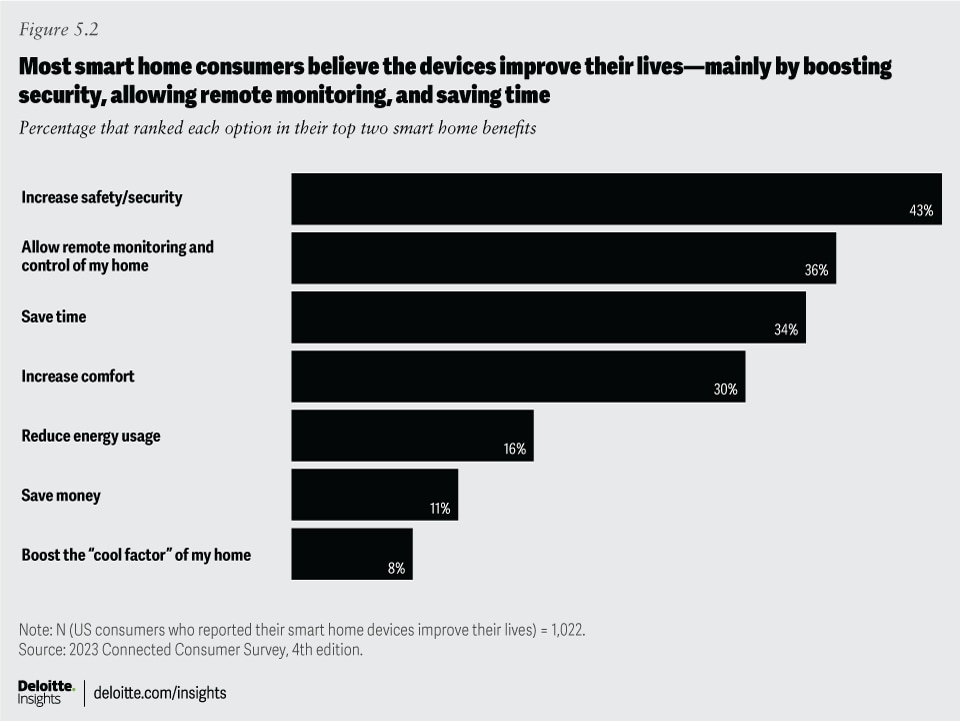

In our survey, 77% of consumers who have embraced smart home devices believe that these technologies improve their overall quality of life. Apart from increasing security, another key advantage of smart home devices they noted is remote monitoring capabilities (figure 5.2). These can allow homeowners to keep an eye on their homes, adjust settings, and receive real-time notifications if a door opens or an alarm is tripped, for instance. Saving time and increasing comfort round out the top four ways smart home devices are seen as improving life. Interestingly, only one in five users reported that smart home devices caused frustration or added complexity. This suggests that most consumers feel smart home technology delivers an overall positive experience.

While consumers focus on using smart devices to achieve more physically secure homes (via security cameras, smart locks and doorbells, and smart smoke detectors), a majority also worry that their smart home devices could be vulnerable to hacking (as we noted in “Data privacy and security worries are on the rise, while trust is down”). Their concern is not misplaced: Researchers have found that smart homes could attract thousands of hacking attempts per week, and articles abound on how to keep a smart home secure.19 Presently, worry about hacking doesn’t appear to be impeding adoption, however: Consumers with over 10 smart home devices are about as worried as those with only one to five devices, and worriers and nonworriers alike have approximately seven smart home devices on average.

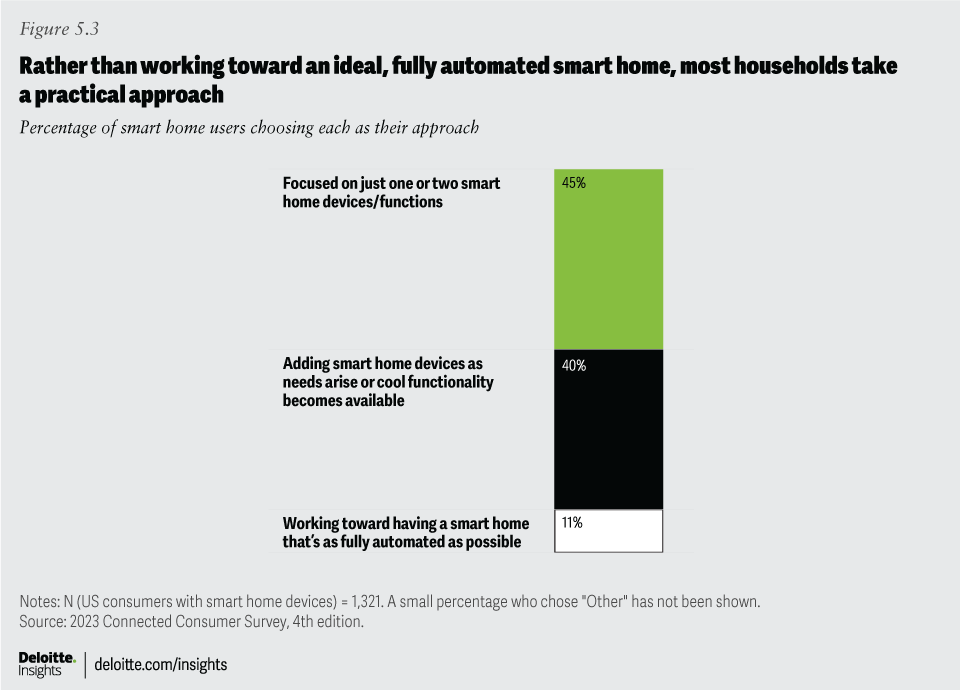

Smart home users take a pragmatic approach

Consumers are pragmatic about using smart home devices, with 85% saying they prioritize specific functions or devices that align with their immediate needs and preferences (figure 5.3), as opposed to working toward an ideal, smartest-possible home (11%). Forty-five percent said they’ll buy and install one or two smart home devices, selecting products that can address their immediate needs. Another 40% of smart home users adopt smart home devices as needs arise or when new and exciting functionalities become available.

Even if they’re not currently pursuing full home automation, 79% of users think interoperability is very or somewhat important, and 34% said they want all their devices to work together seamlessly. Aligning with a specific tech company’s smart home ecosystem could help orchestrate all of one’s smart home devices, but only 31% of the smart home users we surveyed said they have landed on a specific system.20

In fact, homeowners control their smart devices primarily through individual smartphone apps (45%). Voice control to a smart speaker or hub isn’t very common yet (17%); consumers are just as likely to use controls on the device itself (18%). This tendency to rely on individual apps may lead to frustration as users add more devices and need to manage multiple interfaces.21 In the future, a new smart home standard may come to the rescue, allowing smart home devices from different companies and ecosystems to share a single interface, improving functionality and reliability.22

Hybrid workers seek the best of in-office and remote work

Shifting between the office and home can be challenging, but hybrid workers value the flexibility.

Our 2022 survey found that remote work was enormously popular with workers: 99% of those who had worked from home appreciated aspects of the experience, including the lack of commute, enhanced comfort, better focus, and feeling more connected to family. In 2023, as many companies ask employees to return to the office, it appears that they’re offering hybrid schedules to help soften the blow.23

Our survey revealed that 56% of employed adults work from home at least some of the time: 22% work fully from home and 34% keep a hybrid schedule. The remaining 44% work fully in office. We asked hybrid workers how many days they commute into the office vs. work from home: On average, hybrid workers spend 3 days in office and 2.6 days working at home, which correlates with the hybrid schedules that many companies have reportedly adopted.24 More than half of the hybrid workers surveyed (54%) said it’s their employer’s decision that they can work a hybrid schedule, and another 30% said they had arrived at the decision with their employer.

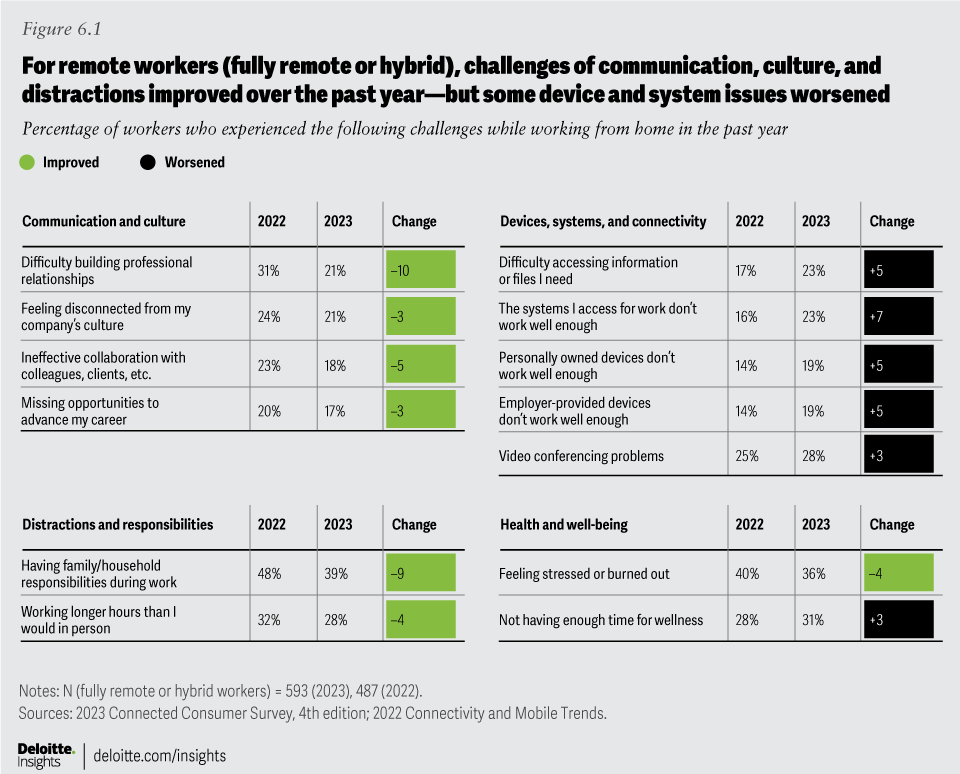

Comparing this year’s findings with last year’s, employees seem to be more successful in navigating some challenges of remote work (figure 6.1). Fewer remote workers say they have difficulty building professional relationships, collaborating, and balancing household responsibilities with work. However, complaints about technology and connectivity have gone up, with more remote employees saying their work systems don’t function well enough and that they have a harder time accessing the information and files they need.

These findings point to a potential need for employers to refresh employee hardware and update the tools and systems that support remote workers. Working at least partially remotely seems to be workers’ preferred approach, but it’s not one that companies can simply “set and forget.”

In this year’s survey, hybrid workers expressed higher job satisfaction than other workers, and at least eight in 10 reported their relationships with family members, colleagues, and managers have improved or stayed the same, compared with when they worked fully in office. At the same time, while they appreciate the flexibility that hybrid work provides, they’re feeling the strain of juggling two work models.25 The challenges come into stark relief when their responses are compared with those of fully at-home workers: Hybrid workers are more likely to feel disconnected from on-site colleagues and say that their collaboration efforts are ineffective, and they’re also more likely to be distracted by nonwork activities, to have difficulty accessing work files, to feel stress and burnout, and to have a hard time prioritizing their well-being. In time, hybrid may well offer the best of in-office and at-home work modes, but hybrid workers may need the support of their employers to overcome some of the challenges.26

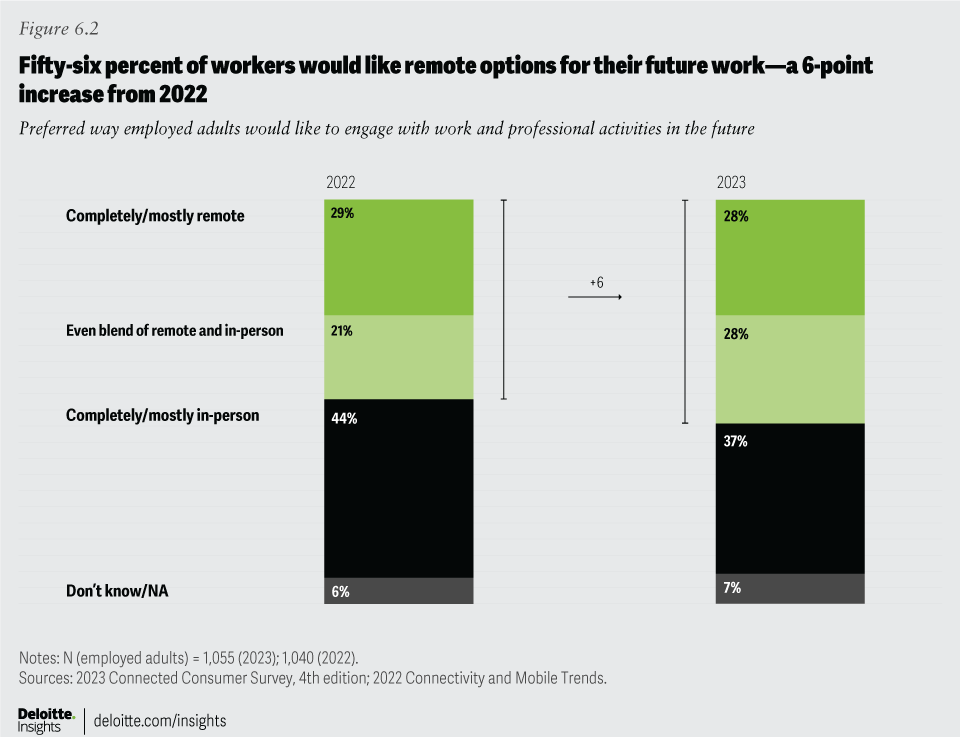

On the whole, workers express a preference for fully remote and hybrid options over in-person work (figure 6.2). Preference for “completely or mostly in-person” has dropped from 44% last year to 37% this year, while preference for an even blend of remote and in-person rose from 21% last year to 28% this year. Going forward, nearly eight in 10 fully remote workers, two-thirds of hybrid workers, and even one-third of fully in-office workers would prefer virtual work options. This shows that workers believe in the promise of hybrid, even as some issues are still being ironed out.

Hybrid creates challenges for employers, as well. Letting workers set their own preferred hybrid schedules could cause workspace usage and in-person collaboration to suffer. However, if a company mandates certain in-office days, employees may resent the reduced flexibility.27 Getting hybrid “right”—with a mix of policies, cultural activities, and collaboration tools that empower workers at home and in the office — is likely to generate benefits for companies and employees.

Remote learners gain experience and find success with virtual classes

Tech and social challenges are lessening as students—and teachers—grow more comfortable with digital learning technologies.

The pandemic catalyzed a dramatic shift to remote learning out of necessity. The phenomenon has endured, with many students continuing to learn remotely by choice: Of our survey respondents who said they had taken classes during the past year, 57% said they learned online from home at least some of the time. Overall, 23% of respondents reported that at least one member of their household is currently attending virtual classes at least some of the time. Remote learners included high school and university students (32% and 29%, respectively), professional development trainees (26%), and those learning for personal development (8%).

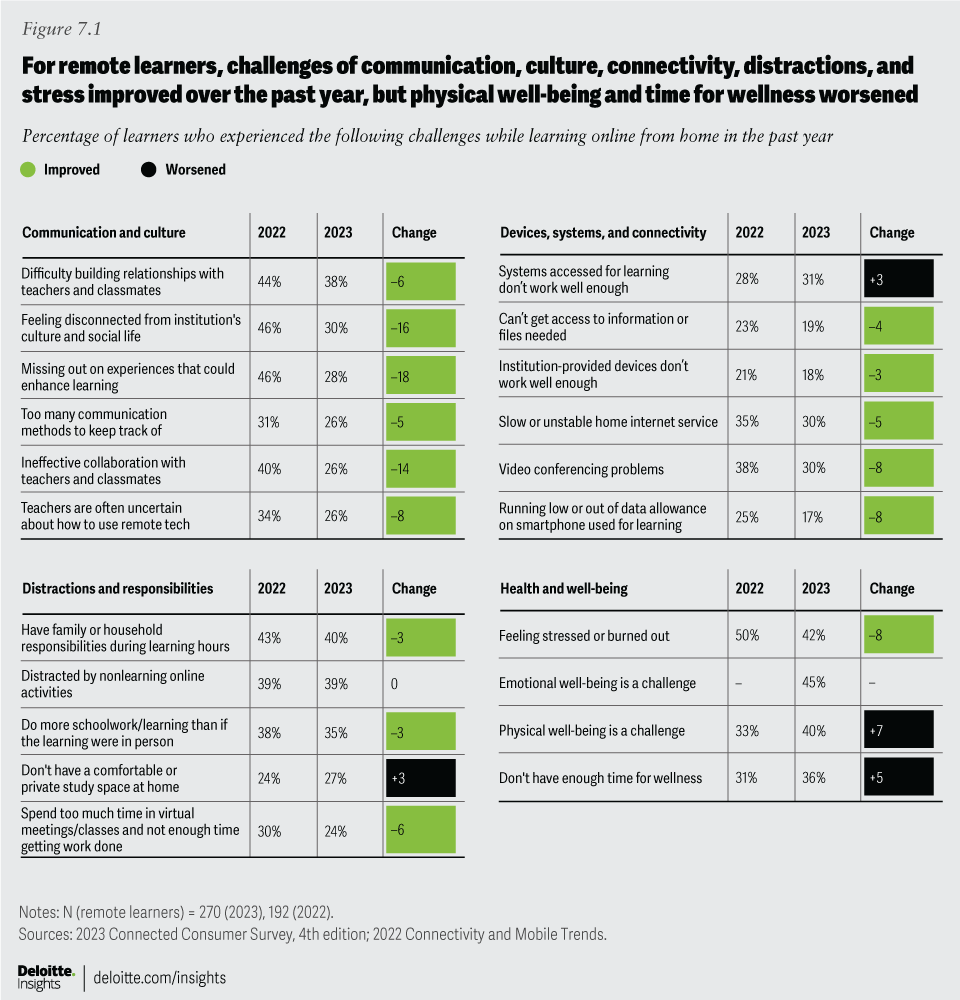

Many of the technological and social challenges that remote learners reported in previous years seem to be abating as the model gains maturity and students grow more comfortable with online learning and teaching tools (figure 7.1). Students surveyed are less likely to feel that they’re missing out on key experiences, and to feel that teachers don’t know how to use virtual tools. They’re also finding it less difficult to build relationships with instructors and classmates. Feelings of stress and burnout have also decreased, with 42% citing them as a challenge, down from 50% a year ago. On the downside, more remote learners report that maintaining physical well-being is a challenge and that they don’t have enough time to focus on wellness.

These issues of emotional and physical well-being, including feelings of stress, emerged as the top challenges of remote learning. Other challenges include having to balance other responsibilities during school hours, along with online distractions. These are roughly in line with the top challenges that remote workers also reported (see, “Hybrid workers seek the best of in-office and remote work”). Changing the locus of learning (or work) to the home arena often means people have more flexibility in when and how to manage household responsibilities, but that can also mean they have to master a complex juggling act of competing schedules and duties—and that can fuel stress. Virtual learners may need to study at times when they can find the most peace and quiet, suggesting an ongoing need for compelling, flexible, asynchronous online tools that institutions can use to help differentiate and elevate learner experiences while alleviating the stress of deadlines and distractions.28

Despite emotional and physical well-being ranking as top challenges, most remote students don’t feel they have worsened compared to when they learned in person. When asked how learning from home has affected their health and relationships, most respondents said their resilience, family and teacher relationships, and physical and emotional well-being have improved or stayed the same. Fewer than two in 10 reported declines.

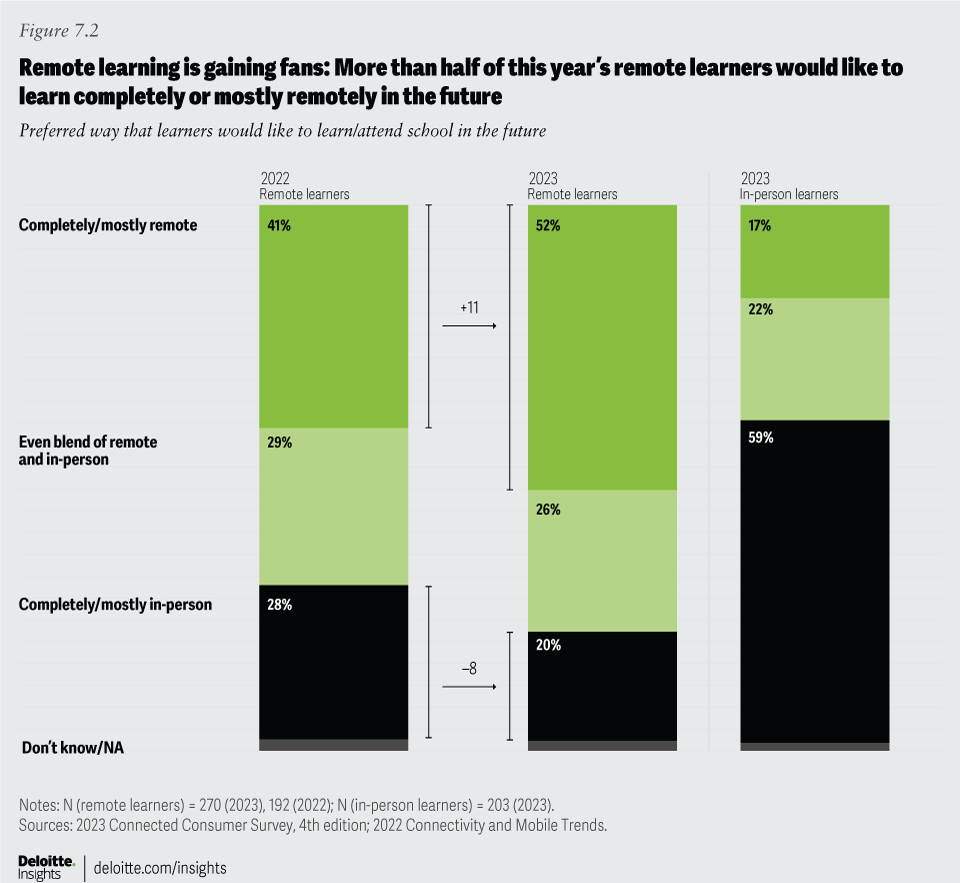

The benefits of online learning appear evident as respondents consider their future preferences. Among those with remote learning experience, more than half would like to continue “completely or mostly remote” (figure 7.2). Another quarter would prefer an even blend of remote and in-person learning, and only one in five would want to learn completely or mostly in person. Notably, only 6% of those with remote learning experience over the past year would like to engage in fully in-person learning (down from 12% in our 2022 survey). Even among in-person students, about four in 10 said they would prefer some virtual options going forward.

Remote learning appears to be an enduring phenomenon — especially among those who have gained experience with it. Although many remote learning challenges are decreasing, some of the biggest challenges around well-being persist. To continue improving the virtual learning experience, schools and education-tech providers could enhance their focus on student well-being, structuring lessons, and experiences to support a more holistic balance of digital and physical activity.29

Virtual health and fitness find their rhythm

Connected consumers improve well-being with virtual health visits and smart watches, shifting focus from tracking biometrics to fitness.

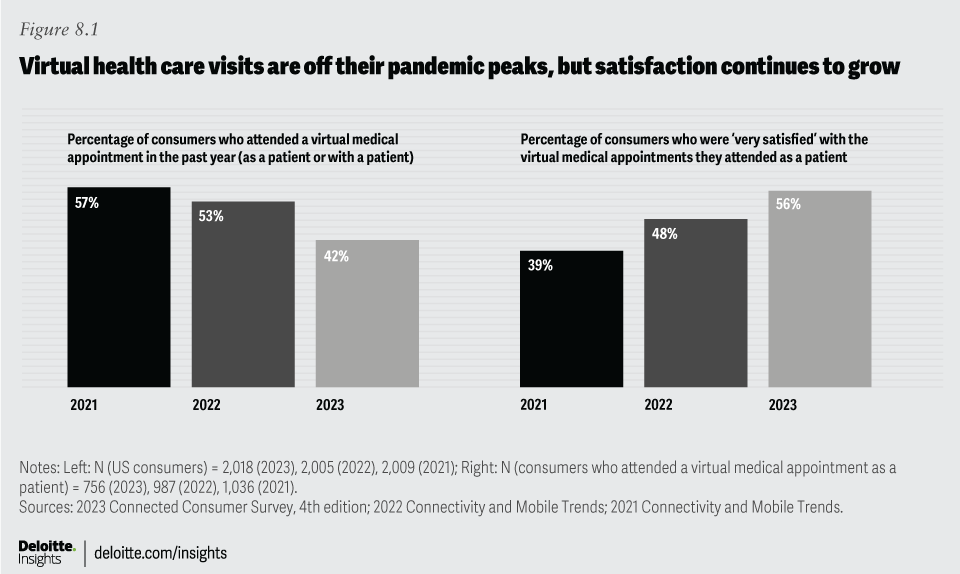

Virtual health skyrocketed between 2021 and 2022, as COVID-19 halted many in-person health care visits.30 Now that face-to-face interactions are more common again, the number of consumers seeking virtual health care appointments has decreased, but those surveyed still find virtual visits convenient and often equally as satisfying as seeing a clinician in the flesh.

In this year’s survey, 42% of respondents said they attended at least one virtual medical appointment, either as a patient or accompanying a patient (figure 8.1). More than half of those who attended as patients reported being “very satisfied” with the experience; only 10% said they were dissatisfied.

As expected, convenience was the top draw of virtual medical appointments, but eight in 10 respondents said they were also satisfied with the technical aspects of the appointment, the quality of care, and the human connection they felt with the practitioner. As video interactions become more commonplace, consumers may find that they’re able to establish a rapport with health care providers and feel “heard” even when they’re connecting remotely.

Looking ahead, a majority of respondents expressed a preference for virtual or hybrid options for attending mental health care or therapy sessions and for checking on chronic conditions—needs that can sometimes be met without requiring an in-person appointment. Only 28% would prefer mental health visits to occur completely or mostly in person. Conversely, nearly half would rather see a provider mostly or completely in person for new symptoms and issues, and 67% would want in-person options for emergency issues. Essentially, they seem to want to use tech to streamline their care experience, depending on their specific health needs.

Another important aspect of digital wellness is health and fitness tracking, either via smartwatch or dedicated fitness wearable. This year’s findings seem to reflect a softening across the category: Compared with 2022, personal ownership of fitness trackers fell seven percentage points to 22%, and connected exercise equipment fell eight points to 13%. Smartwatches are a bright spot: Personal ownership has held steady over the past two years, with 29% of respondents reporting they have one.

Sixty-nine percent of those who own smartwatches and fitness trackers say the devices improve their fitness, and 64% say they improve their health. What they’re tracking has shifted slightly from health metrics to fitness: Monitoring heart health, calories, and blood oxygen levels is down significantly from last year, while counting steps, measuring speed and distance, and tracking performance are up. This would seem to reflect an uptick in outdoor activities and a relative lessening of pandemic vigilance around health signals.

Health and fitness wearables are not ubiquitous yet; 39% of nonowners thought they wouldn’t be useful, and 30% are put off by the cost. However, smartphones, which are ubiquitous, are also being used to help enhance health and wellness. Sixty-four percent of smartphone owners said the device helps to improve their health, and 58% say it helps improve their fitness. Four in 10 said they track fitness activities on their phones, and more than a third use them to manage health care appointments and tasks.

An opportunity for device makers, health care providers, and the wellness ecosystem may lie in streamlining experiences and connecting wearable and phone data feeds to deliver personalized recommendations for users and their health care providers.31 The health care industry should consider how to standardize data types and how to incorporate actionable insights into clinician workflows, enabling improved care delivery that aligns with their payment models.32

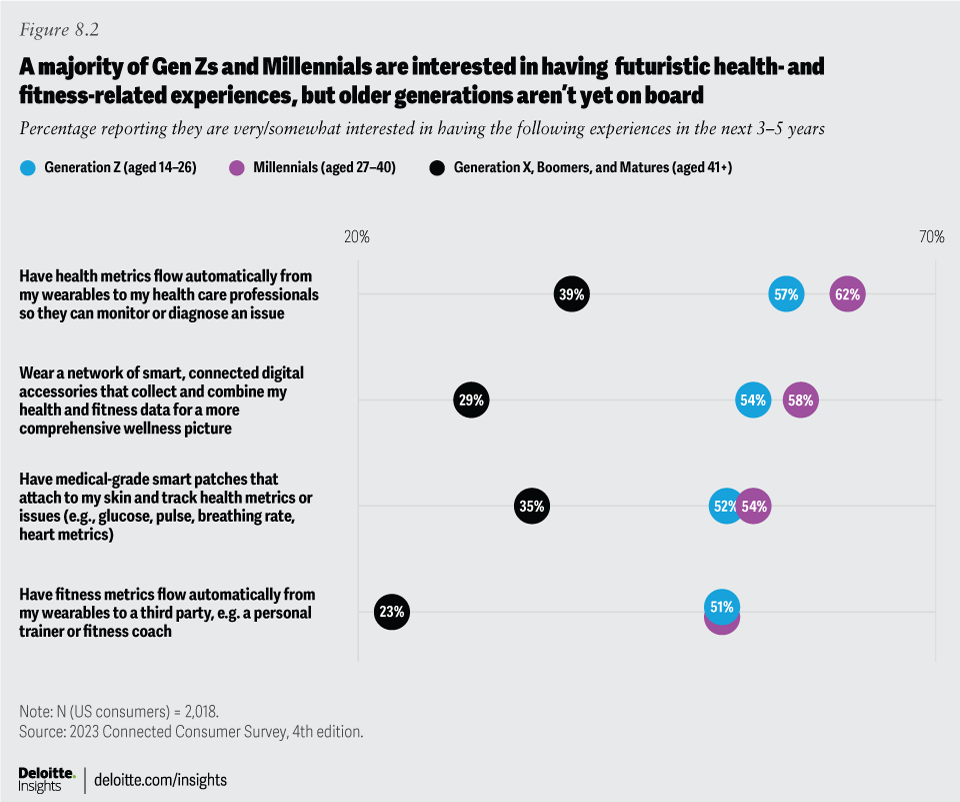

In that vein, we asked respondents how interested they’d be in “futuristic” health care experiences, such as having health data flow directly from wearables to health care providers (figure 8.2). A majority of Millennials and Gen Z respondents were excited by the prospect. More than half of Millennial and Gen Z respondents also expressed interest in an ecosystem of wearables and accessories that aggregate health metrics, and in having medical-grade smart patches for monitoring blood sugar, heart rhythm, and respiratory health and early detection of diseases.33 Younger generations seem to have a higher comfort level with providing digital wellness information in exchange for improved health and fitness advice from professionals.

This split in generational attitudes highlights another challenge for tech companies: how to get older consumers comfortable with health innovations. Elder care is considered a growth area for health technology,34 and companies should prioritize their user experience and marketing efforts to help bring this high-value demographic aboard.

Future of 5G: Consumers have rapidly adopted 5G but are waiting for killer apps

Respondents are largely satisfied with their 5G smartphone service but wonder when they’ll see innovative experiences.

Smartphones are the MVP (most valuable player) device for many consumers: most owned, most used, and most relied on to foster connections with others (see “Digital life often delivers daily benefits but can also fuel tech fatigue and well-being worries”). Even so, smartphone users are holding onto their phones slightly longer before considering an upgrade or replacement. Currently, 30% of smartphone users say their phone is under a year old—a decrease of five percentage points compared with the previous year. And their future purchase plans suggest that they’re in less of a hurry to replace their old phones: Twenty-seven percent of smartphone users plan to purchase a new phone in the next year, a decline from 32% in 2022. The slowing pace may well be due to unease about the economy and personal finances.35

The rollout of 5G networks has been widespread, bringing new possibilities and behaviors to smartphone users.36 Among consumers whose smartphones are less than a year old, the percentage of devices equipped with 5G capability rose from 56% in 2021 to 77% in 2023 (figure 9.1). Moreover, 62% of smartphone consumers we surveyed now report their devices having 5G capability, indicating a notable increase from 50% in 2022. The integration of 5G technology in smartphones is influencing consumer habits, prompting some smartphone users (especially Gen Zs) to spend more time streaming video, playing video games, and using their phone as a hotspot (figure 9.1).

As familiarity with 5G smartphones grows, consumers are developing more realistic expectations regarding the capabilities and performance of 5G networks. In 2022, 48% of 5G smartphone users we surveyed reported that the service exceeded their expectations; in 2023, this percentage has declined to 38%. As 5G networks expand and mature, users’ expectations will likely align more closely with the capabilities of the technology.

Despite the widespread availability of 5G, most 5G smartphone users feel like their devices haven’t tapped the full potential of the technology. A majority (53%) of 5G smartphone users are seeking apps and experiences that take advantage of advanced network capabilities. Moreover, 26% expressed disappointment with the lack of innovative apps and services tailored for the 5G environment. Mobile service providers may be able to tap into this opportunity, as 50% of 5G smartphone users said that they would value premium bundles with innovative digital services and apps designed to make the best use of 5G.

Overall, consumers are satisfied with their current mobile service and see no need for immediate change. Sixty-seven percent of the mobile users we surveyed made no changes to their mobile provider or plan in the past year, and only 18% expressed a likelihood to switch providers in the next year.

5G gains a foothold in home internet

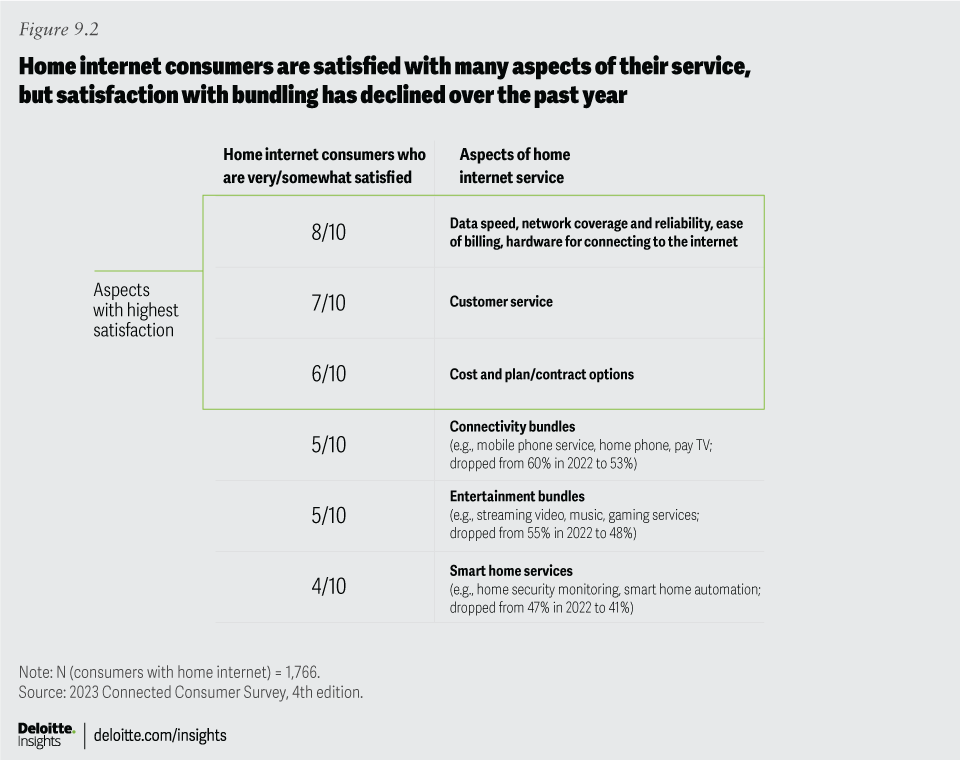

Seven in 10 home internet users made no changes to their internet service in the past year, and most are satisfied with various aspects—just as they were in 2022 (figure 9.2). What’s more, 77% of our survey respondents said they use separate providers for their home internet and mobile services—primarily because they perceive no cost advantage from bundling and also because they believe that the best services in their area are provided by different companies.

It’s worth noting that customer satisfaction with bundles—whether for connectivity, entertainment, or smart home services—has dropped by several percentage points since 2022. This may reflect recent price hikes levied by many streaming services, but this also represents an opportunity for internet providers to appeal to value-conscious consumers through attractively priced bundles—whether it’s providing mobile access, offering connectivity options such as fiber and 5G fixed wireless access (FWA), or partnering with entertainment services to include subsidized or free subscriptions.37

In 2023 and beyond, there may be ample room to grow FWA-mobile convergence bundles: Twelve percent of home internet users surveyed reported having a fixed wireless connection, up 50% from our 2022 survey.38 What could be even more significant is that the majority of these FWA users (52%) indicated that their fixed wireless connection is powered by 5G technology. This represents a considerable increase over 2022, when only 32% of the FWA users in our survey reported having 5G connections. Indeed, 5G FWA has been rapidly capturing broadband share, accounting for 90% of net additional broadband Internet subscribers in 2022.39 More consumers seem willing to embrace the capabilities of 5G fixed wireless connections for their home internet: Twenty-seven percent of home internet users said they would be interested in switching to 5G home internet service, and 14% said they would be interested in switching to a 5G FWA-mobile bundle.

As 5G becomes the standard, for both mobile devices and home internet, an ongoing question is, what kinds of new digital experiences will it enable or augment?40 While that story is still being written, one of the top contenders may be immersive, virtual reality 3D experiences, which can be improved by higher bandwidth and lower latency (see “Immersive 3D and generative AI are shaping the digital future”). Indeed, there are already signs that 5G users spend more hours each week engaging in new experiences such as cloud gaming and augmented reality compared to 4G LTE users.41 We could expect to see Gen Z and millennial consumers leading the uptake of 5G-enabled immersive experiences.

Immersive 3D and generative AI are shaping the digital future

Younger consumers embrace a world where physical and digital experiences blend in engaging and intuitive ways.

Most people already experience a sense of immersion in music, TV, and film. And many—especially younger generations—interact with rich 3D experiences through video games that can transport players into other worlds and bring them together in shared virtual spaces. Whether people do so through screens (as most do) or with virtual reality headsets (as some do), such 3D immersive experiences are becoming so popular that they’re reshaping the landscape of media and entertainment.42

As these experiences become grander and more hyperrealistic, and as they bring together hyperscale audiences, consumers may require greater bandwidth to support them and innovative new devices to help augment their experiences. This evolution of immersion and virtual socialization is also being enabled by generative AI capabilities that can amplify game development while potentially generating personalized, on-demand immersive experiences. This emerging nexus of 3D immersion, interaction, socialization, and personalization is often called “the metaverse.”

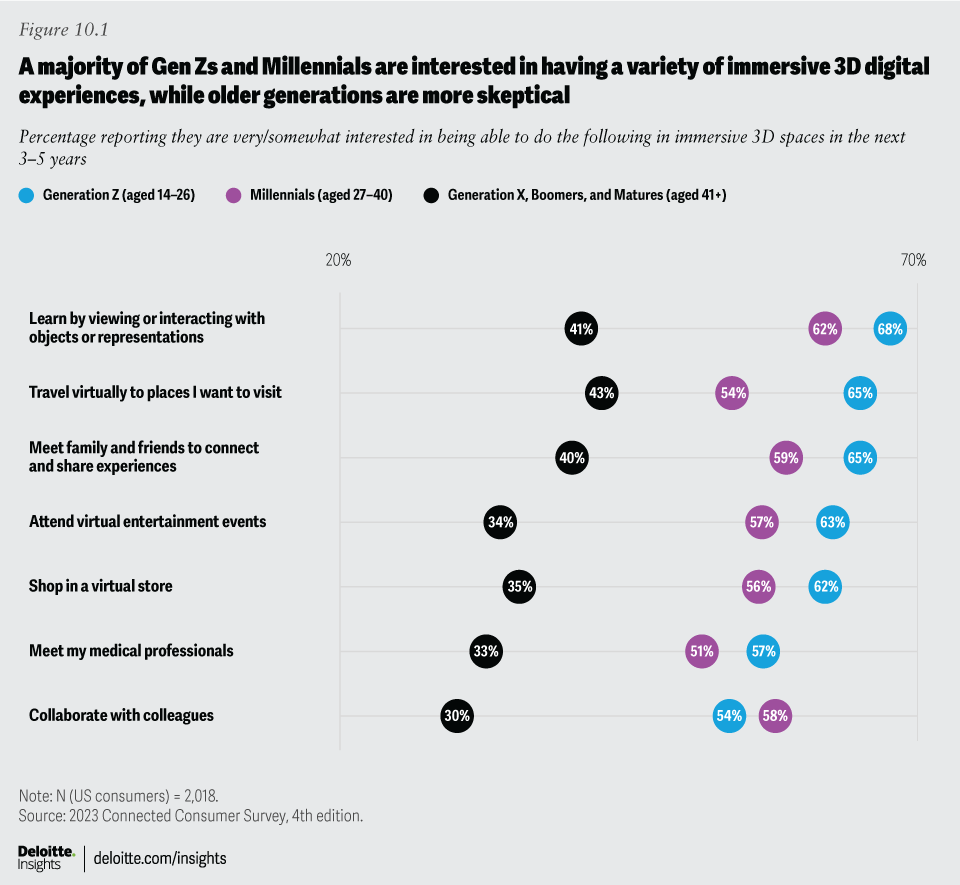

Some of the largest tech companies are investing heavily in next-generation technologies to make these experiences possible.43 While narrative-based and competitive games have dominated 3D immersive interaction, many more kinds of experiences could appeal to more people and add greater value beyond entertainment. We asked our respondents to gauge their level of interest in having a range of immersive 3D virtual experiences: learning by viewing or interacting with 3D objects or representations (such as a 3D art museum or car engine); traveling to places of interest virtually; meeting with friends, family, colleagues, or medical professionals in a 3D space where they can see one another’s gestures and expressions (for example, an examining room with 3D scans, an office space, or a virtual version of the old family homestead); attending 3D virtual entertainment events; and shopping in 3D stores. Many Gen Z and Millennial respondents are more willing to explore this vision of the future, while older generations remain less sure (figure 10.1).

Generative AI is also poised to shape the future of digital life.44 As much as consumers love their devices, they can also be frustrated when managing them becomes a complex chore (see the chapter entitled Digital life often delivers daily benefits but can also fuel tech fatigue and well-being worries). To realize the full promise of connected devices, they likely need to become more intelligent, personalized, and easy to manage.

One area where generative AI may be able to alleviate some of the woes is with chatbots.45 Instead of learning the intricacies and idiosyncrasies of managing each digital device, imagine asking an AI chatbot for help—or instructing the chatbot to handle administrative tasks for you. Even better, imagine using natural language to ask a smart home system (such as a speaker or hub) to get all your devices working together seamlessly, or to get your home ready for a certain situation (for example: “we’re going on vacation tomorrow—adjust all systems and set up our security”). Generative AI may well bring greater personalization to digital devices and make interacting with them more collaborative and intuitive.46 In time, AI chatbots may even be capable of providing companionship, empathy, and trusted advice—lending more of a human element to heavily digital lives.47 AI could also help people spend less time on devices, tracking digital use and suggesting times and ways to step away from screens.

Some companies are already experimenting with bringing generative AI conversational capabilities into consumer devices, making voice assistants smarter.48 Others are working on bringing AI to home automation systems.49 From our survey, it appears that many consumers will welcome new kinds of collaboration with generative AI. Seventeen percent of our survey respondents have already experimented with generative AI or used it for projects, and of these, seven in 10 intend to keep using it. Again, we see distinctive differences by generation: Almost a third (31%) of Gen Z respondents report having used or experimented with generative AI, versus 20% of Millennials, and only 9% of older generations.

One important consideration around generative AI and consumer devices is likely to be how to ensure data privacy and security. As we noted in Data privacy and security worries are on the rise, while trust is down, only half of respondents feel that the benefits they get from online services outweigh their data privacy concerns. As AI-equipped devices collect information, tracking and learning user behaviors and preferences, concerns about data protection are likely to grow. Tech companies should commit to addressing these concerns from the outset, as part of their product and service design process. It’s conceivable that generative AI could be used to tailor privacy and data sharing to suit each person’s comfort level. But trust is often a negotiation: If the benefits are clear enough to users—and the risks low enough—they may be willing to share the kinds of data needed to power the next generation of intelligent devices.

We anticipate that consumers will continue seeking the optimal balance of ease, functionality, and connection, favoring devices and solutions that reduce headaches and deliver seamless experiences. Generative AI may have the potential to help users achieve a better balance between their physical and digital lives while empowering a new era of truly intelligent and personalized ecosystems of connected devices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}