Consumers embrace connected devices and virtual experiences for the long term

Our 2023 study finds that consumers are optimizing their tech usage to find the right balance between digital and physical worlds.

Jana Arbanas

Paul H. Silverglate

Susanne Hupfer

Jeff Loucks

Prashant Raman

Michael Steinhart

In this fourth edition of Deloitte’s Connected Consumer Study,1 we continue to report on US consumers’ digital lives. We researched their attitudes and behaviors around adopting connected consumer devices (technology, entertainment, and smart home), engaging in virtual experiences (remote work and learning, virtual health care visits), using wearables and smartphones to improve health and well-being, and enhancing home and mobile connectivity with 5G (see “About the survey” below).

In our 2021 Deloitte Connectivity and Mobile Trends report, we explored how many consumers, who had been plunged into a pandemic, adapted to their homes becoming headquarters for virtual working, learning, fitness, health care, shopping, socializing, and entertaining. They purchased new devices, upgraded their networks to improve connectivity, and made the best of a difficult situation. Our 2022 report found that, with fewer people working and learning from home, pressure on people, devices, and networks had diminished. Many of the acute challenges of virtual experiences and connectivity improved.2 Consumers were gaining mastery over their digital lives, optimizing the devices they use, and choosing to move forward with the virtual experiences that held the most value for them.

Our 2023 survey finds that, like a modern-day Goldilocks, consumers are struggling to find the right balance between their digital and physical lives. They’re continuing to streamline their household devices, and in the face of economic worries, they’re slowing device purchases. Many have embraced virtual experiences for the long term. At the same time, they’re trying to manage the drawbacks of too much tech—and where they can use tech companies’ help.

About the survey

To understand consumer attitudes toward “digital life,” the Deloitte Center for Technology, Media & Telecommunications surveyed 2,018 US consumers in Q2 2023. This is the fourth annual edition of the survey, which was previously known as Connectivity and Mobile Trends. Aspects of digital life that the survey covered include devices (technology, entertainment, smart home, smartphones), connectivity (home internet and mobile), virtual experiences (work, school, and health care), wearables (fitness trackers and smart watches), and challenges of managing it all. All data was weighted to the most recent US Census to arrive at a representative view of US consumers’ opinions and behaviors. To gain a more detailed understanding of various consumer groups, we also segmented respondents into generational groups defined by their birth year: Generation Z (1997–2009), Millennials (1983–1996), Generation X (1966–1982), Boomers (1947–1965), and Matures (1946 and prior).

Streamlining devices

It’s no surprise that consumers continue to rely heavily on digital devices. However, they’re also still streamlining the devices they own, aiming to maximize benefits while minimizing downsides. We found that, on average, each US household now has 13 device types and 21 devices—each down one from last year. This represents further pruning from the pandemic peak of 2021, when households had 25 devices on average.3 According to respondents, the top reasons for removing devices were that their functionality could now be handled by other devices, they were too costly, or they were too outdated.4

Mastering virtual experiences

Even as 2023 marks a continued return to in-person experiences, the pandemic has led to lasting changes in consumer behavior. People are choosing to carry on with virtual experiences that have worked well for them, including remote work and learning, and attending virtual medical appointments. They have continued to become more proficient at these, but here too, many are still striving to find just the right balance between their virtual and physical worlds.

As many employers urge or even require at least a partial return to offices,5 many workers have embraced hybrid working models (a mixture of in-office and remote work): More than half of our respondents worked at least partially remotely over the past year. Nearly a quarter of households have at least one member learning from home at least some of the time.6 Both remote workers and learners say that challenges of communication, culture, distractions, and stress have improved. When it comes to accessing health care, virtual visits have dipped from their pandemic highs, but satisfaction with such visits has increased steadily. Consumers continue to use wearables, but their focus has shifted from monitoring health metrics to tracking fitness.

Virtual experiences endure by choice, if no longer by necessity: At least two-thirds of those who engaged in virtual work or school over the past year would like remote or hybrid options in the future, and a majority of those who have had virtual health care visits said they prefer remote or hybrid options for certain kinds of health visits in the future, such as for therapy, counseling, and chronic conditions.

Managing the downsides of tech

Most respondents say their connected devices have a positive impact on their lives and help them build meaningful connections (fostering relationships with friends, family, or communities with shared interests). But too much time spent on devices can also stoke tech fatigue and concerns around well-being, data privacy, and security.

Since last year’s survey, consumers have grown more worried that their devices could open them up to security breaches and to having their movements or behaviors tracked. Moreover, households with greater numbers of devices report higher levels of well-being concerns and more data breaches. Indeed, people may be hitting a “device ceiling,” where they may not view adding more devices as bringing enough benefit to make up for the cost, security concerns, and maintenance challenges.

This suggests an area where tech companies can help consumers find the right balance. By making devices more affordable, simpler to secure and interoperate, and easier to set aside when one needs a break, tech providers can help consumers get the most out of their digital devices and experiences—without being overwhelmed.

There’s also a red-flag warning for tech companies: As consumers struggle to protect their data, their trust in tech has declined from 2021 levels. Consumers surveyed want more security and control over their data, but they’re less likely to feel that they’re getting it. Tech companies should double-down on efforts to shore up consumer trust in their devices and services—for example, by enhancing data security measures, communicating transparently about their data-handling practices, and giving consumers more choice over how their data is used.

Slowing device purchases

Facing the economic pressures of 2023—high inflation, risk of recession, and personal financial worries—consumers are tapping the brakes on device purchasing. According to Deloitte’s Global State of the Consumer Tracker, 38% of US consumers feel their financial situation worsened over the past year.7 In our survey, nearly half (49%) of our respondents said they have delayed device purchases in the past year, and 33% feel they can’t afford to buy the tech devices their household needs (up from 25% in 2022).

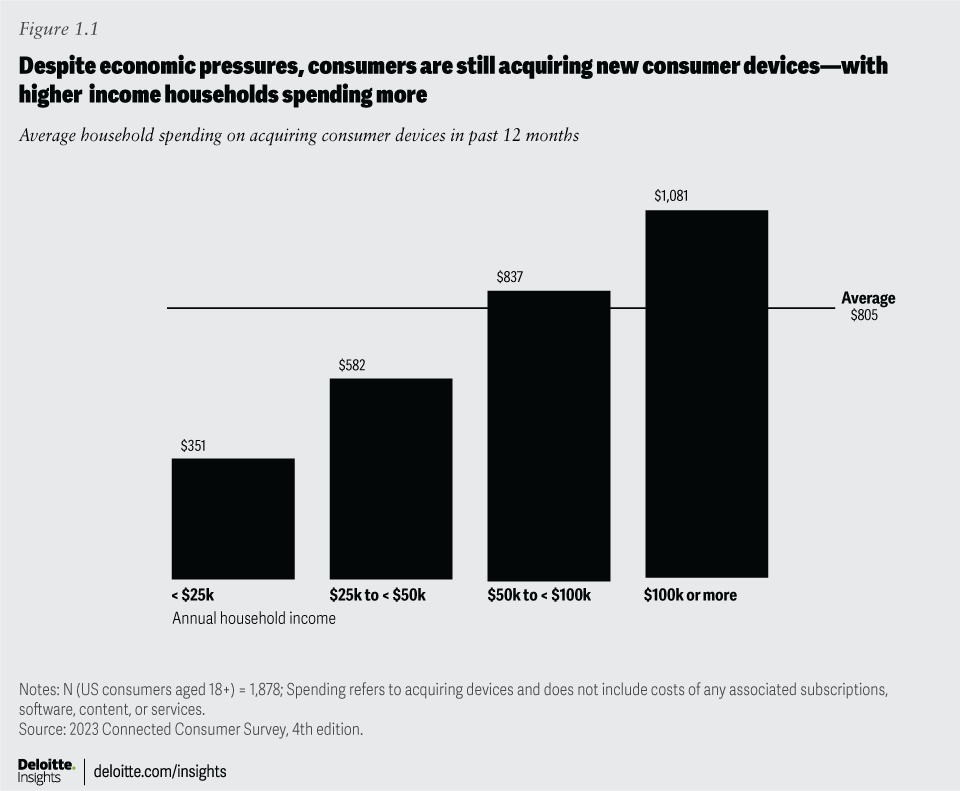

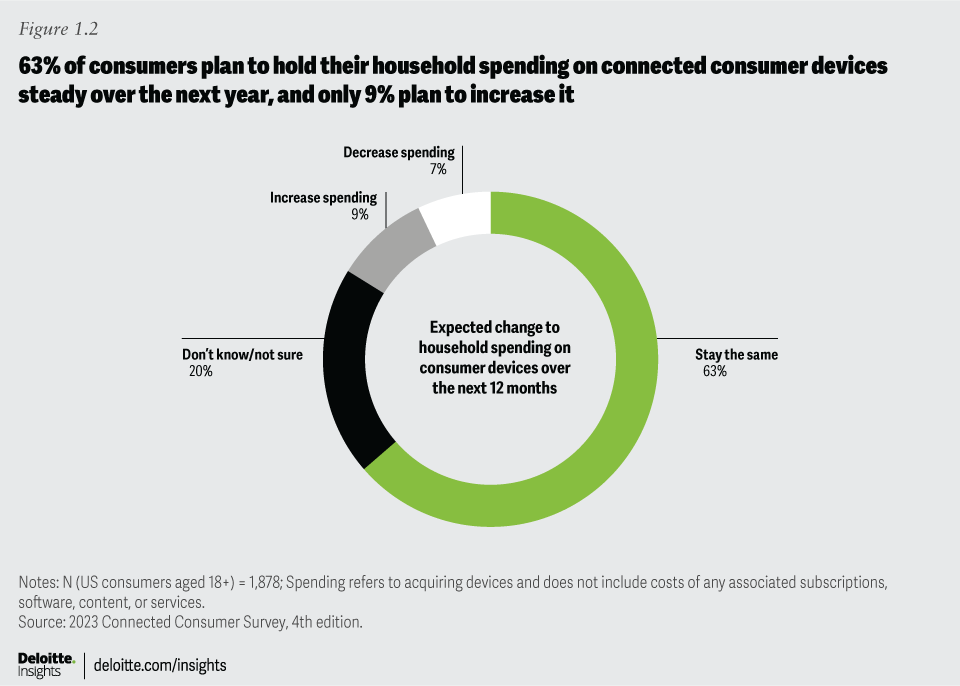

Consumers haven’t closed their wallets entirely, however: Over the past year, 32% have purchased one or two connected devices and 16% purchased three or more. Only three in 10 respondents have bought cheaper devices than they would have purchased ordinarily. Our research found that, on average, US households spent approximately US$800 on acquiring connected devices in the past year (figure 1.1). Looking toward the next 12 months, most consumers (63%) expect their device spending to remain steady, and 7% expect to reduce spending (figure 1.2).8

Since we sounded the alarm last year about privacy and security, screen overload, and tech fatigue,9 consumer discontent seems to have gotten worse. Technology companies, device makers, app developers, and service providers all have an opportunity—some might say an imperative—to help make consumers’ digital lives easier, safer, and more sustainable. If they can make devices easier to use and administer, aid users in controlling their screen time, make data security and privacy simpler to understand and manage, and give users more control over their own data, they may be able to build trust and differentiate themselves in a crowded market. If they fail to meet consumer needs, however, disruptors may step in to take advantage of the opportunity.

{kind=link}

{kind=link}