Optimizing digital ecosystems to create more value

Digital ecosystems have the potential for value creation beyond customers. How can strategy leaders take a broader perspective and capture more value from their investments?

Anne Kwan

Brian Campbell

Diana Kearns-Manolatos

Saurabh Bansode

Tanneasha Gordon

Traditionally, business ecosystems have often focused on enabling an organization’s unique capabilities, products, or offerings through a network of strategic partners, suppliers, and distributors. Digital ecosystems, comprised of the organization’s technology providers, have largely supported consumers and customer value.

Today, the lines between those ecosystems are blurring. As technology continues to drive rapid change, there’s a growing need for business partners to integrate into other organizations’ tech platforms. Uber’s digital ecosystem plays a role in connecting its partners, customers, and drivers, for example. Similarly, Airbnb orchestrates a marketplace which digitally connects hosts with their potential guests. More open and integrated data models are becoming the norm. Connected technologies like digital payments, application programming interfaces, edge computing, and blockchain create new value exchange opportunities.

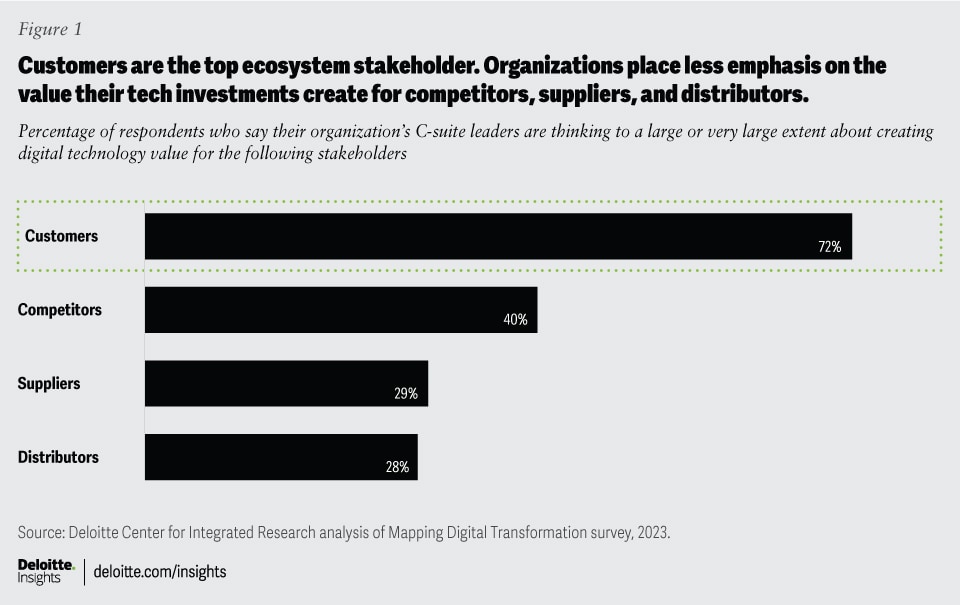

If organizations limit their digital ecosystems to creating value only for customers and end users, they may miss out on opportunities to realize additional value from their tech investments. According to an analysis of 1,600 global tech leaders’ responses to Deloitte Global’s 2023 Mapping Digital Transformation Value survey, most respondents’ organizations don’t appear to be assessing how their tech investments bring value to other groups like competitors, suppliers, or distributors (figure 1).

But those that do report realizing a financial advantage. This analysis revealed that organizations that said their digital ecosystems were focused to a “large” or “very large” extent on creating value not only for customers but also competitors, suppliers, and distributors reported 7 percentage points more enterprise value from digital transformation than the overall global average.1 While that might not seem like a lot, for an organization with US$1 billion in return on investment, that lift could add up to an additional US$70 million in enterprise gains.

What are these high-ecosystem-focused organizations doing differently, and how can leaders take a broader approach to their digital ecosystems to create and capture more of this value? This analysis highlights three key strategies for consideration: creating more data monetization opportunities, better managing ecosystem privacy and security challenges, and reducing technical complexity.2

Unlocking new data monetization strategies across the digital ecosystem

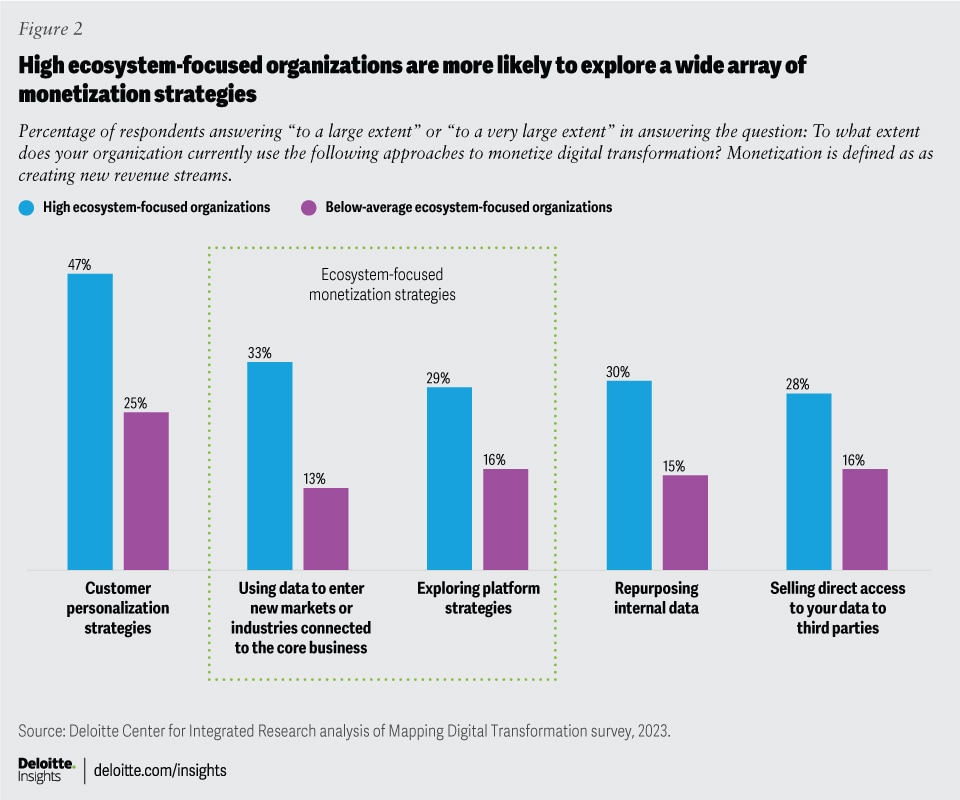

Customer personalization is the most popular strategy for data monetization among respondents overall, and high-ecosystem-focused organizations excel here by 20 percentage points. However, it’s the other strategies that truly set them apart. In the Deloitte Global survey, these organizations are 20 percentage points more likely to enter new markets or industries and 13 percentage points more likely to explore platform strategies, than those reporting a below-average ecosystem focus (figure 2).

Organizations looking to unlock new data monetization strategies could consider:

- Using data to enter new markets or industries connected to the core business. As leaders look for alternatives to traditional mergers and acquisitions, creative partnerships are often a critical path to new markets and industries.3 One health insurance company, for example, has worked beyond the insurance sector to push into the preventative health space while partnering with other global insurance providers.4

- Exploring platform strategies. Platform strategies draw on a common, connected infrastructure where partners can collaborate to create value.5 For example, The PayPal Commerce Platform extended the company’s digital payment infrastructure globally across over 100 currencies, simplifying compliance, reducing fraud, and generating new revenue streams.6 Roche’s aiR health research exchange created a patient, health care provider, and tech center of excellence for community-driven science.7 Finally, Walmart’s online marketplace allows the retailer to monetize supplier, distributor, and customer relationships through ad sales, financial services products, health care, and food, driving online sales.8 Each of these platform strategies could, in part, reflect the organization’s broader business ambitions.

These data monetization strategies can provide new opportunities to generate more value across the digital ecosystem. Organizations can create new revenue streams and diversify their offerings portfolio by partnering with technology providers and using connected technologies to unlock these opportunities.

Evolving operating models to address privacy and security risks

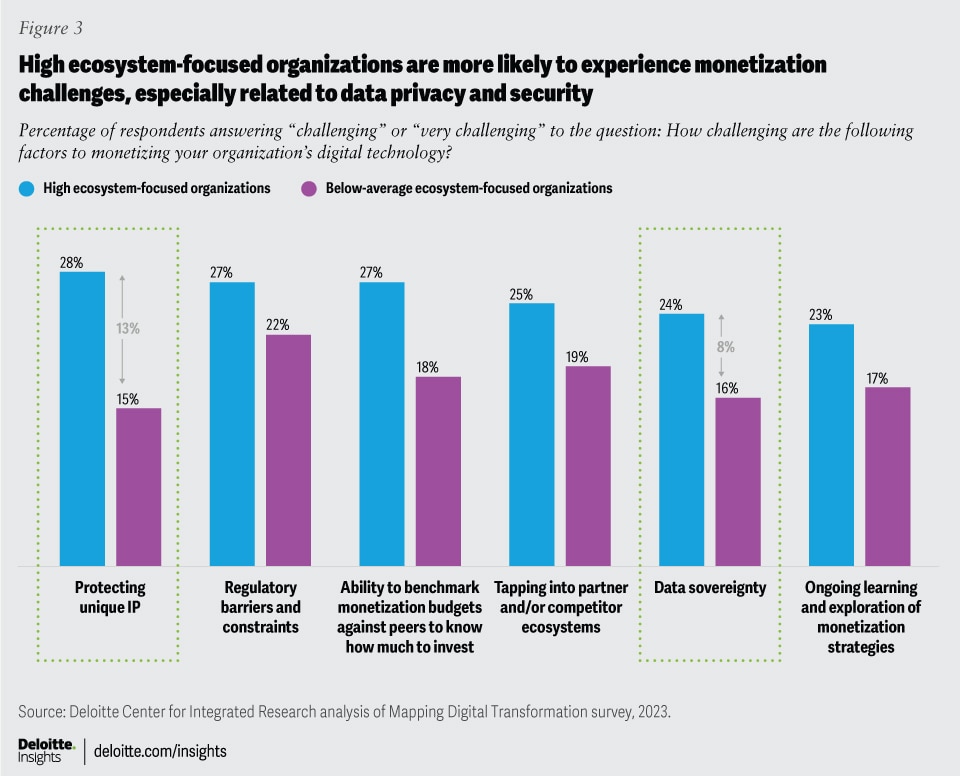

High ecosystem-focused organizations appear to be acutely aware of digital ecosystem risks such as data privacy, security, and accuracy (figure 3). Indeed, this group of respondents is almost twice as likely as organizations with below-average ecosystem focus to experience challenges related to protecting their unique intellectual property while pursuing data monetization strategies across their digital ecosystems.

Organizations can take steps toward overcoming privacy and security challenges by evolving operating models to include open innovation, orchestration, and co-opetition.

- Open innovation: Open innovation can allow organizations to harness ideas, technologies, and expertise from startups, academia, research institutions, partners, and customers, and is becoming more widely accepted. The approach goes one step beyond traditional collaboration to actively seek ideas from external parties as the central approach to innovation and often uses shared technology platforms to do so. For instance, Google assembled a dedicated network of hardware manufacturers, software developers, and telecom companies to develop the Android operating system.9 Procter & Gamble has a dedicated group of external innovators including scientists, engineers, and inventors that systematically contribute ideas to its portfolio of brands. Over the years, this approach has resulted in a nearly 60% increase in research and development productivity, and new products such as Olay Regenerist, Swiffer Dusters, the Crest SpinBrush, and the Mr. Clean Magic Eraser.10 And, Chinese multinational tech company, Baidu, assembled over 220 partners to codevelop its autonomous vehicle platform for ride-hailing, fast-tracking the digital product development in a way that would not have been possible through traditional collaboration methods.11

- Orchestration: An orchestrated operating model is one where organizations maintain tight control over who joins their platform. For example, Salesforce, the customer relationship management software company, closely controls which partners can join its AppExchange ecosystem, which offers more than 150,000 Salesforce customers access to over 4,600 apps.12 A critical aspect of orchestration is managing preferences and privacy to enable trust across the network.

- Co-opetition: Some organizations are making calculated decisions in collaboration with direct competitors. For example, Slack evolved from a chat software platform to a comprehensive workplace collaboration platform through strategic partnerships with would-be competitors, like Zoom and Asana.13 Here, the benefits may have outweighed the competitive risk because the gain is a new capability that advances the total addressable market for all parties. While early category leaders like BlackBerry Messenger may want to hold on to a first-mover advantage, closed technologies come with inherent risks, especially in fast-moving categories where the technology ecosystem is evolving, and competitors are willing to come together to gain market advantage.

Ultimately, the organization’s digital strategy and enterprise road map should dictate its approach to operating models. They can help define where, when, and how to invest in and manage value created from outside the organization across the ecosystem of customers.14 Over time, competitors may replicate the organization’s differentiated capabilities, which could erode value. Once these capabilities become widely replicated, they may neutralize any competitive advantage previously held by the organization. Therefore, it is important to continually monitor the market value of these capabilities and codevelop standards within the ecosystem to create and maintain competitive differentiation.

Reducing complexity across the digital ecosystem to help drive organizational resilience

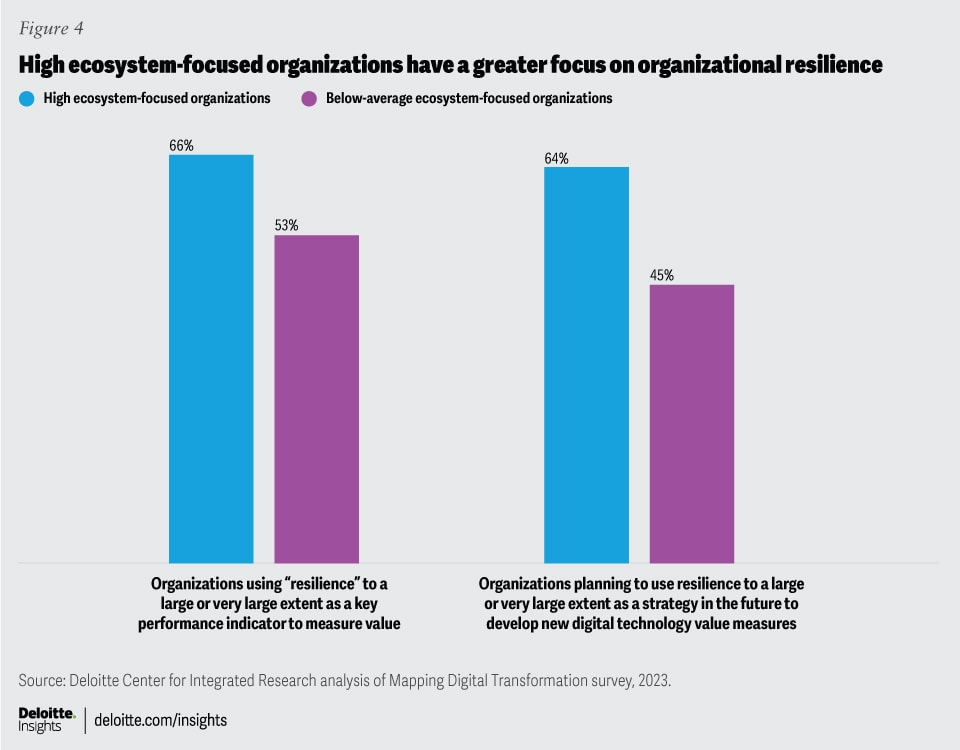

Many businesses are often challenged by the need to remain resilient as their digital ecosystems become increasingly interconnected and complex across numerous technology vendors, a lack of standardization, and multiple jurisdictions. Managing this complexity to maintain organizational resilience is essential to value optimization as duplicative and unnecessary vendors can result in negative network effects across the ecosystem and impact speed to market in a fast-paced-technology environment.15 High-ecosystem-focused organizations surveyed are more likely than low-ecosystem-focused counterparts to measure organizational resilience as an indicator of digital value and to believe that their organizations should develop new measures related to organizational resilience (figure 4).

Organizations often attempt to hedge their tech strategy risk by building a wide network of partners to avoid getting locked into a vendor relationship; however, this can create more complex digital ecosystems to manage. SAP’s digital platform, for example, includes more than 13,000 partners.16 The Wall Street Journal reports that Carhartt, a workwear manufacturer, is paying for 121 software subscriptions, a 105% increase over the last five years.17 Moreover, with generative artificial intelligence bringing a new class of niche vendors to the table, this kind of complexity can easily become unmanageable.18 According to a literature review on platform ecosystem governance, one-third of platform ecosystems fail due to poor management,19 reducing overall value for all of an organization’s stakeholders.20

Business capability and architecture mapping can highlight opportunities to streamline and secure technology systems with trust and competitive boundaries front and center.21 To streamline overlapping functions, organizations should work to identify duplicate business capabilities and domain architectures and evaluate partners based on their level of integration and strategic importance. This can help reduce overall costs, eliminate complexity, and streamline partner structures. While progress can be slow—it took Pegasystems, a workflow automation company, four years to successfully reduce its vendor list by 8%22—visibility into system interdependencies is essential for technology resilience in a fast-changing technology environment. Without starting this hard work, organizations risk piling on further complexity, technical debt, and third-party risk.

Creating value in the digital ecosystem requires collaboration

Organizations often need partners to thrive in the market. Chief strategy officers should be leading these conversations to better understand how value is created across the digital ecosystem and find opportunities to optimize data, work more strategically with technology partners, and reduce complexity. The entire C-suite will typically have a role to play in increasing the likelihood of success. For example, the chief data officer can shape the organization’s data strategy and gain buy-in from the chief executive officer, chief financial officer, and the board. The chief information officer and chief technology officer can lead the charge with technology vendors, designing more open architectures, tools, and communities. And the chief information security officer can enable data security while reducing complexity to facilitate relationship building and trust across the digital ecosystem. This all requires making calculated decisions about technology strategies across the ecosystem to help deepen strategic relationships and manage value.

Methodology

The research is based on findings from executive interviews, literature review, and data analysis from “Mapping digital transformation value.” In February 2023, Deloitte Global surveyed 1,600 global business and technology leaders across 14 countries and six industries: consumer; energy, resources, and industrials; financial services; government and public services; life sciences and health care; and technology, media, and telecommunications.

We developed an ecosystem maturity index based on the extent the respondents said they measure the value their investments bring to these ecosystem participants: customers, competitors, suppliers, and distributors. We then scored based on the Likert scale mean across these responses to classify the Deloitte Global respondents into two groups: “High-ecosystem-focused organizations” had a mean above 3.33, whereas “below-average-ecosystem-focused organizations” had a mean below 3.33.

{kind=link}

{kind=link}

{kind=link}

{kind=link}