Digital payment technology for merchants has been saved

Perspectives

Digital payment technology for merchants

How QR codes will impact the future of payments

When it comes to digital payment technology, quick response (QR) codes are at the top of the class. As consumers have grown increasingly comfortable with QR codes, more companies are adopting them for their payment systems.

Using QR codes for digital payments

Digital payment methods rapidly gained popularity since 2020—a trend that’s likely to continue. More and more merchants are choosing to offer customers a QR code payment option to help make payments faster, safer, and more accessible. In this report, we explore the choices available to merchants and important considerations to successfully implement QR code payments.

QR code payments

Enhancing the customer experience with payment technology

Merchants across a wide array of industries can use QR codes for payments—and would benefit from doing so. With a QR code system set up, businesses new to the market can start accepting payments quickly, while more established merchants can offer it as an additional payment acceptance option to improve the overall experience of the customer checkout journey.

Aspects of a contactless digital payment experience, including faster payments and accessible functionality, are important functions that benefit customers and merchants alike. Lower setup and transaction costs help merchants pass savings along to consumers. Plus, using a digital payment option eliminates the need for cards or money to change hands.

QR code payments in a merchant environment

Whether a merchant chooses to use QR code payments affects all parties involved. Currently, merchants have two choices to consider when implementing QR payments: they can choose a customer-presented code, or they can opt for a merchant-presented code.

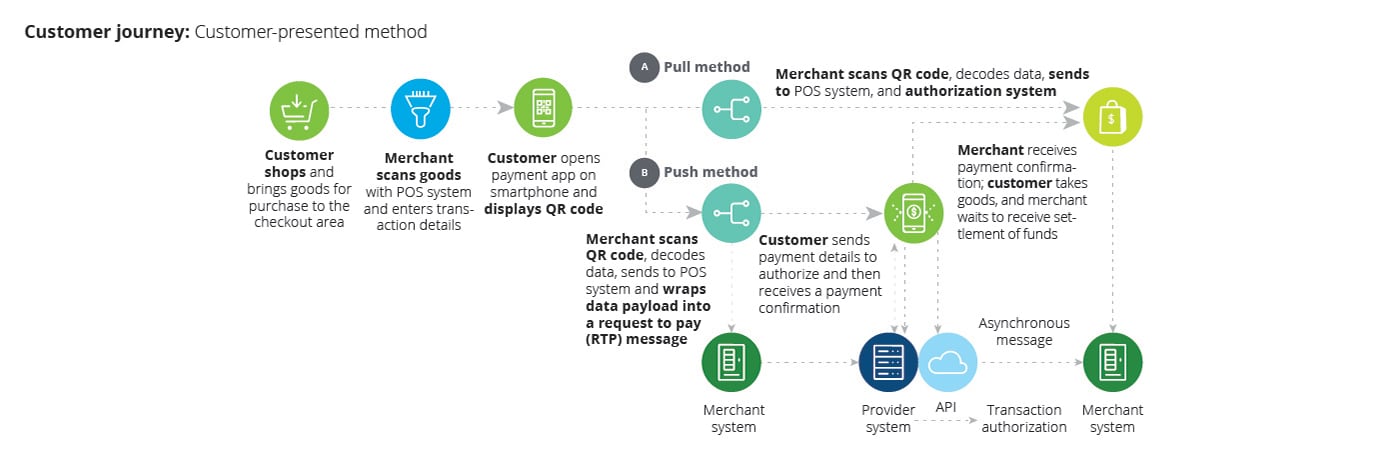

A customer-presented code requires customers to present a QR code for the merchant to scan. Merchants can choose to build their own app for a customer-presented method or choose to accept third-party apps, such as Zelle, Venmo, or PayPal. Loyalty and payments can be combined, just as in the merchant-presented method, allowing for quick and easy checkout.

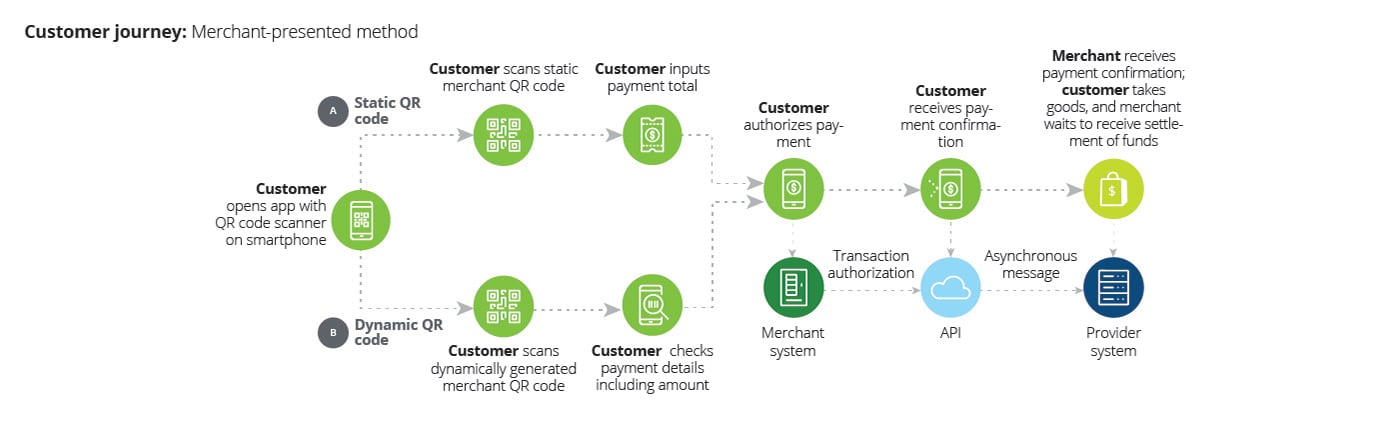

On the other hand, a merchant’s point of sale (POS) system produces a QR code at a point of interest for the customer to scan with a mobile device. In most cases, the customer is able to manually input their payment details upon first use. The merchant-presented method allows for newer and/or smaller merchants to begin accepting electronic payments sooner. Merchants can also opt to display a single static code for consumers to scan, eliminating the need for complex POS setup.

Whether merchant- or customer-presented, consumers will continue to look for ease of use, simplicity, and security in making payments.

Implementing digital payments

While enabling QR code payments offers many benefits, merchants need to evaluate key considerations, including impacts across the business and to the customer’s payment journey and cybersecurity of the payment acceptance ecosystem.

When deciding on and implementing a payment technology, it’s important to consider a few different things. First, QR code payments can be enabled by partnering with third-party providers such as Venmo and PayPal, or by developing in-house systems. Businesses will need to align their customers’ payment journey with the objectives of the checkout experience and the business need.

Additionally, security considerations and controls need to be implemented based on how merchants choose to structure their payment system. QR code payments often require smartphone cameras, so reliance on an additional technology component can introduce new security vulnerabilities.

Choosing your payment technology

Overall, QR code payments are, and will continue to be, popular with consumers. They offer considerable advantages to both merchants and consumers, including increased convenience, accessibility, and speed. However, it’s important for merchants to consider their customer and business needs before adding a new payment form factor.

Recommendations

Branching Out: A Retail Banking Podcast Series

Join us as we dive into conversations with financial services leaders from across the industry in a podcast series from Deloitte’s retail banking practice.

End of cheap deposits

Implications for banks’ deposit betas, asset growth, and funding